ResMed Porter's Five Forces Analysis

From Overview to Strategy Blueprint

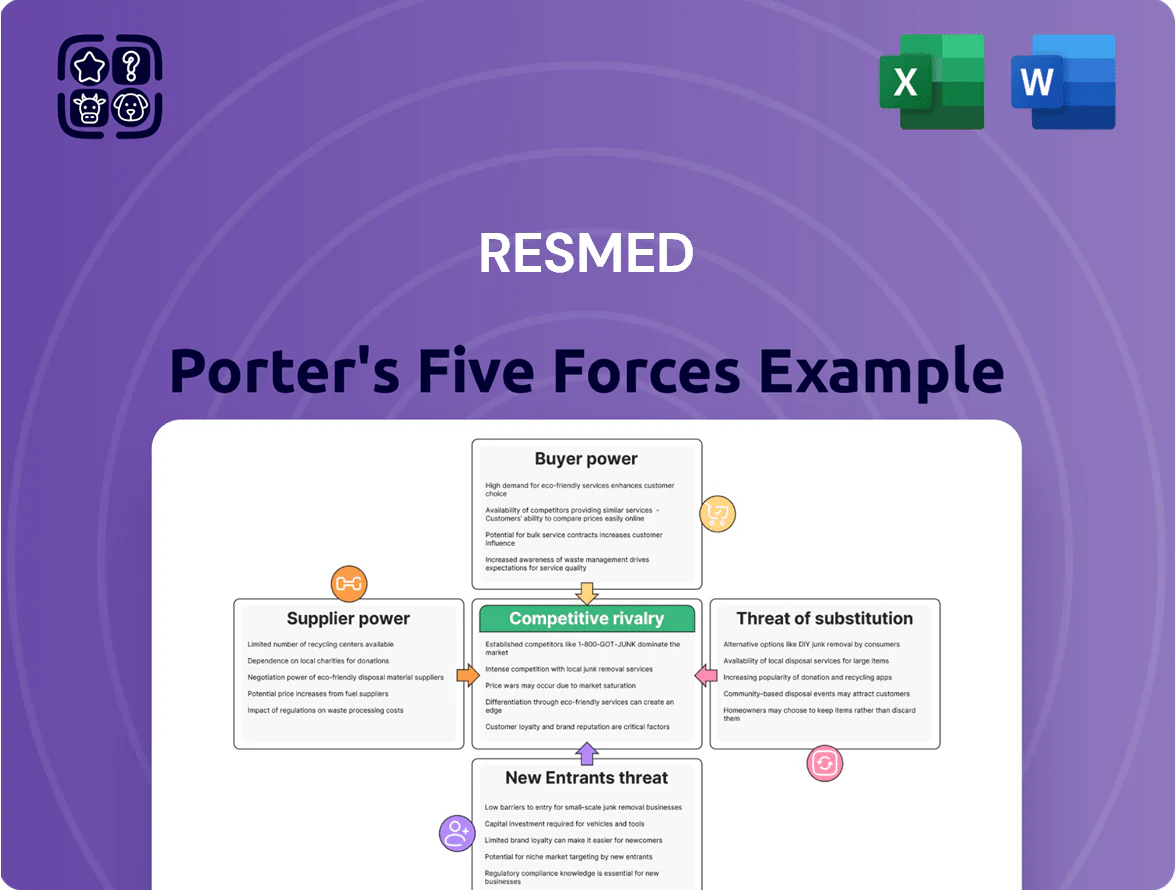

ResMed faces moderate supplier power, high buyer expectations, and robust competitive rivalry driven by innovation in sleep and respiratory care, while regulatory hurdles and substitute technologies pose evolving threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ResMed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized semiconductor and component reliance

ResMed depends on specialized medical-grade semiconductors and proprietary sensors for CPAP/bilevel devices; as of Dec 2025, medical chip suppliers saw ~12% higher ASPs than general chips, giving suppliers pricing power.

Although the global chip shortage eased in 2025, demand for certified medical silicon remains ~20% above pre‑pandemic levels, so single-source suppliers hold leverage.

ResMed mitigates risk by maintaining multi-sourcing and long‑term contracts; in 2024 it reported >30% of components sourced from dual suppliers to ensure continuity.

Raw material price volatility

Suppliers of medical-grade plastics, silicone, and resins hold moderate bargaining power for ResMed because switching risks voiding FDA/CE certifications and delays; in 2024 ResMed reported COGS rising 6.8% year-over-year, partly from input costs. Petroleum-based feedstock swings drove resin prices up ~22% in 2023–24, squeezing gross margin (ResMed GAAP gross margin fell from 57.1% in FY2023 to 55.4% in FY2024).

Consolidation of logistics and distribution partners

Consolidation among global shippers has cut Tier 1 providers, leaving few capable of safely moving sensitive medical devices; DHL, Maersk, and Kuehne+Nagel handled roughly 40% of global container volume in 2024, boosting their leverage.

That concentration lets logistics firms push higher rates and stricter terms—ocean freight rates spiked 22% in 2023–24 on key lanes, hitting suppliers’ negotiating position.

ResMed’s 140+ country footprint and FY2025 supply-chain spend sensitivity mean a 10% freight-cost rise could shave several percentage points off operating margin; shipping reliability directly affects device availability.

Proprietary software and cloud infrastructure providers

ResMed’s AirView and myAir run largely on AWS and Azure, making cloud providers critical suppliers whose platforms host millions of patient records and telehealth services.

Moving that data is costly: estimates run $5–50M for enterprise migrations plus months of downtime risk, creating supplier lock-in that raises switching costs and operational risk.

Cloud vendors also influence compliance and uptime; AWS/Azure SLAs and security features directly affect ResMed’s HIPAA/GDPR posture and service margins.

- Millions of patient records stored on AWS/Azure

- Estimated migration cost $5–50M and months of work

- High switching cost = supplier lock-in

- Cloud SLAs affect compliance, uptime, margins

Limited alternative for high-precision motors

The quiet, high-efficiency motors in ResMed CPAPs are made by a handful of global suppliers meeting medical-grade specs; industry reports in 2024 cite fewer than 6 qualified manufacturers worldwide, concentrating bargaining power.

Any supply disruption would halt production—ResMed reported 2023 inventory turn of ~6x, so halted motor supply could pause months of output and revenue.

Suppliers therefore command leverage in pricing and lead times, reducing ResMed’s negotiating room absent redesign or dual-sourcing.

- Fewer than 6 qualified motor makers (2024)

- ResMed inventory turns ~6x (2023)

- Single-component disruption → months of downtime

Suppliers’ concentrated power inflates costs, raises switching barriers and squeezes margins

Suppliers hold moderate-to-high bargaining power: few qualified motor and medical-chip makers (fewer than 6 and single-source premium ≈+12% ASPs, 2024–25), concentrated logistics (DHL/Maersk/Kuehne ≈40% container share, 2024) and cloud lock-in (AWS/Azure hosting millions of patient records; migration $5–50M) raise switching costs and pressure margins (ResMed GAAP gross margin 55.4% FY2024).

| Metric | Value |

|---|---|

| Qualified motor makers (2024) | fewer than 6 |

| Medical chip ASP premium (2025) | ≈+12% |

| Container share (top 3, 2024) | ≈40% |

| ResMed GAAP gross margin (FY2024) | 55.4% |

| Estimated cloud migration | $5–50M |

What is included in the product

Tailored exclusively for ResMed, this Porter’s Five Forces overview uncovers the key drivers of competition, buyer and supplier power, substitution risks, and barriers to entry, highlighting disruptive forces and strategic levers that influence ResMed’s pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot tailored to ResMed—clarifies competitive pressures across suppliers, buyers, entrants, substitutes, and rivalry for swift strategic decisions.

Customers Bargaining Power

Concentration of Durable Medical Equipment providers

A large share of ResMed’s 2024 revenue—about 38% of device sales—flows through a handful of DME distributors, giving them strong volume leverage; top 5 DMEs negotiated average discounts rising to ~14% in 2024. Continued consolidation in 2025 (M&A deals up 22% YoY) will let these intermediaries press for deeper discounts and extended payment terms, squeezing ResMed’s gross margins unless negotiated volume-based countermeasures are adopted.

Influence of private and public payers

Insurance firms and programs like Medicare set reimbursement for sleep-apnea care; in 2024 Medicare Part B paid about $200–$350 for initial CPAP supplies and capped durable medical equipment reimbursements, constraining ResMed’s pricing power.

If payers cut CPAP coverage, ResMed must lower prices or lose access; a 10% payer rate reduction could reduce device revenue by an estimated $150–200 million annually based on 2024 device sales.

Value-based care pushes ResMed to show cost-effectiveness: studies citing 20–30% reductions in hospital readmissions with PAP therapy support coverage negotiations and preserve favorable payer terms.

Patient brand loyalty and switching costs

Individual patients now act like informed consumers, with 62% of CPAP users in a 2024 ResMed study citing comfort and app connectivity as primary brand drivers.

Integration into ResMed’s myAir app creates data continuity—average user adherence tracked over 12 months—raising switching costs and locking patients into the ecosystem.

That patient-brand affinity offsets some institutional price pressure: ResMed reported 2024 device ASPs steady despite channel discounts, helping protect margins.

Direct-to-consumer market expansion

The growth of online retail and direct-to-consumer (DTC) channels lets ResMed reach patients directly, bypassing DMEs and national distributors so it can better control retail pricing and data capture.

DTC reduces reliance on large DMEs — ResMed reported ~18% of revenue from channels enabling direct sales in FY2025 — but consumers remain highly price-sensitive and compare products to lower-cost CPAP alternatives online.

Hospital system procurement power

- Centralized procurement = stronger buyer leverage

- Competitive bids: ResMed vs Fisher & Paykel

- Software + hardware needed to win contracts

- Digital tools can cut ventilation days ~10%

Buyers squeeze prices but outcomes data and DTC cushion CPAP ASPs

Buyers (DMEs, payers, hospitals, patients) exert high bargaining power: top 5 DMEs drove ~38% of device sales with avg discounts ~14% in 2024; Medicare caps reimbursements ($200–$350 for initial CPAP supplies); DTC ≈18% FY2025 reduces DME reliance but price-sensitive users persist; value-based evidence (20–30% fewer readmissions) and myAir adherence data raise switching costs, partially protecting ASPs.

| Buyer | Key stat |

|---|---|

| Top 5 DMEs | 38% sales; 14% avg discount (2024) |

| Medicare | $200–$350 initial CPAP (2024) |

| DTC | 18% revenue (FY2025) |

| Clinical evidence | 20–30% fewer readmissions |

Preview Before You Purchase

ResMed Porter's Five Forces Analysis

This preview shows the exact ResMed Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate use.

It covers competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry with actionable insights and data-driven conclusions; what you see here is the same complete document available for instant download once you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

ResMed faces moderate supplier power, high buyer expectations, and robust competitive rivalry driven by innovation in sleep and respiratory care, while regulatory hurdles and substitute technologies pose evolving threats.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore ResMed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized semiconductor and component reliance

ResMed depends on specialized medical-grade semiconductors and proprietary sensors for CPAP/bilevel devices; as of Dec 2025, medical chip suppliers saw ~12% higher ASPs than general chips, giving suppliers pricing power.

Although the global chip shortage eased in 2025, demand for certified medical silicon remains ~20% above pre‑pandemic levels, so single-source suppliers hold leverage.

ResMed mitigates risk by maintaining multi-sourcing and long‑term contracts; in 2024 it reported >30% of components sourced from dual suppliers to ensure continuity.

Raw material price volatility

Suppliers of medical-grade plastics, silicone, and resins hold moderate bargaining power for ResMed because switching risks voiding FDA/CE certifications and delays; in 2024 ResMed reported COGS rising 6.8% year-over-year, partly from input costs. Petroleum-based feedstock swings drove resin prices up ~22% in 2023–24, squeezing gross margin (ResMed GAAP gross margin fell from 57.1% in FY2023 to 55.4% in FY2024).

Consolidation of logistics and distribution partners

Consolidation among global shippers has cut Tier 1 providers, leaving few capable of safely moving sensitive medical devices; DHL, Maersk, and Kuehne+Nagel handled roughly 40% of global container volume in 2024, boosting their leverage.

That concentration lets logistics firms push higher rates and stricter terms—ocean freight rates spiked 22% in 2023–24 on key lanes, hitting suppliers’ negotiating position.

ResMed’s 140+ country footprint and FY2025 supply-chain spend sensitivity mean a 10% freight-cost rise could shave several percentage points off operating margin; shipping reliability directly affects device availability.

Proprietary software and cloud infrastructure providers

ResMed’s AirView and myAir run largely on AWS and Azure, making cloud providers critical suppliers whose platforms host millions of patient records and telehealth services.

Moving that data is costly: estimates run $5–50M for enterprise migrations plus months of downtime risk, creating supplier lock-in that raises switching costs and operational risk.

Cloud vendors also influence compliance and uptime; AWS/Azure SLAs and security features directly affect ResMed’s HIPAA/GDPR posture and service margins.

- Millions of patient records stored on AWS/Azure

- Estimated migration cost $5–50M and months of work

- High switching cost = supplier lock-in

- Cloud SLAs affect compliance, uptime, margins

Limited alternative for high-precision motors

The quiet, high-efficiency motors in ResMed CPAPs are made by a handful of global suppliers meeting medical-grade specs; industry reports in 2024 cite fewer than 6 qualified manufacturers worldwide, concentrating bargaining power.

Any supply disruption would halt production—ResMed reported 2023 inventory turn of ~6x, so halted motor supply could pause months of output and revenue.

Suppliers therefore command leverage in pricing and lead times, reducing ResMed’s negotiating room absent redesign or dual-sourcing.

- Fewer than 6 qualified motor makers (2024)

- ResMed inventory turns ~6x (2023)

- Single-component disruption → months of downtime

Suppliers’ concentrated power inflates costs, raises switching barriers and squeezes margins

Suppliers hold moderate-to-high bargaining power: few qualified motor and medical-chip makers (fewer than 6 and single-source premium ≈+12% ASPs, 2024–25), concentrated logistics (DHL/Maersk/Kuehne ≈40% container share, 2024) and cloud lock-in (AWS/Azure hosting millions of patient records; migration $5–50M) raise switching costs and pressure margins (ResMed GAAP gross margin 55.4% FY2024).

| Metric | Value |

|---|---|

| Qualified motor makers (2024) | fewer than 6 |

| Medical chip ASP premium (2025) | ≈+12% |

| Container share (top 3, 2024) | ≈40% |

| ResMed GAAP gross margin (FY2024) | 55.4% |

| Estimated cloud migration | $5–50M |

What is included in the product

Tailored exclusively for ResMed, this Porter’s Five Forces overview uncovers the key drivers of competition, buyer and supplier power, substitution risks, and barriers to entry, highlighting disruptive forces and strategic levers that influence ResMed’s pricing, profitability, and market defense.

A concise Porter's Five Forces snapshot tailored to ResMed—clarifies competitive pressures across suppliers, buyers, entrants, substitutes, and rivalry for swift strategic decisions.

Customers Bargaining Power

Concentration of Durable Medical Equipment providers

A large share of ResMed’s 2024 revenue—about 38% of device sales—flows through a handful of DME distributors, giving them strong volume leverage; top 5 DMEs negotiated average discounts rising to ~14% in 2024. Continued consolidation in 2025 (M&A deals up 22% YoY) will let these intermediaries press for deeper discounts and extended payment terms, squeezing ResMed’s gross margins unless negotiated volume-based countermeasures are adopted.

Influence of private and public payers

Insurance firms and programs like Medicare set reimbursement for sleep-apnea care; in 2024 Medicare Part B paid about $200–$350 for initial CPAP supplies and capped durable medical equipment reimbursements, constraining ResMed’s pricing power.

If payers cut CPAP coverage, ResMed must lower prices or lose access; a 10% payer rate reduction could reduce device revenue by an estimated $150–200 million annually based on 2024 device sales.

Value-based care pushes ResMed to show cost-effectiveness: studies citing 20–30% reductions in hospital readmissions with PAP therapy support coverage negotiations and preserve favorable payer terms.

Patient brand loyalty and switching costs

Individual patients now act like informed consumers, with 62% of CPAP users in a 2024 ResMed study citing comfort and app connectivity as primary brand drivers.

Integration into ResMed’s myAir app creates data continuity—average user adherence tracked over 12 months—raising switching costs and locking patients into the ecosystem.

That patient-brand affinity offsets some institutional price pressure: ResMed reported 2024 device ASPs steady despite channel discounts, helping protect margins.

Direct-to-consumer market expansion

The growth of online retail and direct-to-consumer (DTC) channels lets ResMed reach patients directly, bypassing DMEs and national distributors so it can better control retail pricing and data capture.

DTC reduces reliance on large DMEs — ResMed reported ~18% of revenue from channels enabling direct sales in FY2025 — but consumers remain highly price-sensitive and compare products to lower-cost CPAP alternatives online.

Hospital system procurement power

- Centralized procurement = stronger buyer leverage

- Competitive bids: ResMed vs Fisher & Paykel

- Software + hardware needed to win contracts

- Digital tools can cut ventilation days ~10%

Buyers squeeze prices but outcomes data and DTC cushion CPAP ASPs

Buyers (DMEs, payers, hospitals, patients) exert high bargaining power: top 5 DMEs drove ~38% of device sales with avg discounts ~14% in 2024; Medicare caps reimbursements ($200–$350 for initial CPAP supplies); DTC ≈18% FY2025 reduces DME reliance but price-sensitive users persist; value-based evidence (20–30% fewer readmissions) and myAir adherence data raise switching costs, partially protecting ASPs.

| Buyer | Key stat |

|---|---|

| Top 5 DMEs | 38% sales; 14% avg discount (2024) |

| Medicare | $200–$350 initial CPAP (2024) |

| DTC | 18% revenue (FY2025) |

| Clinical evidence | 20–30% fewer readmissions |

Preview Before You Purchase

ResMed Porter's Five Forces Analysis

This preview shows the exact ResMed Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups, fully formatted and ready for immediate use.

It covers competitive rivalry, supplier and buyer power, threat of substitution, and barriers to entry with actionable insights and data-driven conclusions; what you see here is the same complete document available for instant download once you buy.