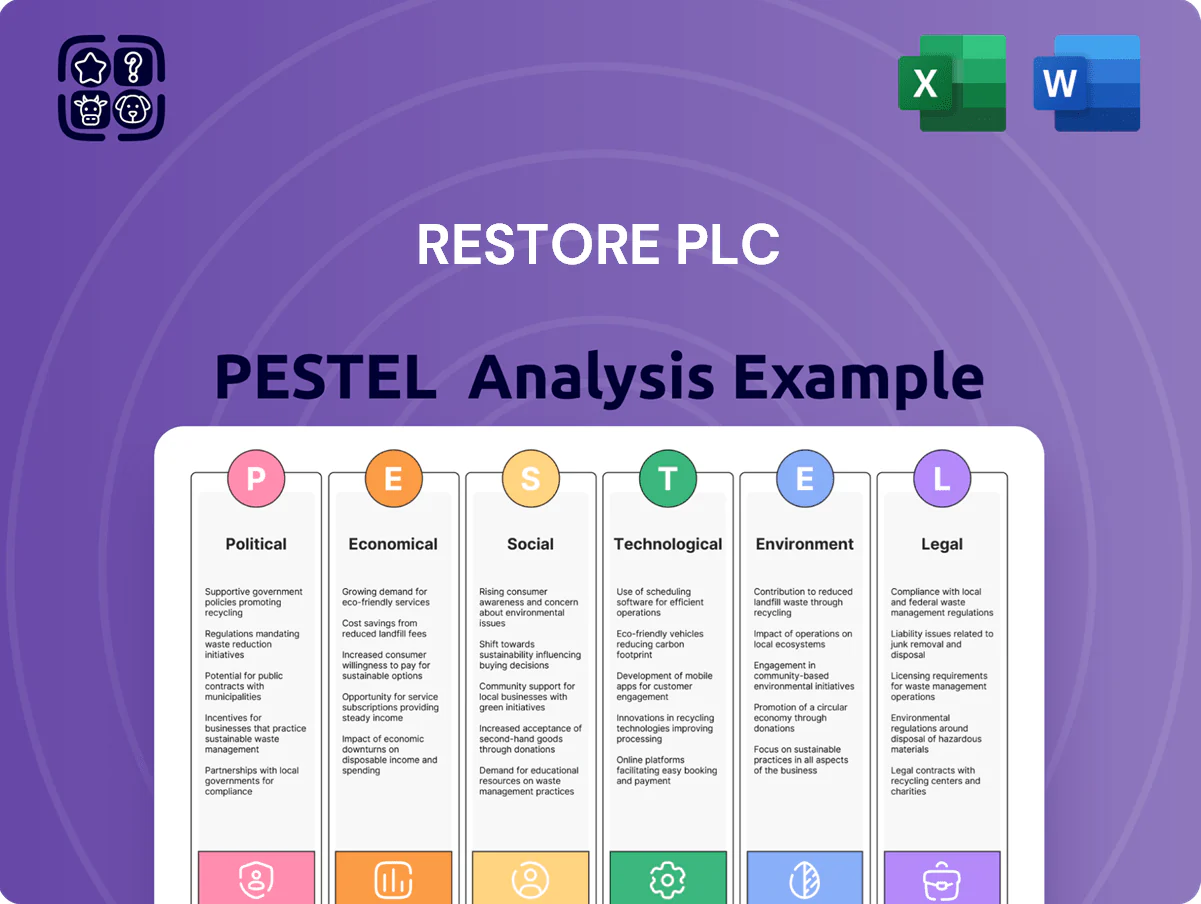

Restore plc PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis of Restore plc—concise, evidence-based insights on political, economic, social, technological, legal, and environmental forces shaping the business; buy the full report for a complete, actionable breakdown to inform investment, strategy, or due diligence.

Political factors

UK Public Sector Outsourcing Trends

The UK government remains a core client for Restore, especially in document management and secure disposal, accounting for an estimated 18–22% of public-sector revenues in 2024–25; ongoing fiscal pressures have driven a 12% rise in outsourcing of admin functions across central/local government in 2024, and forecasts into late 2025 show continued demand—positioning Restore to capture further contracts as departments seek private-sector efficiency gains.

Post-Brexit Regulatory Alignment

Ongoing UK-specific regulatory changes post-Brexit affect handling of data and physical assets, with the UK Data Protection Act 2018 supplemented by UK GDPR adjustments; Restore reported FY2024 revenue £675m, so compliance shifts materially affect service demand and costs.

Government Digital Transformation Initiatives

The UK Government’s Digital First agenda aims to migrate 80% of services online and cut paper storage by an estimated 30% by 2025, directly boosting Restore plc’s Digital & Technology revenues as public sector agencies move records to secure cloud environments; Restore reported a 12% year-on-year rise in digitisation services in FY2024, positioning it as a strategic partner providing large-scale scanning, indexing and secure data migration to meet national modernization targets.

National Security and Data Sovereignty

Heightened national security focus has driven UK data residency rules and demand for secure destruction; 82% of FTSE 350 firms now cite data sovereignty as a procurement criterion (2025 ICM survey).

Restore plc’s 220+ UK sites and 2024 revenue of £404m position it as a sovereign-servicing provider for firms avoiding cross-border data risks.

This localized infrastructure is a clear competitive edge amid rising geopolitical data-espionage concerns and tighter public-sector procurement standards.

- 220+ UK facilities

- £404m revenue (2024)

- 82% FTSE 350 prioritize data sovereignty (2025)

Local Government Funding Pressures

Budgetary constraints at local councils—UK local government grant cuts of about 35% since 2010 and a 2024 average council savings target near 8%—have driven asset consolidation and office-space reduction, creating near-term demand for Restore plc’s relocation and decommissioning services.

However, reduced physical estates and policies promoting digitisation threaten long-term volumes in paper storage; public-sector archive volumes fell an estimated 10–15% across 2022–24 in sampled councils.

Restore must shift toward cost-effective, technology-led offerings—digital conversion, managed cloud records and pay-per-use models—to retain municipal clients facing tightened budgets and preserve revenue per customer.

- Short-term tailwind: surge in decommissioning work from estate consolidation.

- Long-term risk: 10–15% decline in paper storage demand (2022–24 sample).

- Strategic response: scale digital conversion, cloud records and flexible pricing for cash-strapped councils.

Restore grows on UK public-sector demand: 12% digitisation, 18–22% revenues

UK government remains a key Restore client (18–22% public-sector revenues 2024–25) amid outsourcing up 12% in 2024; Digital First aims to cut paper storage 30% by 2025, driving Restore’s 12% FY2024 digitisation growth. Data residency and security heighten demand for UK-based services—220+ sites; 82% FTSE 350 cite data sovereignty (2025). Local council cuts (avg 8% savings target 2024) boost decommissioning but shrink paper volumes 10–15% (2022–24).

| Metric | Value |

|---|---|

| Public-sector revenue share | 18–22% (2024–25) |

| Digitisation growth | 12% YoY (FY2024) |

| Paper storage decline | 10–15% (2022–24 sample) |

| UK sites | 220+ |

| FTSE 350 data sovereignty | 82% (2025) |

| Local council savings target | ~8% (2024) |

What is included in the product

Explores how political, economic, social, technological, environmental and legal forces uniquely impact Restore plc, with each section grounded in current market and regulatory trends relevant to its UK-focused records management, document shredding and technology-enabled services.

A concise, visually segmented Restore plc PESTLE summary that simplifies external risk and market positioning for quick inclusion in presentations or strategy sessions, easily shared across teams and editable for local context or business lines.

Economic factors

Interest Rate Environment and Debt Servicing

Following 2024–2025 volatility, Bank of England base rate stabilization at 5.25% by Dec 2025 brought predictability to Restore plc’s capital allocation; with net debt of £376m and net debt/EBITDA ~2.1x (FY2024), borrowing cost materially affects acquisition returns. Restore’s acquisitive model makes maintaining debt/ equity and interest coverage ratios key—investors watch that net interest expense (c.£18m FY2024) does not compress service-line margins.

Corporate Office Footprint Consolidation

Economic pressures have driven UK firms to shrink office space by about 19% between 2019–2024 in central London and c.10% nationally, boosting Restore plc short-term revenue from workplace relocations and IT asset disposal as vacated sites are cleared.

These one-off conversion and disposal services contributed materially in FY2024 where Restore reported a 6% group revenue uplift in commercial services tied to relocations and asset recovery.

However, the long-term shift to smaller, hybrid offices risks reducing recurring onsite shredding and storage fees—services that comprised roughly 35% of Restore’s recurring revenue mix in 2023–24.

Inflationary Pressures on Labour Costs

As a labour-intensive service group, Restore faced rising wage inflation in 2025, with UK average regular pay growth hitting about 5.1% year‑on‑year in Q3 2025 and National Living Wage increases to £11.44 (Apr 2025); this forced tight cost controls and targeted pricing moves to protect margins. Restore’s ability to offset higher pay via index-linked contracts—reported on 60–70% of its facilities management and records management book—remains a key economic hedge.

Business Investment and Confidence Levels

The health of the UK economy directly affects business discretionary spend on digital transformation; GDP growth slowing to 0.5% in 2024 and business investment falling 1.2% y/y in Q3 2024 reduced appetite for large projects, curbing demand for Restore’s Digital division.

During uncertainty firms delay digitisation, but a return to 1.2% GDP growth forecast for 2025 and corporate IT spend rising 4% y/y would boost demand for Restore’s recycling and data-management solutions.

- UK business investment -1.2% y/y (Q3 2024)

- UK GDP 0.5% (2024); forecast 1.2% (2025)

- Corporate IT spend +4% y/y potential drives Restore Digital uptake

Currency Volatility and Equipment Costs

Fluctuations in the Pound Sterling directly affect Restore plc’s import costs for specialized hardware; a 10% GBP depreciation vs USD/EUR in 2023–24 raised estimated capex for similar firms by c.7–9%, risking higher unit costs for processing centers.

Restore sources IT recycling components and scanning hardware internationally, so unmanaged FX exposure can create quarterly capex spikes and compress 2024 adjusted EBIT margins, given industry tech spend of ~£15–25m annually.

- 10% GBP move ≈ 7–9% capex impact

- International supply chain for IT hardware

- Estimated industry tech spend £15–25m p.a.

- Currency risk can compress adjusted EBIT margins

Restore: Stable BoE, manageable debt (£376m) but revenue & cost pressures ahead

Stable BoE rate at 5.25% (Dec 2025) keeps borrowing predictable; Restore net debt £376m, net debt/EBITDA ~2.1x (FY2024), net interest ≈£18m. Office downsizing (central London −19% 2019–24; UK −10%) drove FY2024 commercial services +6%, but recurring revenue (shredding/storage ~35%) faces pressure. Wage inflation ~5.1% (Q3 2025) and NLW £11.44 raise costs; GBP 10% fall → capex +7–9%.

| Metric | Value |

|---|---|

| Net debt | £376m |

| Net debt/EBITDA | ~2.1x |

| Net interest | £18m |

| Office shrink (UK) | −10% |

| Wage growth (Q3 2025) | 5.1% |

Preview the Actual Deliverable

Restore plc PESTLE Analysis

The preview shown here is the exact Restore plc PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version, professionally structured with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after payment. Don’t just imagine it—this is the real, finished document you’ll own upon checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis of Restore plc—concise, evidence-based insights on political, economic, social, technological, legal, and environmental forces shaping the business; buy the full report for a complete, actionable breakdown to inform investment, strategy, or due diligence.

Political factors

UK Public Sector Outsourcing Trends

The UK government remains a core client for Restore, especially in document management and secure disposal, accounting for an estimated 18–22% of public-sector revenues in 2024–25; ongoing fiscal pressures have driven a 12% rise in outsourcing of admin functions across central/local government in 2024, and forecasts into late 2025 show continued demand—positioning Restore to capture further contracts as departments seek private-sector efficiency gains.

Post-Brexit Regulatory Alignment

Ongoing UK-specific regulatory changes post-Brexit affect handling of data and physical assets, with the UK Data Protection Act 2018 supplemented by UK GDPR adjustments; Restore reported FY2024 revenue £675m, so compliance shifts materially affect service demand and costs.

Government Digital Transformation Initiatives

The UK Government’s Digital First agenda aims to migrate 80% of services online and cut paper storage by an estimated 30% by 2025, directly boosting Restore plc’s Digital & Technology revenues as public sector agencies move records to secure cloud environments; Restore reported a 12% year-on-year rise in digitisation services in FY2024, positioning it as a strategic partner providing large-scale scanning, indexing and secure data migration to meet national modernization targets.

National Security and Data Sovereignty

Heightened national security focus has driven UK data residency rules and demand for secure destruction; 82% of FTSE 350 firms now cite data sovereignty as a procurement criterion (2025 ICM survey).

Restore plc’s 220+ UK sites and 2024 revenue of £404m position it as a sovereign-servicing provider for firms avoiding cross-border data risks.

This localized infrastructure is a clear competitive edge amid rising geopolitical data-espionage concerns and tighter public-sector procurement standards.

- 220+ UK facilities

- £404m revenue (2024)

- 82% FTSE 350 prioritize data sovereignty (2025)

Local Government Funding Pressures

Budgetary constraints at local councils—UK local government grant cuts of about 35% since 2010 and a 2024 average council savings target near 8%—have driven asset consolidation and office-space reduction, creating near-term demand for Restore plc’s relocation and decommissioning services.

However, reduced physical estates and policies promoting digitisation threaten long-term volumes in paper storage; public-sector archive volumes fell an estimated 10–15% across 2022–24 in sampled councils.

Restore must shift toward cost-effective, technology-led offerings—digital conversion, managed cloud records and pay-per-use models—to retain municipal clients facing tightened budgets and preserve revenue per customer.

- Short-term tailwind: surge in decommissioning work from estate consolidation.

- Long-term risk: 10–15% decline in paper storage demand (2022–24 sample).

- Strategic response: scale digital conversion, cloud records and flexible pricing for cash-strapped councils.

Restore grows on UK public-sector demand: 12% digitisation, 18–22% revenues

UK government remains a key Restore client (18–22% public-sector revenues 2024–25) amid outsourcing up 12% in 2024; Digital First aims to cut paper storage 30% by 2025, driving Restore’s 12% FY2024 digitisation growth. Data residency and security heighten demand for UK-based services—220+ sites; 82% FTSE 350 cite data sovereignty (2025). Local council cuts (avg 8% savings target 2024) boost decommissioning but shrink paper volumes 10–15% (2022–24).

| Metric | Value |

|---|---|

| Public-sector revenue share | 18–22% (2024–25) |

| Digitisation growth | 12% YoY (FY2024) |

| Paper storage decline | 10–15% (2022–24 sample) |

| UK sites | 220+ |

| FTSE 350 data sovereignty | 82% (2025) |

| Local council savings target | ~8% (2024) |

What is included in the product

Explores how political, economic, social, technological, environmental and legal forces uniquely impact Restore plc, with each section grounded in current market and regulatory trends relevant to its UK-focused records management, document shredding and technology-enabled services.

A concise, visually segmented Restore plc PESTLE summary that simplifies external risk and market positioning for quick inclusion in presentations or strategy sessions, easily shared across teams and editable for local context or business lines.

Economic factors

Interest Rate Environment and Debt Servicing

Following 2024–2025 volatility, Bank of England base rate stabilization at 5.25% by Dec 2025 brought predictability to Restore plc’s capital allocation; with net debt of £376m and net debt/EBITDA ~2.1x (FY2024), borrowing cost materially affects acquisition returns. Restore’s acquisitive model makes maintaining debt/ equity and interest coverage ratios key—investors watch that net interest expense (c.£18m FY2024) does not compress service-line margins.

Corporate Office Footprint Consolidation

Economic pressures have driven UK firms to shrink office space by about 19% between 2019–2024 in central London and c.10% nationally, boosting Restore plc short-term revenue from workplace relocations and IT asset disposal as vacated sites are cleared.

These one-off conversion and disposal services contributed materially in FY2024 where Restore reported a 6% group revenue uplift in commercial services tied to relocations and asset recovery.

However, the long-term shift to smaller, hybrid offices risks reducing recurring onsite shredding and storage fees—services that comprised roughly 35% of Restore’s recurring revenue mix in 2023–24.

Inflationary Pressures on Labour Costs

As a labour-intensive service group, Restore faced rising wage inflation in 2025, with UK average regular pay growth hitting about 5.1% year‑on‑year in Q3 2025 and National Living Wage increases to £11.44 (Apr 2025); this forced tight cost controls and targeted pricing moves to protect margins. Restore’s ability to offset higher pay via index-linked contracts—reported on 60–70% of its facilities management and records management book—remains a key economic hedge.

Business Investment and Confidence Levels

The health of the UK economy directly affects business discretionary spend on digital transformation; GDP growth slowing to 0.5% in 2024 and business investment falling 1.2% y/y in Q3 2024 reduced appetite for large projects, curbing demand for Restore’s Digital division.

During uncertainty firms delay digitisation, but a return to 1.2% GDP growth forecast for 2025 and corporate IT spend rising 4% y/y would boost demand for Restore’s recycling and data-management solutions.

- UK business investment -1.2% y/y (Q3 2024)

- UK GDP 0.5% (2024); forecast 1.2% (2025)

- Corporate IT spend +4% y/y potential drives Restore Digital uptake

Currency Volatility and Equipment Costs

Fluctuations in the Pound Sterling directly affect Restore plc’s import costs for specialized hardware; a 10% GBP depreciation vs USD/EUR in 2023–24 raised estimated capex for similar firms by c.7–9%, risking higher unit costs for processing centers.

Restore sources IT recycling components and scanning hardware internationally, so unmanaged FX exposure can create quarterly capex spikes and compress 2024 adjusted EBIT margins, given industry tech spend of ~£15–25m annually.

- 10% GBP move ≈ 7–9% capex impact

- International supply chain for IT hardware

- Estimated industry tech spend £15–25m p.a.

- Currency risk can compress adjusted EBIT margins

Restore: Stable BoE, manageable debt (£376m) but revenue & cost pressures ahead

Stable BoE rate at 5.25% (Dec 2025) keeps borrowing predictable; Restore net debt £376m, net debt/EBITDA ~2.1x (FY2024), net interest ≈£18m. Office downsizing (central London −19% 2019–24; UK −10%) drove FY2024 commercial services +6%, but recurring revenue (shredding/storage ~35%) faces pressure. Wage inflation ~5.1% (Q3 2025) and NLW £11.44 raise costs; GBP 10% fall → capex +7–9%.

| Metric | Value |

|---|---|

| Net debt | £376m |

| Net debt/EBITDA | ~2.1x |

| Net interest | £18m |

| Office shrink (UK) | −10% |

| Wage growth (Q3 2025) | 5.1% |

Preview the Actual Deliverable

Restore plc PESTLE Analysis

The preview shown here is the exact Restore plc PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This file is the final version, professionally structured with no placeholders or teasers. The layout, content, and structure visible here are exactly what you’ll download immediately after payment. Don’t just imagine it—this is the real, finished document you’ll own upon checkout.