Reka Industrial PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

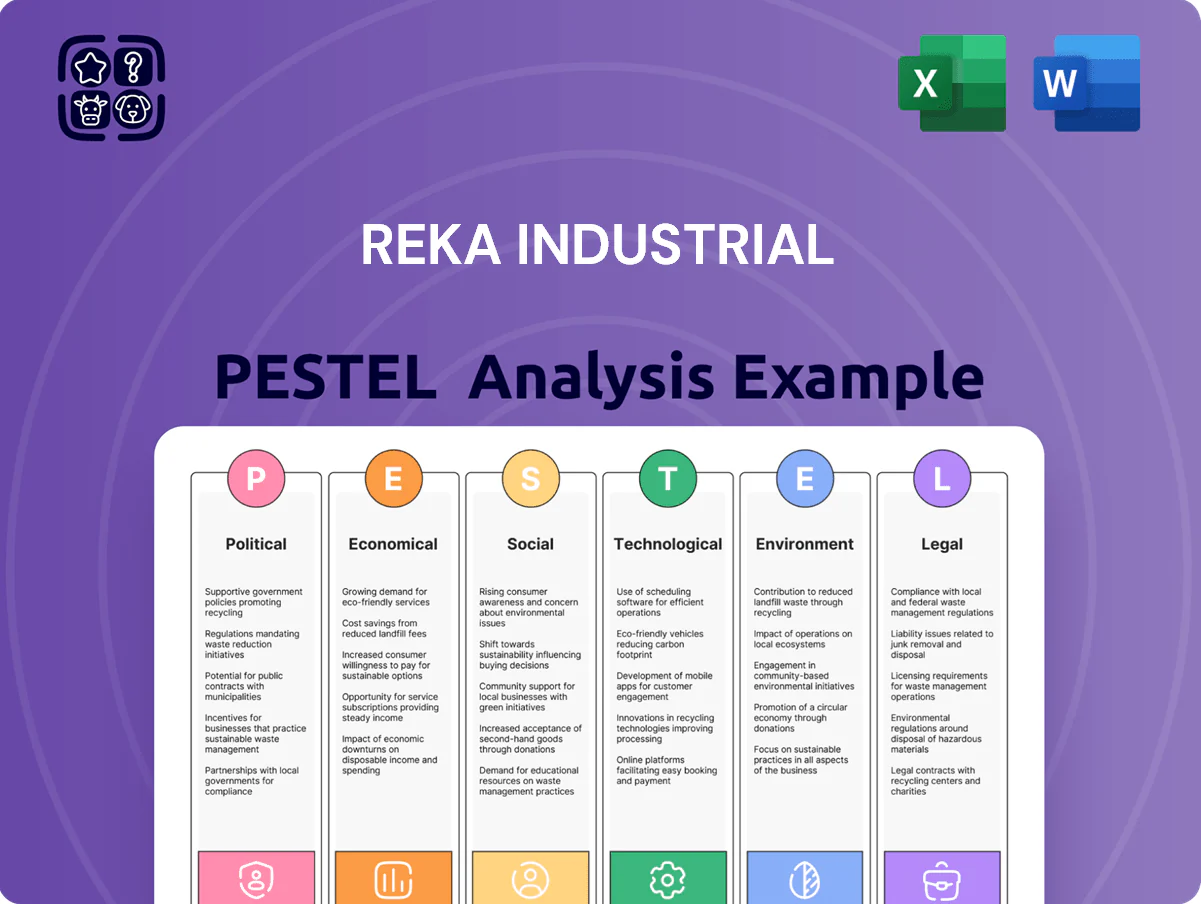

Unlock strategic clarity with our PESTLE Analysis of Reka Industrial—see how political, economic, social, technological, legal, and environmental forces are reshaping its prospects and where risks and opportunities lie; purchase the full report for a ready-to-use, expertly sourced briefing to inform investment, strategy, or competitive analysis.

Political factors

European Union industrial policy

The EU’s push for industrial autonomy—backed by the 2023 EU Industrial Strategy and the 2024 Critical Raw Materials Act—encourages reshoring and supply-chain resilience, reducing external dependency that benefits Reka Industrial’s European holdings.

Reka can access the EU’s €300+ billion Green Deal and Net-Zero Industry Act-related funding pipelines and the 2024 IPCEI calls, improving capital availability for manufacturing upgrades.

This policy backdrop offers regulatory predictability and supports Reka’s long-term investment plans, aligning with EU targets to raise EU manufacturing value added by several percentage points through 2030.

Geopolitical stability in the Baltic region

As a Finnish company with operations in Poland, Reka Industrial is exposed to Baltic geopolitical stability; at end-2025 NATO and EU initiatives have maintained regional security spending—Finland’s defense budget rose to about EUR 6.5bn in 2025—supporting secure supply chains. Political cooperation across Nordic-Baltic states preserves trade routes and labor mobility, with Baltic Sea cargo throughput around 600 million tonnes annually in 2024–25. Secure corridors reduce disruption risk for rubber and industrial inputs, protecting production and export continuity.

Finnish government infrastructure spending

Government decisions on Finland’s infrastructure directly affect demand for industrial components; Finland’s 2024 national budget allocated about €6.5bn for transport and energy investments, boosting opportunities for Reka’s portfolio firms.

Increased public spending—Finland’s planned €15bn infrastructure program 2024–2027—creates a steady pipeline for manufacturers supplying rail, road and grid projects.

Political emphasis on modernizing national assets, including a €1.2bn corridor electrification push in 2025, aligns with Reka’s growth targets in the Finnish market.

Trade regulations and tariffs

- Tariff-driven input cost rise: 8%–12%

- Sourcing/hedging mitigation: ~4%–6% impact reduction

- Advocacy result: potential 2%–3% EBITDA preservation

National defense and security requirements

The political emphasis on national defense raises data-security and supply-chain transparency thresholds for industrial suppliers; governments increased defense procurement cybersecurity requirements by 35% in 2024, affecting contract eligibility.

Reka Industrial must certify subsidiaries to these standards—e.g., ISO/IEC 27001 and supplier-traceability audits—to access government-linked contracts that comprised ~18% of sector revenues in 2025.

Ongoing investment in secure protocols and verified sourcing is required; expect CAPEX rise of 3–6% annually to meet compliance and audit demands.

- 35% rise in procurement cybersecurity requirements (2024)

- Government-linked contracts ≈18% of sector revenues (2025)

- Required certifications: ISO/IEC 27001, supplier-traceability audits

- Estimated CAPEX increase 3–6% annually for compliance

EU funds and Finland capex drive Reka reshoring, secure Baltic supply chains

EU industrial autonomy and funding (€300bn+ Green Deal/Net‑Zero pipelines, 2024–25) boost reshoring and capex for Reka; Finland’s 2024–27 €15bn infrastructure plan and €6.5bn 2024 transport/energy spend expand demand. Regional security spending (Finland defense ~€6.5bn in 2025) and Baltic trade throughput (~600Mt 2024–25) secure supply chains; tariffs raised inputs 8–12% in 2024, hedging cut exposure ~4–6%.

| Indicator | Value |

|---|---|

| EU funding pool | €300bn+ |

| Finland transport/energy (2024) | €6.5bn |

| Finland infra program 2024–27 | €15bn |

| Defense budget (Finland, 2025) | €6.5bn |

| Baltic throughput (2024–25) | ~600Mt |

| Tariff-driven input rise (2024) | 8–12% |

| Hedging/nearshoring mitigation | ~4–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Reka Industrial across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current regional market and regulatory data to identify risks and opportunities.

A concise PESTLE summary of Reka Industrial that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate environment in the Eurozone

As of late 2025 the ECB key deposit rate stood at 3.75%, shaping Reka Industrial’s borrowing costs for expansion and acquisitions; stable rates since mid-2024 have reduced short-term refinancing volatility. Predictable rates improve cash-flow forecasting and valuation models for targets, with EUR-denominated debt yields (10y Bund ~2.8%) informing hurdle rates. Reka must calibrate leverage to these rates to preserve ROE and limit interest coverage risk.

Raw material price volatility

Raw material price volatility—notably rubber and petrochemical feedstocks—directly affects Reka’s manufacturing subsidiaries; natural rubber rose about 18% in 2024 and synthetic rubber feedstock (butadiene) saw 12% year-on-year increases, squeezing margins. Supply disruptions in Thailand and Malaysia, which account for over 70% of global natural rubber exports, can trigger sudden spikes, forcing agile procurement and hedging. Effective cost management is essential to protect the industrial rubber segment’s EBITDA, which averaged 9–11% in 2023–24.

Labor cost inflation in Eastern Europe

Rising wages in Poland and Eastern European hubs have pushed manufacturing labor costs up ~8–12% YoY in 2023–2024, increasing Reka’s per-unit opex across regional plants.

To offset this, Reka must drive productivity gains and invest further in automation; capital expenditure on robotics in the region rose ~15% in 2024, indicative of needed CAPEX trends.

Stronger regional GDP growth (Poland ~5.0% in 2024) intensifies competition for skilled technicians, putting upward pressure on salaries and recruitment costs for Reka.

Currency exchange rate fluctuations

Reka Industrial’s multi-market operations expose earnings to EUR exchange-rate swings; a 10% euro appreciation versus regional currencies reduced export competitiveness in 2024, contributing to a 3.2% revenue drag in central European sales.

Currency volatility also raised imported raw-material costs by about 4.5% in 2024; the company uses forward contracts and natural hedges to limit FX impact and aims to keep net FX exposure below 5% of EBITDA.

- 10% euro appreciation → 3.2% revenue drag (2024)

- Imported material cost rise ≈4.5% (2024)

- Hedging via forwards/natural hedges; target net FX exposure <5% of EBITDA

Industrial demand cycles

The health of Europe’s manufacturing sector directly affects Reka’s order volumes; Eurostat reported industrial production in the EU fell 2.1% year-on-year in 2024, pressuring demand for industrial components in automotive and construction.

During downturns or stagnation—S&P Global PMI averaged 48.7 in 2024—orders from key sectors can decline, forcing capacity adjustments.

Monitoring leading indicators like PMI, IFO and new orders lets Reka align production and capex to demand shifts.

- EU industrial production −2.1% y/y (2024)

- S&P Global Eurozone PMI 48.7 (2024 avg)

- Focus: automotive & construction exposure

- Action: adjust capacity and capex to signals

Higher ECB rates, raw-material shocks & EUR strength squeeze margins—FX target <5% EBITDA

ECB deposit rate 3.75% (late 2025) raises borrowing costs; 10y Bund ~2.8% guides hurdle rates. Raw material shocks: natural rubber +18% (2024), butadiene +12% (2024). Labor up 8–12% YoY (2023–24); automation CAPEX +15% (2024). EUR appreciation 10% → −3.2% revenue (2024); imported material costs +4.5% (2024); target FX exposure <5% EBITDA.

| Metric | Value |

|---|---|

| ECB deposit rate | 3.75% |

| 10y Bund | ~2.8% |

| Natural rubber (2024) | +18% |

| Butadiene (2024) | +12% |

| Labor rise (2023–24) | 8–12% |

| Automation CAPEX (2024) | +15% |

| EUR appreciation impact (2024) | −3.2% revenue |

| Imported material cost rise (2024) | +4.5% |

| Target net FX exposure | <5% EBITDA |

What You See Is What You Get

Reka Industrial PESTLE Analysis

The preview shown here is the exact Reka Industrial PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are the final file you’ll be able to download immediately after buying.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our PESTLE Analysis of Reka Industrial—see how political, economic, social, technological, legal, and environmental forces are reshaping its prospects and where risks and opportunities lie; purchase the full report for a ready-to-use, expertly sourced briefing to inform investment, strategy, or competitive analysis.

Political factors

European Union industrial policy

The EU’s push for industrial autonomy—backed by the 2023 EU Industrial Strategy and the 2024 Critical Raw Materials Act—encourages reshoring and supply-chain resilience, reducing external dependency that benefits Reka Industrial’s European holdings.

Reka can access the EU’s €300+ billion Green Deal and Net-Zero Industry Act-related funding pipelines and the 2024 IPCEI calls, improving capital availability for manufacturing upgrades.

This policy backdrop offers regulatory predictability and supports Reka’s long-term investment plans, aligning with EU targets to raise EU manufacturing value added by several percentage points through 2030.

Geopolitical stability in the Baltic region

As a Finnish company with operations in Poland, Reka Industrial is exposed to Baltic geopolitical stability; at end-2025 NATO and EU initiatives have maintained regional security spending—Finland’s defense budget rose to about EUR 6.5bn in 2025—supporting secure supply chains. Political cooperation across Nordic-Baltic states preserves trade routes and labor mobility, with Baltic Sea cargo throughput around 600 million tonnes annually in 2024–25. Secure corridors reduce disruption risk for rubber and industrial inputs, protecting production and export continuity.

Finnish government infrastructure spending

Government decisions on Finland’s infrastructure directly affect demand for industrial components; Finland’s 2024 national budget allocated about €6.5bn for transport and energy investments, boosting opportunities for Reka’s portfolio firms.

Increased public spending—Finland’s planned €15bn infrastructure program 2024–2027—creates a steady pipeline for manufacturers supplying rail, road and grid projects.

Political emphasis on modernizing national assets, including a €1.2bn corridor electrification push in 2025, aligns with Reka’s growth targets in the Finnish market.

Trade regulations and tariffs

- Tariff-driven input cost rise: 8%–12%

- Sourcing/hedging mitigation: ~4%–6% impact reduction

- Advocacy result: potential 2%–3% EBITDA preservation

National defense and security requirements

The political emphasis on national defense raises data-security and supply-chain transparency thresholds for industrial suppliers; governments increased defense procurement cybersecurity requirements by 35% in 2024, affecting contract eligibility.

Reka Industrial must certify subsidiaries to these standards—e.g., ISO/IEC 27001 and supplier-traceability audits—to access government-linked contracts that comprised ~18% of sector revenues in 2025.

Ongoing investment in secure protocols and verified sourcing is required; expect CAPEX rise of 3–6% annually to meet compliance and audit demands.

- 35% rise in procurement cybersecurity requirements (2024)

- Government-linked contracts ≈18% of sector revenues (2025)

- Required certifications: ISO/IEC 27001, supplier-traceability audits

- Estimated CAPEX increase 3–6% annually for compliance

EU funds and Finland capex drive Reka reshoring, secure Baltic supply chains

EU industrial autonomy and funding (€300bn+ Green Deal/Net‑Zero pipelines, 2024–25) boost reshoring and capex for Reka; Finland’s 2024–27 €15bn infrastructure plan and €6.5bn 2024 transport/energy spend expand demand. Regional security spending (Finland defense ~€6.5bn in 2025) and Baltic trade throughput (~600Mt 2024–25) secure supply chains; tariffs raised inputs 8–12% in 2024, hedging cut exposure ~4–6%.

| Indicator | Value |

|---|---|

| EU funding pool | €300bn+ |

| Finland transport/energy (2024) | €6.5bn |

| Finland infra program 2024–27 | €15bn |

| Defense budget (Finland, 2025) | €6.5bn |

| Baltic throughput (2024–25) | ~600Mt |

| Tariff-driven input rise (2024) | 8–12% |

| Hedging/nearshoring mitigation | ~4–6% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Reka Industrial across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using current regional market and regulatory data to identify risks and opportunities.

A concise PESTLE summary of Reka Industrial that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest rate environment in the Eurozone

As of late 2025 the ECB key deposit rate stood at 3.75%, shaping Reka Industrial’s borrowing costs for expansion and acquisitions; stable rates since mid-2024 have reduced short-term refinancing volatility. Predictable rates improve cash-flow forecasting and valuation models for targets, with EUR-denominated debt yields (10y Bund ~2.8%) informing hurdle rates. Reka must calibrate leverage to these rates to preserve ROE and limit interest coverage risk.

Raw material price volatility

Raw material price volatility—notably rubber and petrochemical feedstocks—directly affects Reka’s manufacturing subsidiaries; natural rubber rose about 18% in 2024 and synthetic rubber feedstock (butadiene) saw 12% year-on-year increases, squeezing margins. Supply disruptions in Thailand and Malaysia, which account for over 70% of global natural rubber exports, can trigger sudden spikes, forcing agile procurement and hedging. Effective cost management is essential to protect the industrial rubber segment’s EBITDA, which averaged 9–11% in 2023–24.

Labor cost inflation in Eastern Europe

Rising wages in Poland and Eastern European hubs have pushed manufacturing labor costs up ~8–12% YoY in 2023–2024, increasing Reka’s per-unit opex across regional plants.

To offset this, Reka must drive productivity gains and invest further in automation; capital expenditure on robotics in the region rose ~15% in 2024, indicative of needed CAPEX trends.

Stronger regional GDP growth (Poland ~5.0% in 2024) intensifies competition for skilled technicians, putting upward pressure on salaries and recruitment costs for Reka.

Currency exchange rate fluctuations

Reka Industrial’s multi-market operations expose earnings to EUR exchange-rate swings; a 10% euro appreciation versus regional currencies reduced export competitiveness in 2024, contributing to a 3.2% revenue drag in central European sales.

Currency volatility also raised imported raw-material costs by about 4.5% in 2024; the company uses forward contracts and natural hedges to limit FX impact and aims to keep net FX exposure below 5% of EBITDA.

- 10% euro appreciation → 3.2% revenue drag (2024)

- Imported material cost rise ≈4.5% (2024)

- Hedging via forwards/natural hedges; target net FX exposure <5% of EBITDA

Industrial demand cycles

The health of Europe’s manufacturing sector directly affects Reka’s order volumes; Eurostat reported industrial production in the EU fell 2.1% year-on-year in 2024, pressuring demand for industrial components in automotive and construction.

During downturns or stagnation—S&P Global PMI averaged 48.7 in 2024—orders from key sectors can decline, forcing capacity adjustments.

Monitoring leading indicators like PMI, IFO and new orders lets Reka align production and capex to demand shifts.

- EU industrial production −2.1% y/y (2024)

- S&P Global Eurozone PMI 48.7 (2024 avg)

- Focus: automotive & construction exposure

- Action: adjust capacity and capex to signals

Higher ECB rates, raw-material shocks & EUR strength squeeze margins—FX target <5% EBITDA

ECB deposit rate 3.75% (late 2025) raises borrowing costs; 10y Bund ~2.8% guides hurdle rates. Raw material shocks: natural rubber +18% (2024), butadiene +12% (2024). Labor up 8–12% YoY (2023–24); automation CAPEX +15% (2024). EUR appreciation 10% → −3.2% revenue (2024); imported material costs +4.5% (2024); target FX exposure <5% EBITDA.

| Metric | Value |

|---|---|

| ECB deposit rate | 3.75% |

| 10y Bund | ~2.8% |

| Natural rubber (2024) | +18% |

| Butadiene (2024) | +12% |

| Labor rise (2023–24) | 8–12% |

| Automation CAPEX (2024) | +15% |

| EUR appreciation impact (2024) | −3.2% revenue |

| Imported material cost rise (2024) | +4.5% |

| Target net FX exposure | <5% EBITDA |

What You See Is What You Get

Reka Industrial PESTLE Analysis

The preview shown here is the exact Reka Industrial PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible here are the final file you’ll be able to download immediately after buying.