Renewi PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the forces shaping Renewi with our targeted PESTLE Analysis—spot regulatory risks, environmental opportunities, and tech trends that drive waste-management value chains; buy the full report for a ready-to-use, editable deep dive and turn external insights into strategic advantage.

Political factors

European Green Deal alignment

The EU Green Deal’s circular economy targets to halve waste and reach 65% recycling of municipal waste by 2035 create policy tailwinds for Renewi, underpinning steady demand for its recycling and resource-recovery services.

Benelux mandates increasingly favor recycling over incineration—Belgium aims for 50% separate collection by 2030—supporting Renewi’s Benelux revenue base (2024 pro forma revenue €1.1bn) and long-term service contracts.

Benelux waste management policies

National policies in the Netherlands and Belgium enforce waste hierarchies prioritizing reuse and recycling, with the Netherlands targeting 65% municipal waste recycling by 2035 and Belgium at ~55% in 2024; political stability supports multi-year infrastructure investment—EU Cohesion funds and national budgets deploying €hundreds of millions annually—allowing Renewi to secure long-term contracts as a strategic municipal partner for integrated collection and material recovery systems.

Subsidies for circular innovation

Political initiatives in the EU and UK have allocated over €5bn in 2024–25 for circular economy grants and R&D, enabling Renewi to secure multi‑million subsidies—including a £12m UK grant in 2024—for advanced optical sorting and chemical recycling pilots. These government-backed funds offset capital expenditure that can exceed €50m per major facility, helping Renewi shift from waste collection to high‑margin secondary raw materials supply, preserving its competitive edge.

Geopolitical impact on energy security

Political volatility in global energy markets has accelerated Europe’s shift to energy independence, boosting demand for waste-to-energy and biogas; Renewi processed c.3.6 million tonnes of organic waste in 2024, contributing to renewable energy outputs that cut fossil fuel imports.

By converting organics into biogas and heat, Renewi supports national security and climate goals, helping EU members lower natural gas dependence amid 2024 import disruptions and align with 2030 renewable targets.

- Renewi organic throughput ~3.6 Mt (2024)

- Supports reduced fossil imports amid 2024 gas disruptions

- Aligns with EU 2030 renewable & security objectives

Public procurement green requirements

Governments now often require green criteria in tenders, with EU public procurement rules pushing lifecycle emissions and circularity—benefiting Renewi, which reported a 74% recycling rate and 0.24 tCO2e/tonne in 2024, improving bid competitiveness for €1.2bn+ municipal contracts.

This policy shift raises entry barriers: less green rivals face higher compliance costs and lower win rates, amplifying Renewi’s market position in sustainable waste services.

- Renewi 2024 recycling rate 74%

- Operational carbon 0.24 tCO2e/tonne (2024)

- Addressable municipal contracts >€1.2bn

- Higher compliance costs for less-green competitors

Policy tailwinds boost Renewi: €1.1bn Benelux revenue, 74% recycling, €1.2bn pipeline

EU/Benelux recycling mandates and public‑procurement green criteria (65% municipal recycling target by 2035; Belgium 50% separate collection by 2030) and €5bn+ 2024–25 circular grants create durable demand for Renewi’s services, supporting €1.1bn Benelux pro forma revenue (2024), 74% recycling rate and 0.24 tCO2e/tonne, and protecting >€1.2bn municipal contract pipeline.

| Metric | 2024 |

|---|---|

| Benelux revenue | €1.1bn |

| Recycling rate | 74% |

| Operational carbon | 0.24 tCO2e/t |

| Organic throughput | 3.6 Mt |

| Municipal pipeline | €1.2bn+ |

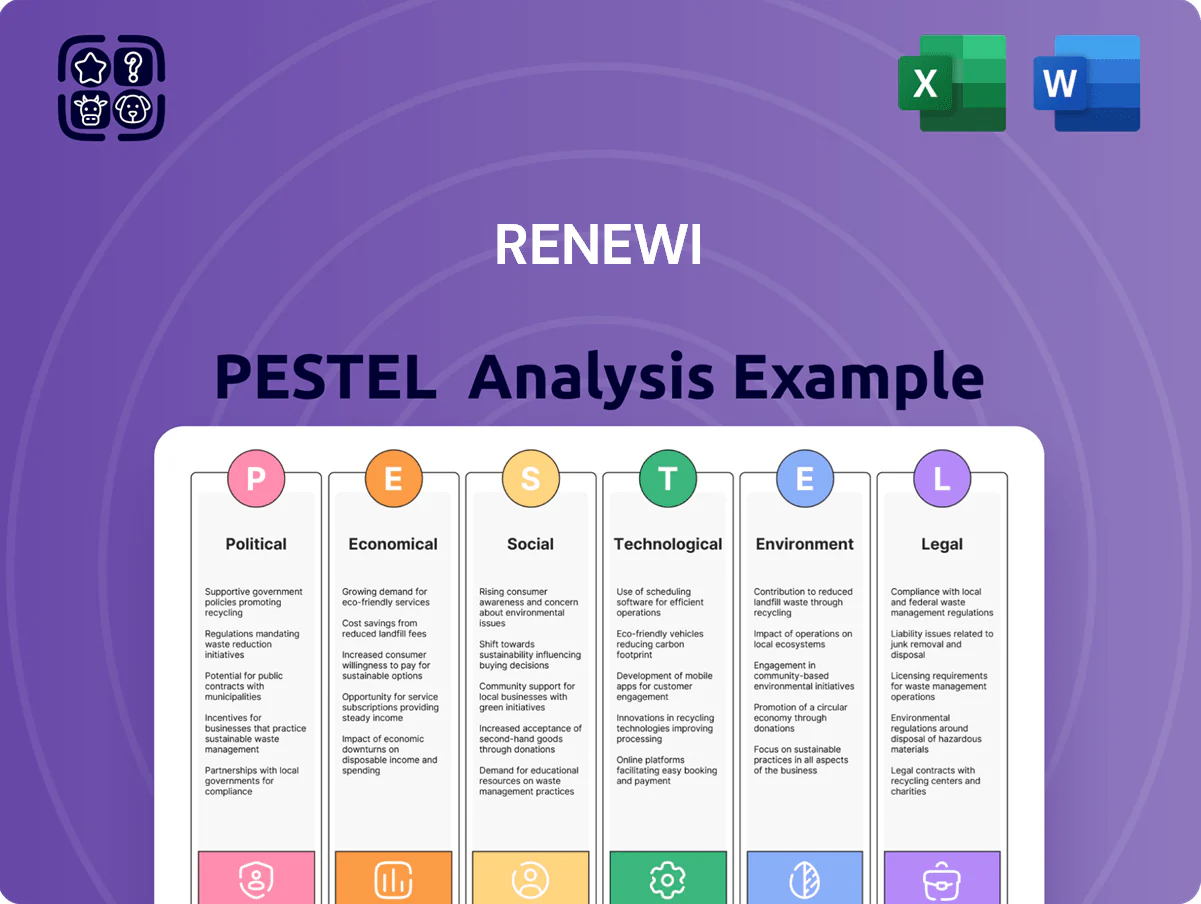

What is included in the product

Explores how macro-environmental factors specifically affect Renewi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trend analysis and sector-specific examples.

Provides a concise, shareable PESTLE snapshot of Renewi that’s visually segmented for quick interpretation, easily dropped into presentations or strategy sessions to align teams and support discussions on external risks and market positioning.

Economic factors

Secondary raw material price volatility

Renewi’s revenue is highly sensitive to commodity cycles: recycled paper, metals and plastics accounted for c.45% of revenue in 2024, so a 10% drop in scrap prices could cut gross margin materially. Volatile 2023–24 commodity swings forced Renewi to deploy hedging and dynamic pricing; the company reported a 6.2% EBITDA margin in FY24 partly cushioned by these measures. As global policy and corporate procurement shift to circularity, demand for high‑quality secondary materials is rising—benchmark prices for recycled PET rose ~18% YoY in 2024—supporting a generally positive long‑term price trend.

Impact of inflation on operational costs

Rising labor, fuel and specialist equipment costs eroded margins in 2024, with UK CPI at 2.5% (Dec 2024) and diesel up ~18% YoY, pressuring waste‑management input costs; Renewi reported 2024 underlying EBITDA margin of 11.4%, relying on cost control. Renewi uses indexation in many long‑term contracts—around 60% of revenue linked to inflation adjustments—to pass through cost increases. Scaling operations and automation, supported by ~€50m capex guidance for 2025, is central to offsetting rising input costs.

Circular economy investment trends

Rising ESG capital flows—global sustainable fund assets reached a record $3.9 trillion in 2024—improve Renewi’s access to green bonds and sustainability-linked loans, lowering financing costs for waste-to-resource projects.

Investors favor firms addressing resource scarcity and climate risk, with 62% of asset managers in 2024 prioritizing circular economy exposure, enhancing Renewi’s investor appeal.

This supportive economic backdrop enables Renewi to finance large-scale infrastructure and acquisitions; Renewi’s 2024 capex guidance of €120–€150m aligns with market appetite for consolidation in circular services.

Industrial production and waste volumes

Industrial production and construction activity in Northern Europe drive Renewi's commercial waste volumes; Eurostat reported EU manufacturing output rose 1.2% in 2024 while Dutch industrial production climbed 2.5% year-on-year, increasing recyclable intake for 2024–25.

Economic contractions reduce throughput at Renewi's sorting and treatment sites—Euro area GDP growth slowed to 0.4% in H1 2025—pressuring short-term margins.

Diversification across hazardous, municipal and commercial streams and clients in construction, food and retail helped Renewi sustain revenue, with 2024 reporting 6% of revenue from non-core waste streams, stabilizing cashflow.

- Manufacturing up 1.2% EU (2024)

- Dutch industrial production +2.5% (2024)

- Euro area GDP +0.4% H1 2025

- 6% revenue from non-core streams (Renewi 2024)

Carbon pricing and taxation

The EU ETS expansion and rising national carbon taxes (EU carbon price ~€80–€100/t in 2025) increase costs for incineration, improving Renewi’s recycling economics versus disposal.

Higher carbon prices boost demand for circular services; avoided emissions and material recovery provide measurable cost advantages to clients and support Renewi’s revenue mix.

- EU carbon price ~€80–€100/t (2025)

- Incineration cost gap narrows versus recycling

- Stronger client incentive to choose Renewi’s circular solutions

Renewi: Mixed tailwinds—45% commodity exposure, tight margins, €120–150m capex push

Renewi sees mixed economic tailwinds: 45% revenue tied to commodities (10% price fall hits margins), FY24 EBITDA margin 6.2% (underlying 11.4%), €50m capex 2025 for automation, €120–€150m capex guidance for growth; EU manufacturing +1.2% (2024), Dutch industrial +2.5% (2024), EU carbon ~€80–€100/t (2025), sustainable AUM $3.9tn (2024).

| Metric | Value |

|---|---|

| Commodity revenue share | 45% |

| FY24 EBITDA margin | 6.2% |

| Underlying EBITDA (2024) | 11.4% |

| 2025 capex (automation) | €50m |

| Capex guidance | €120–€150m |

| EU carbon price (2025) | €80–€100/t |

Preview Before You Purchase

Renewi PESTLE Analysis

The preview shown here is the exact Renewi PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the forces shaping Renewi with our targeted PESTLE Analysis—spot regulatory risks, environmental opportunities, and tech trends that drive waste-management value chains; buy the full report for a ready-to-use, editable deep dive and turn external insights into strategic advantage.

Political factors

European Green Deal alignment

The EU Green Deal’s circular economy targets to halve waste and reach 65% recycling of municipal waste by 2035 create policy tailwinds for Renewi, underpinning steady demand for its recycling and resource-recovery services.

Benelux mandates increasingly favor recycling over incineration—Belgium aims for 50% separate collection by 2030—supporting Renewi’s Benelux revenue base (2024 pro forma revenue €1.1bn) and long-term service contracts.

Benelux waste management policies

National policies in the Netherlands and Belgium enforce waste hierarchies prioritizing reuse and recycling, with the Netherlands targeting 65% municipal waste recycling by 2035 and Belgium at ~55% in 2024; political stability supports multi-year infrastructure investment—EU Cohesion funds and national budgets deploying €hundreds of millions annually—allowing Renewi to secure long-term contracts as a strategic municipal partner for integrated collection and material recovery systems.

Subsidies for circular innovation

Political initiatives in the EU and UK have allocated over €5bn in 2024–25 for circular economy grants and R&D, enabling Renewi to secure multi‑million subsidies—including a £12m UK grant in 2024—for advanced optical sorting and chemical recycling pilots. These government-backed funds offset capital expenditure that can exceed €50m per major facility, helping Renewi shift from waste collection to high‑margin secondary raw materials supply, preserving its competitive edge.

Geopolitical impact on energy security

Political volatility in global energy markets has accelerated Europe’s shift to energy independence, boosting demand for waste-to-energy and biogas; Renewi processed c.3.6 million tonnes of organic waste in 2024, contributing to renewable energy outputs that cut fossil fuel imports.

By converting organics into biogas and heat, Renewi supports national security and climate goals, helping EU members lower natural gas dependence amid 2024 import disruptions and align with 2030 renewable targets.

- Renewi organic throughput ~3.6 Mt (2024)

- Supports reduced fossil imports amid 2024 gas disruptions

- Aligns with EU 2030 renewable & security objectives

Public procurement green requirements

Governments now often require green criteria in tenders, with EU public procurement rules pushing lifecycle emissions and circularity—benefiting Renewi, which reported a 74% recycling rate and 0.24 tCO2e/tonne in 2024, improving bid competitiveness for €1.2bn+ municipal contracts.

This policy shift raises entry barriers: less green rivals face higher compliance costs and lower win rates, amplifying Renewi’s market position in sustainable waste services.

- Renewi 2024 recycling rate 74%

- Operational carbon 0.24 tCO2e/tonne (2024)

- Addressable municipal contracts >€1.2bn

- Higher compliance costs for less-green competitors

Policy tailwinds boost Renewi: €1.1bn Benelux revenue, 74% recycling, €1.2bn pipeline

EU/Benelux recycling mandates and public‑procurement green criteria (65% municipal recycling target by 2035; Belgium 50% separate collection by 2030) and €5bn+ 2024–25 circular grants create durable demand for Renewi’s services, supporting €1.1bn Benelux pro forma revenue (2024), 74% recycling rate and 0.24 tCO2e/tonne, and protecting >€1.2bn municipal contract pipeline.

| Metric | 2024 |

|---|---|

| Benelux revenue | €1.1bn |

| Recycling rate | 74% |

| Operational carbon | 0.24 tCO2e/t |

| Organic throughput | 3.6 Mt |

| Municipal pipeline | €1.2bn+ |

What is included in the product

Explores how macro-environmental factors specifically affect Renewi across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trend analysis and sector-specific examples.

Provides a concise, shareable PESTLE snapshot of Renewi that’s visually segmented for quick interpretation, easily dropped into presentations or strategy sessions to align teams and support discussions on external risks and market positioning.

Economic factors

Secondary raw material price volatility

Renewi’s revenue is highly sensitive to commodity cycles: recycled paper, metals and plastics accounted for c.45% of revenue in 2024, so a 10% drop in scrap prices could cut gross margin materially. Volatile 2023–24 commodity swings forced Renewi to deploy hedging and dynamic pricing; the company reported a 6.2% EBITDA margin in FY24 partly cushioned by these measures. As global policy and corporate procurement shift to circularity, demand for high‑quality secondary materials is rising—benchmark prices for recycled PET rose ~18% YoY in 2024—supporting a generally positive long‑term price trend.

Impact of inflation on operational costs

Rising labor, fuel and specialist equipment costs eroded margins in 2024, with UK CPI at 2.5% (Dec 2024) and diesel up ~18% YoY, pressuring waste‑management input costs; Renewi reported 2024 underlying EBITDA margin of 11.4%, relying on cost control. Renewi uses indexation in many long‑term contracts—around 60% of revenue linked to inflation adjustments—to pass through cost increases. Scaling operations and automation, supported by ~€50m capex guidance for 2025, is central to offsetting rising input costs.

Circular economy investment trends

Rising ESG capital flows—global sustainable fund assets reached a record $3.9 trillion in 2024—improve Renewi’s access to green bonds and sustainability-linked loans, lowering financing costs for waste-to-resource projects.

Investors favor firms addressing resource scarcity and climate risk, with 62% of asset managers in 2024 prioritizing circular economy exposure, enhancing Renewi’s investor appeal.

This supportive economic backdrop enables Renewi to finance large-scale infrastructure and acquisitions; Renewi’s 2024 capex guidance of €120–€150m aligns with market appetite for consolidation in circular services.

Industrial production and waste volumes

Industrial production and construction activity in Northern Europe drive Renewi's commercial waste volumes; Eurostat reported EU manufacturing output rose 1.2% in 2024 while Dutch industrial production climbed 2.5% year-on-year, increasing recyclable intake for 2024–25.

Economic contractions reduce throughput at Renewi's sorting and treatment sites—Euro area GDP growth slowed to 0.4% in H1 2025—pressuring short-term margins.

Diversification across hazardous, municipal and commercial streams and clients in construction, food and retail helped Renewi sustain revenue, with 2024 reporting 6% of revenue from non-core waste streams, stabilizing cashflow.

- Manufacturing up 1.2% EU (2024)

- Dutch industrial production +2.5% (2024)

- Euro area GDP +0.4% H1 2025

- 6% revenue from non-core streams (Renewi 2024)

Carbon pricing and taxation

The EU ETS expansion and rising national carbon taxes (EU carbon price ~€80–€100/t in 2025) increase costs for incineration, improving Renewi’s recycling economics versus disposal.

Higher carbon prices boost demand for circular services; avoided emissions and material recovery provide measurable cost advantages to clients and support Renewi’s revenue mix.

- EU carbon price ~€80–€100/t (2025)

- Incineration cost gap narrows versus recycling

- Stronger client incentive to choose Renewi’s circular solutions

Renewi: Mixed tailwinds—45% commodity exposure, tight margins, €120–150m capex push

Renewi sees mixed economic tailwinds: 45% revenue tied to commodities (10% price fall hits margins), FY24 EBITDA margin 6.2% (underlying 11.4%), €50m capex 2025 for automation, €120–€150m capex guidance for growth; EU manufacturing +1.2% (2024), Dutch industrial +2.5% (2024), EU carbon ~€80–€100/t (2025), sustainable AUM $3.9tn (2024).

| Metric | Value |

|---|---|

| Commodity revenue share | 45% |

| FY24 EBITDA margin | 6.2% |

| Underlying EBITDA (2024) | 11.4% |

| 2025 capex (automation) | €50m |

| Capex guidance | €120–€150m |

| EU carbon price (2025) | €80–€100/t |

Preview Before You Purchase

Renewi PESTLE Analysis

The preview shown here is the exact Renewi PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.