Regal Rexnord Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

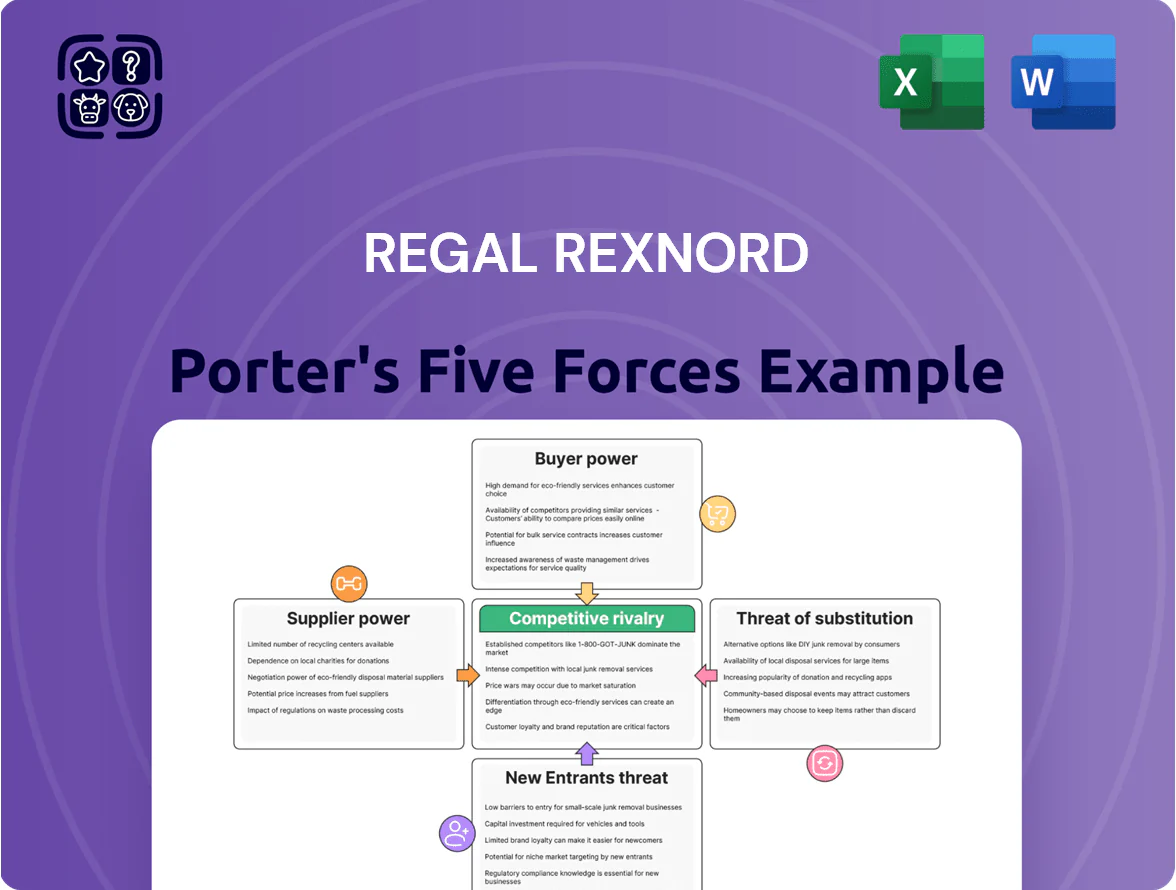

Regal Rexnord faces moderate supplier power, pricing pressure from industrial buyers, and steady rivalry as consolidation and aftermarket services shape competitive dynamics.

Barriers to entry are mixed—capital-intensive manufacturing deters newcomers, but niche tech and service models could erode share, while substitutes and digitalization slowly shift value propositions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Regal Rexnord’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Regal Rexnord depends on steel, copper, aluminum and rare-earth magnets for motors and powertrains, and by end-2025 global shifts and trade policies kept price volatility high—steel up ~12% and copper up ~9% year-to-date in 2025. Because these commodities trade on global exchanges (LME, SHFE), Regal Rexnord has limited ability to move market prices, though its 2024 procurement volume (~$1.6bn materials spend) secures modest volume discounts. High input-price volatility raises margin pressure and forces tighter working-capital management and hedging use.

Specialized Electronic Component Sourcing

The shift to smart sensors and digital controls means Regal Rexnord needs specialized semiconductors and electronics from a small set of global suppliers; industry data shows 70–80% of high-performance motion-control ICs come from fewer than five vendors as of 2025, giving those suppliers pricing and lead-time power. This concentration raises supplier bargaining leverage, pressuring margins and forcing Regal Rexnord to absorb higher input costs or invest in dual sourcing and inventory buffers to avoid production delays.

Energy and Logistics Cost Pressures

Suppliers for energy-intensive processes and logistics pressure Regal Rexnord via volatile costs—benchmark electricity rose ~12% in US industrial rates 2022–2024 and diesel averaged $3.70/gal in 2024, raising operating expenses across the value chain.

With global carbon pricing coverage expanding to ~21% of emissions by 2025 and EU carbon price near €90/ton in 2025, suppliers commonly pass compliance costs to buyers.

Regal Rexnord must hedge energy, optimize routes, and push supplier contracts to protect margins; energy and freight cost increases could cut EBITDA margins several hundred basis points if unmitigated.

Supplier Consolidation Trends

The industrial supplier base has consolidated: the top 10 global bearing and motion-component suppliers now account for roughly 62% of market share (2024), giving larger vendors stronger leverage over pricing, payment terms, and lead times for specialized aerospace and medical parts.

Regal Rexnord offsets this by diversifying suppliers across North America, Europe, and Asia, reducing single-source exposure and shortening critical lead times by an estimated 12% vs 2021.

- Top-10 suppliers ≈62% market share (2024)

- Larger suppliers push stricter payment terms, longer lead times

- Supplier diversification across 3 regions

- Estimated 12% lead-time reduction since 2021

Vertical Integration and Hedging Strategies

Regal Rexnord offsets supplier power through hedging and internal manufacture of key components; by late 2025 internal production covered about 28% of high-value parts for powertrain lines, downshifting external buy dependency.

This vertical integration cut input cost volatility: rolling 12-month supplier price exposure dropped from ±9.4% in 2023 to ±3.2% by Q4 2025, improving schedule reliability and margin protection.

- 28% of high-value parts internalized by late 2025

- Supplier price exposure reduced to ±3.2% (Q4 2025)

- Improved on-time production for complex powertrains

Regal Rexnord shrinks supplier risk—28% integration trims price exposure to ±3.2%

Suppliers hold moderate-to-high power: commodity inputs (steel up ~12%, copper +9% YTD 2025) and concentrated high-performance IC vendors (70–80% from <5 suppliers) pressure margins; top-10 component suppliers control ~62% (2024). Regal Rexnord hedges, regional diversification and 28% vertical integration cut rolling price exposure to ±3.2% by Q4 2025, trimming lead times ~12% versus 2021.

| Metric | Value |

|---|---|

| Steel price change (2025 YTD) | +12% |

| Copper price change (2025 YTD) | +9% |

| High-performance IC concentration (2025) | 70–80% |

| Top-10 supplier share (2024) | 62% |

| Vertical integration (late 2025) | 28% |

| Price exposure (rolling 12m, Q4 2025) | ±3.2% |

| Lead-time reduction vs 2021 | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Regal Rexnord uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, plus strategic implications for pricing, margins, and market positioning.

A concise Porter's Five Forces summary for Regal Rexnord that highlights supplier, buyer, competitive, entrant, and substitute pressures—ideal for swift strategic decisions.

Customers Bargaining Power

High OEM Concentration in Key Segments

About 40% of Regal Rexnord’s 2024 revenue came from large OEMs in HVAC, food & beverage, and aerospace, giving these buyers outsized leverage over pricing and terms.

High-volume purchases and multiyear contracts mean OEMs can demand custom designs, extended warranties, and tiered pricing, pressuring gross margins (2024 gross margin 24.1%).

Loss of one major OEM (top 5 customers ~35% of sales) would materially hit revenue, so Regal negotiates concessions to secure long-term supply agreements.

Distribution Channel Influence

Industrial distributors drive aftermarket access and small-user sales, giving them outsized leverage on Regal Rexnord’s product placement and pricing; distributors accounted for roughly 28% of global industrial motor and gearbox channel sales in 2024. Regal Rexnord must offer better service levels and financial incentives to stay preferred, as many distributors stock rival brands like ABB and SEW‑Eurodrive. By end‑2025, distributor consolidation—top 10 distributors up 14% M&A since 2021—boosted rebate and payment-term negotiating power.

Switching Costs and Integration Depth

The highly engineered nature of Regal Rexnord’s industrial powertrains and motors creates high switching costs once integrated, with redesigns often taking 3–9 months and costing 5–15% of a plant upgrade budget; that technical lock‑in reduced customer churn to an estimated 2–4% annually in 2024.

Demand for Energy Efficiency and Sustainability

Customers now push for energy-efficient, sustainable motors to hit ESG targets and comply with tightening regs; by late 2025 procurement teams will demand IE4/IE5 efficiency at prices near standard IE3 levels, giving buyers more leverage.

Regal Rexnord must invest in IE4/IE5 R&D and scale production—otherwise it risks losing share to low-cost, high-efficiency rivals; FY2024 peers reported 5–8% margin premiums on IE4 lines, showing real financial pressure.

- Buyers favor IE4/IE5 by 2025

- Price parity expectation increases bargaining power

- Peers report 5–8% margin premium on high-efficiency lines

- Innovation and scale needed to retain share

Price Sensitivity in Commodity Product Lines

In Regal Rexnord’s commodity motor and component lines, buyers are highly price sensitive with low brand loyalty; industry data show price-driven churn of 12–18% annually in standardized motor segments (2024 US market study).

Customers switch for small savings, so Regal Rexnord emphasizes value-added features and digital monitoring (ABB-style condition monitoring adoption rose 22% 2023–24) to justify premium pricing and protect margins.

- Price-driven churn 12–18% (2024)

- Digital monitoring adoption +22% (2023–24)

- Value-adds used to sustain 3–5% higher ASP

Regal under pricing pressure: invest in efficiency R&D and digital value‑adds to defend ASP

Buyers hold high bargaining power: top OEMs (~40% of 2024 revenue; top 5 ≈35%) and distributors (~28% channel share) pressure pricing and terms, seeking IE4/IE5 at near‑IE3 prices; commodity buyers drive 12–18% churn. Regal must invest in efficiency R&D and digital value‑adds to protect a 3–5% ASP premium and avoid margin erosion (2024 gross margin 24.1%).

| Metric | 2024 |

|---|---|

| OEM share | ~40% |

| Top‑5 customer share | ~35% |

| Distributor channel | ~28% |

| Gross margin | 24.1% |

| Commodity churn | 12–18% |

Preview Before You Purchase

Regal Rexnord Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Regal Rexnord you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file ready for download and use the moment you buy, containing supplier power, buyer power, competitive rivalry, threat of entry, and substitute analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Regal Rexnord faces moderate supplier power, pricing pressure from industrial buyers, and steady rivalry as consolidation and aftermarket services shape competitive dynamics.

Barriers to entry are mixed—capital-intensive manufacturing deters newcomers, but niche tech and service models could erode share, while substitutes and digitalization slowly shift value propositions.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Regal Rexnord’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Raw Material Commodity Volatility

Regal Rexnord depends on steel, copper, aluminum and rare-earth magnets for motors and powertrains, and by end-2025 global shifts and trade policies kept price volatility high—steel up ~12% and copper up ~9% year-to-date in 2025. Because these commodities trade on global exchanges (LME, SHFE), Regal Rexnord has limited ability to move market prices, though its 2024 procurement volume (~$1.6bn materials spend) secures modest volume discounts. High input-price volatility raises margin pressure and forces tighter working-capital management and hedging use.

Specialized Electronic Component Sourcing

The shift to smart sensors and digital controls means Regal Rexnord needs specialized semiconductors and electronics from a small set of global suppliers; industry data shows 70–80% of high-performance motion-control ICs come from fewer than five vendors as of 2025, giving those suppliers pricing and lead-time power. This concentration raises supplier bargaining leverage, pressuring margins and forcing Regal Rexnord to absorb higher input costs or invest in dual sourcing and inventory buffers to avoid production delays.

Energy and Logistics Cost Pressures

Suppliers for energy-intensive processes and logistics pressure Regal Rexnord via volatile costs—benchmark electricity rose ~12% in US industrial rates 2022–2024 and diesel averaged $3.70/gal in 2024, raising operating expenses across the value chain.

With global carbon pricing coverage expanding to ~21% of emissions by 2025 and EU carbon price near €90/ton in 2025, suppliers commonly pass compliance costs to buyers.

Regal Rexnord must hedge energy, optimize routes, and push supplier contracts to protect margins; energy and freight cost increases could cut EBITDA margins several hundred basis points if unmitigated.

Supplier Consolidation Trends

The industrial supplier base has consolidated: the top 10 global bearing and motion-component suppliers now account for roughly 62% of market share (2024), giving larger vendors stronger leverage over pricing, payment terms, and lead times for specialized aerospace and medical parts.

Regal Rexnord offsets this by diversifying suppliers across North America, Europe, and Asia, reducing single-source exposure and shortening critical lead times by an estimated 12% vs 2021.

- Top-10 suppliers ≈62% market share (2024)

- Larger suppliers push stricter payment terms, longer lead times

- Supplier diversification across 3 regions

- Estimated 12% lead-time reduction since 2021

Vertical Integration and Hedging Strategies

Regal Rexnord offsets supplier power through hedging and internal manufacture of key components; by late 2025 internal production covered about 28% of high-value parts for powertrain lines, downshifting external buy dependency.

This vertical integration cut input cost volatility: rolling 12-month supplier price exposure dropped from ±9.4% in 2023 to ±3.2% by Q4 2025, improving schedule reliability and margin protection.

- 28% of high-value parts internalized by late 2025

- Supplier price exposure reduced to ±3.2% (Q4 2025)

- Improved on-time production for complex powertrains

Regal Rexnord shrinks supplier risk—28% integration trims price exposure to ±3.2%

Suppliers hold moderate-to-high power: commodity inputs (steel up ~12%, copper +9% YTD 2025) and concentrated high-performance IC vendors (70–80% from <5 suppliers) pressure margins; top-10 component suppliers control ~62% (2024). Regal Rexnord hedges, regional diversification and 28% vertical integration cut rolling price exposure to ±3.2% by Q4 2025, trimming lead times ~12% versus 2021.

| Metric | Value |

|---|---|

| Steel price change (2025 YTD) | +12% |

| Copper price change (2025 YTD) | +9% |

| High-performance IC concentration (2025) | 70–80% |

| Top-10 supplier share (2024) | 62% |

| Vertical integration (late 2025) | 28% |

| Price exposure (rolling 12m, Q4 2025) | ±3.2% |

| Lead-time reduction vs 2021 | ~12% |

What is included in the product

Tailored Porter's Five Forces analysis for Regal Rexnord uncovering competitive intensity, buyer and supplier leverage, threat of substitutes and new entrants, plus strategic implications for pricing, margins, and market positioning.

A concise Porter's Five Forces summary for Regal Rexnord that highlights supplier, buyer, competitive, entrant, and substitute pressures—ideal for swift strategic decisions.

Customers Bargaining Power

High OEM Concentration in Key Segments

About 40% of Regal Rexnord’s 2024 revenue came from large OEMs in HVAC, food & beverage, and aerospace, giving these buyers outsized leverage over pricing and terms.

High-volume purchases and multiyear contracts mean OEMs can demand custom designs, extended warranties, and tiered pricing, pressuring gross margins (2024 gross margin 24.1%).

Loss of one major OEM (top 5 customers ~35% of sales) would materially hit revenue, so Regal negotiates concessions to secure long-term supply agreements.

Distribution Channel Influence

Industrial distributors drive aftermarket access and small-user sales, giving them outsized leverage on Regal Rexnord’s product placement and pricing; distributors accounted for roughly 28% of global industrial motor and gearbox channel sales in 2024. Regal Rexnord must offer better service levels and financial incentives to stay preferred, as many distributors stock rival brands like ABB and SEW‑Eurodrive. By end‑2025, distributor consolidation—top 10 distributors up 14% M&A since 2021—boosted rebate and payment-term negotiating power.

Switching Costs and Integration Depth

The highly engineered nature of Regal Rexnord’s industrial powertrains and motors creates high switching costs once integrated, with redesigns often taking 3–9 months and costing 5–15% of a plant upgrade budget; that technical lock‑in reduced customer churn to an estimated 2–4% annually in 2024.

Demand for Energy Efficiency and Sustainability

Customers now push for energy-efficient, sustainable motors to hit ESG targets and comply with tightening regs; by late 2025 procurement teams will demand IE4/IE5 efficiency at prices near standard IE3 levels, giving buyers more leverage.

Regal Rexnord must invest in IE4/IE5 R&D and scale production—otherwise it risks losing share to low-cost, high-efficiency rivals; FY2024 peers reported 5–8% margin premiums on IE4 lines, showing real financial pressure.

- Buyers favor IE4/IE5 by 2025

- Price parity expectation increases bargaining power

- Peers report 5–8% margin premium on high-efficiency lines

- Innovation and scale needed to retain share

Price Sensitivity in Commodity Product Lines

In Regal Rexnord’s commodity motor and component lines, buyers are highly price sensitive with low brand loyalty; industry data show price-driven churn of 12–18% annually in standardized motor segments (2024 US market study).

Customers switch for small savings, so Regal Rexnord emphasizes value-added features and digital monitoring (ABB-style condition monitoring adoption rose 22% 2023–24) to justify premium pricing and protect margins.

- Price-driven churn 12–18% (2024)

- Digital monitoring adoption +22% (2023–24)

- Value-adds used to sustain 3–5% higher ASP

Regal under pricing pressure: invest in efficiency R&D and digital value‑adds to defend ASP

Buyers hold high bargaining power: top OEMs (~40% of 2024 revenue; top 5 ≈35%) and distributors (~28% channel share) pressure pricing and terms, seeking IE4/IE5 at near‑IE3 prices; commodity buyers drive 12–18% churn. Regal must invest in efficiency R&D and digital value‑adds to protect a 3–5% ASP premium and avoid margin erosion (2024 gross margin 24.1%).

| Metric | 2024 |

|---|---|

| OEM share | ~40% |

| Top‑5 customer share | ~35% |

| Distributor channel | ~28% |

| Gross margin | 24.1% |

| Commodity churn | 12–18% |

Preview Before You Purchase

Regal Rexnord Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Regal Rexnord you’ll receive immediately after purchase—no placeholders, no mockups.

The document displayed here is the full, professionally formatted file ready for download and use the moment you buy, containing supplier power, buyer power, competitive rivalry, threat of entry, and substitute analysis.