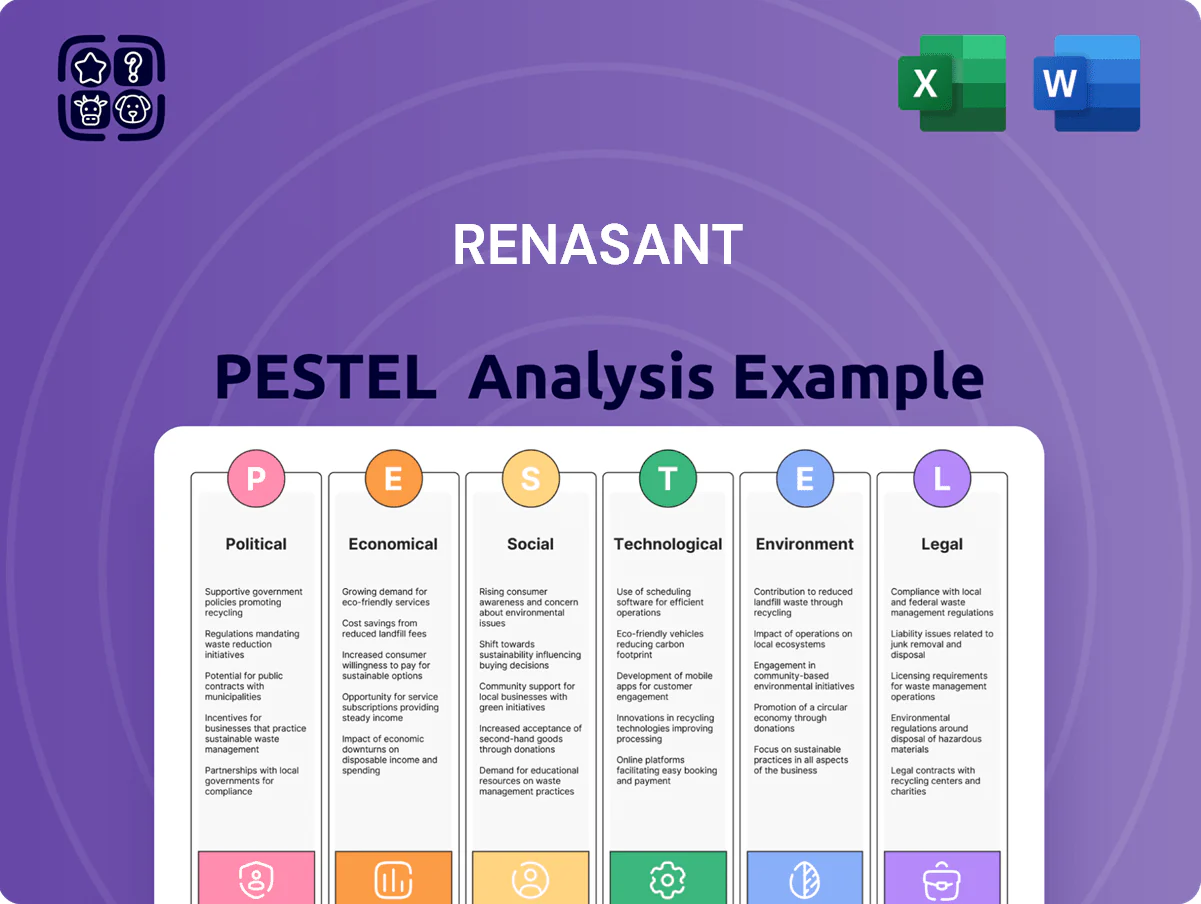

Renasant PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological trends are shaping Renasant’s strategic outlook with our focused PESTLE Analysis—designed for investors and strategists who need fast, actionable intelligence; purchase the full report for a complete, downloadable breakdown you can use in boardrooms and models.

Political factors

Federal Regulatory Shifts

The 2024 elections prompted federal regulatory recalibration, and by late 2025 CFPB and FDIC guidance has tightened oversight affecting fee disclosures and incremental lending-capital tests; banks reported a 12% rise in compliance costs industry-wide in 2024–25. Renasant, with $18.6 billion in assets (2025 est.), must retool policies as fee-structure constraints and higher capital scrutiny alter net interest margins. These rule shifts demand substantial administrative resources to maintain compliance across Alabama, Mississippi, Tennessee, Georgia, and Florida.

State-Level Fiscal Policies

Operating primarily in the Southeast, Renasant is influenced by conservative fiscal policies in Mississippi, Alabama, and Tennessee, where 2024 state corporate tax rates range from 5% (Mississippi phased down) to 6.5% (Alabama) and business incentives exceeded $1.2 billion regionally in 2023, boosting relocations and expansions.

Municipal Infrastructure Funding

Renasant benefits from strong municipal infrastructure funding across the Sunbelt, where federal Bipartisan Infrastructure Law and FY2025 state allocations drive a projected $120–150bn in regional projects through 2026, boosting demand for public‑sector financing and construction lending; rising municipal bond issuance (+8% YoY in 2024) and state capital plans support loan growth and strengthen long‑term asset quality in developing corridors.

Trade Policy Impacts on Local Business

Renasant’s exposure to manufacturing and agricultural clients makes it vulnerable to trade-policy shifts; 2024 US tariff adjustments and 2023–24 soybean export volatility (US exports fell ~8% YoY in 2024) can compress client cash flows and increase nonperforming loans in commercial portfolios.

Political decisions on trade and tariffs can reduce borrowers’ revenues and raise delinquencies; Renasant must track geopolitical developments and stress-test loans—commercial CRE and C&I segments saw charge-off sensitivity of ~0.2–0.5% under trade shock scenarios in recent industry stress tests.

- Serve concentrated sectors: manufacturing/agriculture exposure

- Key risk: tariffs and trade agreements altering cash flow

- Action: monitor geopolitics, perform stress tests, adjust credit limits

- Metric: export-driven revenue swings (~8% export change) affect NPLs/charge-offs

Government Small Business Support

Political initiatives via the SBA and local grant programs—which supported over 5 million small-business loans totaling roughly $800 billion nationwide from 2020–2024—are critical to Renasant’s community banking model, enabling targeted CRE and C&I lending in its footprint.

Shifts in program administration can favor larger banks with scale, changing market share; community banks like Renasant counter by using local relationships to capture higher-margin small-business accounts.

Renasant leverages these frameworks to deepen ties with entrepreneurs and startups, noting small-business deposits and loan originations rose by mid-single digits in 2023–2025 within its Gulf South markets.

- SBA/related programs: ~$800B loans 2020–2024

- Renasant: mid-single-digit growth in small-business lending 2023–2025

- Risk: administrative changes can shift share to national banks

- Opportunity: stronger local relationships boost deposit and fee income

Renasant Faces Margin Squeeze as CFPB/FDIC Costs Rise; SE Infra Lifts Loan Demand

Federal CFPB/FDIC tightening raised compliance costs ~12% in 2024–25; Renasant ($18.6B assets, 2025 est.) faces margin pressure from fee limits and capital tests. Southeast state tax rates 2024: MS ~5%, AL 6.5%; regional incentives >$1.2B (2023) spurred relocations boosting C&I demand. Infrastructure funding (BIL+FY2025) drives $120–150B projects through 2026, lifting municipal lending; export volatility (~−8% YoY soy, 2024) heightens commercial credit risk.

| Metric | Value |

|---|---|

| Assets (Renasant) | $18.6B (2025 est.) |

| Compliance cost change | +12% (2024–25) |

| Regional incentives | $1.2B (2023) |

| Infra projects (Southeast) | $120–150B (through 2026) |

| Soy export change | −8% YoY (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Renasant across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, consultants, and investors for scenario planning and strategy design.

A concise, shareable PESTLE summary that clarifies Renasant’s external risks and opportunities for quick alignment in meetings, easily dropped into presentations or planning packs.

Economic factors

Interest Rate Stabilization

By end-2025, interest rate stabilization—with the federal funds rate holding near 5.25%—has improved predictability for Renasant’s net interest margin, which narrowed to 3.10% in FY2024 but showed stabilization in early 2025. Renasant adjusted deposit pricing, trimming average deposit cost to about 0.95% in 2025 while staying competitive in key Southeast markets. This plateaued rate cycle enables more accurate long-term forecasting and deliberate capital allocation toward growth initiatives.

Southeast Regional Growth

The Southeast grew 2.8% real GDP in 2024 vs US 1.9%, with Nashville and Atlanta among fastest-growing MSAs; Renasant’s footprint in these markets supports a steady pipeline—Q4 2024 mortgage originations rose ~12% in the Southeast and commercial loan growth there outpaced national CRE by ~3pp. This regional resilience helps buffer Renasant against broader national slowdowns.

Commercial Real Estate Health

The performance of commercial real estate is a key economic indicator for Renasant, with CRE loans representing about 38% of total loans at Regional banks in 2024; office demand shows persistent weakness with national vacancy rates near 17% Q4 2024, while Southern industrial vacancy remained below 6% and multi-family fundamentals supported by 3.5% annual rent growth in 2024. Renasant’s portfolio concentration and active risk management of office exposures will be critical to preserve asset quality through 2025.

Consumer Spending and Debt

Lingering 2024 inflation and elevated household debt — US consumer debt hit $17.9 trillion Q4 2024 — pressure Renasant’s retail banking margins and demand for credit, prompting close monitoring of delinquency rates (card charge-offs rose to ~3.5% in late 2024) and credit card utilization (avg ~29% nationally).

Renasant tailors offerings via personalized wealth management, increased debt consolidation loans, and payment-assist programs to mitigate credit risk and retain customers.

- Household debt $17.9T (Q4 2024)

- Credit card utilization ~29%

- Card charge-off ~3.5% (late 2024)

- Focus: wealth mgmt, consolidation, payment assistance

Inflationary Pressure on Costs

- Wage inflation ~4.5% (2024)

- Renasant ROA 0.72% (2024)

- Bank tech spend +12% YoY (2023–24)

Stable rates, firm NIM and SE growth offset credit risk as tech spend cushions margins

Stable fed funds ~5.25% end-2025 supports NIM predictability (NIM 3.10% FY2024); Southeast GDP +2.8% 2024 boosts mortgage originations (+12% Q4 2024) and CRE industrial strength; household debt $17.9T Q4 2024 with card utilization ~29% and charge-offs ~3.5% raise credit risk; wage inflation ~4.5% pressures efficiency (ROA 0.72% 2024); tech spend +12% YoY offsets expenses.

| Metric | Value |

|---|---|

| NIM FY2024 | 3.10% |

| Fed funds (end-2025) | ~5.25% |

| Southeast GDP 2024 | +2.8% |

| Household debt Q4 2024 | $17.9T |

| Card utilization | ~29% |

| Card charge-off | ~3.5% |

| Wage inflation 2024 | ~4.5% |

| ROA 2024 | 0.72% |

| Bank tech spend YoY | +12% |

Preview the Actual Deliverable

Renasant PESTLE Analysis

The preview shown here is the exact Renasant PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, economic cycles, and technological trends are shaping Renasant’s strategic outlook with our focused PESTLE Analysis—designed for investors and strategists who need fast, actionable intelligence; purchase the full report for a complete, downloadable breakdown you can use in boardrooms and models.

Political factors

Federal Regulatory Shifts

The 2024 elections prompted federal regulatory recalibration, and by late 2025 CFPB and FDIC guidance has tightened oversight affecting fee disclosures and incremental lending-capital tests; banks reported a 12% rise in compliance costs industry-wide in 2024–25. Renasant, with $18.6 billion in assets (2025 est.), must retool policies as fee-structure constraints and higher capital scrutiny alter net interest margins. These rule shifts demand substantial administrative resources to maintain compliance across Alabama, Mississippi, Tennessee, Georgia, and Florida.

State-Level Fiscal Policies

Operating primarily in the Southeast, Renasant is influenced by conservative fiscal policies in Mississippi, Alabama, and Tennessee, where 2024 state corporate tax rates range from 5% (Mississippi phased down) to 6.5% (Alabama) and business incentives exceeded $1.2 billion regionally in 2023, boosting relocations and expansions.

Municipal Infrastructure Funding

Renasant benefits from strong municipal infrastructure funding across the Sunbelt, where federal Bipartisan Infrastructure Law and FY2025 state allocations drive a projected $120–150bn in regional projects through 2026, boosting demand for public‑sector financing and construction lending; rising municipal bond issuance (+8% YoY in 2024) and state capital plans support loan growth and strengthen long‑term asset quality in developing corridors.

Trade Policy Impacts on Local Business

Renasant’s exposure to manufacturing and agricultural clients makes it vulnerable to trade-policy shifts; 2024 US tariff adjustments and 2023–24 soybean export volatility (US exports fell ~8% YoY in 2024) can compress client cash flows and increase nonperforming loans in commercial portfolios.

Political decisions on trade and tariffs can reduce borrowers’ revenues and raise delinquencies; Renasant must track geopolitical developments and stress-test loans—commercial CRE and C&I segments saw charge-off sensitivity of ~0.2–0.5% under trade shock scenarios in recent industry stress tests.

- Serve concentrated sectors: manufacturing/agriculture exposure

- Key risk: tariffs and trade agreements altering cash flow

- Action: monitor geopolitics, perform stress tests, adjust credit limits

- Metric: export-driven revenue swings (~8% export change) affect NPLs/charge-offs

Government Small Business Support

Political initiatives via the SBA and local grant programs—which supported over 5 million small-business loans totaling roughly $800 billion nationwide from 2020–2024—are critical to Renasant’s community banking model, enabling targeted CRE and C&I lending in its footprint.

Shifts in program administration can favor larger banks with scale, changing market share; community banks like Renasant counter by using local relationships to capture higher-margin small-business accounts.

Renasant leverages these frameworks to deepen ties with entrepreneurs and startups, noting small-business deposits and loan originations rose by mid-single digits in 2023–2025 within its Gulf South markets.

- SBA/related programs: ~$800B loans 2020–2024

- Renasant: mid-single-digit growth in small-business lending 2023–2025

- Risk: administrative changes can shift share to national banks

- Opportunity: stronger local relationships boost deposit and fee income

Renasant Faces Margin Squeeze as CFPB/FDIC Costs Rise; SE Infra Lifts Loan Demand

Federal CFPB/FDIC tightening raised compliance costs ~12% in 2024–25; Renasant ($18.6B assets, 2025 est.) faces margin pressure from fee limits and capital tests. Southeast state tax rates 2024: MS ~5%, AL 6.5%; regional incentives >$1.2B (2023) spurred relocations boosting C&I demand. Infrastructure funding (BIL+FY2025) drives $120–150B projects through 2026, lifting municipal lending; export volatility (~−8% YoY soy, 2024) heightens commercial credit risk.

| Metric | Value |

|---|---|

| Assets (Renasant) | $18.6B (2025 est.) |

| Compliance cost change | +12% (2024–25) |

| Regional incentives | $1.2B (2023) |

| Infra projects (Southeast) | $120–150B (through 2026) |

| Soy export change | −8% YoY (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Renasant across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to inform executives, consultants, and investors for scenario planning and strategy design.

A concise, shareable PESTLE summary that clarifies Renasant’s external risks and opportunities for quick alignment in meetings, easily dropped into presentations or planning packs.

Economic factors

Interest Rate Stabilization

By end-2025, interest rate stabilization—with the federal funds rate holding near 5.25%—has improved predictability for Renasant’s net interest margin, which narrowed to 3.10% in FY2024 but showed stabilization in early 2025. Renasant adjusted deposit pricing, trimming average deposit cost to about 0.95% in 2025 while staying competitive in key Southeast markets. This plateaued rate cycle enables more accurate long-term forecasting and deliberate capital allocation toward growth initiatives.

Southeast Regional Growth

The Southeast grew 2.8% real GDP in 2024 vs US 1.9%, with Nashville and Atlanta among fastest-growing MSAs; Renasant’s footprint in these markets supports a steady pipeline—Q4 2024 mortgage originations rose ~12% in the Southeast and commercial loan growth there outpaced national CRE by ~3pp. This regional resilience helps buffer Renasant against broader national slowdowns.

Commercial Real Estate Health

The performance of commercial real estate is a key economic indicator for Renasant, with CRE loans representing about 38% of total loans at Regional banks in 2024; office demand shows persistent weakness with national vacancy rates near 17% Q4 2024, while Southern industrial vacancy remained below 6% and multi-family fundamentals supported by 3.5% annual rent growth in 2024. Renasant’s portfolio concentration and active risk management of office exposures will be critical to preserve asset quality through 2025.

Consumer Spending and Debt

Lingering 2024 inflation and elevated household debt — US consumer debt hit $17.9 trillion Q4 2024 — pressure Renasant’s retail banking margins and demand for credit, prompting close monitoring of delinquency rates (card charge-offs rose to ~3.5% in late 2024) and credit card utilization (avg ~29% nationally).

Renasant tailors offerings via personalized wealth management, increased debt consolidation loans, and payment-assist programs to mitigate credit risk and retain customers.

- Household debt $17.9T (Q4 2024)

- Credit card utilization ~29%

- Card charge-off ~3.5% (late 2024)

- Focus: wealth mgmt, consolidation, payment assistance

Inflationary Pressure on Costs

- Wage inflation ~4.5% (2024)

- Renasant ROA 0.72% (2024)

- Bank tech spend +12% YoY (2023–24)

Stable rates, firm NIM and SE growth offset credit risk as tech spend cushions margins

Stable fed funds ~5.25% end-2025 supports NIM predictability (NIM 3.10% FY2024); Southeast GDP +2.8% 2024 boosts mortgage originations (+12% Q4 2024) and CRE industrial strength; household debt $17.9T Q4 2024 with card utilization ~29% and charge-offs ~3.5% raise credit risk; wage inflation ~4.5% pressures efficiency (ROA 0.72% 2024); tech spend +12% YoY offsets expenses.

| Metric | Value |

|---|---|

| NIM FY2024 | 3.10% |

| Fed funds (end-2025) | ~5.25% |

| Southeast GDP 2024 | +2.8% |

| Household debt Q4 2024 | $17.9T |

| Card utilization | ~29% |

| Card charge-off | ~3.5% |

| Wage inflation 2024 | ~4.5% |

| ROA 2024 | 0.72% |

| Bank tech spend YoY | +12% |

Preview the Actual Deliverable

Renasant PESTLE Analysis

The preview shown here is the exact Renasant PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.