Resideo PESTLE Analysis

Your Competitive Advantage Starts with This Report

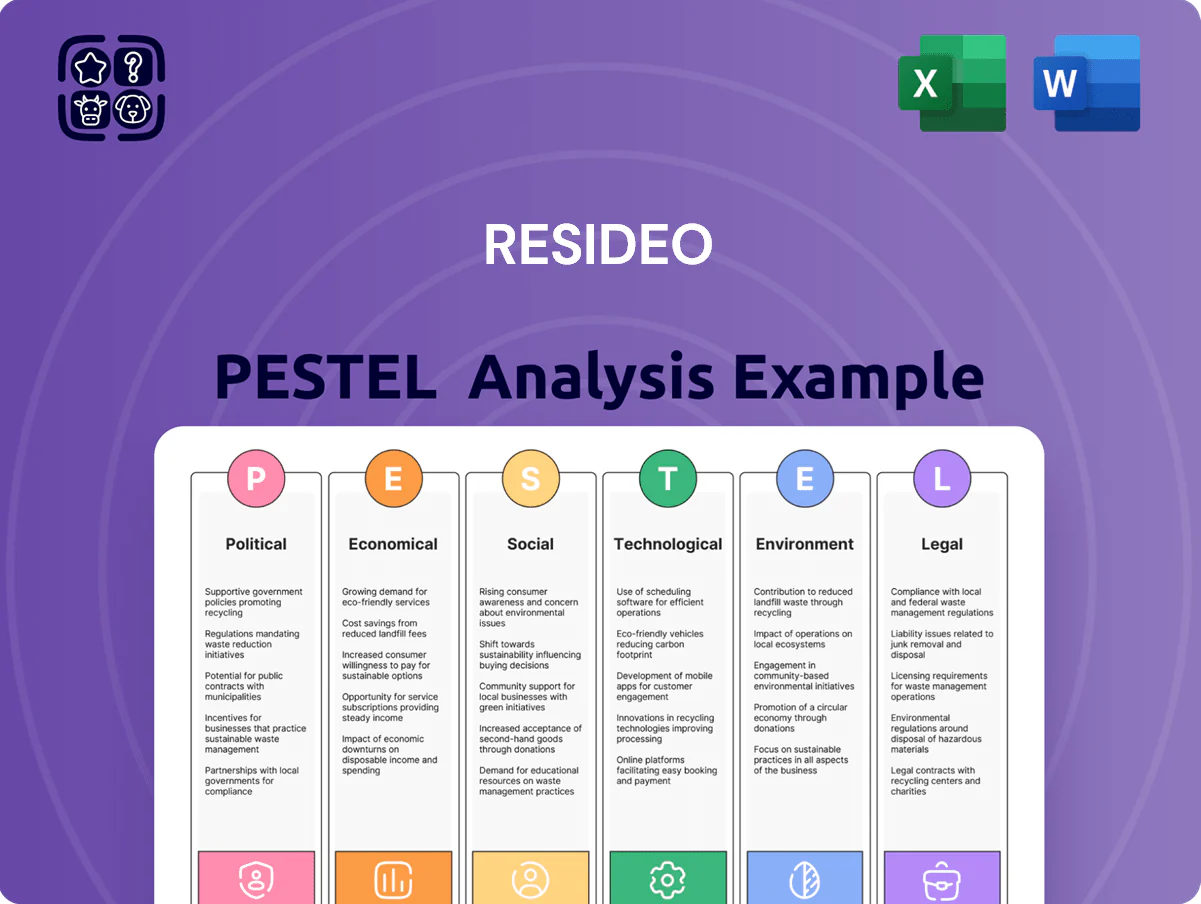

Gain a strategic advantage with our PESTLE Analysis of Resideo—concise, research-backed insights into the political, economic, social, technological, legal, and environmental forces shaping the company’s outlook; perfect for investors and strategists. Purchase the full report to access detailed risk assessments, opportunity mapping, and ready-to-use charts that accelerate smarter decisions.

Political factors

Global Trade and Tariff Policies

Changes in US tariff policy and renegotiated trade agreements with Asia and Mexico can raise Resideo's COGS; in 2024 Resideo reported 2023 gross margin of 27.1%, sensitive to input-cost shifts across its global supply chain. Protectionist moves forcing nearshoring or rerouting could add millions in logistics and capital costs, pressuring margins on security and comfort products. Management must monitor tariffs and adjust sourcing to sustain competitive pricing.

Government Energy Efficiency Incentives

Federal programs such as the Inflation Reduction Act offer tax credits and rebates—IRAs Home Efficiency Rebate and 30% tax credit for qualifying equipment—reducing upfront costs and increasing adoption of smart thermostats and HVAC controls; DOE estimates residential efficiency measures could cut household energy usage by up to 15% annually.

These mandates and incentives lower total cost of ownership, directly boosting demand for Resideo’s premium energy-management products; Resideo’s comfort segment, which represented ~40% of 2024 revenue, is positioned to capture market share as incentives persist.

Continued political support for residential decarbonization through 2025 is a primary growth driver, with analysts projecting smart thermostat penetration rising from ~20% in 2023 to 30–35% by 2025 under current incentive regimes.

Housing Policy and Urban Planning

Government pushes for affordable housing and higher residential density—e.g., US federal and state housing initiatives targeting 2–4 million new units by 2030—increase demand for Resideo’s HVAC, security and fire-safety systems tied to new builds; smart-city grants (over $100 billion in US infrastructure funding 2021–2025) and updated model building codes (IEBC/IRC adoptions increasing smart-home/fire-safety mandates) favor Resideo’s product mix; conversely, zoning restrictions or political gridlock slowing US housing starts (down ~6% YoY in 2024) would compress ADI Global Distribution’s project pipeline and revenue visibility.

Infrastructure and Security Standards

National security concerns over IoT and telecoms push regulators to restrict components in professional security systems; in 2024 US and EU measures targeted suppliers linked to sanctioned entities, impacting procurement for firms like Resideo.

Resideo must vet suppliers against government restricted-entity lists to retain eligibility for public contracts and large-scale residential projects—US federal procurement exclusions affected ~1,200 entities in 2024.

Political pressure raises certification and data-handling standards for connected home tech; stricter approvals can delay product launches and add compliance costs, estimated at 2–4% of revenue for security product lines in 2024.

- Regulatory tightening in 2024 targeted ~1,200 entities

- Compliance cost impact ~2–4% of security revenue

- Supply-chain vetting required for public contracts

International Regulatory Alignment

As a global operator, Resideo must adapt to differing political climates across EMEA and APAC that impose varied product standards and certification timelines, affecting time-to-market and compliance costs.

Political instability in select markets raises distribution disruption risk and can add 3–6% to operating expenses via higher insurance and security costs, per regional risk assessments in 2024.

Harmonizing product safety and wireless communication standards is critical to protect Resideo’s global share—noncompliance risks lost revenue in markets representing over 40% of international sales.

- Varied certification timelines increase compliance costs

- Instability can add 3–6% to operating expenses

- 40%+ of international sales sensitive to standards alignment

Resideo margins, regulatory costs and IRA rebates reshape smart-thermostat growth

Political factors: tariffs, trade shifts and protectionism can raise COGS and logistics costs; Resideo’s 2023 gross margin 27.1% is sensitive to input-cost shifts. IRA and federal rebates (30% tax credit; Home Efficiency Rebate) boost smart-thermostat demand; comfort ~40% of 2024 revenue. Regulatory vetting and tighter IoT/security rules (affecting ~1,200 entities in 2024) raise compliance ~2–4% of security revenue.

| Metric | Value |

|---|---|

| Gross margin (2023) | 27.1% |

| Comfort share (2024 rev) | ~40% |

| Smart-thermostat penetration (2023) | ~20% |

| Projected penetration (2025) | 30–35% |

| Entities targeted by regulations (2024) | ~1,200 |

| Compliance cost impact | 2–4% of security revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Resideo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section expanded into multiple, company-specific subpoints and forward-looking insights to support scenario planning.

Resideo PESTLE summary delivers a concise, visually segmented overview of external factors for quick interpretation in meetings or presentations, easily shareable and editable for team alignment or client reports.

Economic factors

Mortgage Rates and Housing Starts

Resideo's sales track the US housing cycle and mortgage rates; as of Dec 2025 the 30-year fixed mortgage averaged about 6.7%, up from ~3% in 2021, dampening new home starts which fell 8% year-over-year in 2024 and remained below pre-pandemic peaks. High rates reduce home turnovers and new-build demand for security, HVAC and smart-home installs, pressuring near-term revenue. Lower rates boost renovation spending—home improvement outlays rose 5% in 2024—creating retrofit opportunities for Resideo’s product mix.

Inflation and Material Costs

Fluctuations in prices for semiconductors, plastics and metals—semiconductor spot prices rose ~18% in 2023—directly pressure Resideo’s gross margins, given component intensity in smart-home products. Sustained inflation pushed US CPI to 3.4% in 2024, contributing to rising labor costs in Resideo’s manufacturing and distribution networks. The company may need price increases that risk testing consumer elasticity in ADI Global Distribution, where FY2024 gross margin was ~28.5%. Managing operational efficiency and sourcing is therefore critical to protect profitability.

Consumer Discretionary Spending

While Resideo sells essential safety devices, many smart-home upgrades remain discretionary; in 2024 US consumer discretionary spending fell 1.2% YoY, prompting homeowners to delay thermostat or automation upgrades and opt for repairs over replacements. Resideo’s tiered pricing and value-first offerings—reflected in 2024 service revenue growth of 8%—help cushion revenue volatility during economic contractions by retaining budget-conscious customers.

Currency Exchange Rate Volatility

With roughly 45% of Resideo’s FY2024 revenue generated outside the US, Dollar moves versus the Euro and other currencies materially affect reported EPS; a 5% USD strength versus EUR reduced 2024 reported revenue by an estimated 1.8%.

Economic instability in Europe and LATAM can create negative translation effects even with flat local volumes, as seen in Q3 2024 when FX reduced segment revenue by about $30 million.

Resideo employs hedging programs and natural currency offsets, but sustained weakness in key regional currencies remains a persistent risk to consolidated financial results and forecasting.

- ~45% FY2024 revenue non-US exposure

- 5% USD appreciation ≈ 1.8% revenue hit

- Q3 2024 FX impact ≈ $30M

- Hedging mitigates but does not eliminate prolonged currency risk

Labor Market Dynamics for Professional Installers

Resideo depends on a pro-channel of contractors; U.S. construction employment rose to 7.9 million in 2025 but skilled HVAC technicians remain scarce, with a 2024 BLS projection of 5% faster-than-average growth and ~28% of firms reporting hiring difficulty in 2024, constraining installation throughput.

Maintaining ADI Global Distribution as the preferred supplier preserves channel volume—ADI served ~300,000 pro customers in 2024—mitigating bottlenecks by providing training, inventory and financing programs.

- Construction employment 2025: 7.9M

- HVAC tech growth projection (BLS 2024): +5%

- Firms reporting hiring difficulty (2024): ~28%

- ADI pro customers (2024): ~300,000

Resideo: Housing slump, cost inflation & FX drag amid retrofit demand boost

Resideo revenue tied to US housing/mortgage cycles; 30-yr rate ~6.7% (Dec 2025) cut new starts and demand, while 2024 home improvement +5% aids retrofit sales. Input cost inflation (semiconductors +18% in 2023) and 2024 CPI 3.4% pressured margins; FY2024 non-US ~45% revenue exposes FX (5% USD↑ ≈ -1.8% revenue; Q3 2024 FX ≈ -$30M). Skilled HVAC shortages constrain installs.

| Metric | Value |

|---|---|

| Non-US revenue FY2024 | ~45% |

| 30-yr mortgage (Dec 2025) | ~6.7% |

| Home improvement 2024 | +5% |

| Semiconductor spot change 2023 | +18% |

| CPI 2024 (US) | 3.4% |

| FX Q3 2024 impact | ~-$30M |

Preview Before You Purchase

Resideo PESTLE Analysis

The preview shown here is the exact Resideo PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are identical to the file you’ll download immediately after payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our PESTLE Analysis of Resideo—concise, research-backed insights into the political, economic, social, technological, legal, and environmental forces shaping the company’s outlook; perfect for investors and strategists. Purchase the full report to access detailed risk assessments, opportunity mapping, and ready-to-use charts that accelerate smarter decisions.

Political factors

Global Trade and Tariff Policies

Changes in US tariff policy and renegotiated trade agreements with Asia and Mexico can raise Resideo's COGS; in 2024 Resideo reported 2023 gross margin of 27.1%, sensitive to input-cost shifts across its global supply chain. Protectionist moves forcing nearshoring or rerouting could add millions in logistics and capital costs, pressuring margins on security and comfort products. Management must monitor tariffs and adjust sourcing to sustain competitive pricing.

Government Energy Efficiency Incentives

Federal programs such as the Inflation Reduction Act offer tax credits and rebates—IRAs Home Efficiency Rebate and 30% tax credit for qualifying equipment—reducing upfront costs and increasing adoption of smart thermostats and HVAC controls; DOE estimates residential efficiency measures could cut household energy usage by up to 15% annually.

These mandates and incentives lower total cost of ownership, directly boosting demand for Resideo’s premium energy-management products; Resideo’s comfort segment, which represented ~40% of 2024 revenue, is positioned to capture market share as incentives persist.

Continued political support for residential decarbonization through 2025 is a primary growth driver, with analysts projecting smart thermostat penetration rising from ~20% in 2023 to 30–35% by 2025 under current incentive regimes.

Housing Policy and Urban Planning

Government pushes for affordable housing and higher residential density—e.g., US federal and state housing initiatives targeting 2–4 million new units by 2030—increase demand for Resideo’s HVAC, security and fire-safety systems tied to new builds; smart-city grants (over $100 billion in US infrastructure funding 2021–2025) and updated model building codes (IEBC/IRC adoptions increasing smart-home/fire-safety mandates) favor Resideo’s product mix; conversely, zoning restrictions or political gridlock slowing US housing starts (down ~6% YoY in 2024) would compress ADI Global Distribution’s project pipeline and revenue visibility.

Infrastructure and Security Standards

National security concerns over IoT and telecoms push regulators to restrict components in professional security systems; in 2024 US and EU measures targeted suppliers linked to sanctioned entities, impacting procurement for firms like Resideo.

Resideo must vet suppliers against government restricted-entity lists to retain eligibility for public contracts and large-scale residential projects—US federal procurement exclusions affected ~1,200 entities in 2024.

Political pressure raises certification and data-handling standards for connected home tech; stricter approvals can delay product launches and add compliance costs, estimated at 2–4% of revenue for security product lines in 2024.

- Regulatory tightening in 2024 targeted ~1,200 entities

- Compliance cost impact ~2–4% of security revenue

- Supply-chain vetting required for public contracts

International Regulatory Alignment

As a global operator, Resideo must adapt to differing political climates across EMEA and APAC that impose varied product standards and certification timelines, affecting time-to-market and compliance costs.

Political instability in select markets raises distribution disruption risk and can add 3–6% to operating expenses via higher insurance and security costs, per regional risk assessments in 2024.

Harmonizing product safety and wireless communication standards is critical to protect Resideo’s global share—noncompliance risks lost revenue in markets representing over 40% of international sales.

- Varied certification timelines increase compliance costs

- Instability can add 3–6% to operating expenses

- 40%+ of international sales sensitive to standards alignment

Resideo margins, regulatory costs and IRA rebates reshape smart-thermostat growth

Political factors: tariffs, trade shifts and protectionism can raise COGS and logistics costs; Resideo’s 2023 gross margin 27.1% is sensitive to input-cost shifts. IRA and federal rebates (30% tax credit; Home Efficiency Rebate) boost smart-thermostat demand; comfort ~40% of 2024 revenue. Regulatory vetting and tighter IoT/security rules (affecting ~1,200 entities in 2024) raise compliance ~2–4% of security revenue.

| Metric | Value |

|---|---|

| Gross margin (2023) | 27.1% |

| Comfort share (2024 rev) | ~40% |

| Smart-thermostat penetration (2023) | ~20% |

| Projected penetration (2025) | 30–35% |

| Entities targeted by regulations (2024) | ~1,200 |

| Compliance cost impact | 2–4% of security revenue |

What is included in the product

Explores how external macro-environmental factors uniquely affect Resideo across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section expanded into multiple, company-specific subpoints and forward-looking insights to support scenario planning.

Resideo PESTLE summary delivers a concise, visually segmented overview of external factors for quick interpretation in meetings or presentations, easily shareable and editable for team alignment or client reports.

Economic factors

Mortgage Rates and Housing Starts

Resideo's sales track the US housing cycle and mortgage rates; as of Dec 2025 the 30-year fixed mortgage averaged about 6.7%, up from ~3% in 2021, dampening new home starts which fell 8% year-over-year in 2024 and remained below pre-pandemic peaks. High rates reduce home turnovers and new-build demand for security, HVAC and smart-home installs, pressuring near-term revenue. Lower rates boost renovation spending—home improvement outlays rose 5% in 2024—creating retrofit opportunities for Resideo’s product mix.

Inflation and Material Costs

Fluctuations in prices for semiconductors, plastics and metals—semiconductor spot prices rose ~18% in 2023—directly pressure Resideo’s gross margins, given component intensity in smart-home products. Sustained inflation pushed US CPI to 3.4% in 2024, contributing to rising labor costs in Resideo’s manufacturing and distribution networks. The company may need price increases that risk testing consumer elasticity in ADI Global Distribution, where FY2024 gross margin was ~28.5%. Managing operational efficiency and sourcing is therefore critical to protect profitability.

Consumer Discretionary Spending

While Resideo sells essential safety devices, many smart-home upgrades remain discretionary; in 2024 US consumer discretionary spending fell 1.2% YoY, prompting homeowners to delay thermostat or automation upgrades and opt for repairs over replacements. Resideo’s tiered pricing and value-first offerings—reflected in 2024 service revenue growth of 8%—help cushion revenue volatility during economic contractions by retaining budget-conscious customers.

Currency Exchange Rate Volatility

With roughly 45% of Resideo’s FY2024 revenue generated outside the US, Dollar moves versus the Euro and other currencies materially affect reported EPS; a 5% USD strength versus EUR reduced 2024 reported revenue by an estimated 1.8%.

Economic instability in Europe and LATAM can create negative translation effects even with flat local volumes, as seen in Q3 2024 when FX reduced segment revenue by about $30 million.

Resideo employs hedging programs and natural currency offsets, but sustained weakness in key regional currencies remains a persistent risk to consolidated financial results and forecasting.

- ~45% FY2024 revenue non-US exposure

- 5% USD appreciation ≈ 1.8% revenue hit

- Q3 2024 FX impact ≈ $30M

- Hedging mitigates but does not eliminate prolonged currency risk

Labor Market Dynamics for Professional Installers

Resideo depends on a pro-channel of contractors; U.S. construction employment rose to 7.9 million in 2025 but skilled HVAC technicians remain scarce, with a 2024 BLS projection of 5% faster-than-average growth and ~28% of firms reporting hiring difficulty in 2024, constraining installation throughput.

Maintaining ADI Global Distribution as the preferred supplier preserves channel volume—ADI served ~300,000 pro customers in 2024—mitigating bottlenecks by providing training, inventory and financing programs.

- Construction employment 2025: 7.9M

- HVAC tech growth projection (BLS 2024): +5%

- Firms reporting hiring difficulty (2024): ~28%

- ADI pro customers (2024): ~300,000

Resideo: Housing slump, cost inflation & FX drag amid retrofit demand boost

Resideo revenue tied to US housing/mortgage cycles; 30-yr rate ~6.7% (Dec 2025) cut new starts and demand, while 2024 home improvement +5% aids retrofit sales. Input cost inflation (semiconductors +18% in 2023) and 2024 CPI 3.4% pressured margins; FY2024 non-US ~45% revenue exposes FX (5% USD↑ ≈ -1.8% revenue; Q3 2024 FX ≈ -$30M). Skilled HVAC shortages constrain installs.

| Metric | Value |

|---|---|

| Non-US revenue FY2024 | ~45% |

| 30-yr mortgage (Dec 2025) | ~6.7% |

| Home improvement 2024 | +5% |

| Semiconductor spot change 2023 | +18% |

| CPI 2024 (US) | 3.4% |

| FX Q3 2024 impact | ~-$30M |

Preview Before You Purchase

Resideo PESTLE Analysis

The preview shown here is the exact Resideo PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible in the preview are identical to the file you’ll download immediately after payment.