Regions Financial Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

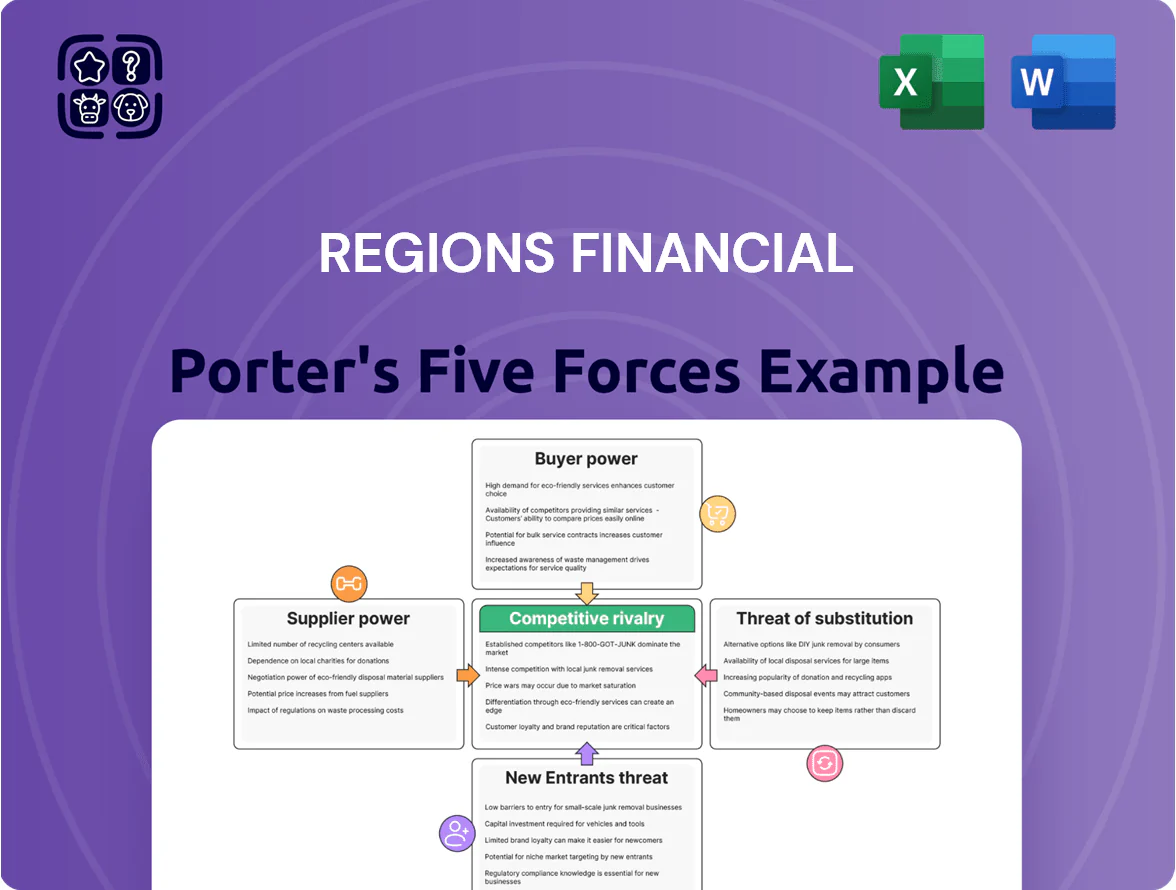

Regions Financial faces moderate buyer power, intense rivalry among regional banks, and regulatory hurdles that shape margins and strategy, while digital entrants raise the threat of substitutes and scale limits new-entrant impact.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Regions Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of Deposits and Capital Providers

Specialized Financial Technology Vendors

Regions relies on third-party core-banking, cloud, and cyber vendors; switching these platforms can exceed hundreds of millions in migration costs and 18–24 months of downtime risk, so vendors keep strong leverage at renewal.

With the top 5 tech conglomerates controlling ~60% of enterprise cloud and security spend by 2024, Regions faces steep pricing pressure while needing digital upgrades to avoid losing retail and commercial customers.

Skilled Labor and Specialized Talent

The market for financial professionals in data analytics, wealth management, and compliance is tight across the South and Midwest; Regions Financial competes with megabanks and fintechs, pushing median tech-pay up ~12% year-over-year and raising total compensation per specialist to roughly $140k in 2025, per industry surveys. This talent squeeze increases operating expenses and constrains scalability, making skilled labor a meaningful supplier-side bottleneck for Regions.

Regulatory and Compliance Service Providers

- Dependence: SEC and Basel III compliance

- Bargaining power: high due to niche expertise

- Price pressure: Big Four rates +8–12% (2023–25)

- Negotiation limit: avoid fines/reputation loss

Access to Wholesale Funding Markets

Regions relies on wholesale funding and Federal Home Loan Bank advances alongside retail deposits; at YE 2024 wholesale borrowings were about $24.3 billion, supplementing liquidity needs.

Availability and pricing hinge on macro rates and ratings; a one-notch downgrade in 2023 would have raised funding spreads by ~30–60 bps, based on bank market data.

If Regions’ credit profile weakens, institutional lenders can demand much higher premiums, lifting the bank’s cost of funds and squeezing net interest margin.

- Wholesale borrowings: $24.3B (YE 2024)

- FHLB access: key liquidity backstop

- One-notch downgrade ≈ +30–60 bps funding spread

- Higher premiums → lower net interest margin

Deposit-driven funding strain, rising wholesale costs and supplier concentration risk

| Metric | Value |

|---|---|

| Deposits | $120B (Q3 2025) |

| Deposit share | ~70% |

| NIM | 2.45% FY2025 |

| Wholesale | $24.3B YE2024 |

What is included in the product

Tailored Porter’s Five Forces analysis for Regions Financial that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

One-sheet Porter’s Five Forces for Regions Financial—quickly visualize competitive pressure and regulatory risk to guide capital allocation and branch strategy decisions.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

In 2025, with instant transfers and account opening via mobile apps, retail customers can shift deposits in minutes, so Regions must keep fees low and digital service high to limit churn; FDIC data shows 45% of consumers switched at least one financial service in 2024. Customer loyalty now hinges on app experience and uptime—Regions’ Net Promoter Score and digital transaction costs are key battlegrounds as basic checking/savings have become commoditized.

Price Sensitivity of Commercial Borrowers

Middle-market and corporate clients routinely invite bids from multiple banks, letting them push spreads down; in 2024 syndicated loan pricing show average institutional middle-market spreads near 250–300 bps, pressuring Regions to match offers.

These sophisticated borrowers secure tighter covenants and fees by pitting regional and national lenders against each other, forcing Regions to concede margin to win deals.

Keeping high-quality commercial relationships is strategic: top 20% of commercial clients generate roughly 60% of fee and interest income, so Regions often trade short-term yield for long-term revenue.

Transparency and Rate Comparison Tools

The rise of online aggregators like Bankrate and NerdWallet lets customers compare mortgage rates, CD yields, and loan APRs in real time; by 2024, 63% of US consumers used rate-comparison tools for major financial decisions, per J.D. Power. This transparency cuts banks’ information advantage and compresses margins—Regions faced pressure as average savings yields rose 20 bps in 2023–24. Well-informed customers now hold more negotiating leverage at acquisition.

Demand for Integrated Wealth Management

- HNWI wealth $84.6T (2024)

- 28% US HNWI use multi-advisor setups (2023)

- Need: bundled services at lower fees

Influence of Small Business Ecosystems

Small business owners in Regions Financial’s footprint demand tailored lending, integrated payroll, and merchant services; by 2024 SMB deposits represented roughly 18% of regional deposits, so losing them would dent core revenue.

As SMBs scale, their bargaining power increases; 42% of mid‑market SMBs surveyed in 2024 negotiated lower merchant fees or bespoke credit lines, pressuring Regions to match pricing and product flexibility.

If Regions fails to offer specialized credit lines and competitive transaction fees, fintechs (which captured about 16% of SMB payments volume in 2024) can erode its regional economic base.

- SMB deposits ≈18% of regional deposits (2024)

- 42% mid‑market SMBs negotiated fees/credit (2024)

- Fintechs captured ~16% SMB payments volume (2024)

Customers Power Fee Compression: Switches, HNW Multi-Advisor Use & Fintech SMB Share

Customers hold high bargaining power: retail users can switch accounts in minutes (45% switched a service in 2024), HNWIs control large investable pools ($84.6T in 2024) and 28% use multi-advisor models, SMBs supply ~18% of deposits and 42% negotiated fees in 2024, while fintechs took ~16% SMB payments—forcing Regions to compress fees and invest in digital service.

| Metric | Value (Year) |

|---|---|

| Retail switch rate | 45% (2024) |

| HNWI investable wealth | $84.6T (2024) |

| HNWI multi-advisor | 28% (2023) |

| SMB deposit share | ~18% (2024) |

| SMB negotiated fees | 42% (2024) |

| Fintech SMB payments | ~16% (2024) |

Preview Before You Purchase

Regions Financial Porter's Five Forces Analysis

This preview shows the exact Regions Financial Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Regions Financial faces moderate buyer power, intense rivalry among regional banks, and regulatory hurdles that shape margins and strategy, while digital entrants raise the threat of substitutes and scale limits new-entrant impact.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Regions Financial’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Cost of Deposits and Capital Providers

Specialized Financial Technology Vendors

Regions relies on third-party core-banking, cloud, and cyber vendors; switching these platforms can exceed hundreds of millions in migration costs and 18–24 months of downtime risk, so vendors keep strong leverage at renewal.

With the top 5 tech conglomerates controlling ~60% of enterprise cloud and security spend by 2024, Regions faces steep pricing pressure while needing digital upgrades to avoid losing retail and commercial customers.

Skilled Labor and Specialized Talent

The market for financial professionals in data analytics, wealth management, and compliance is tight across the South and Midwest; Regions Financial competes with megabanks and fintechs, pushing median tech-pay up ~12% year-over-year and raising total compensation per specialist to roughly $140k in 2025, per industry surveys. This talent squeeze increases operating expenses and constrains scalability, making skilled labor a meaningful supplier-side bottleneck for Regions.

Regulatory and Compliance Service Providers

- Dependence: SEC and Basel III compliance

- Bargaining power: high due to niche expertise

- Price pressure: Big Four rates +8–12% (2023–25)

- Negotiation limit: avoid fines/reputation loss

Access to Wholesale Funding Markets

Regions relies on wholesale funding and Federal Home Loan Bank advances alongside retail deposits; at YE 2024 wholesale borrowings were about $24.3 billion, supplementing liquidity needs.

Availability and pricing hinge on macro rates and ratings; a one-notch downgrade in 2023 would have raised funding spreads by ~30–60 bps, based on bank market data.

If Regions’ credit profile weakens, institutional lenders can demand much higher premiums, lifting the bank’s cost of funds and squeezing net interest margin.

- Wholesale borrowings: $24.3B (YE 2024)

- FHLB access: key liquidity backstop

- One-notch downgrade ≈ +30–60 bps funding spread

- Higher premiums → lower net interest margin

Deposit-driven funding strain, rising wholesale costs and supplier concentration risk

| Metric | Value |

|---|---|

| Deposits | $120B (Q3 2025) |

| Deposit share | ~70% |

| NIM | 2.45% FY2025 |

| Wholesale | $24.3B YE2024 |

What is included in the product

Tailored Porter’s Five Forces analysis for Regions Financial that uncovers competitive drivers, customer and supplier influence, entry barriers, substitutes, and disruptive threats to inform strategic decisions and investor materials.

One-sheet Porter’s Five Forces for Regions Financial—quickly visualize competitive pressure and regulatory risk to guide capital allocation and branch strategy decisions.

Customers Bargaining Power

Low Switching Costs for Retail Consumers

In 2025, with instant transfers and account opening via mobile apps, retail customers can shift deposits in minutes, so Regions must keep fees low and digital service high to limit churn; FDIC data shows 45% of consumers switched at least one financial service in 2024. Customer loyalty now hinges on app experience and uptime—Regions’ Net Promoter Score and digital transaction costs are key battlegrounds as basic checking/savings have become commoditized.

Price Sensitivity of Commercial Borrowers

Middle-market and corporate clients routinely invite bids from multiple banks, letting them push spreads down; in 2024 syndicated loan pricing show average institutional middle-market spreads near 250–300 bps, pressuring Regions to match offers.

These sophisticated borrowers secure tighter covenants and fees by pitting regional and national lenders against each other, forcing Regions to concede margin to win deals.

Keeping high-quality commercial relationships is strategic: top 20% of commercial clients generate roughly 60% of fee and interest income, so Regions often trade short-term yield for long-term revenue.

Transparency and Rate Comparison Tools

The rise of online aggregators like Bankrate and NerdWallet lets customers compare mortgage rates, CD yields, and loan APRs in real time; by 2024, 63% of US consumers used rate-comparison tools for major financial decisions, per J.D. Power. This transparency cuts banks’ information advantage and compresses margins—Regions faced pressure as average savings yields rose 20 bps in 2023–24. Well-informed customers now hold more negotiating leverage at acquisition.

Demand for Integrated Wealth Management

- HNWI wealth $84.6T (2024)

- 28% US HNWI use multi-advisor setups (2023)

- Need: bundled services at lower fees

Influence of Small Business Ecosystems

Small business owners in Regions Financial’s footprint demand tailored lending, integrated payroll, and merchant services; by 2024 SMB deposits represented roughly 18% of regional deposits, so losing them would dent core revenue.

As SMBs scale, their bargaining power increases; 42% of mid‑market SMBs surveyed in 2024 negotiated lower merchant fees or bespoke credit lines, pressuring Regions to match pricing and product flexibility.

If Regions fails to offer specialized credit lines and competitive transaction fees, fintechs (which captured about 16% of SMB payments volume in 2024) can erode its regional economic base.

- SMB deposits ≈18% of regional deposits (2024)

- 42% mid‑market SMBs negotiated fees/credit (2024)

- Fintechs captured ~16% SMB payments volume (2024)

Customers Power Fee Compression: Switches, HNW Multi-Advisor Use & Fintech SMB Share

Customers hold high bargaining power: retail users can switch accounts in minutes (45% switched a service in 2024), HNWIs control large investable pools ($84.6T in 2024) and 28% use multi-advisor models, SMBs supply ~18% of deposits and 42% negotiated fees in 2024, while fintechs took ~16% SMB payments—forcing Regions to compress fees and invest in digital service.

| Metric | Value (Year) |

|---|---|

| Retail switch rate | 45% (2024) |

| HNWI investable wealth | $84.6T (2024) |

| HNWI multi-advisor | 28% (2023) |

| SMB deposit share | ~18% (2024) |

| SMB negotiated fees | 42% (2024) |

| Fintech SMB payments | ~16% (2024) |

Preview Before You Purchase

Regions Financial Porter's Five Forces Analysis

This preview shows the exact Regions Financial Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.