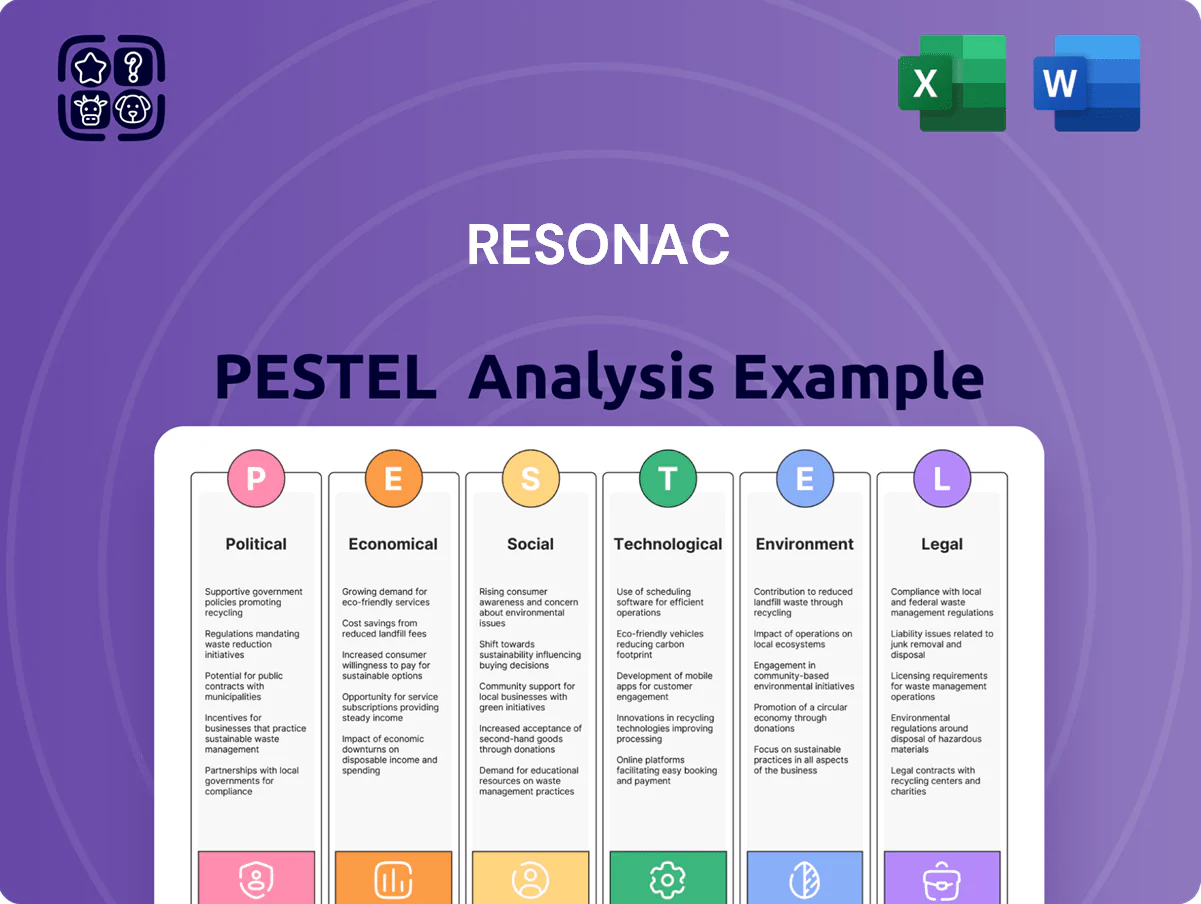

Resonac PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our Resonac PESTLE Analysis—concise, expert-backed insight into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors, consultants, and planners. Purchase the full report to access deep-dive findings, actionable recommendations, and ready-to-use Word/Excel files that save research time and power smarter decisions—download instantly.

Political factors

Geopolitical Semiconductor Alliances

The Japan–US semiconductor partnership in late 2025 strengthens supply-chain security for critical materials; bilateral deals have supported a 12% increase in Japan-US high-end materials trade to $8.9bn in 2024, benefiting Resonac which supplies photoresists and polishing slurries.

Export Control Regulations

Strict export controls on advanced technology to China, Russia and certain Southeast Asian nations pressure Japanese chemical firms; in 2024 Japan issued over 1,200 individual export licenses for electronics-related chemicals, tightening approvals for products classified under HS codes used by Resonac.

Resonac must navigate complex licensing and end-use checks to protect ~$1.8bn in FY2024 electronics-related revenue, balancing compliance costs that rose an estimated 6–9% with efforts to retain global market share.

These rules require a robust internal monitoring framework—including automated screening and audit trails—to reduce trade-flow disruptions and limit political friction that could impact up to 15% of export volumes to controlled regions.

Domestic Industrial Subsidies

Japan committed about JPY 1.4 trillion (≈USD 10.0bn) through 2025 to bolster domestic semiconductor supply chains; Resonac has tapped these industrial subsidies to underwrite roughly JPY 30–50 billion in capex for next‑generation packaging materials and SiC power semiconductor projects, cutting R&D financing needs and lowering project-level risk, effectively de-risking capital-intensive development and accelerating commercialization timelines.

Energy Policy and Security

Japan's 2030 energy plan targets 20-22% renewables and 20-22% nuclear; renewed reactor restarts cut wholesale power costs, directly lowering Resonac's energy expenses for its 2024 petrochemical output valued at ~¥250bn.

Carbon pricing proposals (est. ¥5,000–¥10,000/ton CO2) and subsidies for green hydrogen affect feedstock competitiveness, raising potential operating costs for energy-intensive units if implemented.

Aligning with national energy security—stockpiling LNG and promoting domestic power—supports stable supply chains critical to Resonac's long-term manufacturing continuity.

- 2030 targets: 20-22% renewables, 20-22% nuclear

- Wholesale power down with reactor restarts → lower OPEX for petrochemicals

- Carbon price range ¥5,000–¥10,000/ton impacts margins

- Energy security measures (LNG, domestic generation) reduce supply risk

Regional Stability in Southeast Asia

Resonac’s manufacturing footprint in Southeast Asia—accounting for about 28% of its 2024 consolidated production capacity—faces risks from political shifts in Indonesia, Thailand and Vietnam; localized unrest could disrupt supply chains and spike logistic costs by an estimated 4–7%.

To mitigate this, Resonac keeps diversified sites across multiple countries and invested ¥32.4bn (approx $225m) in 2024 capacity resilience and logistics redundancy.

Ongoing government engagement secures permits and infrastructure support, with recent MOUs in 2024 reducing tariff exposure and expediting utilities for two major plants.

- 28% of capacity in SEA

- Potential 4–7% logistic cost shock from local disruptions

- ¥32.4bn invested in resilience (2024)

- 2024 MOUs to lower tariff and utility delays

Geopolitics Hit Resonac: $1.8bn Revenue Risk, ¥32.4bn Resilience Spend, 28% SEA

Political drivers—US-Japan semiconductor deals, tight export controls, energy policy and SEA geopolitical risk—directly affect Resonac’s supply chains, compliance costs, capex funding and energy/OPEX; 2024 figures: ~$1.8bn electronics revenue exposure, JPY30–50bn capex subsidies, ¥32.4bn resilience spend, 28% capacity in SEA, carbon price ¥5,000–¥10,000/ton.

| Metric | 2024/2025 |

|---|---|

| Electronics revenue at risk | $1.8bn |

| Capex subsidies used | JPY30–50bn |

| Resilience spend | ¥32.4bn |

| SEA capacity | 28% |

| Carbon price range | ¥5,000–¥10,000/ton |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Resonac, with data-backed trends and region-specific examples to surface risks and opportunities for executives, investors, and strategists.

Condenses Resonac's PESTLE into a clean, shareable summary that highlights key external risks and opportunities by category, enabling quick alignment in meetings, slide decks, or client reports.

Economic factors

Global Semiconductor Market Recovery

By end-2025 the global semiconductor market returned to robust growth with industry revenues forecast at about $700 billion for 2025, up ~12% year-on-year, fueling demand for Resonac’s high-purity ceramic and dielectric materials used in HPC and AI chips.

Currency Exchange Rate Volatility

The JPY/USD swung ~8% in 2024, and a weaker yen boosted Resonac’s export competitiveness but raised naphtha import costs by an estimated ¥6–8 billion in FY2024, pressuring gross margins. Resonac reported FX losses of ¥1.2 billion in Q3 2024; implementing layered hedging (forwards, options) and natural hedges is vital to stabilize EBITDA and protect margins against further volatility.

Raw Material and Energy Costs

Global commodity price volatility pushed naphtha and ethylene feedstock costs up ~18% YoY in 2024, lifting basic chemical input costs and squeezing Resonac’s margins.

With petrochemical product price realizations lagging, Resonac struggles to fully pass through higher costs without volume loss in competitive domestic and Asian markets.

Oil/gas market shifts—LNG spot prices fell ~12% in 2025 H1 while crude remained volatile—drive Resonac to invest in resource-efficient processes to cut feedstock intensity and lower unit costs.

Inflationary Trends and Wage Growth

Persistent inflation—2024 CPI averaged 3.5% in the US and 4.0% in the EU—has pushed nominal wages up, increasing Resonac’s labor and operational costs across global plants.

Resonac must balance competitive pay to retain specialized staff while enforcing strict cost controls to protect margins; 2024 sector wage growth ranged 4–6% in chemical manufacturing.

To offset rising wages, the firm needs accelerated automation and productivity gains; capital expenditure on automation rose ~8% industrywide in 2024.

- 2024 CPI: US 3.5%, EU 4.0%

- Chemical sector wage growth: 4–6% (2024)

- Industry automation capex +8% (2024)

Interest Rate Environments

Monetary policy shifts by the Bank of Japan and global central banks directly affect Resonac’s borrowing costs for infrastructure and expansion; JPY corporate lending spreads fell to about 0.9% in H2 2025 from 1.4% in 2024, easing financing pressure.

With headline interest rates stabilizing in late 2025—BOJ moving toward normalization and global 10-year yields retreating to ~3.5%—Resonac gains more favorable conditions for long-term project financing and capex.

This lower-rate backdrop underpins an aggressive M&A push: Resonac completed or announced deals totaling roughly JPY 120–150 billion in 2025, leveraging cheaper debt to expand its chemical and materials portfolio.

- H2 2025 corporate lending spreads ≈ 0.9% (vs 1.4% in 2024)

- Global 10-year yields ≈ 3.5% in late 2025

- Resonac M&A activity ~JPY 120–150bn in 2025

Resonac rides $700B chip boom as costs, FX and wages squeeze margins; ¥120–150bn M&A

Global semiconductor demand (2025 est. ~$700bn, +12% YoY) boosts Resonac product demand; weaker JPY (~-8% in 2024) improved exports but added ~¥6–8bn naphtha cost and ¥1.2bn FX loss (Q3 2024). Feedstock costs +18% (2024) and wage inflation (chem sector 4–6%) squeezed margins; H2 2025 lending spreads ~0.9% enabled ~¥120–150bn M&A.

| Metric | Value |

|---|---|

| Semiconductor market 2025 | $700bn (+12%) |

| JPY move 2024 | -8% |

| Naphtha cost impact | ¥6–8bn |

| Feedstock change 2024 | +18% |

| Wage growth 2024 | 4–6% |

| H2 2025 lending spread | ~0.9% |

| 2025 M&A | ¥120–150bn |

Same Document Delivered

Resonac PESTLE Analysis

The preview shown here is the exact Resonac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. What you see in the screenshot is the real product and will be available for immediate download upon payment. This file includes the complete PESTLE analysis content and layout as displayed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic clarity with our Resonac PESTLE Analysis—concise, expert-backed insight into political, economic, social, technological, legal, and environmental forces shaping the company’s future; ideal for investors, consultants, and planners. Purchase the full report to access deep-dive findings, actionable recommendations, and ready-to-use Word/Excel files that save research time and power smarter decisions—download instantly.

Political factors

Geopolitical Semiconductor Alliances

The Japan–US semiconductor partnership in late 2025 strengthens supply-chain security for critical materials; bilateral deals have supported a 12% increase in Japan-US high-end materials trade to $8.9bn in 2024, benefiting Resonac which supplies photoresists and polishing slurries.

Export Control Regulations

Strict export controls on advanced technology to China, Russia and certain Southeast Asian nations pressure Japanese chemical firms; in 2024 Japan issued over 1,200 individual export licenses for electronics-related chemicals, tightening approvals for products classified under HS codes used by Resonac.

Resonac must navigate complex licensing and end-use checks to protect ~$1.8bn in FY2024 electronics-related revenue, balancing compliance costs that rose an estimated 6–9% with efforts to retain global market share.

These rules require a robust internal monitoring framework—including automated screening and audit trails—to reduce trade-flow disruptions and limit political friction that could impact up to 15% of export volumes to controlled regions.

Domestic Industrial Subsidies

Japan committed about JPY 1.4 trillion (≈USD 10.0bn) through 2025 to bolster domestic semiconductor supply chains; Resonac has tapped these industrial subsidies to underwrite roughly JPY 30–50 billion in capex for next‑generation packaging materials and SiC power semiconductor projects, cutting R&D financing needs and lowering project-level risk, effectively de-risking capital-intensive development and accelerating commercialization timelines.

Energy Policy and Security

Japan's 2030 energy plan targets 20-22% renewables and 20-22% nuclear; renewed reactor restarts cut wholesale power costs, directly lowering Resonac's energy expenses for its 2024 petrochemical output valued at ~¥250bn.

Carbon pricing proposals (est. ¥5,000–¥10,000/ton CO2) and subsidies for green hydrogen affect feedstock competitiveness, raising potential operating costs for energy-intensive units if implemented.

Aligning with national energy security—stockpiling LNG and promoting domestic power—supports stable supply chains critical to Resonac's long-term manufacturing continuity.

- 2030 targets: 20-22% renewables, 20-22% nuclear

- Wholesale power down with reactor restarts → lower OPEX for petrochemicals

- Carbon price range ¥5,000–¥10,000/ton impacts margins

- Energy security measures (LNG, domestic generation) reduce supply risk

Regional Stability in Southeast Asia

Resonac’s manufacturing footprint in Southeast Asia—accounting for about 28% of its 2024 consolidated production capacity—faces risks from political shifts in Indonesia, Thailand and Vietnam; localized unrest could disrupt supply chains and spike logistic costs by an estimated 4–7%.

To mitigate this, Resonac keeps diversified sites across multiple countries and invested ¥32.4bn (approx $225m) in 2024 capacity resilience and logistics redundancy.

Ongoing government engagement secures permits and infrastructure support, with recent MOUs in 2024 reducing tariff exposure and expediting utilities for two major plants.

- 28% of capacity in SEA

- Potential 4–7% logistic cost shock from local disruptions

- ¥32.4bn invested in resilience (2024)

- 2024 MOUs to lower tariff and utility delays

Geopolitics Hit Resonac: $1.8bn Revenue Risk, ¥32.4bn Resilience Spend, 28% SEA

Political drivers—US-Japan semiconductor deals, tight export controls, energy policy and SEA geopolitical risk—directly affect Resonac’s supply chains, compliance costs, capex funding and energy/OPEX; 2024 figures: ~$1.8bn electronics revenue exposure, JPY30–50bn capex subsidies, ¥32.4bn resilience spend, 28% capacity in SEA, carbon price ¥5,000–¥10,000/ton.

| Metric | 2024/2025 |

|---|---|

| Electronics revenue at risk | $1.8bn |

| Capex subsidies used | JPY30–50bn |

| Resilience spend | ¥32.4bn |

| SEA capacity | 28% |

| Carbon price range | ¥5,000–¥10,000/ton |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Resonac, with data-backed trends and region-specific examples to surface risks and opportunities for executives, investors, and strategists.

Condenses Resonac's PESTLE into a clean, shareable summary that highlights key external risks and opportunities by category, enabling quick alignment in meetings, slide decks, or client reports.

Economic factors

Global Semiconductor Market Recovery

By end-2025 the global semiconductor market returned to robust growth with industry revenues forecast at about $700 billion for 2025, up ~12% year-on-year, fueling demand for Resonac’s high-purity ceramic and dielectric materials used in HPC and AI chips.

Currency Exchange Rate Volatility

The JPY/USD swung ~8% in 2024, and a weaker yen boosted Resonac’s export competitiveness but raised naphtha import costs by an estimated ¥6–8 billion in FY2024, pressuring gross margins. Resonac reported FX losses of ¥1.2 billion in Q3 2024; implementing layered hedging (forwards, options) and natural hedges is vital to stabilize EBITDA and protect margins against further volatility.

Raw Material and Energy Costs

Global commodity price volatility pushed naphtha and ethylene feedstock costs up ~18% YoY in 2024, lifting basic chemical input costs and squeezing Resonac’s margins.

With petrochemical product price realizations lagging, Resonac struggles to fully pass through higher costs without volume loss in competitive domestic and Asian markets.

Oil/gas market shifts—LNG spot prices fell ~12% in 2025 H1 while crude remained volatile—drive Resonac to invest in resource-efficient processes to cut feedstock intensity and lower unit costs.

Inflationary Trends and Wage Growth

Persistent inflation—2024 CPI averaged 3.5% in the US and 4.0% in the EU—has pushed nominal wages up, increasing Resonac’s labor and operational costs across global plants.

Resonac must balance competitive pay to retain specialized staff while enforcing strict cost controls to protect margins; 2024 sector wage growth ranged 4–6% in chemical manufacturing.

To offset rising wages, the firm needs accelerated automation and productivity gains; capital expenditure on automation rose ~8% industrywide in 2024.

- 2024 CPI: US 3.5%, EU 4.0%

- Chemical sector wage growth: 4–6% (2024)

- Industry automation capex +8% (2024)

Interest Rate Environments

Monetary policy shifts by the Bank of Japan and global central banks directly affect Resonac’s borrowing costs for infrastructure and expansion; JPY corporate lending spreads fell to about 0.9% in H2 2025 from 1.4% in 2024, easing financing pressure.

With headline interest rates stabilizing in late 2025—BOJ moving toward normalization and global 10-year yields retreating to ~3.5%—Resonac gains more favorable conditions for long-term project financing and capex.

This lower-rate backdrop underpins an aggressive M&A push: Resonac completed or announced deals totaling roughly JPY 120–150 billion in 2025, leveraging cheaper debt to expand its chemical and materials portfolio.

- H2 2025 corporate lending spreads ≈ 0.9% (vs 1.4% in 2024)

- Global 10-year yields ≈ 3.5% in late 2025

- Resonac M&A activity ~JPY 120–150bn in 2025

Resonac rides $700B chip boom as costs, FX and wages squeeze margins; ¥120–150bn M&A

Global semiconductor demand (2025 est. ~$700bn, +12% YoY) boosts Resonac product demand; weaker JPY (~-8% in 2024) improved exports but added ~¥6–8bn naphtha cost and ¥1.2bn FX loss (Q3 2024). Feedstock costs +18% (2024) and wage inflation (chem sector 4–6%) squeezed margins; H2 2025 lending spreads ~0.9% enabled ~¥120–150bn M&A.

| Metric | Value |

|---|---|

| Semiconductor market 2025 | $700bn (+12%) |

| JPY move 2024 | -8% |

| Naphtha cost impact | ¥6–8bn |

| Feedstock change 2024 | +18% |

| Wage growth 2024 | 4–6% |

| H2 2025 lending spread | ~0.9% |

| 2025 M&A | ¥120–150bn |

Same Document Delivered

Resonac PESTLE Analysis

The preview shown here is the exact Resonac PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers. What you see in the screenshot is the real product and will be available for immediate download upon payment. This file includes the complete PESTLE analysis content and layout as displayed.