Resideo Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

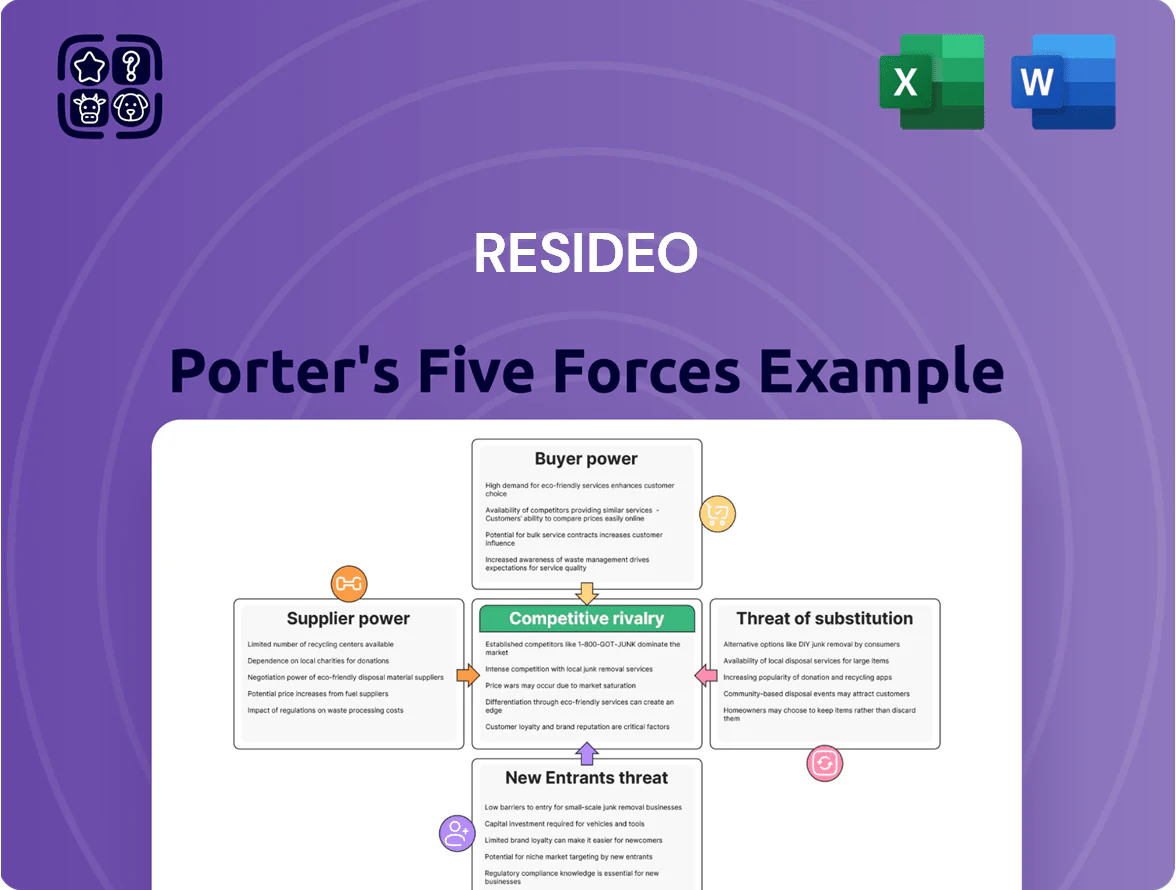

Resideo faces moderate buyer power and supplier influence, tempered by strong brand relationships in smart-home aftermarket channels, while rivalry is intensified by legacy HVAC and new IoT entrants—barriers to entry are moderate due to tech integration needs, and substitution risk hinges on platform convergence. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Resideo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and electronic component vendors

Resideo depends on specialized microchips and electronic sub-assemblies for its smart thermostats and security panels, and with the top 10 semiconductor firms controlling about 75% of global fab capacity in 2025, supplier leverage on pricing and lead times stays high.

Volatility in raw material costs for manufacturing

Resideo’s hardware production depends on plastics, metals and resins whose prices swung sharply in 2021–2023; e.g., global polyethylene costs rose ~40% in 2021 and copper averaged $9,500/ton in 2023, exposing margins to raw-material shocks.

Long-term contracts and supplier diversification reduce volatility, but essential inputs still give suppliers moderate pricing power; a 5–8% input-cost spike can shave several points off gross margin based on Resideo’s 2024 gross margin ~32%.

Dependency on third-party contract manufacturers

Resideo relies on a mix of internal plants and contract manufacturers for ~40–60% of production, and many partners hold niche automation and scale that would cost hundreds of millions to replicate.

That dependence gives suppliers leverage to press for higher margins; Resideo flagged supplier cost inflation in its FY2024 10-K, noting raw material and energy pressures pushed COGS up ~6% year-over-year.

Importance of proprietary software and cloud service providers

As Resideo moves into integrated smart-home ecosystems, reliance on cloud providers such as Amazon Web Services (AWS) and Microsoft Azure—which together held about 60% of global cloud market share in 2024—creates supplier power that directly affects uptime, latency, and data costs.

These providers host Resideo’s app connectivity and storage; their scale and proprietary services raise switching costs—migrating multi-region, containerized workloads can exceed millions of dollars and months of downtime—so they retain strong bargaining leverage.

What this estimate hides: vendor lock-in also ties Resideo to provider roadmaps and pricing changes, which can compress margins if usage grows (Resideo revenue was $2.9B in FY2024).

- Cloud market share (2024): AWS+Azure ≈60%

- Resideo FY2024 revenue: $2.9B

- Migration cost/time: potentially millions and months

- High switching costs → strong supplier bargaining power

Influence of logistics and freight shipping partners

Resideo’s ADI Global Distribution relies on global freight partners to deliver to professional installers; in 2024 freight costs rose ~18% year-over-year, squeezing margins for distribution-heavy peers.

Consolidation among carriers (top 5 global freight firms control ~60% of ocean capacity in 2024) gives providers leverage to raise fuel surcharges and lead times, directly raising Resideo’s distribution costs and inventory carrying needs.

Large logistics firms thus wield strong supplier power because timely, affordable shipping is essential to ADI’s inventory flow and service levels; a 1% rise in freight equals roughly 0.3–0.5% hit to gross margin for distribution segments.

- 2024 freight +18% YoY

- Top 5 carriers ≈60% ocean capacity

- 1% freight ↑ → 0.3–0.5% gross margin impact

Supplier concentration, material & logistics inflation threaten Resideo’s margins and $2.9B revenue

Suppliers exert moderate-to-strong power: semiconductors (top10 ≈75% fab capacity, 2025), raw-material price swings (polyethylene +40% in 2021; copper ~$9,500/ton in 2023), cloud providers (AWS+Azure ≈60% market, 2024), and consolidated freight (top5 ocean ≈60%, freight +18% in 2024) raise costs and switching costs, risking Resideo’s ~32% gross margin and $2.9B FY2024 revenue.

| Metric | Value |

|---|---|

| Top10 semiconductor fab share (2025) | ≈75% |

| Polyethylene price move (2021) | +40% |

| Copper avg price (2023) | $9,500/ton |

| AWS+Azure market share (2024) | ≈60% |

| Freight YoY (2024) | +18% |

| Resideo gross margin (2024) | ≈32% |

| Resideo FY2024 revenue | $2.9B |

What is included in the product

Tailored Porter's Five Forces analysis for Resideo that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to its market position, with actionable strategic insights.

A concise Porter's Five Forces one-sheet for Resideo—quickly spot competitive pressures and prioritize strategic responses to ease decision-making.

Customers Bargaining Power

High leverage of big-box retail chains

Large retailers such as The Home Depot and Best Buy represented roughly 28% of Resideo Technologies’ consumer revenue in FY2024, giving them strong leverage to push for lower wholesale prices and larger promotional allowances.

With national chains able to reallocate shelf space quickly, Resideo faces the risk of replacement by rival brands unless it offers attractive margins, exclusive SKUs, or marketing support.

As a result, Resideo increased retail marketing and channel discounts to about 6–8% of revenue in 2024 to defend shelf placement and brand visibility.

Influence of the professional installer and dealer network

A substantial share of Resideo’s fiscal 2024 revenue—about 62% of product sales—flows through professional HVAC and security contractors who act as gatekeepers and can switch brands based on installation ease or support, giving them high bargaining power.

Resideo counters this by running ADI Global Distribution, which provided training to over 45,000 technicians in 2024 and offers loyalty incentives that helped retain roughly 78% of its pro-channel customers that year.

Price sensitivity of residential homeowners

Individual homeowners are highly price-sensitive; 68% of US consumers compared smart-home prices online in 2024, limiting Resideo’s pricing power. Brand loyalty to Honeywell Home cushions churn—Resideo reported stable installed-base revenue of $1.1bn in FY2024—but surveys show 42% would switch for cheaper options if value gaps shrink. That sensitivity caps aggressive price hikes or Resideo risks share loss to low-cost competitors.

Low switching costs for smart home ecosystems

By late 2025, Matter interoperability lowers switching costs: 40% of US smart-home device shipments were Matter-capable in 2024, and adoption is rising, so consumers can mix brands with less friction.

That flexibility erodes Resideo’s ecosystem lock-in, forcing emphasis on superior UX, cloud features, and recurring services to defend ARPU and reduce churn.

- Matter adoption: ~40% of 2024 US shipments

- Risk: higher churn without strong software

- Response: invest in UX, cloud services, subscriptions

Volume requirements of commercial and multi-family developers

Large-scale builders and property managers buy Resideo comfort and security systems in bulk, securing discounts—US multifamily construction spending hit $212 billion in 2024, giving these buyers scale-based leverage.

They focus on total cost of ownership and multi-year service contracts, pushing Resideo to include comprehensive support and reduce lifecycle costs.

The ability to switch vendors across projects worth millions per development raises procurement leverage and pricing pressure on Resideo.

- 2024 US multifamily spend: $212B

- Buyers demand multi-year support

- Bulk purchases → significant discounts

- Vendor-switching raises Resideo negotiation risk

Resideo: Pro dominance, Matter easing pricing, 45k ADI techs and 78% pro retention

Customers hold strong leverage: big retailers ~28% of FY2024 consumer revenue, pro contractors ~62% of product sales, multifamily buyers influenced by $212B 2024 US spend; Matter adoption (~40% of 2024 US shipments) raises switching ease, capping pricing power. Resideo counters with ADI training (45,000 techs in 2024), 78% pro retention, and 6–8% revenue in retail/channel discounts.

| Metric | 2024 |

|---|---|

| Retailer share | 28% |

| Pro channel share | 62% |

| ADI trained techs | 45,000 |

| Pro retention | 78% |

| Retail/channel discounts | 6–8% rev |

| Matter adoption US | ~40% |

| Multifamily spend US | $212B |

Preview Before You Purchase

Resideo Porter's Five Forces Analysis

This preview shows the exact Resideo Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, ready for decision-making and presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Resideo faces moderate buyer power and supplier influence, tempered by strong brand relationships in smart-home aftermarket channels, while rivalry is intensified by legacy HVAC and new IoT entrants—barriers to entry are moderate due to tech integration needs, and substitution risk hinges on platform convergence. This brief snapshot only scratches the surface; unlock the full Porter's Five Forces Analysis to explore Resideo’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and electronic component vendors

Resideo depends on specialized microchips and electronic sub-assemblies for its smart thermostats and security panels, and with the top 10 semiconductor firms controlling about 75% of global fab capacity in 2025, supplier leverage on pricing and lead times stays high.

Volatility in raw material costs for manufacturing

Resideo’s hardware production depends on plastics, metals and resins whose prices swung sharply in 2021–2023; e.g., global polyethylene costs rose ~40% in 2021 and copper averaged $9,500/ton in 2023, exposing margins to raw-material shocks.

Long-term contracts and supplier diversification reduce volatility, but essential inputs still give suppliers moderate pricing power; a 5–8% input-cost spike can shave several points off gross margin based on Resideo’s 2024 gross margin ~32%.

Dependency on third-party contract manufacturers

Resideo relies on a mix of internal plants and contract manufacturers for ~40–60% of production, and many partners hold niche automation and scale that would cost hundreds of millions to replicate.

That dependence gives suppliers leverage to press for higher margins; Resideo flagged supplier cost inflation in its FY2024 10-K, noting raw material and energy pressures pushed COGS up ~6% year-over-year.

Importance of proprietary software and cloud service providers

As Resideo moves into integrated smart-home ecosystems, reliance on cloud providers such as Amazon Web Services (AWS) and Microsoft Azure—which together held about 60% of global cloud market share in 2024—creates supplier power that directly affects uptime, latency, and data costs.

These providers host Resideo’s app connectivity and storage; their scale and proprietary services raise switching costs—migrating multi-region, containerized workloads can exceed millions of dollars and months of downtime—so they retain strong bargaining leverage.

What this estimate hides: vendor lock-in also ties Resideo to provider roadmaps and pricing changes, which can compress margins if usage grows (Resideo revenue was $2.9B in FY2024).

- Cloud market share (2024): AWS+Azure ≈60%

- Resideo FY2024 revenue: $2.9B

- Migration cost/time: potentially millions and months

- High switching costs → strong supplier bargaining power

Influence of logistics and freight shipping partners

Resideo’s ADI Global Distribution relies on global freight partners to deliver to professional installers; in 2024 freight costs rose ~18% year-over-year, squeezing margins for distribution-heavy peers.

Consolidation among carriers (top 5 global freight firms control ~60% of ocean capacity in 2024) gives providers leverage to raise fuel surcharges and lead times, directly raising Resideo’s distribution costs and inventory carrying needs.

Large logistics firms thus wield strong supplier power because timely, affordable shipping is essential to ADI’s inventory flow and service levels; a 1% rise in freight equals roughly 0.3–0.5% hit to gross margin for distribution segments.

- 2024 freight +18% YoY

- Top 5 carriers ≈60% ocean capacity

- 1% freight ↑ → 0.3–0.5% gross margin impact

Supplier concentration, material & logistics inflation threaten Resideo’s margins and $2.9B revenue

Suppliers exert moderate-to-strong power: semiconductors (top10 ≈75% fab capacity, 2025), raw-material price swings (polyethylene +40% in 2021; copper ~$9,500/ton in 2023), cloud providers (AWS+Azure ≈60% market, 2024), and consolidated freight (top5 ocean ≈60%, freight +18% in 2024) raise costs and switching costs, risking Resideo’s ~32% gross margin and $2.9B FY2024 revenue.

| Metric | Value |

|---|---|

| Top10 semiconductor fab share (2025) | ≈75% |

| Polyethylene price move (2021) | +40% |

| Copper avg price (2023) | $9,500/ton |

| AWS+Azure market share (2024) | ≈60% |

| Freight YoY (2024) | +18% |

| Resideo gross margin (2024) | ≈32% |

| Resideo FY2024 revenue | $2.9B |

What is included in the product

Tailored Porter's Five Forces analysis for Resideo that uncovers competitive drivers, buyer/supplier power, entry barriers, substitutes, and disruptive threats to its market position, with actionable strategic insights.

A concise Porter's Five Forces one-sheet for Resideo—quickly spot competitive pressures and prioritize strategic responses to ease decision-making.

Customers Bargaining Power

High leverage of big-box retail chains

Large retailers such as The Home Depot and Best Buy represented roughly 28% of Resideo Technologies’ consumer revenue in FY2024, giving them strong leverage to push for lower wholesale prices and larger promotional allowances.

With national chains able to reallocate shelf space quickly, Resideo faces the risk of replacement by rival brands unless it offers attractive margins, exclusive SKUs, or marketing support.

As a result, Resideo increased retail marketing and channel discounts to about 6–8% of revenue in 2024 to defend shelf placement and brand visibility.

Influence of the professional installer and dealer network

A substantial share of Resideo’s fiscal 2024 revenue—about 62% of product sales—flows through professional HVAC and security contractors who act as gatekeepers and can switch brands based on installation ease or support, giving them high bargaining power.

Resideo counters this by running ADI Global Distribution, which provided training to over 45,000 technicians in 2024 and offers loyalty incentives that helped retain roughly 78% of its pro-channel customers that year.

Price sensitivity of residential homeowners

Individual homeowners are highly price-sensitive; 68% of US consumers compared smart-home prices online in 2024, limiting Resideo’s pricing power. Brand loyalty to Honeywell Home cushions churn—Resideo reported stable installed-base revenue of $1.1bn in FY2024—but surveys show 42% would switch for cheaper options if value gaps shrink. That sensitivity caps aggressive price hikes or Resideo risks share loss to low-cost competitors.

Low switching costs for smart home ecosystems

By late 2025, Matter interoperability lowers switching costs: 40% of US smart-home device shipments were Matter-capable in 2024, and adoption is rising, so consumers can mix brands with less friction.

That flexibility erodes Resideo’s ecosystem lock-in, forcing emphasis on superior UX, cloud features, and recurring services to defend ARPU and reduce churn.

- Matter adoption: ~40% of 2024 US shipments

- Risk: higher churn without strong software

- Response: invest in UX, cloud services, subscriptions

Volume requirements of commercial and multi-family developers

Large-scale builders and property managers buy Resideo comfort and security systems in bulk, securing discounts—US multifamily construction spending hit $212 billion in 2024, giving these buyers scale-based leverage.

They focus on total cost of ownership and multi-year service contracts, pushing Resideo to include comprehensive support and reduce lifecycle costs.

The ability to switch vendors across projects worth millions per development raises procurement leverage and pricing pressure on Resideo.

- 2024 US multifamily spend: $212B

- Buyers demand multi-year support

- Bulk purchases → significant discounts

- Vendor-switching raises Resideo negotiation risk

Resideo: Pro dominance, Matter easing pricing, 45k ADI techs and 78% pro retention

Customers hold strong leverage: big retailers ~28% of FY2024 consumer revenue, pro contractors ~62% of product sales, multifamily buyers influenced by $212B 2024 US spend; Matter adoption (~40% of 2024 US shipments) raises switching ease, capping pricing power. Resideo counters with ADI training (45,000 techs in 2024), 78% pro retention, and 6–8% revenue in retail/channel discounts.

| Metric | 2024 |

|---|---|

| Retailer share | 28% |

| Pro channel share | 62% |

| ADI trained techs | 45,000 |

| Pro retention | 78% |

| Retail/channel discounts | 6–8% rev |

| Matter adoption US | ~40% |

| Multifamily spend US | $212B |

Preview Before You Purchase

Resideo Porter's Five Forces Analysis

This preview shows the exact Resideo Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed is the same professionally written, fully formatted file you'll be able to download and use the moment you buy, ready for decision-making and presentation.