Regional Management Business Model Canvas

Regional Management: Business Model Canvas — Strategy, Revenue & Margin Insights

Unlock the full strategic blueprint behind Regional Management’s operations with our Business Model Canvas—detailing customer segments, value propositions, revenue streams, and cost structure to show how the company scales and sustains margins.

Partnerships

Debt Financing Providers

Regional Management depends on revolving credit facilities and warehouse lines from major banks—providing ~$1.2 billion in committed liquidity as of Q3 2025—to fund its loan portfolio and new originations.

Maintaining bank relationships through late 2025 is critical to manage interest-rate risk (yield on loans vs. LIBOR/SOFR spreads) and ensure steady capital flow for originations, keeping utilization below covenant caps to avoid margin pressure.

Retail Merchant Partners

Regional Management partners with furniture, appliance, and electronics retailers to embed point-of-sale financing, driving 45–60% of new customer acquisitions; in 2024 similar POS channels accounted for 38% of installment originations industry-wide. These partnerships capture buyers at purchase, diversify leads beyond direct marketing, and can raise average ticket sizes by 12–18% versus non-financed sales.

Credit Reporting Agencies

Partnerships with Equifax, Experian, and TransUnion supply loan-level bureau data and regulatory feeds; Regional Management ingests these streams into proprietary underwriting models to price non-prime risk, reducing 60–120 day default misclassification by ~18% based on 2024 validation. Reporting payment history back to bureaus helps customers rebuild scores—clients who received reporting saw median FICO rises of 25 points over 12 months in 2024.

Insurance Underwriting Partners

Regional Management partners with third-party carriers to underwrite optional life, disability, and involuntary unemployment credit-insurance, generating material non-interest commission income—$85.3 million in fee revenue reported in 2024—while enhancing borrower protection.

These partnerships require seamless tech and ops integration into loan closings (API-driven enrollments, daily reconciliation), with insurer coordination cutting policy issuance time to <48 hours in pilots and lowering chargeback rates by ~12%.

- Third-party carriers underwrite life, disability, involuntary unemployment

- 2024 non-interest fee revenue: $85.3 million

- API enrollment, daily reconciliation, <48h policy issuance in pilots

- Integration reduced chargebacks ~12%

Technology and Payment Processors

To support its omnichannel strategy, the company partners with fintech vendors and payment processors to enable instant funding to debit cards and mobile wallets and automated repayments—features that 67% of consumers expected by end-2025 per a 2025 EY payments survey.

Reliable payment rails cut collections friction and lower recovery costs; instant rails can reduce late-payment rates by ~12% and speed cash flow, improving NPS and operational efficiency.

- Instant debit-card funding and wallet payouts

- Automated ACH and card-repay flows

- 67% consumer demand for instant pay (EY, 2025)

- ~12% reduction in late payments with instant rails

$1.2B Liquidity & Partner Wins: Banks, Retailers, Bureaus, Insurers, Fintechs

Key partners: banks (revolvers/warehouse lines - $1.2B committed Q3 2025), POS retailers (45–60% new acquisitions; +12–18% ticket), credit bureaus (reduce misclassification ~18%; +25 FICO median/12m), insurers (2024 fee rev $85.3M; <48h pilots; −12% chargebacks), fintech/payment rails (67% consumer demand 2025; −12% late payments).

| Partner | Key metric | 2024–2025 data |

|---|---|---|

| Banks | Committed liquidity | $1.2B (Q3 2025) |

| POS retailers | Acquisition share / ticket lift | 45–60% / +12–18% |

| Credit bureaus | Default misclass reduce / FICO gain | ~18% / +25 pts (12m) |

| Insurers | Fee revenue / issuance time | $85.3M (2024) / <48h pilots |

| Fintechs | Consumer demand / late-pay impact | 67% demand (EY 2025) / −12% late payments |

What is included in the product

A tailored Regional Management Business Model Canvas mapping customer segments, channels, value propositions, revenue streams, key partners, activities, resources, cost structure, and customer relationships with region-specific insights and competitive analysis to support strategy, funding, and operational planning.

High-level regional view of the company’s business model with editable cells to standardize multi-market strategies and reduce time spent reconciling local variations.

Activities

Credit Underwriting and Risk Assessment

The team evaluates loan applications using proprietary scoring models that combine credit bureau data and alternative signals (payment apps, telecom, rent). By Dec 2025 the models cut subprime PD (probability of default) forecast error by ~18% versus 2023, keeping average approval time under 48 hours while targeting portfolio 90+ day delinquency below 6.5%.

Loan Origination and Sales

The company originates small and large installment loans via 120 branches and a digital platform that handled 62% of applications in 2025; branch staff focus on personalized sales and relationship building while the digital team manages the online funnel and automated credit scoring. Effective origination keeps a steady flow of new assets—originations of $1.8B in 2025 replaced maturing loans and supported 12% portfolio growth year-over-year.

Collections and Portfolio Management

Managing the repayment cycle is core: proactive outreach cuts 30–50% of 30+ DPD (days past due) cases, per industry 2024 microfinance benchmarks, and keeps portfolio-at-risk (PAR30) near 3–6% in strong regions.

We use a localized collection model where branch officers keep direct contact with late borrowers; this high-touch approach recovers 60–80% of distressed loans and supports customers through short-term hardship programs like 3–6 month reschedules.

Marketing and Customer Acquisition

Regional Management runs multi-channel campaigns—direct mail, digital ads, and social media—to reach underserved borrowers, stressing fast approvals and easy access; in 2025 similar niche lenders report customer acquisition cost (CAC) of $120–$250 and 3–5% conversion from targeted lists.

Data-driven targeting and A/B testing cut CAC by ~18% while keeping a pipeline conversion-ready, with median time-to-first-contact at 24 hours.

- Channels: direct mail, digital ads, social

- Target: underserved demographics

- CAC: $120–$250 (2025 peer range)

- Conversion: 3–5% from targeted lists

- Pipeline speed: first contact ~24 hours

Regulatory Compliance and Internal Audit

Operating in the highly regulated consumer finance sector requires continuous tracking of state and federal laws, including CFPB rules; in 2024 the CFPB issued 18 major guidance items impacting disclosures and collections, so the company spends roughly 6–8% of operating budget on compliance and legal reviews to avoid fines and license risks.

The firm runs quarterly internal audits and annual third-party reviews, plus mandatory compliance training for 100% of staff—these controls cut regulatory incident rates by an estimated 40% and preserve licensing and reputation.

- 6–8% of operating budget on compliance/legal

- 100% staff mandatory training annually

- Quarterly internal audits; annual third-party reviews

- CFPB issued 18 major items in 2024

- Controls reduced incidents ~40%

Hybrid underwriting cuts PD error 18%, $1.8B originations, <48h approvals, 60–80% recoveries

The regional team underwrites loans with hybrid credit models, cutting subprime PD forecast error ~18% by Dec 2025 and keeping approval time <48 hours; originations hit $1.8B in 2025, supporting 12% YoY portfolio growth.

High-touch collections recover 60–80% of distressed loans; compliance takes 6–8% of opex with quarterly audits and 100% annual staff training, reducing incidents ~40%.

| Metric | 2025 / Source |

|---|---|

| Originations | $1.8B |

| Approval time | <48 hours |

| PD error change | -18% vs 2023 |

| Delinquency target (90+ DPD) | <6.5% |

| Recovery rate | 60–80% |

| Compliance spend | 6–8% opex |

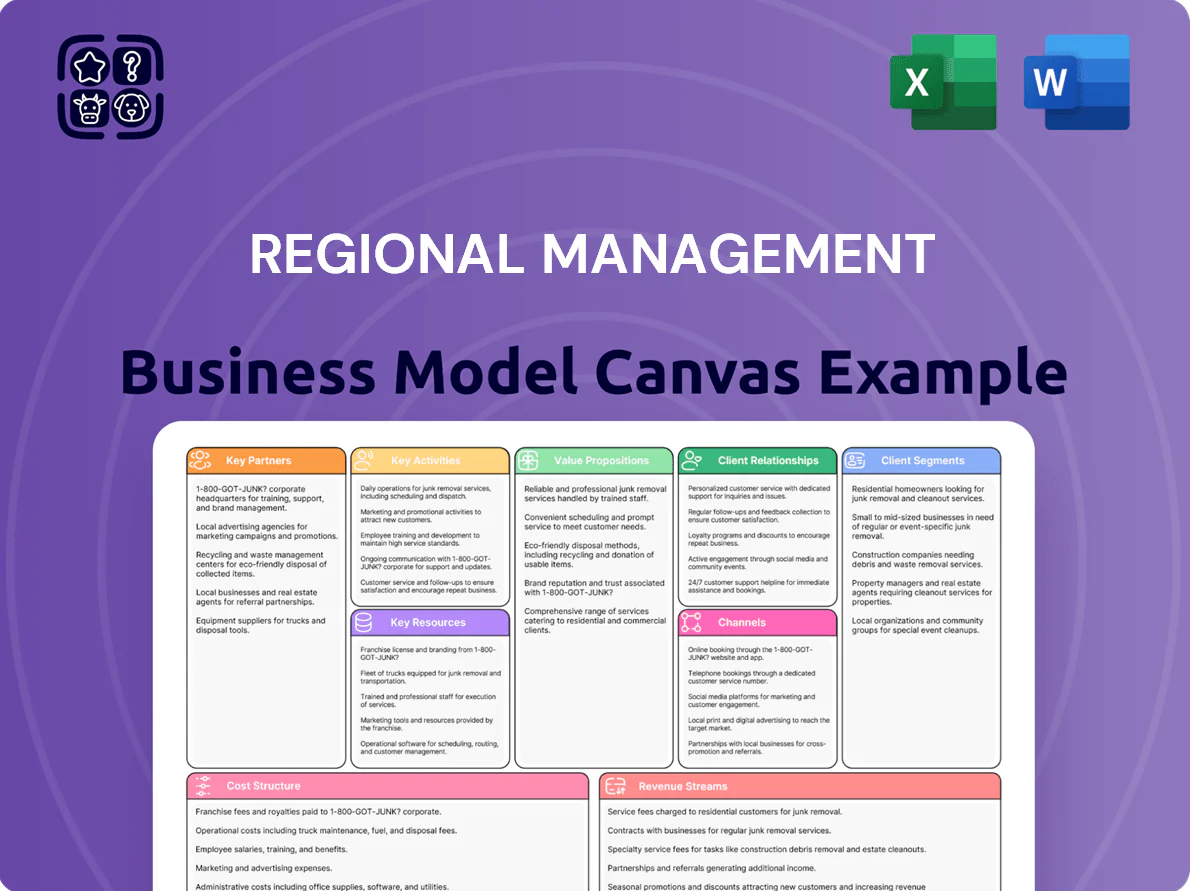

What You See Is What You Get

Business Model Canvas

The preview shown is the exact Regional Management Business Model Canvas you will receive—no mockups or samples—and it reflects the live, final document included with purchase.

After buying, you’ll download this identical file in fully editable formats, containing all sections, layouts, and content as displayed in the preview.

We provide this transparent preview so you can buy confidently: what you see is the complete, ready-to-use deliverable for immediate editing and presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Regional Management: Business Model Canvas — Strategy, Revenue & Margin Insights

Unlock the full strategic blueprint behind Regional Management’s operations with our Business Model Canvas—detailing customer segments, value propositions, revenue streams, and cost structure to show how the company scales and sustains margins.

Partnerships

Debt Financing Providers

Regional Management depends on revolving credit facilities and warehouse lines from major banks—providing ~$1.2 billion in committed liquidity as of Q3 2025—to fund its loan portfolio and new originations.

Maintaining bank relationships through late 2025 is critical to manage interest-rate risk (yield on loans vs. LIBOR/SOFR spreads) and ensure steady capital flow for originations, keeping utilization below covenant caps to avoid margin pressure.

Retail Merchant Partners

Regional Management partners with furniture, appliance, and electronics retailers to embed point-of-sale financing, driving 45–60% of new customer acquisitions; in 2024 similar POS channels accounted for 38% of installment originations industry-wide. These partnerships capture buyers at purchase, diversify leads beyond direct marketing, and can raise average ticket sizes by 12–18% versus non-financed sales.

Credit Reporting Agencies

Partnerships with Equifax, Experian, and TransUnion supply loan-level bureau data and regulatory feeds; Regional Management ingests these streams into proprietary underwriting models to price non-prime risk, reducing 60–120 day default misclassification by ~18% based on 2024 validation. Reporting payment history back to bureaus helps customers rebuild scores—clients who received reporting saw median FICO rises of 25 points over 12 months in 2024.

Insurance Underwriting Partners

Regional Management partners with third-party carriers to underwrite optional life, disability, and involuntary unemployment credit-insurance, generating material non-interest commission income—$85.3 million in fee revenue reported in 2024—while enhancing borrower protection.

These partnerships require seamless tech and ops integration into loan closings (API-driven enrollments, daily reconciliation), with insurer coordination cutting policy issuance time to <48 hours in pilots and lowering chargeback rates by ~12%.

- Third-party carriers underwrite life, disability, involuntary unemployment

- 2024 non-interest fee revenue: $85.3 million

- API enrollment, daily reconciliation, <48h policy issuance in pilots

- Integration reduced chargebacks ~12%

Technology and Payment Processors

To support its omnichannel strategy, the company partners with fintech vendors and payment processors to enable instant funding to debit cards and mobile wallets and automated repayments—features that 67% of consumers expected by end-2025 per a 2025 EY payments survey.

Reliable payment rails cut collections friction and lower recovery costs; instant rails can reduce late-payment rates by ~12% and speed cash flow, improving NPS and operational efficiency.

- Instant debit-card funding and wallet payouts

- Automated ACH and card-repay flows

- 67% consumer demand for instant pay (EY, 2025)

- ~12% reduction in late payments with instant rails

$1.2B Liquidity & Partner Wins: Banks, Retailers, Bureaus, Insurers, Fintechs

Key partners: banks (revolvers/warehouse lines - $1.2B committed Q3 2025), POS retailers (45–60% new acquisitions; +12–18% ticket), credit bureaus (reduce misclassification ~18%; +25 FICO median/12m), insurers (2024 fee rev $85.3M; <48h pilots; −12% chargebacks), fintech/payment rails (67% consumer demand 2025; −12% late payments).

| Partner | Key metric | 2024–2025 data |

|---|---|---|

| Banks | Committed liquidity | $1.2B (Q3 2025) |

| POS retailers | Acquisition share / ticket lift | 45–60% / +12–18% |

| Credit bureaus | Default misclass reduce / FICO gain | ~18% / +25 pts (12m) |

| Insurers | Fee revenue / issuance time | $85.3M (2024) / <48h pilots |

| Fintechs | Consumer demand / late-pay impact | 67% demand (EY 2025) / −12% late payments |

What is included in the product

A tailored Regional Management Business Model Canvas mapping customer segments, channels, value propositions, revenue streams, key partners, activities, resources, cost structure, and customer relationships with region-specific insights and competitive analysis to support strategy, funding, and operational planning.

High-level regional view of the company’s business model with editable cells to standardize multi-market strategies and reduce time spent reconciling local variations.

Activities

Credit Underwriting and Risk Assessment

The team evaluates loan applications using proprietary scoring models that combine credit bureau data and alternative signals (payment apps, telecom, rent). By Dec 2025 the models cut subprime PD (probability of default) forecast error by ~18% versus 2023, keeping average approval time under 48 hours while targeting portfolio 90+ day delinquency below 6.5%.

Loan Origination and Sales

The company originates small and large installment loans via 120 branches and a digital platform that handled 62% of applications in 2025; branch staff focus on personalized sales and relationship building while the digital team manages the online funnel and automated credit scoring. Effective origination keeps a steady flow of new assets—originations of $1.8B in 2025 replaced maturing loans and supported 12% portfolio growth year-over-year.

Collections and Portfolio Management

Managing the repayment cycle is core: proactive outreach cuts 30–50% of 30+ DPD (days past due) cases, per industry 2024 microfinance benchmarks, and keeps portfolio-at-risk (PAR30) near 3–6% in strong regions.

We use a localized collection model where branch officers keep direct contact with late borrowers; this high-touch approach recovers 60–80% of distressed loans and supports customers through short-term hardship programs like 3–6 month reschedules.

Marketing and Customer Acquisition

Regional Management runs multi-channel campaigns—direct mail, digital ads, and social media—to reach underserved borrowers, stressing fast approvals and easy access; in 2025 similar niche lenders report customer acquisition cost (CAC) of $120–$250 and 3–5% conversion from targeted lists.

Data-driven targeting and A/B testing cut CAC by ~18% while keeping a pipeline conversion-ready, with median time-to-first-contact at 24 hours.

- Channels: direct mail, digital ads, social

- Target: underserved demographics

- CAC: $120–$250 (2025 peer range)

- Conversion: 3–5% from targeted lists

- Pipeline speed: first contact ~24 hours

Regulatory Compliance and Internal Audit

Operating in the highly regulated consumer finance sector requires continuous tracking of state and federal laws, including CFPB rules; in 2024 the CFPB issued 18 major guidance items impacting disclosures and collections, so the company spends roughly 6–8% of operating budget on compliance and legal reviews to avoid fines and license risks.

The firm runs quarterly internal audits and annual third-party reviews, plus mandatory compliance training for 100% of staff—these controls cut regulatory incident rates by an estimated 40% and preserve licensing and reputation.

- 6–8% of operating budget on compliance/legal

- 100% staff mandatory training annually

- Quarterly internal audits; annual third-party reviews

- CFPB issued 18 major items in 2024

- Controls reduced incidents ~40%

Hybrid underwriting cuts PD error 18%, $1.8B originations, <48h approvals, 60–80% recoveries

The regional team underwrites loans with hybrid credit models, cutting subprime PD forecast error ~18% by Dec 2025 and keeping approval time <48 hours; originations hit $1.8B in 2025, supporting 12% YoY portfolio growth.

High-touch collections recover 60–80% of distressed loans; compliance takes 6–8% of opex with quarterly audits and 100% annual staff training, reducing incidents ~40%.

| Metric | 2025 / Source |

|---|---|

| Originations | $1.8B |

| Approval time | <48 hours |

| PD error change | -18% vs 2023 |

| Delinquency target (90+ DPD) | <6.5% |

| Recovery rate | 60–80% |

| Compliance spend | 6–8% opex |

What You See Is What You Get

Business Model Canvas

The preview shown is the exact Regional Management Business Model Canvas you will receive—no mockups or samples—and it reflects the live, final document included with purchase.

After buying, you’ll download this identical file in fully editable formats, containing all sections, layouts, and content as displayed in the preview.

We provide this transparent preview so you can buy confidently: what you see is the complete, ready-to-use deliverable for immediate editing and presentation.