Redwood Trust Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

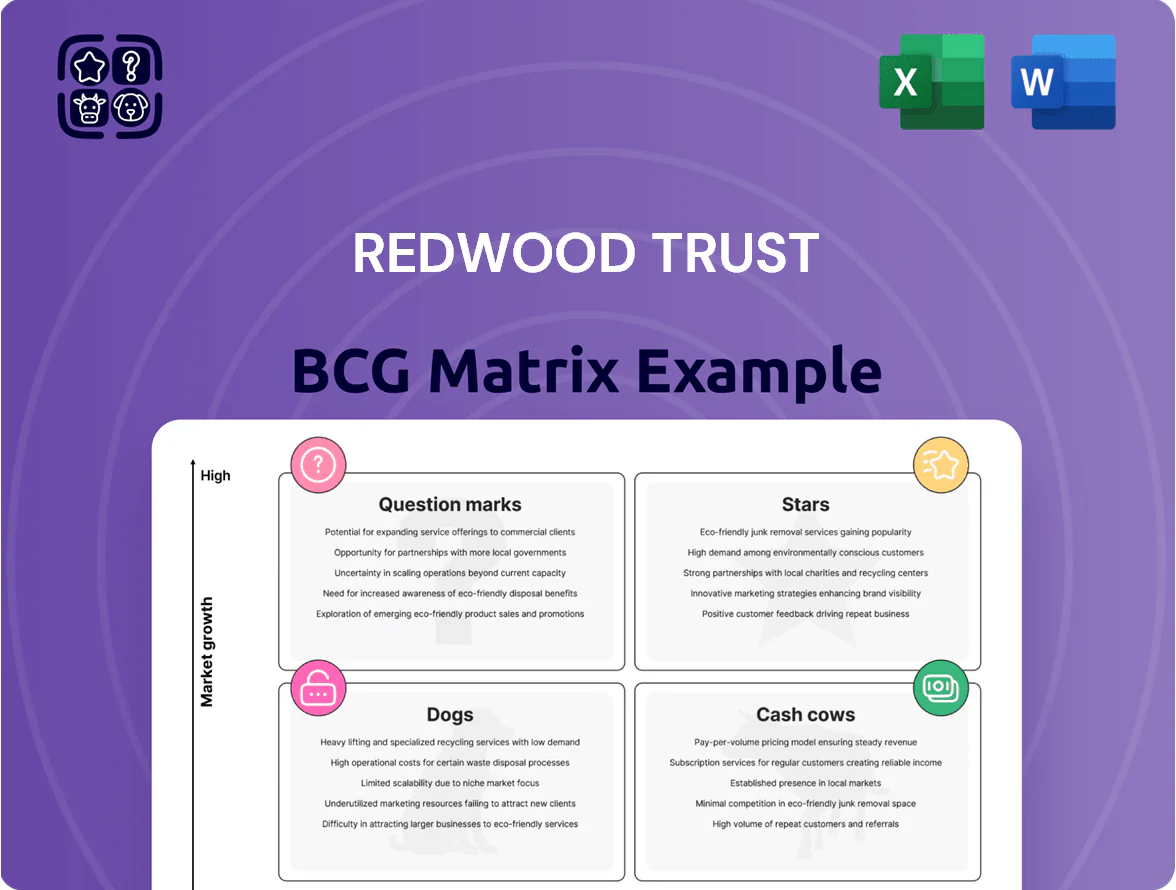

Redwood Trust’s brief BCG Matrix snapshot highlights its core mortgage-focused offerings poised between Cash Cow stability and Question Mark growth potential amid rising rates and credit shifts. This preview teases quadrant placements and strategic implications, but the full BCG Matrix delivers detailed product-level mappings, revenue and market-share analytics, and targeted recommendations to optimize capital allocation. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that clarifies which businesses to double down on, restructure, or divest.

Stars

Sequoia Residential Mortgage Platform

Sequoia Residential Mortgage Platform, Redwood Trust’s flagship residential conduit, posted a record $23 billion in 2025 volume and captured roughly 7% of the jumbo mortgage market by year-end amid banks retreating from non-agency lending.

High market share in a rebounding housing sector makes Sequoia a Star in the BCG Matrix: it drives growth but consumes capital for loan aggregation while producing significant fee income from securitizations and servicing.

Aspire Non-QM Expansion

Aspire is Redwood Trust’s high-growth expanded-credit (non-QM) platform; loan locks rose 20% sequentially in Q4 2025, signaling strong demand among borrowers outside agency criteria.

Redwood launched a dedicated securitization shelf in Jan 2026 to scale funding; the move targets deeper market presence and faster warehouse-to-securitization capacity.

Building distribution needs heavy investment—sales, compliance, and capital—but Aspire is rapidly gaining share in a non-QM market that grew ~18% YOY in 2025, per industry data.

CoreVest Small-Balance Production

CoreVest Small-Balance Production shifted to smaller-balance Business Purpose Loans (BPLs), focusing on residential transition and DSCR (debt-service-coverage-ratio) loans to professional investors.

By Q4 2025 this unit returned 30% on capital, led origination volumes of ~$1.2B annualized and benefited from rising single-family-rental demand and institutional buy-to-rent flows.

It holds a leadership spot within Redwood Trust’s BCG Matrix Stars: high market share and high growth, but needs continuous capital—estimated $400M+—to fund a strong origination pipeline into 2026.

Home Equity Investment (HEI) Products

Redwood Trust expanded Home Equity Investment (HEI) offerings via the Aspire platform to tap an estimated US$10.2 trillion in homeowner equity; HEI saw sharp momentum in 2025 as an alternative to 8–12% second mortgages and HELOCs, driving rapid originations and strong fee revenue growth.

The nascent HEI market grew ~40% YoY in 2025; Redwood’s early-mover scale and distribution give it Star status in the BCG matrix, prioritized for capital allocation and national roll-out.

- Target market: US$10.2T homeowner equity

- 2025 market growth: ~40% YoY

- Alternative rates: avoids 8–12% loan costs

- Status: Star — scaling for dominance

Capital-Light Distribution Channels

Redwood’s move to an originate-to-distribute model drove mortgage banking volumes up 111% year-over-year in 2025, boosting fee income while capping balance-sheet exposure.

Using joint ventures and whole‑loan sales plus securitizations let Redwood extend reach across non‑agency channels without large leverage increases; net leverage remained near 6.2x in FY2025.

That capital‑light flexibility supports retaining high market share as interest rates shifted in late 2025 and into 2026, keeping exposure tolerant to spread widening.

- +111% mortgage volumes in 2025

- Joint ventures + whole‑loan sales + securitizations

- Net leverage ≈ 6.2x FY2025

- Resilient non‑agency share into 2026 rate shifts

Redwood’s Stars — Sequoia, Aspire, CoreVest, HEI Drive High-Growth, Need $400M+ Capital

Sequoia, Aspire, CoreVest and HEI are Stars in Redwood Trust’s BCG matrix: high share and high growth driven by $23B Sequoia volume (2025), Aspire loan locks +20% Q4 2025, CoreVest ~$1.2B annualized origination with 30% RoC, HEI market +40% YoY (2025); Stars need ongoing capital (~$400M+) and securitization capacity (shelf launched Jan 2026).

| Unit | 2025/Q4 | Metric |

|---|---|---|

| Sequoia | 2025 | $23B vol; ~7% jumbo share |

| Aspire | Q4 2025 | Locks +20% seq |

| CoreVest | Q4 2025 | $1.2B ann; 30% RoC |

| HEI | 2025 | Market +40% YoY; $10.2T equity |

What is included in the product

BCG Matrix analysis for Redwood Trust: quadrant placement, strategic moves (invest/hold/divest), and macro/micro risks per unit.

One-page BCG Matrix positioning Redwood Trust segments to highlight growth vs. cash needs for clear C-suite decisions.

Cash Cows

Redwood Investments Retained Portfolio

The Redwood Investments retained portfolio, made of high-quality mortgage-backed securities and bridge loans, generated steady interest income with minimal new marketing spend and delivered a 17% return on capital by year-end 2025.

That 17% RoC produced essential cash flow—covering dividends and funding new growth—while acting as a mature profit center that milks returns from prior successful mortgage banking originations.

Residential Jumbo Securitization Shelf

Redwood Trust’s Residential Jumbo Securitization Shelf is a cash cow: as a premier issuer of private-label jumbo mortgage-backed securities (MBS), it keeps market share with lower incremental costs than newer entrants, generating steady fee income from servicing and management.

Operating efficiency rose sharply—operating cost per loan improved 44% in 2025, cutting unit costs to roughly $1,120 from $2,000 in 2024 (here’s the quick math: 2,000×0.56≈1,120).

Legacy shelves plus new-issue programs produced predictable servicing and structuring fees equal to about 18% of Redwood’s 2025 distributable cash flow, supporting dividends and reinvestment.

CoreVest Term Loan Servicing

CoreVest Term Loan Servicing, Redwood Trusts cash cow, handles stabilized rental portfolios and produced roughly $45m in servicing fee revenue in 2024, offering predictable, high-margin cash flow versus bridge loans.

Servicing Rights and Fee Income

Redwood’s Mortgage Servicing Rights (MSRs) and fee businesses provided steady liquidity and a natural hedge in 2025, with servicing income rising as production scaled to $23 billion; servicing-generated revenue represented roughly 18–22% of total recurring income that year, boosting cash flow stability.

The MSR unit needs low capital reinvestment versus origination, freeing excess cash for balance-sheet uses and buybacks; servicing cash yields averaged about 120–150 bps on MSR balances in 2025, supporting redeployment.

- Servicing tied to $23B production in 2025

- Recurring income ~18–22% from servicing

- Cash yield ~120–150 bps on MSRs

- Low capex needs enable redeployment

Strategic Joint Venture Partnerships

Redwood’s strategic joint ventures with institutional partners such as CPP Investments have matured into steady fee-generating vehicles, delivering management fees and carried interest that totaled roughly $85m in 2024 and contributed ~18% of fee revenue.

These structures let Redwood retain market presence in large-scale housing credit while third-party capital assumes primary risk, producing high-margin, low-growth-requirement cash flows that bolster liquidity and ROE.

- 2024 fee+carry ≈ $85m

- ~18% of fee revenue (2024)

- Low capital at risk for Redwood

- High margin, steady cash flow

Redwood’s low-capital cash engines: 17% RoC, $23B servicing, $130M+ fee revenue

Redwood’s cash cows—retained MBS/bridge portfolio, MSRs, CoreVest servicing, and JV fee vehicles—generated steady, low-capital cash: 17% RoC on retained portfolio (2025), servicing tied to $23B production (2025) producing ~18–22% of recurring income and 120–150 bps cash yield, CoreVest servicing ≈ $45m revenue (2024), JV fees+carry ≈ $85m (2024).

| Item | Metric |

|---|---|

| Retained portfolio | 17% RoC (2025) |

| Servicing | $23B prod; 18–22% income; 120–150 bps |

| CoreVest | $45m rev (2024) |

| JV fees+carry | $85m (2024) |

Full Transparency, Always

Redwood Trust BCG Matrix

The file you're previewing is the exact Redwood Trust BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the polished, presentation-ready document crafted for strategic clarity.

This preview mirrors the full deliverable: a professionally formatted BCG Matrix with market-backed positioning and concise insights, ready to download and use immediately.

Once purchased, the same editable file will be sent to your inbox—perfect for printing, editing, or presenting to stakeholders without further modification.

No mockups or drafts here—this is the final analysis-ready report designed by strategy experts to plug directly into your planning and investor materials.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Redwood Trust’s brief BCG Matrix snapshot highlights its core mortgage-focused offerings poised between Cash Cow stability and Question Mark growth potential amid rising rates and credit shifts. This preview teases quadrant placements and strategic implications, but the full BCG Matrix delivers detailed product-level mappings, revenue and market-share analytics, and targeted recommendations to optimize capital allocation. Purchase the complete report for a ready-to-use Word analysis plus an Excel summary that clarifies which businesses to double down on, restructure, or divest.

Stars

Sequoia Residential Mortgage Platform

Sequoia Residential Mortgage Platform, Redwood Trust’s flagship residential conduit, posted a record $23 billion in 2025 volume and captured roughly 7% of the jumbo mortgage market by year-end amid banks retreating from non-agency lending.

High market share in a rebounding housing sector makes Sequoia a Star in the BCG Matrix: it drives growth but consumes capital for loan aggregation while producing significant fee income from securitizations and servicing.

Aspire Non-QM Expansion

Aspire is Redwood Trust’s high-growth expanded-credit (non-QM) platform; loan locks rose 20% sequentially in Q4 2025, signaling strong demand among borrowers outside agency criteria.

Redwood launched a dedicated securitization shelf in Jan 2026 to scale funding; the move targets deeper market presence and faster warehouse-to-securitization capacity.

Building distribution needs heavy investment—sales, compliance, and capital—but Aspire is rapidly gaining share in a non-QM market that grew ~18% YOY in 2025, per industry data.

CoreVest Small-Balance Production

CoreVest Small-Balance Production shifted to smaller-balance Business Purpose Loans (BPLs), focusing on residential transition and DSCR (debt-service-coverage-ratio) loans to professional investors.

By Q4 2025 this unit returned 30% on capital, led origination volumes of ~$1.2B annualized and benefited from rising single-family-rental demand and institutional buy-to-rent flows.

It holds a leadership spot within Redwood Trust’s BCG Matrix Stars: high market share and high growth, but needs continuous capital—estimated $400M+—to fund a strong origination pipeline into 2026.

Home Equity Investment (HEI) Products

Redwood Trust expanded Home Equity Investment (HEI) offerings via the Aspire platform to tap an estimated US$10.2 trillion in homeowner equity; HEI saw sharp momentum in 2025 as an alternative to 8–12% second mortgages and HELOCs, driving rapid originations and strong fee revenue growth.

The nascent HEI market grew ~40% YoY in 2025; Redwood’s early-mover scale and distribution give it Star status in the BCG matrix, prioritized for capital allocation and national roll-out.

- Target market: US$10.2T homeowner equity

- 2025 market growth: ~40% YoY

- Alternative rates: avoids 8–12% loan costs

- Status: Star — scaling for dominance

Capital-Light Distribution Channels

Redwood’s move to an originate-to-distribute model drove mortgage banking volumes up 111% year-over-year in 2025, boosting fee income while capping balance-sheet exposure.

Using joint ventures and whole‑loan sales plus securitizations let Redwood extend reach across non‑agency channels without large leverage increases; net leverage remained near 6.2x in FY2025.

That capital‑light flexibility supports retaining high market share as interest rates shifted in late 2025 and into 2026, keeping exposure tolerant to spread widening.

- +111% mortgage volumes in 2025

- Joint ventures + whole‑loan sales + securitizations

- Net leverage ≈ 6.2x FY2025

- Resilient non‑agency share into 2026 rate shifts

Redwood’s Stars — Sequoia, Aspire, CoreVest, HEI Drive High-Growth, Need $400M+ Capital

Sequoia, Aspire, CoreVest and HEI are Stars in Redwood Trust’s BCG matrix: high share and high growth driven by $23B Sequoia volume (2025), Aspire loan locks +20% Q4 2025, CoreVest ~$1.2B annualized origination with 30% RoC, HEI market +40% YoY (2025); Stars need ongoing capital (~$400M+) and securitization capacity (shelf launched Jan 2026).

| Unit | 2025/Q4 | Metric |

|---|---|---|

| Sequoia | 2025 | $23B vol; ~7% jumbo share |

| Aspire | Q4 2025 | Locks +20% seq |

| CoreVest | Q4 2025 | $1.2B ann; 30% RoC |

| HEI | 2025 | Market +40% YoY; $10.2T equity |

What is included in the product

BCG Matrix analysis for Redwood Trust: quadrant placement, strategic moves (invest/hold/divest), and macro/micro risks per unit.

One-page BCG Matrix positioning Redwood Trust segments to highlight growth vs. cash needs for clear C-suite decisions.

Cash Cows

Redwood Investments Retained Portfolio

The Redwood Investments retained portfolio, made of high-quality mortgage-backed securities and bridge loans, generated steady interest income with minimal new marketing spend and delivered a 17% return on capital by year-end 2025.

That 17% RoC produced essential cash flow—covering dividends and funding new growth—while acting as a mature profit center that milks returns from prior successful mortgage banking originations.

Residential Jumbo Securitization Shelf

Redwood Trust’s Residential Jumbo Securitization Shelf is a cash cow: as a premier issuer of private-label jumbo mortgage-backed securities (MBS), it keeps market share with lower incremental costs than newer entrants, generating steady fee income from servicing and management.

Operating efficiency rose sharply—operating cost per loan improved 44% in 2025, cutting unit costs to roughly $1,120 from $2,000 in 2024 (here’s the quick math: 2,000×0.56≈1,120).

Legacy shelves plus new-issue programs produced predictable servicing and structuring fees equal to about 18% of Redwood’s 2025 distributable cash flow, supporting dividends and reinvestment.

CoreVest Term Loan Servicing

CoreVest Term Loan Servicing, Redwood Trusts cash cow, handles stabilized rental portfolios and produced roughly $45m in servicing fee revenue in 2024, offering predictable, high-margin cash flow versus bridge loans.

Servicing Rights and Fee Income

Redwood’s Mortgage Servicing Rights (MSRs) and fee businesses provided steady liquidity and a natural hedge in 2025, with servicing income rising as production scaled to $23 billion; servicing-generated revenue represented roughly 18–22% of total recurring income that year, boosting cash flow stability.

The MSR unit needs low capital reinvestment versus origination, freeing excess cash for balance-sheet uses and buybacks; servicing cash yields averaged about 120–150 bps on MSR balances in 2025, supporting redeployment.

- Servicing tied to $23B production in 2025

- Recurring income ~18–22% from servicing

- Cash yield ~120–150 bps on MSRs

- Low capex needs enable redeployment

Strategic Joint Venture Partnerships

Redwood’s strategic joint ventures with institutional partners such as CPP Investments have matured into steady fee-generating vehicles, delivering management fees and carried interest that totaled roughly $85m in 2024 and contributed ~18% of fee revenue.

These structures let Redwood retain market presence in large-scale housing credit while third-party capital assumes primary risk, producing high-margin, low-growth-requirement cash flows that bolster liquidity and ROE.

- 2024 fee+carry ≈ $85m

- ~18% of fee revenue (2024)

- Low capital at risk for Redwood

- High margin, steady cash flow

Redwood’s low-capital cash engines: 17% RoC, $23B servicing, $130M+ fee revenue

Redwood’s cash cows—retained MBS/bridge portfolio, MSRs, CoreVest servicing, and JV fee vehicles—generated steady, low-capital cash: 17% RoC on retained portfolio (2025), servicing tied to $23B production (2025) producing ~18–22% of recurring income and 120–150 bps cash yield, CoreVest servicing ≈ $45m revenue (2024), JV fees+carry ≈ $85m (2024).

| Item | Metric |

|---|---|

| Retained portfolio | 17% RoC (2025) |

| Servicing | $23B prod; 18–22% income; 120–150 bps |

| CoreVest | $45m rev (2024) |

| JV fees+carry | $85m (2024) |

Full Transparency, Always

Redwood Trust BCG Matrix

The file you're previewing is the exact Redwood Trust BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the polished, presentation-ready document crafted for strategic clarity.

This preview mirrors the full deliverable: a professionally formatted BCG Matrix with market-backed positioning and concise insights, ready to download and use immediately.

Once purchased, the same editable file will be sent to your inbox—perfect for printing, editing, or presenting to stakeholders without further modification.

No mockups or drafts here—this is the final analysis-ready report designed by strategy experts to plug directly into your planning and investor materials.