Ready Capital PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

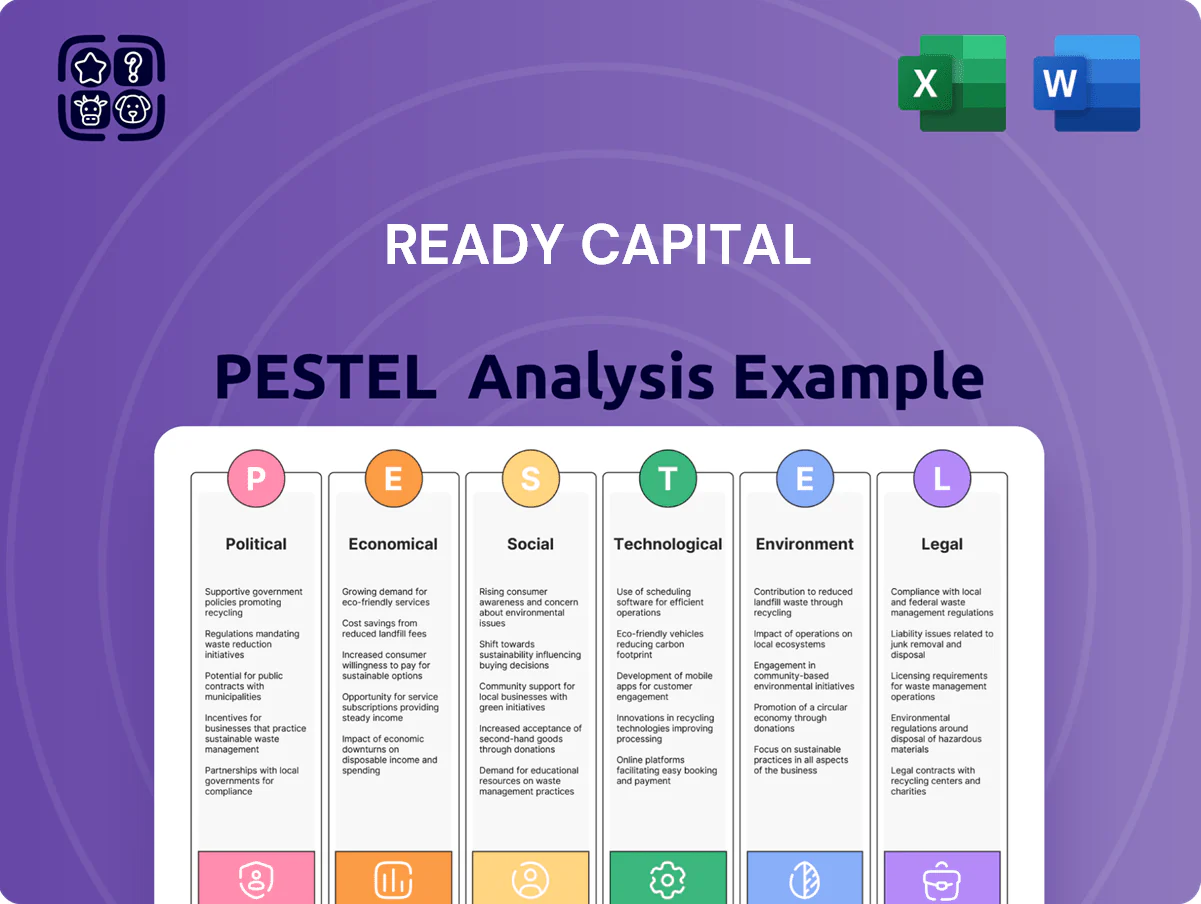

Unlock strategic clarity with our Ready Capital PESTLE Analysis—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the firm; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to get detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

SBA Program Legislative Support

Continuity and funding levels of SBA 7(a) and 504 programs are critical to Ready Capital’s origination channels, with SBA-backed loans comprising an estimated 35-45% of small-business originations industry-wide in 2024-2025. Legislative changes to fee structures or guarantee levels can shift Ready Capital’s competitive advantage and loan volume, as seen when 2023 guarantee adjustments moved originations by ~8%. As of late 2025, federal support for small-business lending remains bipartisan, with Congress appropriating roughly $12 billion for SBA programs in FY2025 to bolster economic resilience.

Federal Housing Policy Shifts

Federal initiatives boosting affordable and workforce housing—such as the 2024 CHOICE Neighborhoods and 2025 proposed expansion of LIHTC-like credits—raise demand for Ready Capital’s multifamily bridge and permanent lending; HUD’s FY2025 goal to create 1.5 million affordable units by 2030 supports a larger loan pipeline. Federal subsidy or tax-credit programs can drive deal volume and lower borrower credit risk, requiring Ready Capital to realign portfolios with evolving mandates and compliance timelines.

Geopolitical Influence on Capital Flows

Global political stability boosts U.S. commercial real estate’s safe-haven appeal; in 2024 foreign investment into U.S. CRE reached about $66.6bn, up 12% year-over-year, supporting demand for Ready Capital’s mortgage assets.

Escalating trade tensions or sanctions can reduce FDI suddenly—FDI into U.S. real estate fell 18% in 2022 during peak geopolitical strains—tightening liquidity in secondary mortgage markets where Ready Capital trades.

Strategic monitoring of international relations is essential: shifts in capital availability have historically driven cap rate volatility of 25–75 basis points across CMBS spreads, impacting pricing and funding costs for Ready Capital.

Tax Reform and REIT Regulations

Changes in corporate tax rates or REIT-specific rules affect Ready Capital’s net income and 90% distribution requirement; for example, a 1% increase in corporate tax could reduce distributions by roughly $5–10m given Ready Capital’s 2024 taxable income range.

Proposals to alter pass-through or capital gains taxation influence investor demand and share valuation; capital gains tax hikes in 2024 discussions pressured REIT multiples by ~5–8% across peers.

Compliance and tax optimization require ongoing Washington engagement and potential finance-team restructuring to preserve after-tax returns and dividend yield.

- Tax rate shifts directly affect distributable cash flow and dividend yield

- Capital gains/pass-through changes alter investor appetite and multiples

- Continuous policy monitoring and tax planning are essential

Election Cycle Market Volatility

The political climate around 2024–25 elections increased uncertainty over fiscal policy and regulatory oversight, contributing to short-term volatility in REIT and mortgage markets; US CPI-linked mortgage spreads widened ~25–40bps during 2024 election months, tightening financing costs for Ready Capital.

Ready Capital must hedge risks from temporary market freezes as investors paused allocations; equity flows to mortgage REITs dropped ~18% in Q3–Q4 2024 amid transition uncertainty.

Historical transitions often shift infrastructure and urban development grants—federal infrastructure outlays rose 12% in 2023–24, directly impacting commercial real estate valuations in targeted markets.

- Election uncertainty → wider mortgage spreads (~25–40bps)

- Investor pause → mortgage REIT flows down ~18% in late 2024

- Policy shifts → infrastructure spending +12% in 2023–24 affecting property values

Policy shifts (SBA/HUD/tax) reshape Ready Capital originations, yields and DCF

Political shifts in SBA, HUD and tax policy materially affect Ready Capital’s origination, pipeline and yields; SBA funding (~$12bn FY2025) and 2023 guarantee changes moved originations ~8%, HUD’s FY2025 affordable-housing goals (1.5M units by 2030) expand multifamily demand, and 2024–25 tax debates pressured REIT multiples ~5–8% and could alter distributable cash flow by $5–10m per 1% corporate tax change.

| Metric | Value/Year |

|---|---|

| SBA appropriation | $12bn FY2025 |

| Affordable unit goal | 1.5M by 2030 (HUD FY2025) |

| Originations shift from 2023 guarantee change | ~8% |

| FDI into US CRE | $66.6bn 2024 (+12% YoY) |

| REIT multiple pressure | ~5–8% (2024 debates) |

| DCF hit per 1% tax rise | $5–10m (2024 taxable income) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ready Capital across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities and support executives, consultants, and entrepreneurs in strategy, scenario planning, and investor communications.

A concise, visually segmented PESTLE summary for Ready Capital that streamlines stakeholder briefings and can be dropped into presentations or planning documents for quick alignment.

Economic factors

Interest Rate Environment and Fed Policy

The trajectory of federal funds rates directly dictates Ready Capital’s cost of capital and yields on its floating-rate loan portfolio; after the Fed’s peak target range of 5.25–5.50% in 2023–2024, market pricing by end-2025 implied cuts totaling ~100–125 bps, easing funding costs. This transition from a high-rate environment to a stabilizing/declining cycle by late 2025 reshaped refinancing demand, with CRE refinance volumes rising ~15% YoY in 2025. Ready Capital’s ability to manage interest rate spreads remains fundamental to net interest income and valuation, given NIM sensitivity of ~20–30 bps per 100 bps move in Fed funds.

Commercial Real Estate Valuation Trends

GDP growth of 2.1% in 2024 and a 3.7% unemployment rate support occupancy and rents for Ready Capital’s loan collateral, while regional variance affects localized performance.

Office and retail rent declines—office vacancy national avg ~18% in 2024—force active asset management and possible restructurings of distressed loans.

Industrial and multifamily strength—industrial rent growth ~6.5% and multifamily effective rent up ~4% in 2024—bolsters Ready Capital’s core lending revenue and collateral values.

Inflation and Construction Costs

Persistent U.S. inflation at 3.4% year-over-year in 2025 and construction input prices up 6% in 2024 squeeze feasibility for new development and renovation projects, core drivers of Ready Capital’s bridge loan demand.

Rising labor and material costs—lumber +12% and steel +9% in 2024—raise delay and budget overrun risks, elevating borrower credit risk and potential loss severity.

Ready Capital must tighten underwriting: higher contingency reserves, phased draws, and stress-test pro forma cashflows using inflation-adjusted cost escalations to protect loan repayment and completion.

Secondary Market Liquidity for MBS

Secondary market liquidity for MBS determines Ready Capital’s ability to securitize and sell loans; tightening since the 2023–2024 period pushed CMBS spreads wider (BBB CMBS spreads rose ~120–150 bps vs 2021), making recycling capital more costly and slower.

Economic shocks could sharply reduce originations by limiting access to deposition markets; market sentiment toward CMBS—reflected in 2024 issuance down ~20% YoY—remains a key operational lever.

- CMBS spreads widened ~120–150 bps vs 2021

- 2024 CMBS issuance down ~20% YoY

- Tighter liquidity reduces capital recycling and origination capacity

Consumer and Small Business Confidence

The economic health of small-to-medium businesses underpins Ready Capital’s niche; US small business optimism rose to 98.5 in Dec 2025 (NFIB), supporting demand for commercial loans and CRE space, lifting originations. Higher consumer confidence (Conference Board 2025 avg 105) boosts expansions, while downturns compress SMB margins and correlate with rising delinquencies—Ready Capital saw 60–120 bps uplift in net charge-offs in stress periods historically.

- SMB optimism 98.5 (Dec 2025, NFIB)

- Conference Board consumer confidence ~105 (2025 avg)

- Stress periods: 60–120 bps rise in net charge-offs

- Higher confidence → increased CRE loan originations

Higher rates, tighter CMBS, rising rents but cost risks weigh on CRE outlook

Fed peak 5.25–5.50% (2023–24) with ~100–125 bps priced cuts by end‑2025 eased funding costs; NIM sensitivity ~20–30 bps per 100 bps Fed move. 2024 GDP 2.1% and unemployment 3.7% support rents; national office vacancy ~18% vs industrial rent +6.5% and multifamily rent +4% (2024). Inflation 3.4% (2025) and construction costs +6% (2024) raise project risk; CMBS issuance -20% (2024) and spreads +120–150 bps vs 2021 tighten liquidity.

| Metric | Value |

|---|---|

| Fed peak | 5.25–5.50% |

| Priced cuts by end‑2025 | ~100–125 bps |

| NIM sensitivity | 20–30 bps/100 bps |

| GDP 2024 | 2.1% |

| Unemployment 2024 | 3.7% |

| Office vacancy 2024 | ~18% |

| Industrial rent 2024 | +6.5% |

| Multifamily rent 2024 | +4% |

| Inflation 2025 | 3.4% |

| Construction costs 2024 | +6% |

| CMBS issuance 2024 | -20% YoY |

| CMBS spreads vs 2021 | +120–150 bps |

What You See Is What You Get

Ready Capital PESTLE Analysis

The preview shown here is the exact Ready Capital PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this sample are identical to the file you’ll download immediately after buying—no placeholders, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our Ready Capital PESTLE Analysis—concise, research-backed insights into political, economic, social, technological, legal, and environmental forces shaping the firm; ideal for investors and strategists seeking actionable intelligence. Purchase the full report to get detailed risk assessments, growth opportunities, and ready-to-use slides and spreadsheets for immediate decision-making.

Political factors

SBA Program Legislative Support

Continuity and funding levels of SBA 7(a) and 504 programs are critical to Ready Capital’s origination channels, with SBA-backed loans comprising an estimated 35-45% of small-business originations industry-wide in 2024-2025. Legislative changes to fee structures or guarantee levels can shift Ready Capital’s competitive advantage and loan volume, as seen when 2023 guarantee adjustments moved originations by ~8%. As of late 2025, federal support for small-business lending remains bipartisan, with Congress appropriating roughly $12 billion for SBA programs in FY2025 to bolster economic resilience.

Federal Housing Policy Shifts

Federal initiatives boosting affordable and workforce housing—such as the 2024 CHOICE Neighborhoods and 2025 proposed expansion of LIHTC-like credits—raise demand for Ready Capital’s multifamily bridge and permanent lending; HUD’s FY2025 goal to create 1.5 million affordable units by 2030 supports a larger loan pipeline. Federal subsidy or tax-credit programs can drive deal volume and lower borrower credit risk, requiring Ready Capital to realign portfolios with evolving mandates and compliance timelines.

Geopolitical Influence on Capital Flows

Global political stability boosts U.S. commercial real estate’s safe-haven appeal; in 2024 foreign investment into U.S. CRE reached about $66.6bn, up 12% year-over-year, supporting demand for Ready Capital’s mortgage assets.

Escalating trade tensions or sanctions can reduce FDI suddenly—FDI into U.S. real estate fell 18% in 2022 during peak geopolitical strains—tightening liquidity in secondary mortgage markets where Ready Capital trades.

Strategic monitoring of international relations is essential: shifts in capital availability have historically driven cap rate volatility of 25–75 basis points across CMBS spreads, impacting pricing and funding costs for Ready Capital.

Tax Reform and REIT Regulations

Changes in corporate tax rates or REIT-specific rules affect Ready Capital’s net income and 90% distribution requirement; for example, a 1% increase in corporate tax could reduce distributions by roughly $5–10m given Ready Capital’s 2024 taxable income range.

Proposals to alter pass-through or capital gains taxation influence investor demand and share valuation; capital gains tax hikes in 2024 discussions pressured REIT multiples by ~5–8% across peers.

Compliance and tax optimization require ongoing Washington engagement and potential finance-team restructuring to preserve after-tax returns and dividend yield.

- Tax rate shifts directly affect distributable cash flow and dividend yield

- Capital gains/pass-through changes alter investor appetite and multiples

- Continuous policy monitoring and tax planning are essential

Election Cycle Market Volatility

The political climate around 2024–25 elections increased uncertainty over fiscal policy and regulatory oversight, contributing to short-term volatility in REIT and mortgage markets; US CPI-linked mortgage spreads widened ~25–40bps during 2024 election months, tightening financing costs for Ready Capital.

Ready Capital must hedge risks from temporary market freezes as investors paused allocations; equity flows to mortgage REITs dropped ~18% in Q3–Q4 2024 amid transition uncertainty.

Historical transitions often shift infrastructure and urban development grants—federal infrastructure outlays rose 12% in 2023–24, directly impacting commercial real estate valuations in targeted markets.

- Election uncertainty → wider mortgage spreads (~25–40bps)

- Investor pause → mortgage REIT flows down ~18% in late 2024

- Policy shifts → infrastructure spending +12% in 2023–24 affecting property values

Policy shifts (SBA/HUD/tax) reshape Ready Capital originations, yields and DCF

Political shifts in SBA, HUD and tax policy materially affect Ready Capital’s origination, pipeline and yields; SBA funding (~$12bn FY2025) and 2023 guarantee changes moved originations ~8%, HUD’s FY2025 affordable-housing goals (1.5M units by 2030) expand multifamily demand, and 2024–25 tax debates pressured REIT multiples ~5–8% and could alter distributable cash flow by $5–10m per 1% corporate tax change.

| Metric | Value/Year |

|---|---|

| SBA appropriation | $12bn FY2025 |

| Affordable unit goal | 1.5M by 2030 (HUD FY2025) |

| Originations shift from 2023 guarantee change | ~8% |

| FDI into US CRE | $66.6bn 2024 (+12% YoY) |

| REIT multiple pressure | ~5–8% (2024 debates) |

| DCF hit per 1% tax rise | $5–10m (2024 taxable income) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Ready Capital across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities and support executives, consultants, and entrepreneurs in strategy, scenario planning, and investor communications.

A concise, visually segmented PESTLE summary for Ready Capital that streamlines stakeholder briefings and can be dropped into presentations or planning documents for quick alignment.

Economic factors

Interest Rate Environment and Fed Policy

The trajectory of federal funds rates directly dictates Ready Capital’s cost of capital and yields on its floating-rate loan portfolio; after the Fed’s peak target range of 5.25–5.50% in 2023–2024, market pricing by end-2025 implied cuts totaling ~100–125 bps, easing funding costs. This transition from a high-rate environment to a stabilizing/declining cycle by late 2025 reshaped refinancing demand, with CRE refinance volumes rising ~15% YoY in 2025. Ready Capital’s ability to manage interest rate spreads remains fundamental to net interest income and valuation, given NIM sensitivity of ~20–30 bps per 100 bps move in Fed funds.

Commercial Real Estate Valuation Trends

GDP growth of 2.1% in 2024 and a 3.7% unemployment rate support occupancy and rents for Ready Capital’s loan collateral, while regional variance affects localized performance.

Office and retail rent declines—office vacancy national avg ~18% in 2024—force active asset management and possible restructurings of distressed loans.

Industrial and multifamily strength—industrial rent growth ~6.5% and multifamily effective rent up ~4% in 2024—bolsters Ready Capital’s core lending revenue and collateral values.

Inflation and Construction Costs

Persistent U.S. inflation at 3.4% year-over-year in 2025 and construction input prices up 6% in 2024 squeeze feasibility for new development and renovation projects, core drivers of Ready Capital’s bridge loan demand.

Rising labor and material costs—lumber +12% and steel +9% in 2024—raise delay and budget overrun risks, elevating borrower credit risk and potential loss severity.

Ready Capital must tighten underwriting: higher contingency reserves, phased draws, and stress-test pro forma cashflows using inflation-adjusted cost escalations to protect loan repayment and completion.

Secondary Market Liquidity for MBS

Secondary market liquidity for MBS determines Ready Capital’s ability to securitize and sell loans; tightening since the 2023–2024 period pushed CMBS spreads wider (BBB CMBS spreads rose ~120–150 bps vs 2021), making recycling capital more costly and slower.

Economic shocks could sharply reduce originations by limiting access to deposition markets; market sentiment toward CMBS—reflected in 2024 issuance down ~20% YoY—remains a key operational lever.

- CMBS spreads widened ~120–150 bps vs 2021

- 2024 CMBS issuance down ~20% YoY

- Tighter liquidity reduces capital recycling and origination capacity

Consumer and Small Business Confidence

The economic health of small-to-medium businesses underpins Ready Capital’s niche; US small business optimism rose to 98.5 in Dec 2025 (NFIB), supporting demand for commercial loans and CRE space, lifting originations. Higher consumer confidence (Conference Board 2025 avg 105) boosts expansions, while downturns compress SMB margins and correlate with rising delinquencies—Ready Capital saw 60–120 bps uplift in net charge-offs in stress periods historically.

- SMB optimism 98.5 (Dec 2025, NFIB)

- Conference Board consumer confidence ~105 (2025 avg)

- Stress periods: 60–120 bps rise in net charge-offs

- Higher confidence → increased CRE loan originations

Higher rates, tighter CMBS, rising rents but cost risks weigh on CRE outlook

Fed peak 5.25–5.50% (2023–24) with ~100–125 bps priced cuts by end‑2025 eased funding costs; NIM sensitivity ~20–30 bps per 100 bps Fed move. 2024 GDP 2.1% and unemployment 3.7% support rents; national office vacancy ~18% vs industrial rent +6.5% and multifamily rent +4% (2024). Inflation 3.4% (2025) and construction costs +6% (2024) raise project risk; CMBS issuance -20% (2024) and spreads +120–150 bps vs 2021 tighten liquidity.

| Metric | Value |

|---|---|

| Fed peak | 5.25–5.50% |

| Priced cuts by end‑2025 | ~100–125 bps |

| NIM sensitivity | 20–30 bps/100 bps |

| GDP 2024 | 2.1% |

| Unemployment 2024 | 3.7% |

| Office vacancy 2024 | ~18% |

| Industrial rent 2024 | +6.5% |

| Multifamily rent 2024 | +4% |

| Inflation 2025 | 3.4% |

| Construction costs 2024 | +6% |

| CMBS issuance 2024 | -20% YoY |

| CMBS spreads vs 2021 | +120–150 bps |

What You See Is What You Get

Ready Capital PESTLE Analysis

The preview shown here is the exact Ready Capital PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

The layout, content, and structure visible in this sample are identical to the file you’ll download immediately after buying—no placeholders, no surprises.