Redwood Trust SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Redwood Trust's conservative capital structure and niche focus in residential mortgage securities underpin steady income, but regulatory shifts and interest-rate volatility pose material risks to returns. Competitive pressures from larger REITs and liquidity constraints could limit growth, while tech-enabled underwriting and distressed-market opportunities offer upside. What you’ve seen is just the beginning—purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel tools for strategic planning and investment decisions.

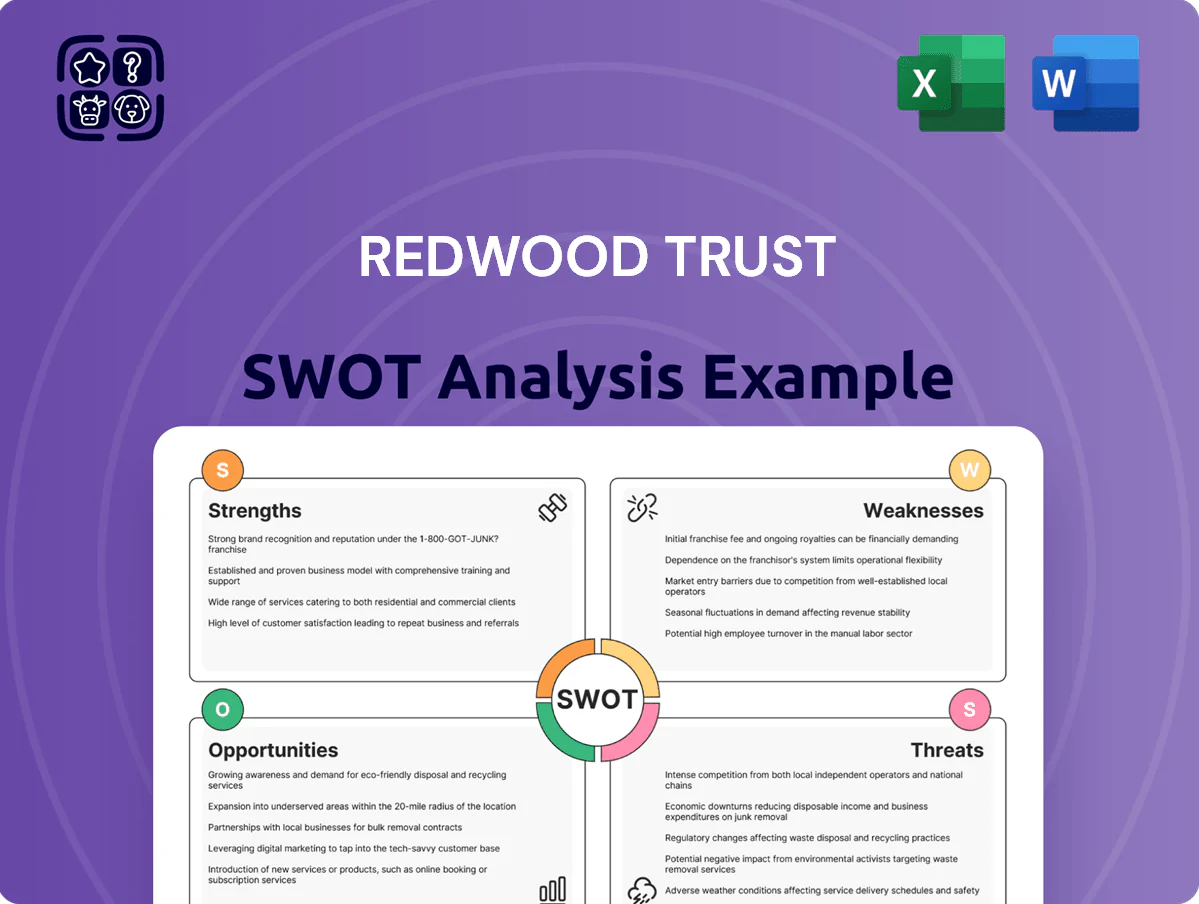

Strengths

Diversified Housing Credit Platform

Redwood Trust operates across residential mortgage banking, business-purpose lending, and investment portfolios, enabling shifts of capital to higher-margin areas; in 2025 YTD the firm reported $1.8B originations and a 12% rise in investment portfolio yield to 4.6%, showing pivot capacity. This mix balances consumer mortgages with investor loans, lowering exposure to any single housing downturn and preserving NII—net interest income—stability.

Established Securitization Pipeline

Redwood Trust has a long-standing reputation as a premier private-label securitizer via Sequoia and CoreVest, having securitized over $45 billion cumulatively by 2024; this pipeline lets it recycle capital and shift loans off balance sheet while holding top-credit tranches. Deep institutional ties—over 120 active investors as of Q4 2025—sustain liquidity through moderate volatility, supporting repeat issuance and margin stability.

Robust Capital Position

As of late 2025, Redwood Trust maintained conservative leverage with debt-to-equity near 2.8x and liquidity of about $1.1 billion, providing a buffer against economic shocks.

Access to diverse funding—$800M in committed warehouse lines and $600M of corporate debt capacity—supported sustained loan originations of roughly $3.2 billion YTD.

This financial stability lets Redwood bid on distressed residential mortgage assets competitors often avoid, boosting opportunistic returns above peers by an estimated 150–250 basis points.

Leadership in Non-Agency Markets

Redwood Trust specializes in jumbo and non-qualified mortgage (Non-QM) lending, serving borrowers outside GSE (government-sponsored enterprise) limits where banks pulled back; as of FY2024 Redwood held roughly $6.1B in credit investments, concentrated in high-credit-quality loans.

By targeting borrowers with strong credit profiles but nonconforming documentation, Redwood captures yield premiums—non-agency spreads ran about 150–300 basis points over agency product in 2024—creating a durable moat against generalist REITs that lack specialized underwriting and servicing infrastructure.

- Focused on jumbo/Non-QM: $6.1B credit assets (2024)

- Higher yields: ~150–300 bps spread vs agency (2024)

- Servicing/underwriting moat: costly to replicate

Technology-Driven Operational Efficiency

Redwood Trust has cut loan production costs by about 18% since 2022 via advanced analytics and digital lending platforms, boosting annualized ROA and improving credit-model accuracy—default prediction AUC rose to ~0.82 in 2024.

Digital partner interfaces expanded business-purpose lending share to roughly 27% of originations in 2024, speeding acquisition and improving servicing efficiency.

- 18% lower production costs since 2022

- AUC ~0.82 for credit models (2024)

- 27% share of originations in business-purpose lending (2024)

Redwood Trust: $1.8B originations, 4.6% yield, strong liquidity & 150–300bp excess spreads

Redwood Trust’s diversified mix (residential, business-purpose, investments) drove $1.8B originations YTD 2025 and lifted portfolio yield to 4.6%, keeping NII stable; securitization legacy (>$45B cumul. by 2024) and 120+ investors support liquidity and repeat issuance. Conservative leverage (~2.8x) and $1.1B liquidity plus $800M warehouse/$600M debt capacity back opportunistic buying and ~150–250 bps excess returns in jumbo/Non-QM niches.

| Metric | Value |

|---|---|

| Originations YTD 2025 | $1.8B |

| Portfolio yield 2025 | 4.6% |

| Cumulative securitized | >$45B (by 2024) |

| Leverage (D/E) | ~2.8x |

| Liquidity | $1.1B |

| Warehouse lines | $800M |

| Debt capacity | $600M |

| Non-agency spread | 150–300 bps (2024) |

What is included in the product

Provides a clear SWOT framework analyzing Redwood Trust’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in mortgage finance and real estate investment.

Provides a concise Redwood Trust SWOT snapshot for rapid strategic alignment, highlighting strengths in mortgage REIT expertise and risk areas like interest-rate sensitivity for quick stakeholder briefings.

Weaknesses

Sensitivity to Interest Rate Volatility

Like most mortgage REITs, Redwood Trust’s book value and EPS swing sharply with benchmark rates; a 100bp rise in 2022 cut many mREIT book values by ~15–20%, and similar moves would hit Redwood’s Agency and non-Agency portfolios. Sharp rate jumps create unrealized MTM losses and compressed gain-on-sale margins for Redwood’s mortgage banking unit—gain-on-sale fell 30% y/y in 2023 industry-wide. Falling rates raise prepayment speeds (CPR), shortening high-yield assets and reducing future interest income; Redwood reported CPR spikes of 200–300bps in prior rate drops.

Dependence on Capital Markets

Redwood Trust depends on securitization and secondary markets to sell loans; in 2024 roughly 78% of its mortgage originations were financed via private-label securitizations, so market access is core. If private-label demand stalls, loans pile up on the balance sheet, raising financing costs—Redwood’s debt-to-equity was about 2.1x in Q3 2024, showing leverage sensitivity. A prolonged market disruption could sharply widen spreads and cut net interest margin, exposing the firm to systemic shocks beyond its control.

Concentration in Higher-Balance Loans

Complex Hedging Requirements

Managing Redwood Trust’s mix of mortgage-backed securities and whole loans needs costly, advanced hedges; in 2025 the firm reported $21.4B of total investments, raising sensitivity to basis and duration mismatches.

Hedge slippage or imperfect correlation can create earnings drag or capital loss—Redwood’s 2024 net investment income declined 12% year-over-year, partly tied to hedging costs.

These instruments and layered derivatives make filings harder for novice investors to parse, increasing reliance on advisor analysis and raising governance scrutiny.

- Portfolio size: $21.4B (2025)

- 2024 NII down 12% YoY

- High basis/duration mismatch risk

- Complex disclosures limit retail understanding

Operational Overhead Costs

Operating a full-scale mortgage banking and investment platform forces Redwood Trust to carry high fixed costs—compliance, staff, and tech—estimated at hundreds of millions annually across the sector; S&P data shows mortgage operators’ non-interest expense ratios rose to ~1.8% in 2024.

When loan originations fall (Redwood reported originations down 22% YoY in 2024), these overheads compress ROE quickly; maintaining dual residential and commercial infrastructure needs continual capex and ops spend regardless of revenue.

- High fixed costs: compliance, staff, tech

- Sector non-interest expense ≈1.8% (2024)

- Originations −22% YoY for Redwood (2024)

- Ongoing capex for residential + commercial platforms

Rate sensitivity, funding squeeze and jumbo exposure slash mREIT value and NII

Rate sensitivity drives big MTM swings (100bp moves cut mREIT book values ~15–20%); 2024 NII fell 12% YoY and basis/duration mismatch risk rises with $21.4B portfolio (2025). Heavy reliance on private-label securitizations (≈78% originations financed, 2024) and originations −22% YoY (2024) amplify funding and liquidity risk. Jumbo concentration (≈62% originations, 2024) ups housing-cycle exposure; high fixed costs (sector non-interest expense ≈1.8%, 2024) compress ROE.

| Metric | Value |

|---|---|

| Portfolio size | $21.4B (2025) |

| 2024 NII change | −12% YoY |

| Private-label financing | ≈78% of originations (2024) |

| Originations | −22% YoY (2024) |

| Jumbo share | ≈62% of originations (2024) |

| Sector non-interest expense | ≈1.8% (2024) |

What You See Is What You Get

Redwood Trust SWOT Analysis

This is the actual Redwood Trust SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report you'll get, and once purchased the complete, editable version will be available for immediate download.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Redwood Trust's conservative capital structure and niche focus in residential mortgage securities underpin steady income, but regulatory shifts and interest-rate volatility pose material risks to returns. Competitive pressures from larger REITs and liquidity constraints could limit growth, while tech-enabled underwriting and distressed-market opportunities offer upside. What you’ve seen is just the beginning—purchase the full SWOT analysis to access a professionally formatted Word report and editable Excel tools for strategic planning and investment decisions.

Strengths

Diversified Housing Credit Platform

Redwood Trust operates across residential mortgage banking, business-purpose lending, and investment portfolios, enabling shifts of capital to higher-margin areas; in 2025 YTD the firm reported $1.8B originations and a 12% rise in investment portfolio yield to 4.6%, showing pivot capacity. This mix balances consumer mortgages with investor loans, lowering exposure to any single housing downturn and preserving NII—net interest income—stability.

Established Securitization Pipeline

Redwood Trust has a long-standing reputation as a premier private-label securitizer via Sequoia and CoreVest, having securitized over $45 billion cumulatively by 2024; this pipeline lets it recycle capital and shift loans off balance sheet while holding top-credit tranches. Deep institutional ties—over 120 active investors as of Q4 2025—sustain liquidity through moderate volatility, supporting repeat issuance and margin stability.

Robust Capital Position

As of late 2025, Redwood Trust maintained conservative leverage with debt-to-equity near 2.8x and liquidity of about $1.1 billion, providing a buffer against economic shocks.

Access to diverse funding—$800M in committed warehouse lines and $600M of corporate debt capacity—supported sustained loan originations of roughly $3.2 billion YTD.

This financial stability lets Redwood bid on distressed residential mortgage assets competitors often avoid, boosting opportunistic returns above peers by an estimated 150–250 basis points.

Leadership in Non-Agency Markets

Redwood Trust specializes in jumbo and non-qualified mortgage (Non-QM) lending, serving borrowers outside GSE (government-sponsored enterprise) limits where banks pulled back; as of FY2024 Redwood held roughly $6.1B in credit investments, concentrated in high-credit-quality loans.

By targeting borrowers with strong credit profiles but nonconforming documentation, Redwood captures yield premiums—non-agency spreads ran about 150–300 basis points over agency product in 2024—creating a durable moat against generalist REITs that lack specialized underwriting and servicing infrastructure.

- Focused on jumbo/Non-QM: $6.1B credit assets (2024)

- Higher yields: ~150–300 bps spread vs agency (2024)

- Servicing/underwriting moat: costly to replicate

Technology-Driven Operational Efficiency

Redwood Trust has cut loan production costs by about 18% since 2022 via advanced analytics and digital lending platforms, boosting annualized ROA and improving credit-model accuracy—default prediction AUC rose to ~0.82 in 2024.

Digital partner interfaces expanded business-purpose lending share to roughly 27% of originations in 2024, speeding acquisition and improving servicing efficiency.

- 18% lower production costs since 2022

- AUC ~0.82 for credit models (2024)

- 27% share of originations in business-purpose lending (2024)

Redwood Trust: $1.8B originations, 4.6% yield, strong liquidity & 150–300bp excess spreads

Redwood Trust’s diversified mix (residential, business-purpose, investments) drove $1.8B originations YTD 2025 and lifted portfolio yield to 4.6%, keeping NII stable; securitization legacy (>$45B cumul. by 2024) and 120+ investors support liquidity and repeat issuance. Conservative leverage (~2.8x) and $1.1B liquidity plus $800M warehouse/$600M debt capacity back opportunistic buying and ~150–250 bps excess returns in jumbo/Non-QM niches.

| Metric | Value |

|---|---|

| Originations YTD 2025 | $1.8B |

| Portfolio yield 2025 | 4.6% |

| Cumulative securitized | >$45B (by 2024) |

| Leverage (D/E) | ~2.8x |

| Liquidity | $1.1B |

| Warehouse lines | $800M |

| Debt capacity | $600M |

| Non-agency spread | 150–300 bps (2024) |

What is included in the product

Provides a clear SWOT framework analyzing Redwood Trust’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in mortgage finance and real estate investment.

Provides a concise Redwood Trust SWOT snapshot for rapid strategic alignment, highlighting strengths in mortgage REIT expertise and risk areas like interest-rate sensitivity for quick stakeholder briefings.

Weaknesses

Sensitivity to Interest Rate Volatility

Like most mortgage REITs, Redwood Trust’s book value and EPS swing sharply with benchmark rates; a 100bp rise in 2022 cut many mREIT book values by ~15–20%, and similar moves would hit Redwood’s Agency and non-Agency portfolios. Sharp rate jumps create unrealized MTM losses and compressed gain-on-sale margins for Redwood’s mortgage banking unit—gain-on-sale fell 30% y/y in 2023 industry-wide. Falling rates raise prepayment speeds (CPR), shortening high-yield assets and reducing future interest income; Redwood reported CPR spikes of 200–300bps in prior rate drops.

Dependence on Capital Markets

Redwood Trust depends on securitization and secondary markets to sell loans; in 2024 roughly 78% of its mortgage originations were financed via private-label securitizations, so market access is core. If private-label demand stalls, loans pile up on the balance sheet, raising financing costs—Redwood’s debt-to-equity was about 2.1x in Q3 2024, showing leverage sensitivity. A prolonged market disruption could sharply widen spreads and cut net interest margin, exposing the firm to systemic shocks beyond its control.

Concentration in Higher-Balance Loans

Complex Hedging Requirements

Managing Redwood Trust’s mix of mortgage-backed securities and whole loans needs costly, advanced hedges; in 2025 the firm reported $21.4B of total investments, raising sensitivity to basis and duration mismatches.

Hedge slippage or imperfect correlation can create earnings drag or capital loss—Redwood’s 2024 net investment income declined 12% year-over-year, partly tied to hedging costs.

These instruments and layered derivatives make filings harder for novice investors to parse, increasing reliance on advisor analysis and raising governance scrutiny.

- Portfolio size: $21.4B (2025)

- 2024 NII down 12% YoY

- High basis/duration mismatch risk

- Complex disclosures limit retail understanding

Operational Overhead Costs

Operating a full-scale mortgage banking and investment platform forces Redwood Trust to carry high fixed costs—compliance, staff, and tech—estimated at hundreds of millions annually across the sector; S&P data shows mortgage operators’ non-interest expense ratios rose to ~1.8% in 2024.

When loan originations fall (Redwood reported originations down 22% YoY in 2024), these overheads compress ROE quickly; maintaining dual residential and commercial infrastructure needs continual capex and ops spend regardless of revenue.

- High fixed costs: compliance, staff, tech

- Sector non-interest expense ≈1.8% (2024)

- Originations −22% YoY for Redwood (2024)

- Ongoing capex for residential + commercial platforms

Rate sensitivity, funding squeeze and jumbo exposure slash mREIT value and NII

Rate sensitivity drives big MTM swings (100bp moves cut mREIT book values ~15–20%); 2024 NII fell 12% YoY and basis/duration mismatch risk rises with $21.4B portfolio (2025). Heavy reliance on private-label securitizations (≈78% originations financed, 2024) and originations −22% YoY (2024) amplify funding and liquidity risk. Jumbo concentration (≈62% originations, 2024) ups housing-cycle exposure; high fixed costs (sector non-interest expense ≈1.8%, 2024) compress ROE.

| Metric | Value |

|---|---|

| Portfolio size | $21.4B (2025) |

| 2024 NII change | −12% YoY |

| Private-label financing | ≈78% of originations (2024) |

| Originations | −22% YoY (2024) |

| Jumbo share | ≈62% of originations (2024) |

| Sector non-interest expense | ≈1.8% (2024) |

What You See Is What You Get

Redwood Trust SWOT Analysis

This is the actual Redwood Trust SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality; the preview below is taken directly from the full report you'll get, and once purchased the complete, editable version will be available for immediate download.