Relacom AB PESTLE Analysis

Your Shortcut to Market Insight Starts Here

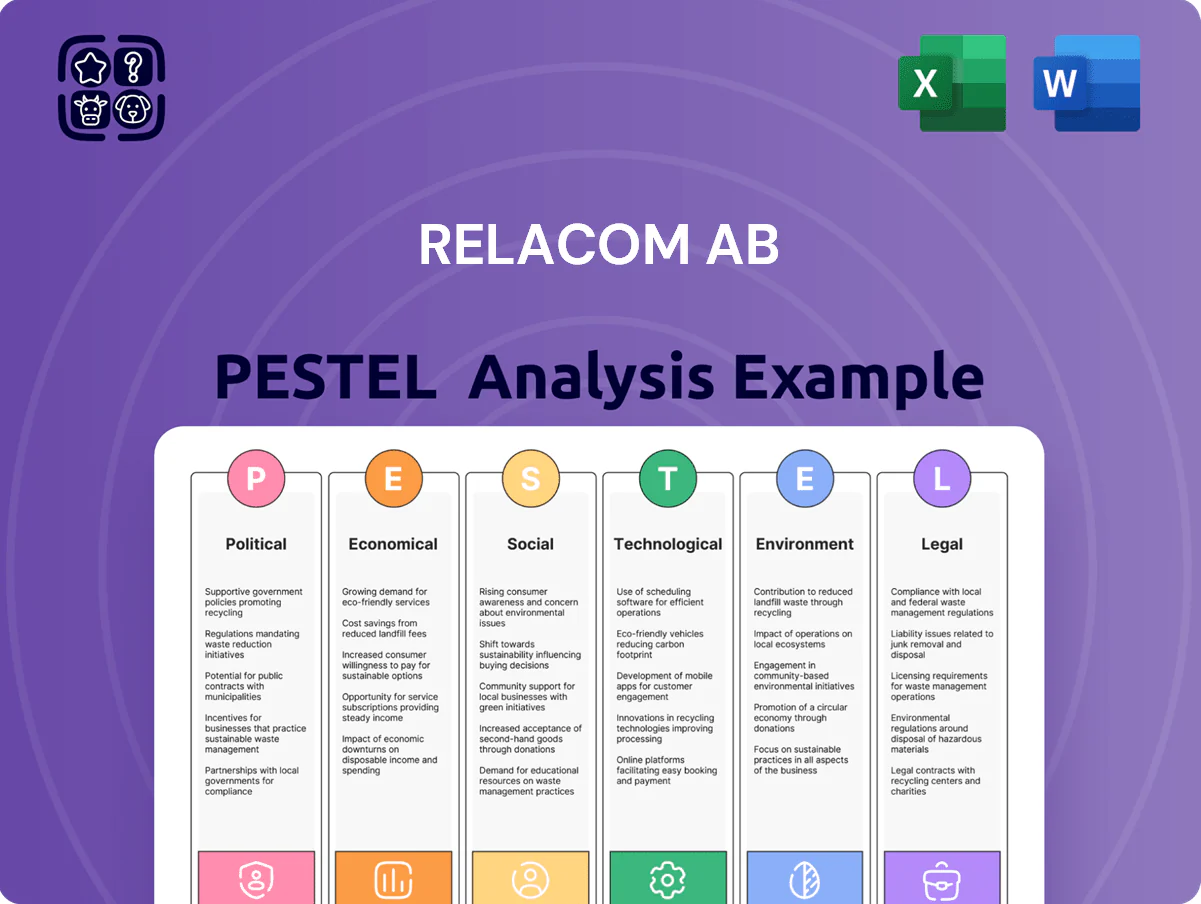

Gain a strategic advantage with our PESTLE Analysis of Relacom AB—uncover how political shifts, economic trends, social changes, technological advances, legal risks, and environmental factors shape its trajectory; buy the full report to access ready-to-use, expert insights and downloadable formats that accelerate decision-making and strengthen your competitive strategy.

Political factors

European Infrastructure Funding

The EU’s Connecting Europe Facility and Digital Europe Programme committed over €45bn for 2021–2027, accelerating fiber rollouts and grid upgrades that subsidize projects tied to Eltel and legacy Relacom operations; in 2024 Nordic states increased infrastructure allocations—Sweden +6% and Finland +4% year-on-year—aligning national budgets to secure digital/energy sovereignty and de-risk long-term contracts for regional telecom and power modernization.

Geopolitical Security Regulations

Northern European governments now enforce strict hardware security for critical infrastructure, with vendor screening excluding high-risk suppliers from core 5G and power grids; Norway and Sweden reported 78% of telecom tenders in 2024 included explicit supplier-origin clauses.

This political shift forced OEMs and integrators like Relacom AB to increase supply-chain transparency—EU digital infrastructure rules in 2025 require 95% component traceability for public contracts.

Failure to comply risks loss of lucrative public work: Nordic state procurement for 2024–25 allocated roughly EUR 3.2 billion to secure-network projects, often limited to cleared vendors.

Digital Sovereignty Initiatives

Sweden and Nordic neighbors are doubling down on digital sovereignty, with Sweden allocating SEK 7.5bn (2024–2026) to secure critical networks and EU rules pushing local procurement for 5G and fiber projects; political pressure favors vendors with local presence and high-security clearances, benefiting Relacom given its long-term contracts with state utilities and telecoms, where 70% of critical maintenance now requires domestically anchored suppliers.

Energy Independence Policies

- EU grid investment: EUR 120–180bn/year (to 2026)

- Target renewables share: 60%+ in some EU markets by 2030

- Increased recurring O&M and commissioning opportunities for field-service firms

Public-Private Partnerships

Governments increasingly use public-private partnerships to bridge the digital divide in rural Nordic areas, funding projects that reached €1.3bn in broadband subsidies across Sweden, Norway and Finland in 2024.

These agreements give Relacom AB revenue visibility and fund long-term maintenance; PPP-backed contracts often span 10–15 years, supporting predictable cash flows and CAPEX planning.

Nordic political stability—Scandinavia ranking top 10 in the 2024 Global Peace Index—reduces contract risk and aids strategic expansion.

- €1.3bn broadband subsidies (2024)

- Typical PPP terms: 10–15 years

- Nordic: top 10 Global Peace Index (2024)

EU/Nordic funding surge fuels local-secure grids, broadband and long-term O&M wins

Nordic/EU policy boosts spending for secure digital and energy grids—EU 2021–27 funds €45bn+ and Nordic states hiked 2024 infrastructure budgets (Sweden +6%, Finland +4%), creating long-term PPPs (10–15 yrs) and €1.3bn broadband subsidies; strict supplier-origin/security rules (95% traceability by 2025) steer contracts to local, cleared vendors, expanding recurring O&M for Relacom.

| Metric | Value |

|---|---|

| EU digital funds (2021–27) | €45bn+ |

| Nordic infra change (2024) | Sweden +6%, Finland +4% |

| Broadband subsidies (2024) | €1.3bn |

| Procurement traceability (2025) | 95% |

| PPP term | 10–15 yrs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors specifically impact Relacom AB’s telecom and service operations, using current regional market data and regulatory trends to identify key threats and opportunities.

A concise, shareable PESTLE summary of Relacom AB, neatly segmented for quick interpretation in meetings or presentations and editable for region- or line-specific notes to support risk discussions, strategic alignment, and consultant reports.

Economic factors

Inflationary Pressure on Labor

Persistent wage inflation in the Nordics pushed average private-sector wages up about 5.2% in 2024, raising Relacom AB’s technical labor costs materially; maintaining skilled field technicians now consumes a larger share of revenue given typical field-service margins of 4–8%. Service contracts’ thin margins force investments in efficiency: optimized routing and workforce management can cut operational costs by 8–12%, crucial to offset rising payroll pressure.

Interest Rate Environment

While global policy rates have eased from 2022 peaks, Sweden's repo rate at 4.00% (Riksbank, Dec 2025) and ECB at 3.75% keep borrowing costly, pressuring Relacom clients’ CAPEX; 2024 telecom capex growth slowed to 1.8% YoY in EMEA, with many operators deferring projects. Higher financing costs push operators toward maintenance over new builds and require demonstrable IRRs—often above 10–12%—to secure funding for large deployments.

Regional GDP Growth

The Nordic economic health strongly influences demand for Relacom ABs communication and power services; Sweden and Finland GDP growth of 1.9% and 1.7% in 2024 (IMF) supports higher spending on high-speed internet and sustainable energy solutions. Rising capex in Nordic telecoms—estimated SEK 45bn in Sweden 2024—boosts infrastructure contracts. This steady growth provides resilience against global downturns, underpinning long-term service demand.

Skilled Labor Shortages

The scarcity of qualified field technicians and engineers is constraining Relacom AB’s growth in 2024–25, with Europe-wide vacancy rates for telecom technicians near 12% and average recruitment costs up ~18% year-on-year.

High demand is driving greater use of subcontractors, increasing project margins by an estimated 3–5 percentage points, and pushing wage inflation in the sector by ~6% in 2024.

Relacom is expanding internal training; 2024 capex for workforce development rose ~20%, aiming to reduce subcontracting spend by 10% over three years.

- Technician vacancy ~12%

- Recruitment costs +18% YoY

- Wage inflation ~6% (2024)

- Training capex +20% (2024)

- Target subcontracting reduction 10% in 3 years

Currency Exchange Volatility

- SEK/EUR ±5% ~ ±1.2–1.8 pp margin impact

- Q4 2024 Eurozone GDP +0.5%, inflation ~2.4%

- Import-driven capex sensitivity increases procurement costs

Wage inflation and tech shortages squeeze service margins as training spend rises

Wage inflation (~6% in 2024) and technician vacancy (~12%) raised field labor costs, squeezing 4–8% service margins; workforce training capex +20% (2024) aims to cut subcontracting 10% in 3 years. Sweden GDP 1.9% and Finland 1.7% (2024) sustain demand while telecom capex growth slowed to 1.8% (EMEA, 2024). Sweden repo ~4.00% (Dec 2025) keeps borrowing costly; SEK/EUR ±5% swings affect margins ~1.2–1.8 pp.

| Metric | 2024/2025 |

|---|---|

| Wage inflation | ~6% |

| Technician vacancy | ~12% |

| Training capex | +20% (2024) |

| Telecom capex EMEA | +1.8% (2024) |

| Sweden GDP | 1.9% (2024) |

| Repo rate Sweden | 4.00% (Dec 2025) |

| SEK/EUR swing impact | ±5% → ±1.2–1.8 pp margin |

Full Version Awaits

Relacom AB PESTLE Analysis

The preview shown here is the exact Relacom AB PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic advantage with our PESTLE Analysis of Relacom AB—uncover how political shifts, economic trends, social changes, technological advances, legal risks, and environmental factors shape its trajectory; buy the full report to access ready-to-use, expert insights and downloadable formats that accelerate decision-making and strengthen your competitive strategy.

Political factors

European Infrastructure Funding

The EU’s Connecting Europe Facility and Digital Europe Programme committed over €45bn for 2021–2027, accelerating fiber rollouts and grid upgrades that subsidize projects tied to Eltel and legacy Relacom operations; in 2024 Nordic states increased infrastructure allocations—Sweden +6% and Finland +4% year-on-year—aligning national budgets to secure digital/energy sovereignty and de-risk long-term contracts for regional telecom and power modernization.

Geopolitical Security Regulations

Northern European governments now enforce strict hardware security for critical infrastructure, with vendor screening excluding high-risk suppliers from core 5G and power grids; Norway and Sweden reported 78% of telecom tenders in 2024 included explicit supplier-origin clauses.

This political shift forced OEMs and integrators like Relacom AB to increase supply-chain transparency—EU digital infrastructure rules in 2025 require 95% component traceability for public contracts.

Failure to comply risks loss of lucrative public work: Nordic state procurement for 2024–25 allocated roughly EUR 3.2 billion to secure-network projects, often limited to cleared vendors.

Digital Sovereignty Initiatives

Sweden and Nordic neighbors are doubling down on digital sovereignty, with Sweden allocating SEK 7.5bn (2024–2026) to secure critical networks and EU rules pushing local procurement for 5G and fiber projects; political pressure favors vendors with local presence and high-security clearances, benefiting Relacom given its long-term contracts with state utilities and telecoms, where 70% of critical maintenance now requires domestically anchored suppliers.

Energy Independence Policies

- EU grid investment: EUR 120–180bn/year (to 2026)

- Target renewables share: 60%+ in some EU markets by 2030

- Increased recurring O&M and commissioning opportunities for field-service firms

Public-Private Partnerships

Governments increasingly use public-private partnerships to bridge the digital divide in rural Nordic areas, funding projects that reached €1.3bn in broadband subsidies across Sweden, Norway and Finland in 2024.

These agreements give Relacom AB revenue visibility and fund long-term maintenance; PPP-backed contracts often span 10–15 years, supporting predictable cash flows and CAPEX planning.

Nordic political stability—Scandinavia ranking top 10 in the 2024 Global Peace Index—reduces contract risk and aids strategic expansion.

- €1.3bn broadband subsidies (2024)

- Typical PPP terms: 10–15 years

- Nordic: top 10 Global Peace Index (2024)

EU/Nordic funding surge fuels local-secure grids, broadband and long-term O&M wins

Nordic/EU policy boosts spending for secure digital and energy grids—EU 2021–27 funds €45bn+ and Nordic states hiked 2024 infrastructure budgets (Sweden +6%, Finland +4%), creating long-term PPPs (10–15 yrs) and €1.3bn broadband subsidies; strict supplier-origin/security rules (95% traceability by 2025) steer contracts to local, cleared vendors, expanding recurring O&M for Relacom.

| Metric | Value |

|---|---|

| EU digital funds (2021–27) | €45bn+ |

| Nordic infra change (2024) | Sweden +6%, Finland +4% |

| Broadband subsidies (2024) | €1.3bn |

| Procurement traceability (2025) | 95% |

| PPP term | 10–15 yrs |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors specifically impact Relacom AB’s telecom and service operations, using current regional market data and regulatory trends to identify key threats and opportunities.

A concise, shareable PESTLE summary of Relacom AB, neatly segmented for quick interpretation in meetings or presentations and editable for region- or line-specific notes to support risk discussions, strategic alignment, and consultant reports.

Economic factors

Inflationary Pressure on Labor

Persistent wage inflation in the Nordics pushed average private-sector wages up about 5.2% in 2024, raising Relacom AB’s technical labor costs materially; maintaining skilled field technicians now consumes a larger share of revenue given typical field-service margins of 4–8%. Service contracts’ thin margins force investments in efficiency: optimized routing and workforce management can cut operational costs by 8–12%, crucial to offset rising payroll pressure.

Interest Rate Environment

While global policy rates have eased from 2022 peaks, Sweden's repo rate at 4.00% (Riksbank, Dec 2025) and ECB at 3.75% keep borrowing costly, pressuring Relacom clients’ CAPEX; 2024 telecom capex growth slowed to 1.8% YoY in EMEA, with many operators deferring projects. Higher financing costs push operators toward maintenance over new builds and require demonstrable IRRs—often above 10–12%—to secure funding for large deployments.

Regional GDP Growth

The Nordic economic health strongly influences demand for Relacom ABs communication and power services; Sweden and Finland GDP growth of 1.9% and 1.7% in 2024 (IMF) supports higher spending on high-speed internet and sustainable energy solutions. Rising capex in Nordic telecoms—estimated SEK 45bn in Sweden 2024—boosts infrastructure contracts. This steady growth provides resilience against global downturns, underpinning long-term service demand.

Skilled Labor Shortages

The scarcity of qualified field technicians and engineers is constraining Relacom AB’s growth in 2024–25, with Europe-wide vacancy rates for telecom technicians near 12% and average recruitment costs up ~18% year-on-year.

High demand is driving greater use of subcontractors, increasing project margins by an estimated 3–5 percentage points, and pushing wage inflation in the sector by ~6% in 2024.

Relacom is expanding internal training; 2024 capex for workforce development rose ~20%, aiming to reduce subcontracting spend by 10% over three years.

- Technician vacancy ~12%

- Recruitment costs +18% YoY

- Wage inflation ~6% (2024)

- Training capex +20% (2024)

- Target subcontracting reduction 10% in 3 years

Currency Exchange Volatility

- SEK/EUR ±5% ~ ±1.2–1.8 pp margin impact

- Q4 2024 Eurozone GDP +0.5%, inflation ~2.4%

- Import-driven capex sensitivity increases procurement costs

Wage inflation and tech shortages squeeze service margins as training spend rises

Wage inflation (~6% in 2024) and technician vacancy (~12%) raised field labor costs, squeezing 4–8% service margins; workforce training capex +20% (2024) aims to cut subcontracting 10% in 3 years. Sweden GDP 1.9% and Finland 1.7% (2024) sustain demand while telecom capex growth slowed to 1.8% (EMEA, 2024). Sweden repo ~4.00% (Dec 2025) keeps borrowing costly; SEK/EUR ±5% swings affect margins ~1.2–1.8 pp.

| Metric | 2024/2025 |

|---|---|

| Wage inflation | ~6% |

| Technician vacancy | ~12% |

| Training capex | +20% (2024) |

| Telecom capex EMEA | +1.8% (2024) |

| Sweden GDP | 1.9% (2024) |

| Repo rate Sweden | 4.00% (Dec 2025) |

| SEK/EUR swing impact | ±5% → ±1.2–1.8 pp margin |

Full Version Awaits

Relacom AB PESTLE Analysis

The preview shown here is the exact Relacom AB PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.