Retif Group PESTLE Analysis

Skip the Research. Get the Strategy.

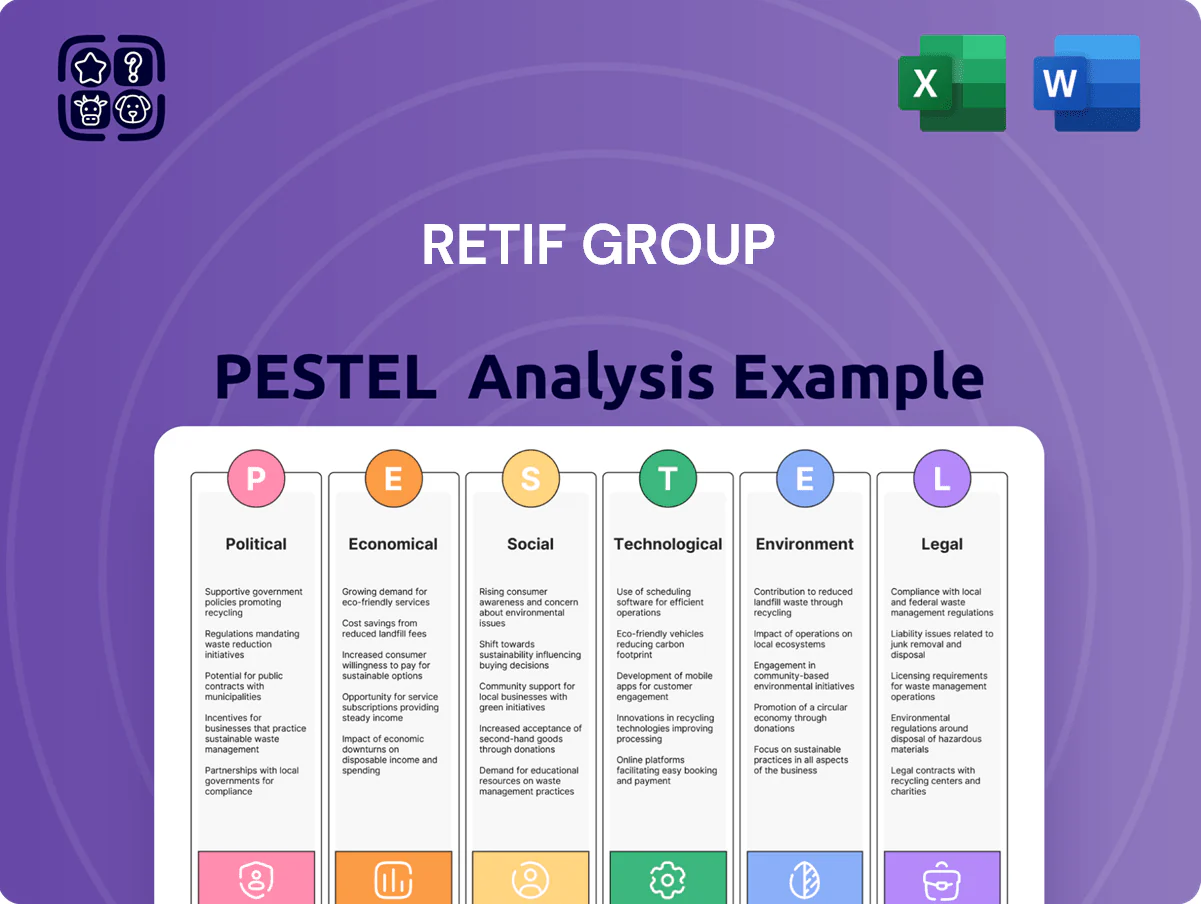

Gain a competitive edge with our PESTLE Analysis of Retif Group—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and risks; buy the full report to access actionable, ready-to-use insights and downloadable templates for immediate decision-making.

Political factors

EU Trade Policy Stability

Retif's cross-border operations depend on stable EU trade rules to keep inventory flowing; in 2024 intra-EU trade accounted for about 66% of EU goods trade, highlighting exposure to customs shifts. Protectionist policies could raise tariffs on imported MDF, metals and plastics—inputs representing roughly 40–55% of shopfitting material costs—compressing margins. Navigating post-Brexit UK divergence adds compliance costs; UK-EU goods trade fell 15% in 2021–23, signaling persistent frictions.

Government SME Support

Small and medium enterprises account for an estimated 70% of Retif Group’s customer base, so national fiscal measures that target SMEs materially affect demand for retail fixtures and equipment. In 2024 EU SME recovery funds disbursed roughly €45bn toward digital and physical retail upgrades, boosting purchasing power for premium store equipment. A 2025 cut in subsidies or a 3–5 percentage-point rise in corporate taxes could reduce SME capex by an estimated 10–15%, weakening Retif’s sales. Continued government grants for store modernization therefore remain a key revenue driver.

Geopolitical Supply Chain Risk

Regional conflicts and China-Taiwan tensions risk disrupting supplies of metal, wood and plastic components—Asia accounts for roughly 60% of global furniture and equipment manufacturing—raising component shortages for Retif. Political instability drives freight rate volatility; container rates spiked over 300% in 2021 and remain ~40% above pre-COVID levels in 2024, extending lead times for specialized shop equipment. Retif must diversify sourcing and increase UK/EU inventory buffers to mitigate corridor risks.

Labor Market Regulations

Political moves raising minimum wages in France (SMIC rose 1.9% to €1,353/month in 2025) and Spain (minimum wage up 8% to €1,260/month in 2024) increase Retif’s cost base and clients’ payroll expenses, squeezing retailer margins.

Employment law changes—higher social charges and stricter contracts—raise operating costs for Retif and its customers; French employer social contributions averaged ~45% of gross pay in 2024.

Stricter labor rules accelerate retailer demand for automation: uptake in POS and self-checkout equipment grew ~12% YoY in EU retail tech spend 2024, benefiting Retif’s sales.

- Higher minimum wages (France €1,353; Spain €1,260) → increased payroll costs

- Employer social charges ~45% in France raise overheads

- EU retail automation spend +12% YoY 2024 → opportunity for Retif

- Employment law tightening shifts demand toward automation solutions

Urban Planning Policies

Local government pedestrianization and revitalization projects reshape footfall: EU cities saw a 12% average increase in city-center pedestrian counts in 2023, benefiting Retif clients supplying shop fittings and display equipment.

Policies favoring local commerce—e.g., France's 2024 anti-big-box measures—boost demand for boutique-style fittings, with small retail spending up 6% YoY in 2024.

Conversely, strict zoning and limits on retail floor area can constrain new store openings, pressuring equipment sales; in 2023 building permits for retail fell 8% in key markets.

- +12% city-center pedestrian growth (2023 average)

- +6% small retail spending YoY (2024)

- -8% retail building permits (2023)

Political risks, rising costs, and automation reshape Retif’s EU trade and margins

Political risks (trade/tariffs, labor rules, subsidies, local policies) materially affect Retif: 66% intra-EU trade exposure (2024), inputs 40–55% cost share, UK-EU trade -15% (2021–23), EU SME recovery €45bn (2024), container rates ~40% above pre-COVID (2024), SMIC €1,353 (2025), Spain MW €1,260 (2024), EU retail automation +12% YoY (2024).

| Metric | Value |

|---|---|

| Intra-EU trade share | 66% (2024) |

| Inputs cost share | 40–55% |

| UK-EU trade change | -15% (2021–23) |

| EU SME fund | €45bn (2024) |

| Container rates | ~+40% vs pre-COVID (2024) |

| France minimum wage | €1,353 (2025) |

| Spain minimum wage | €1,260 (2024) |

| EU retail automation growth | +12% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Retif Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific examples and forward-looking insights to support strategic planning, investor confidence, and actionable risk-opportunity identification.

Condenses Retif Group's PESTLE into a clear, shareable snapshot that teams can drop into presentations or planning sessions for quick alignment on external risks and strategic positioning.

Economic factors

Inflation and Purchasing Power

Persisting inflation across Europe—EU HICP rose 3.7% y/y in 2025 Q4—squeezes retailers’ purchasing power, raising Retif Group’s cost of goods sold and compressing margins. Steel and glass input costs climbed ~12–15% in 2024–25, inflating fixture prices and forcing clients to postpone renovations or choose lower-cost display solutions. Reduced discretionary spending by independent retailers may cut project volumes for Retif.

Interest Rate Fluctuations

The cost of borrowing directly affects retailers financing new Retif store rollouts or major refits; eurozone policy rates rose from 0% in 2021 to 3.75% by Dec 2024, squeezing capex for many operators. Higher rates have slowed retail real estate activity—European retail transactions fell about 18% in 2023—reducing demand for fit-out and equipment contracts. Retif’s flexible vendor financing and extended customer credit terms become a competitive advantage when central banks keep monetary policy tight.

Consumer Spending Patterns

Economic cycles strongly influence Retif Group, with retail sales in the EU rising 2.3% in 2024 boosting demand for POS and retail fixtures that drive Retif’s revenue.

Shifts toward discount chains or luxury brands force Retif to reallocate inventory—discount-focused packaging volumes grew 6% in 2024 while premium fixture spend rose 4% among luxury retailers.

During downturns consumers prioritize essentials; in 2023–2024 demand for cost-effective packaging and basic POS systems increased as retailers cut aesthetic upgrade budgets by an estimated 8%.

Energy Costs and Logistics

Fluctuating energy prices raised European industrial electricity costs by about 12% in 2024 versus 2022, increasing manufacturing costs for Retif's store equipment and squeezing margins.

Fuel surcharges lifted road freight rates ~18% in 2023–24, raising shipping costs for bulky shelving and counters across Europe and pressuring client pricing.

Retif must optimize logistics, adopt energy-efficient warehousing (LED, HVAC, solar) and route consolidation to preserve its competitive pricing.

- Industrial electricity +12% (2022–24)

- Road freight +18% (2023–24)

- Focus: route consolidation, energy-efficient warehouses, fuel-surcharge management

Currency Exchange Volatility

For Retif Group operations outside the Eurozone, notably the UK, GBP/EUR volatility (GBP fell ~6% vs EUR in 2024) can squeeze margins and force price adjustments, reducing competitiveness.

Euro weakness vs USD (EUR down ~4% in 2024) raises import costs for manufacturing partners sourcing components priced in stronger currencies.

Strategic hedging and localized sourcing—hedge coverage of 60–80% and nearshoring—are critical to stabilise financials.

- GBP/EUR -6% (2024)

- EUR/USD -4% (2024)

- Recommended hedge coverage 60–80%

- Priority: localized sourcing/nearshoring

Rising costs, weaker EUR: margins squeezed—hedge 60–80% and nearshore to protect profits

Inflation (EU HICP +3.7% y/y 2025Q4) and input cost rises (steel/glass +12–15% 2024–25) compress margins; eurozone rates 3.75% (Dec 2024) curb capex and retail transactions (-18% 2023). Energy +12% (2022–24) and road freight +18% (2023–24) raise operating costs; FX: GBP/EUR -6% (2024), EUR/USD -4% (2024); hedge coverage 60–80% and nearshoring recommended.

| Metric | Change |

|---|---|

| EU HICP 2025Q4 | +3.7% y/y |

| Steel/Glass 2024–25 | +12–15% |

| Policy rate (Dec 2024) | 3.75% |

| Energy (2022–24) | +12% |

| Road freight (2023–24) | +18% |

| GBP/EUR (2024) | -6% |

| EUR/USD (2024) | -4% |

| Hedge recommendation | 60–80% |

Preview Before You Purchase

Retif Group PESTLE Analysis

The preview shown here is the exact Retif Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a competitive edge with our PESTLE Analysis of Retif Group—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and risks; buy the full report to access actionable, ready-to-use insights and downloadable templates for immediate decision-making.

Political factors

EU Trade Policy Stability

Retif's cross-border operations depend on stable EU trade rules to keep inventory flowing; in 2024 intra-EU trade accounted for about 66% of EU goods trade, highlighting exposure to customs shifts. Protectionist policies could raise tariffs on imported MDF, metals and plastics—inputs representing roughly 40–55% of shopfitting material costs—compressing margins. Navigating post-Brexit UK divergence adds compliance costs; UK-EU goods trade fell 15% in 2021–23, signaling persistent frictions.

Government SME Support

Small and medium enterprises account for an estimated 70% of Retif Group’s customer base, so national fiscal measures that target SMEs materially affect demand for retail fixtures and equipment. In 2024 EU SME recovery funds disbursed roughly €45bn toward digital and physical retail upgrades, boosting purchasing power for premium store equipment. A 2025 cut in subsidies or a 3–5 percentage-point rise in corporate taxes could reduce SME capex by an estimated 10–15%, weakening Retif’s sales. Continued government grants for store modernization therefore remain a key revenue driver.

Geopolitical Supply Chain Risk

Regional conflicts and China-Taiwan tensions risk disrupting supplies of metal, wood and plastic components—Asia accounts for roughly 60% of global furniture and equipment manufacturing—raising component shortages for Retif. Political instability drives freight rate volatility; container rates spiked over 300% in 2021 and remain ~40% above pre-COVID levels in 2024, extending lead times for specialized shop equipment. Retif must diversify sourcing and increase UK/EU inventory buffers to mitigate corridor risks.

Labor Market Regulations

Political moves raising minimum wages in France (SMIC rose 1.9% to €1,353/month in 2025) and Spain (minimum wage up 8% to €1,260/month in 2024) increase Retif’s cost base and clients’ payroll expenses, squeezing retailer margins.

Employment law changes—higher social charges and stricter contracts—raise operating costs for Retif and its customers; French employer social contributions averaged ~45% of gross pay in 2024.

Stricter labor rules accelerate retailer demand for automation: uptake in POS and self-checkout equipment grew ~12% YoY in EU retail tech spend 2024, benefiting Retif’s sales.

- Higher minimum wages (France €1,353; Spain €1,260) → increased payroll costs

- Employer social charges ~45% in France raise overheads

- EU retail automation spend +12% YoY 2024 → opportunity for Retif

- Employment law tightening shifts demand toward automation solutions

Urban Planning Policies

Local government pedestrianization and revitalization projects reshape footfall: EU cities saw a 12% average increase in city-center pedestrian counts in 2023, benefiting Retif clients supplying shop fittings and display equipment.

Policies favoring local commerce—e.g., France's 2024 anti-big-box measures—boost demand for boutique-style fittings, with small retail spending up 6% YoY in 2024.

Conversely, strict zoning and limits on retail floor area can constrain new store openings, pressuring equipment sales; in 2023 building permits for retail fell 8% in key markets.

- +12% city-center pedestrian growth (2023 average)

- +6% small retail spending YoY (2024)

- -8% retail building permits (2023)

Political risks, rising costs, and automation reshape Retif’s EU trade and margins

Political risks (trade/tariffs, labor rules, subsidies, local policies) materially affect Retif: 66% intra-EU trade exposure (2024), inputs 40–55% cost share, UK-EU trade -15% (2021–23), EU SME recovery €45bn (2024), container rates ~40% above pre-COVID (2024), SMIC €1,353 (2025), Spain MW €1,260 (2024), EU retail automation +12% YoY (2024).

| Metric | Value |

|---|---|

| Intra-EU trade share | 66% (2024) |

| Inputs cost share | 40–55% |

| UK-EU trade change | -15% (2021–23) |

| EU SME fund | €45bn (2024) |

| Container rates | ~+40% vs pre-COVID (2024) |

| France minimum wage | €1,353 (2025) |

| Spain minimum wage | €1,260 (2024) |

| EU retail automation growth | +12% YoY (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Retif Group across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven, region- and industry-specific examples and forward-looking insights to support strategic planning, investor confidence, and actionable risk-opportunity identification.

Condenses Retif Group's PESTLE into a clear, shareable snapshot that teams can drop into presentations or planning sessions for quick alignment on external risks and strategic positioning.

Economic factors

Inflation and Purchasing Power

Persisting inflation across Europe—EU HICP rose 3.7% y/y in 2025 Q4—squeezes retailers’ purchasing power, raising Retif Group’s cost of goods sold and compressing margins. Steel and glass input costs climbed ~12–15% in 2024–25, inflating fixture prices and forcing clients to postpone renovations or choose lower-cost display solutions. Reduced discretionary spending by independent retailers may cut project volumes for Retif.

Interest Rate Fluctuations

The cost of borrowing directly affects retailers financing new Retif store rollouts or major refits; eurozone policy rates rose from 0% in 2021 to 3.75% by Dec 2024, squeezing capex for many operators. Higher rates have slowed retail real estate activity—European retail transactions fell about 18% in 2023—reducing demand for fit-out and equipment contracts. Retif’s flexible vendor financing and extended customer credit terms become a competitive advantage when central banks keep monetary policy tight.

Consumer Spending Patterns

Economic cycles strongly influence Retif Group, with retail sales in the EU rising 2.3% in 2024 boosting demand for POS and retail fixtures that drive Retif’s revenue.

Shifts toward discount chains or luxury brands force Retif to reallocate inventory—discount-focused packaging volumes grew 6% in 2024 while premium fixture spend rose 4% among luxury retailers.

During downturns consumers prioritize essentials; in 2023–2024 demand for cost-effective packaging and basic POS systems increased as retailers cut aesthetic upgrade budgets by an estimated 8%.

Energy Costs and Logistics

Fluctuating energy prices raised European industrial electricity costs by about 12% in 2024 versus 2022, increasing manufacturing costs for Retif's store equipment and squeezing margins.

Fuel surcharges lifted road freight rates ~18% in 2023–24, raising shipping costs for bulky shelving and counters across Europe and pressuring client pricing.

Retif must optimize logistics, adopt energy-efficient warehousing (LED, HVAC, solar) and route consolidation to preserve its competitive pricing.

- Industrial electricity +12% (2022–24)

- Road freight +18% (2023–24)

- Focus: route consolidation, energy-efficient warehouses, fuel-surcharge management

Currency Exchange Volatility

For Retif Group operations outside the Eurozone, notably the UK, GBP/EUR volatility (GBP fell ~6% vs EUR in 2024) can squeeze margins and force price adjustments, reducing competitiveness.

Euro weakness vs USD (EUR down ~4% in 2024) raises import costs for manufacturing partners sourcing components priced in stronger currencies.

Strategic hedging and localized sourcing—hedge coverage of 60–80% and nearshoring—are critical to stabilise financials.

- GBP/EUR -6% (2024)

- EUR/USD -4% (2024)

- Recommended hedge coverage 60–80%

- Priority: localized sourcing/nearshoring

Rising costs, weaker EUR: margins squeezed—hedge 60–80% and nearshore to protect profits

Inflation (EU HICP +3.7% y/y 2025Q4) and input cost rises (steel/glass +12–15% 2024–25) compress margins; eurozone rates 3.75% (Dec 2024) curb capex and retail transactions (-18% 2023). Energy +12% (2022–24) and road freight +18% (2023–24) raise operating costs; FX: GBP/EUR -6% (2024), EUR/USD -4% (2024); hedge coverage 60–80% and nearshoring recommended.

| Metric | Change |

|---|---|

| EU HICP 2025Q4 | +3.7% y/y |

| Steel/Glass 2024–25 | +12–15% |

| Policy rate (Dec 2024) | 3.75% |

| Energy (2022–24) | +12% |

| Road freight (2023–24) | +18% |

| GBP/EUR (2024) | -6% |

| EUR/USD (2024) | -4% |

| Hedge recommendation | 60–80% |

Preview Before You Purchase

Retif Group PESTLE Analysis

The preview shown here is the exact Retif Group PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investment review.