RealD Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

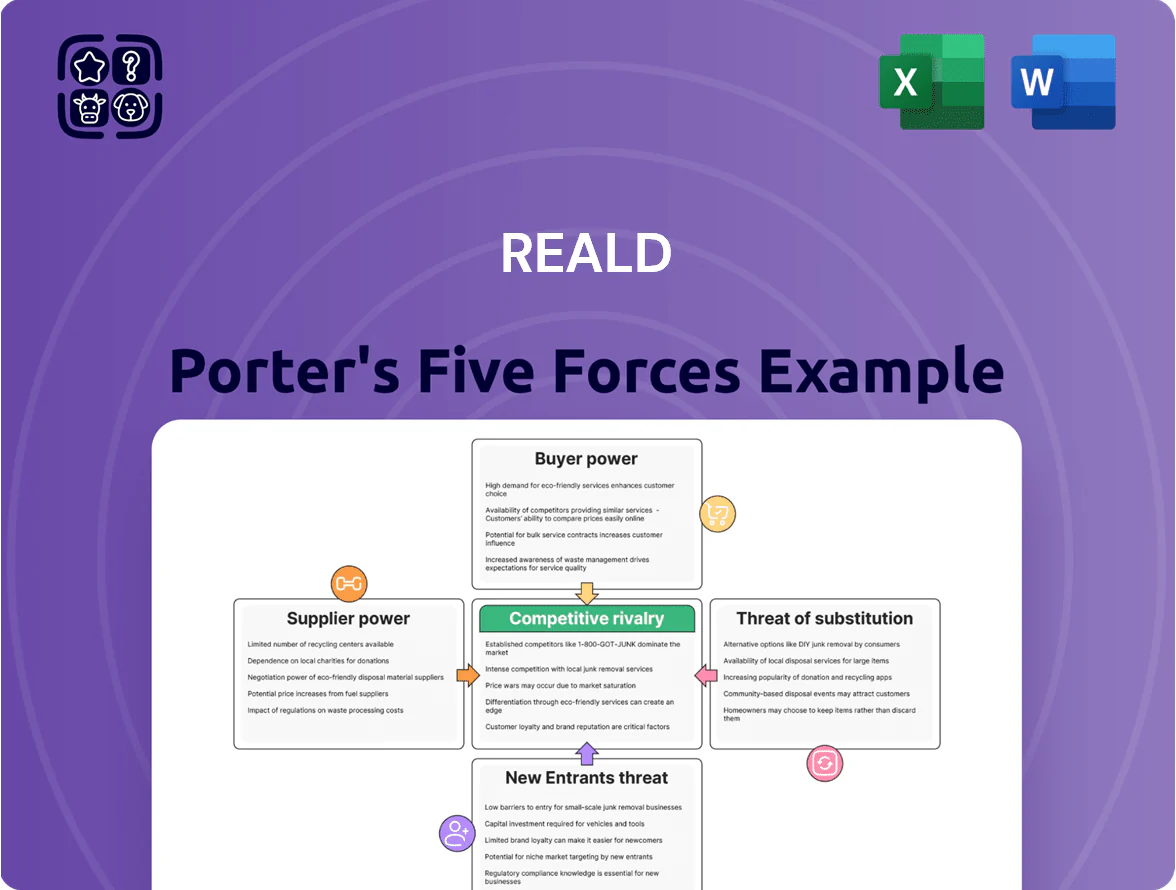

RealD operates in a niche yet tech-driven entertainment market where supplier leverage, buyer expectations, and substitute technologies shape profitability; competitive rivalry is moderate but innovation cycles and licensing dynamics raise strategic risk.

Suppliers Bargaining Power

Specialized Optical Component Manufacturers

RealD depends on a few high-precision manufacturers for patented circular polarizing filters and silver-screen coatings; these suppliers run specialized fabs not easily replaced, so supplier switching is costly and slow.

Even though RealD owns the IP, suppliers control critical processes, giving them moderate leverage; industry reports (2024) show lead-time variability of 8–20 weeks and supplier price uplifts of 5–12% for advanced optical materials.

Manufacturing of Passive 3D Glasses

The manufacturing of passive 3D glasses is outsourced to large-scale Asian manufacturers; suppliers exert moderate power via volume control and raw-material swings—PET lenses and metal hinges—affecting margins on millions of units (RealD shipped ~40 million glasses in 2024). RealD limits risk by keeping a diversified supplier base and price-negotiation leverage, so supplier power is present but contained.

Digital Projector OEM Partnerships

Digital projector OEMs like Barco, Christie, and Sony exert strong supplier power: RealD must integrate with their projectors for exhibitor adoption, and in 2024 these three supplied roughly 70% of global cinema projectors (Source: IHS Markit).

Any OEM shift—eg favoring alternate 3D standards or laser modules—could cut RealD channel reach quickly; a single major OEM contract change can affect access to tens of thousands of screens worldwide.

Intellectual Property and R&D Talent

The pool of stereoscopic imaging and light-science engineers is small; industry reports show global AR/VR optics talent shortages at ~30% in 2024, raising hiring costs and tail salaries by 15–25%.

Replacing key researchers risks losing proprietary know-how to tech giants; RealD’s R&D spend must stay high—RealD reported R&D-driven capex and payroll representing ~12% of revenue in 2023—to keep its pipeline ahead.

- Specialist talent scarce—~30% shortage (2024)

- Retention raises salaries 15–25%

- Key-person risk vs tech giants

- R&D/headcount ~12% of revenue (RealD 2023)

Logistics and Distribution Partners

Shipping specialized equipment and millions of 3D glasses to 3,500+ global locations needs a robust logistics network; providers raised rates as fuel and freight volatility surged in 2025, with global airfreight costs up ~22% year-over-year and container rates spiking intermittently.

Those providers hold bargaining power: RealD faced decisions to absorb higher logistics costs—compressing margins—or pass them to exhibitors, which risks slowing 3D system adoption and lowering annual deployment growth below prior ~5% targets.

Supplier squeeze: 70% OEM dominance, long lead times, rising costs & talent gaps

Suppliers hold moderate-to-high bargaining power: specialized optical fabs and projector OEMs (Barco, Christie, Sony ~70% market share 2024) create switching costs and channel dependence; lead times 8–20 weeks and supplier price uplifts 5–12% (2024) squeeze margins; logistics inflation (airfreight +22% 2025) and talent shortages (~30% gap, salaries +15–25%) add cost pressure.

| Metric | Value |

|---|---|

| Projector OEM share (2024) | Barco/Christie/Sony ~70% |

| Lead-time range (2024) | 8–20 weeks |

| Supplier price uplift (2024) | 5–12% |

| Glasses shipped (2024) | ~40M units |

| Airfreight change (2025) | +22% |

| Talent shortage (2024) | ~30% |

What is included in the product

Tailored Porter's Five Forces overview for RealD that uncovers competitive pressures, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect market share and pricing.

A concise RealD Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for swift decision-making and slide-ready summaries.

Customers Bargaining Power

Consolidation of Global Cinema Circuits

The bargaining power of buyers is high: in 2024 the top five global exhibitors (AMC, Cinemark, Cineworld, Wanda, and Cinemas Unidos) controlled roughly 38% of worldwide screens, letting them demand lower licensing fees or richer revenue shares from RealD.

If a major chain (AMC operates ~9,000 screens globally in 2024) flips to a rival 3D tech, RealD would lose a material share of box-office 3D venues and annual licensing revenue—likely mid-to-high single-digit percent of total revenue based on 2023-24 disclosures.

Movie Studio Content Pipeline

RealD’s value hinges on studios’ 3D slate: in 2024 Disney and Warner Bros released fewer than 10 major studio 3D titles combined, down ~40% vs 2019, so a lower 3D output cuts RealD’s addressable market and licensing revenue; studios’ format choices (2D, IMAX, Dolby Cinema) and box-office ROI make them powerful indirect customers who effectively decide RealD’s demand via creative and budget choices.

Consumer Preference Shifts

Moviegoers set pricing power: by end-2025 average willingness-to-pay for 3D premiums fell ~8% vs 2019, and 2D HFR (high-frame-rate) releases lifted attendance in some markets by 4–6%, forcing RealD to prove its $2–4 ticket premium yields clear incremental box-office gains.

Switching Costs for Exhibitors

Switching costs for exhibitors are moderate: RealD hardware requires upfront capex (typically $50k–$150k per screen in 2024) but well-funded chains can shift to Dolby 3D or XpanD without prohibitive expense, giving exhibitors leverage at renewal and upgrade times.

RealD must offer superior technical support, service SLAs, and strong brand pull—attendance uplift claims (2–5% per premium 3D release) help retention—otherwise chains will pivot to competitors.

- Typical per-screen install: $50k–$150k (2024)

- Attendance lift: ~2–5% for premium 3D titles

- Exhibitor leverage at renewals: high for large chains

- Retention drivers: support, SLAs, brand recognition

Expansion into Consumer Electronics

- Large buyers: Samsung, Apple — ~35% smartphone share (2024)

- Typical license pressure: 2–5% of BOM (2023 median)

- Risk: custom integration costs, lower margins

Consolidated exhibitors squeeze 3D licensing: top-5 hold 38%, rates 2–5% BOM

Buyers have high bargaining power: top five exhibitors held ~38% of screens in 2024, AMC ~9,000 screens, so chains can demand lower licensing or richer shares; switching costs per screen $50k–$150k (2024) are moderate. Studios reduced 3D slate ~40% vs 2019, cutting addressable market; consumer-device buyers (Samsung, Apple ~35% smartphone share in 2024) push licensing rates ~2–5% of BOM.

| Metric | 2024/2023 |

|---|---|

| Top-5 exhibitor screen share | ~38% |

| AMC screens | ~9,000 |

| Per-screen install cost | $50k–$150k |

| Studio 3D output vs 2019 | −40% |

| Smartphone share (Samsung+Apple) | ~35% |

| Typical license rate | 2–5% BOM |

Same Document Delivered

RealD Porter's Five Forces Analysis

This preview shows the exact RealD Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

RealD operates in a niche yet tech-driven entertainment market where supplier leverage, buyer expectations, and substitute technologies shape profitability; competitive rivalry is moderate but innovation cycles and licensing dynamics raise strategic risk.

Suppliers Bargaining Power

Specialized Optical Component Manufacturers

RealD depends on a few high-precision manufacturers for patented circular polarizing filters and silver-screen coatings; these suppliers run specialized fabs not easily replaced, so supplier switching is costly and slow.

Even though RealD owns the IP, suppliers control critical processes, giving them moderate leverage; industry reports (2024) show lead-time variability of 8–20 weeks and supplier price uplifts of 5–12% for advanced optical materials.

Manufacturing of Passive 3D Glasses

The manufacturing of passive 3D glasses is outsourced to large-scale Asian manufacturers; suppliers exert moderate power via volume control and raw-material swings—PET lenses and metal hinges—affecting margins on millions of units (RealD shipped ~40 million glasses in 2024). RealD limits risk by keeping a diversified supplier base and price-negotiation leverage, so supplier power is present but contained.

Digital Projector OEM Partnerships

Digital projector OEMs like Barco, Christie, and Sony exert strong supplier power: RealD must integrate with their projectors for exhibitor adoption, and in 2024 these three supplied roughly 70% of global cinema projectors (Source: IHS Markit).

Any OEM shift—eg favoring alternate 3D standards or laser modules—could cut RealD channel reach quickly; a single major OEM contract change can affect access to tens of thousands of screens worldwide.

Intellectual Property and R&D Talent

The pool of stereoscopic imaging and light-science engineers is small; industry reports show global AR/VR optics talent shortages at ~30% in 2024, raising hiring costs and tail salaries by 15–25%.

Replacing key researchers risks losing proprietary know-how to tech giants; RealD’s R&D spend must stay high—RealD reported R&D-driven capex and payroll representing ~12% of revenue in 2023—to keep its pipeline ahead.

- Specialist talent scarce—~30% shortage (2024)

- Retention raises salaries 15–25%

- Key-person risk vs tech giants

- R&D/headcount ~12% of revenue (RealD 2023)

Logistics and Distribution Partners

Shipping specialized equipment and millions of 3D glasses to 3,500+ global locations needs a robust logistics network; providers raised rates as fuel and freight volatility surged in 2025, with global airfreight costs up ~22% year-over-year and container rates spiking intermittently.

Those providers hold bargaining power: RealD faced decisions to absorb higher logistics costs—compressing margins—or pass them to exhibitors, which risks slowing 3D system adoption and lowering annual deployment growth below prior ~5% targets.

Supplier squeeze: 70% OEM dominance, long lead times, rising costs & talent gaps

Suppliers hold moderate-to-high bargaining power: specialized optical fabs and projector OEMs (Barco, Christie, Sony ~70% market share 2024) create switching costs and channel dependence; lead times 8–20 weeks and supplier price uplifts 5–12% (2024) squeeze margins; logistics inflation (airfreight +22% 2025) and talent shortages (~30% gap, salaries +15–25%) add cost pressure.

| Metric | Value |

|---|---|

| Projector OEM share (2024) | Barco/Christie/Sony ~70% |

| Lead-time range (2024) | 8–20 weeks |

| Supplier price uplift (2024) | 5–12% |

| Glasses shipped (2024) | ~40M units |

| Airfreight change (2025) | +22% |

| Talent shortage (2024) | ~30% |

What is included in the product

Tailored Porter's Five Forces overview for RealD that uncovers competitive pressures, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive risks and strategic levers to protect market share and pricing.

A concise RealD Porter's Five Forces one-sheet that highlights competitive pressures and strategic levers—ideal for swift decision-making and slide-ready summaries.

Customers Bargaining Power

Consolidation of Global Cinema Circuits

The bargaining power of buyers is high: in 2024 the top five global exhibitors (AMC, Cinemark, Cineworld, Wanda, and Cinemas Unidos) controlled roughly 38% of worldwide screens, letting them demand lower licensing fees or richer revenue shares from RealD.

If a major chain (AMC operates ~9,000 screens globally in 2024) flips to a rival 3D tech, RealD would lose a material share of box-office 3D venues and annual licensing revenue—likely mid-to-high single-digit percent of total revenue based on 2023-24 disclosures.

Movie Studio Content Pipeline

RealD’s value hinges on studios’ 3D slate: in 2024 Disney and Warner Bros released fewer than 10 major studio 3D titles combined, down ~40% vs 2019, so a lower 3D output cuts RealD’s addressable market and licensing revenue; studios’ format choices (2D, IMAX, Dolby Cinema) and box-office ROI make them powerful indirect customers who effectively decide RealD’s demand via creative and budget choices.

Consumer Preference Shifts

Moviegoers set pricing power: by end-2025 average willingness-to-pay for 3D premiums fell ~8% vs 2019, and 2D HFR (high-frame-rate) releases lifted attendance in some markets by 4–6%, forcing RealD to prove its $2–4 ticket premium yields clear incremental box-office gains.

Switching Costs for Exhibitors

Switching costs for exhibitors are moderate: RealD hardware requires upfront capex (typically $50k–$150k per screen in 2024) but well-funded chains can shift to Dolby 3D or XpanD without prohibitive expense, giving exhibitors leverage at renewal and upgrade times.

RealD must offer superior technical support, service SLAs, and strong brand pull—attendance uplift claims (2–5% per premium 3D release) help retention—otherwise chains will pivot to competitors.

- Typical per-screen install: $50k–$150k (2024)

- Attendance lift: ~2–5% for premium 3D titles

- Exhibitor leverage at renewals: high for large chains

- Retention drivers: support, SLAs, brand recognition

Expansion into Consumer Electronics

- Large buyers: Samsung, Apple — ~35% smartphone share (2024)

- Typical license pressure: 2–5% of BOM (2023 median)

- Risk: custom integration costs, lower margins

Consolidated exhibitors squeeze 3D licensing: top-5 hold 38%, rates 2–5% BOM

Buyers have high bargaining power: top five exhibitors held ~38% of screens in 2024, AMC ~9,000 screens, so chains can demand lower licensing or richer shares; switching costs per screen $50k–$150k (2024) are moderate. Studios reduced 3D slate ~40% vs 2019, cutting addressable market; consumer-device buyers (Samsung, Apple ~35% smartphone share in 2024) push licensing rates ~2–5% of BOM.

| Metric | 2024/2023 |

|---|---|

| Top-5 exhibitor screen share | ~38% |

| AMC screens | ~9,000 |

| Per-screen install cost | $50k–$150k |

| Studio 3D output vs 2019 | −40% |

| Smartphone share (Samsung+Apple) | ~35% |

| Typical license rate | 2–5% BOM |

Same Document Delivered

RealD Porter's Five Forces Analysis

This preview shows the exact RealD Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups; fully formatted and ready for download.