Rich Products Corp. SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Rich Products Corp. combines a deep product portfolio and global supply chain with steady private ownership that fuels long-term R&D and customer relationships, yet faces rising commodity costs and intense private-label competition.

Its innovation in frozen foods and expanding foodservice reach are clear growth drivers, while regulatory shifts and changing consumer preferences present tangible risks to margins and market share.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

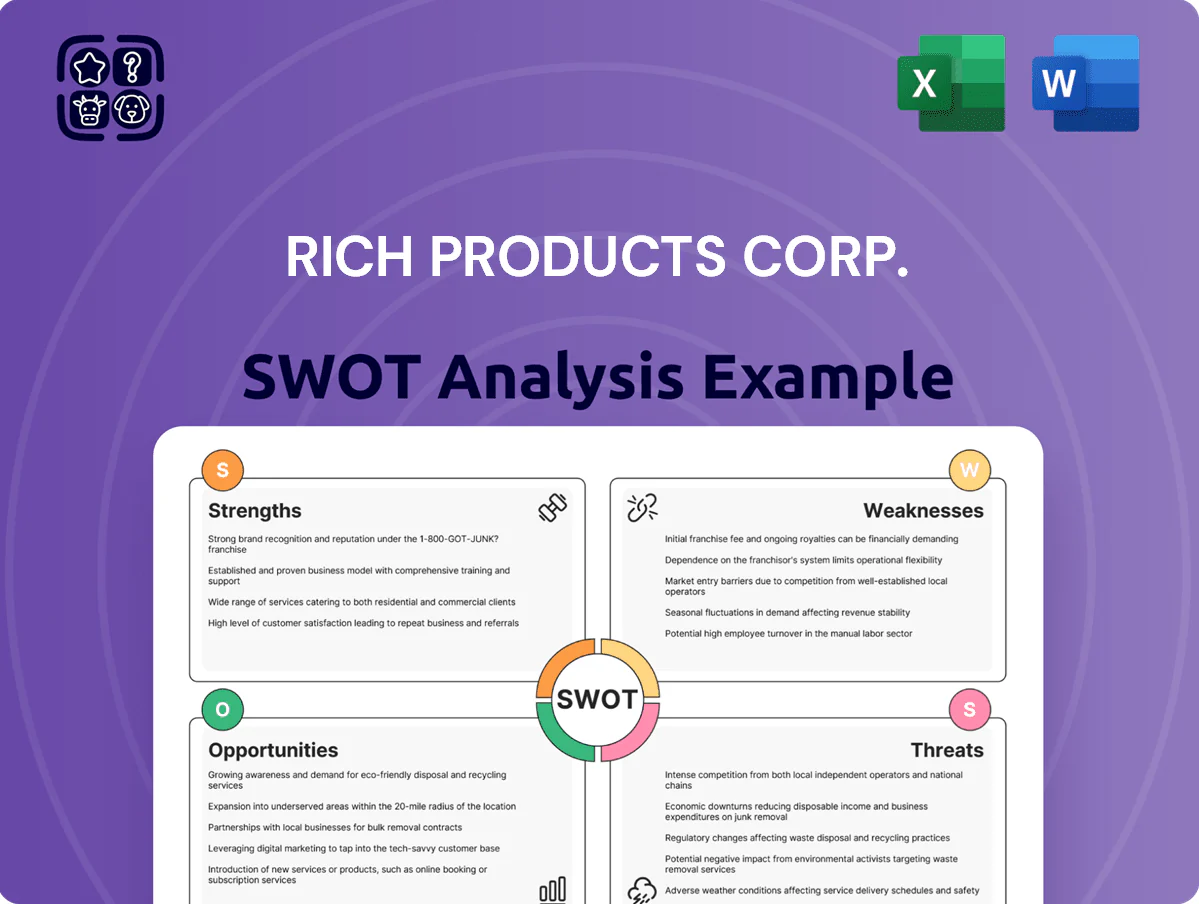

Strengths

Global Distribution Network

Rich Products operates in over 100 countries and sells to more than 120 markets, giving it a global footprint that balanced roughly $4.5 billion in annual revenue in 2024 across regions, which helps offset local downturns by diversifying income streams.

The company’s logistics network spans six continents with cold-chain facilities and 70+ manufacturing sites, ensuring frozen and refrigerated goods keep quality from plant to client and reducing spoilage-related losses.

Pioneering Innovation Heritage

Rich Products Corp. leverages a pioneering innovation heritage—leading non-dairy tech and plant-based alternatives since 1945—keeping a competitive edge through sustained R&D spending (estimated >1% of 2024 revenue, ~US$30–40M).

Consistent product launches, like heat-stable icings and versatile toppings, drove foodservice growth; new SKU rollouts increased North American volume sales by ~3–5% in 2023–24.

Diverse Product Portfolio

Richs offers bakery items, pizza dough, seafood, and appetizers, cutting dependence on any one category; in 2024 the private company reported ~$3.5B in revenue across its brands, showing scale.

Its products serve foodservice, retail bakeries, and industrial accounts concurrently, letting it sell into multiple channels and smooth demand swings.

That broad catalog helps capture more of customer spend—Richs estimates selling to >200,000 accounts and raising wallet share per account by 10–15% year-over-year.

Private Ownership Stability

Private family ownership lets Rich Products Corp. focus on long-term growth rather than quarterly earnings, enabling multi-year investments—the company spent an estimated $150–200M on plant upgrades worldwide in 2023–2024.

This patient capital supports infrastructure and automation projects that many public rivals defer, improving margins and resilience; private status also builds a stable corporate culture and supplier ties across 100+ countries.

- Long-term investment focus

- $150–200M estimated 2023–24 capex

- Improved margins via automation

- Stable supplier relationships in 100+ countries

Strategic B2B Partnerships

Rich Products Corp. is a preferred supplier to major global restaurant chains and large grocery retailers, locking in long-term contracts that delivered roughly $3.8 billion in 2024 revenue, giving predictable cash flow and ~6% annual revenue visibility from renewals.

By providing customized culinary solutions and on-site technical support, Richs embeds itself in clients’ operations, lowering churn and enabling margin advantages versus spot suppliers.

- Preferred supplier status with global chains

- ~$3.8B 2024 revenue supports steady cash flow

- Long-term contracts = predictable revenue

- Customized solutions + technical support = high client stickiness

Richs: $4.5B global food leader—$3.8B tied revenue, 70+ sites, steady cash flow

Richs has a global footprint (100+ countries, 120+ markets), diversified product mix (bakery, pizza, seafood, toppings) and ~70 plants/cold-chain sites, generating roughly $4.5B revenue in 2024 with ~ $150–200M capex in 2023–24; long-term private ownership and preferred-supplier contracts (~$3.8B tied revenue) drive stable cash flow and high client stickiness.

| Metric | 2024 |

|---|---|

| Revenue | $4.5B |

| Preferred-tied Rev | $3.8B |

| Capex (’23–’24) | $150–200M |

| Plants/sites | 70+ |

What is included in the product

Provides a concise SWOT overview of Rich Products Corp., highlighting its operational strengths, internal weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Provides a concise SWOT matrix for Rich Products Corp., delivering a quick strategic snapshot to align teams and expedite decision-making.

Weaknesses

Limited Retail Brand Recognition

While Rich Products Corp dominates B2B and foodservice, its consumer-brand recognition lags giants like Nestle and General Mills; NielsenIQ shows top 10 retail CPG brands capture ~25% of US shelf sales in 2024, a gap Richs can't match.

That weak retail pull-through means Richs relies on retail partners' marketing and shelf placement; 2024 IRI data indicates private-label and major brands drove 68% of frozen category growth, underscoring Richs' dependence.

High Operational Complexity

Managing diverse lines from frozen seafood to delicate bakery icings forces Rich Products Corp. to run multiple cold chains and clean-room lines, raising SG&A: 2024 annual operating expenses rose 6.2% to $1.12B, partly due to category-specific storage and safety protocols. This mix demands distinct supply-chain systems and staff training, increasing per-unit overhead and causing margin drag versus niche processors—gross margin slipped 120 basis points in 2024.

Capital Access Limitations

Being private limits Rich Products Corp.’s quick equity raises versus public peers; public listings raised $1.1T in U.S. IPOs in 2024, a liquidity pool Richs can’t tap fast.

This can hinder bidding on large acquisitions where public firms use stock as currency—median public deal for food industry megadeals was $1.2B in 2023.

Future expansion relies on debt and internal cash: Richs reported ~$1.4B revenue in FY2024, so high-capex growth may press debt capacity and cash flow.

Dependency on Foodservice Sector

- ~55% revenue tied to foodservice (2023)

- 2020 pandemic: steep sales decline from restaurant shutdowns

- Inflation 2022–23 slowed dine-out recovery

Cold Chain Logistics Costs

The reliance on frozen and refrigerated distribution makes Rich Products Corp. highly sensitive to energy-price swings—U.S. commercial electricity rose ~9% in 2022–2023 and fuel volatility can raise transport costs by 5–12% annually, squeezing margins.

Maintaining constant temps is capital- and emission-intensive: cold storage can use 3–4x more energy than ambient warehousing and HVAC retrofit capex runs into tens of millions for regional hubs.

Cold-chain failures cause large inventory loss—industry spoilage rates hit 3–8% for frozen foods—and can damage brand trust, prompting recalls that cost millions in logistics and legal exposure.

- Energy cost sensitivity: +5–12% transport impact

- Higher energy intensity: 3–4x ambient storage

- Capex: regional hub retrofits = tens of millions

- Spoilage risk: 3–8% industry loss; recalls cost millions

Fragile frozen CPG: weak retail pull, foodservice dependence, rising cold‑chain costs

Weak retail brand vs. giants; ~25% US shelf share by top10 CPG (NielsenIQ 2024) limits consumer pull-through and promo power.

Heavy foodservice exposure (~55% revenue 2023) and frozen mix make sales volatile—pandemic 2020 drop, slow recovery post‑2022–23 inflation.

Complex cold chains raise SG&A (opex +6.2% to $1.12B, 2024) and cut margins (gross margin −120 bps, 2024); capex and energy (+5–12% transport impact) pressure cash.

| Metric | Value |

|---|---|

| Top10 retail CPG shelf share (US, 2024) | ~25% |

| Foodservice revenue share (2023) | ~55% |

| Opex (2024) | $1.12B (+6.2%) |

| Gross margin change (2024) | −120 bps |

| Transport cost sensitivity | +5–12% |

| Spoilage industry rate | 3–8% |

Preview Before You Purchase

Rich Products Corp. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Rich Products Corp. combines a deep product portfolio and global supply chain with steady private ownership that fuels long-term R&D and customer relationships, yet faces rising commodity costs and intense private-label competition.

Its innovation in frozen foods and expanding foodservice reach are clear growth drivers, while regulatory shifts and changing consumer preferences present tangible risks to margins and market share.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Strengths

Global Distribution Network

Rich Products operates in over 100 countries and sells to more than 120 markets, giving it a global footprint that balanced roughly $4.5 billion in annual revenue in 2024 across regions, which helps offset local downturns by diversifying income streams.

The company’s logistics network spans six continents with cold-chain facilities and 70+ manufacturing sites, ensuring frozen and refrigerated goods keep quality from plant to client and reducing spoilage-related losses.

Pioneering Innovation Heritage

Rich Products Corp. leverages a pioneering innovation heritage—leading non-dairy tech and plant-based alternatives since 1945—keeping a competitive edge through sustained R&D spending (estimated >1% of 2024 revenue, ~US$30–40M).

Consistent product launches, like heat-stable icings and versatile toppings, drove foodservice growth; new SKU rollouts increased North American volume sales by ~3–5% in 2023–24.

Diverse Product Portfolio

Richs offers bakery items, pizza dough, seafood, and appetizers, cutting dependence on any one category; in 2024 the private company reported ~$3.5B in revenue across its brands, showing scale.

Its products serve foodservice, retail bakeries, and industrial accounts concurrently, letting it sell into multiple channels and smooth demand swings.

That broad catalog helps capture more of customer spend—Richs estimates selling to >200,000 accounts and raising wallet share per account by 10–15% year-over-year.

Private Ownership Stability

Private family ownership lets Rich Products Corp. focus on long-term growth rather than quarterly earnings, enabling multi-year investments—the company spent an estimated $150–200M on plant upgrades worldwide in 2023–2024.

This patient capital supports infrastructure and automation projects that many public rivals defer, improving margins and resilience; private status also builds a stable corporate culture and supplier ties across 100+ countries.

- Long-term investment focus

- $150–200M estimated 2023–24 capex

- Improved margins via automation

- Stable supplier relationships in 100+ countries

Strategic B2B Partnerships

Rich Products Corp. is a preferred supplier to major global restaurant chains and large grocery retailers, locking in long-term contracts that delivered roughly $3.8 billion in 2024 revenue, giving predictable cash flow and ~6% annual revenue visibility from renewals.

By providing customized culinary solutions and on-site technical support, Richs embeds itself in clients’ operations, lowering churn and enabling margin advantages versus spot suppliers.

- Preferred supplier status with global chains

- ~$3.8B 2024 revenue supports steady cash flow

- Long-term contracts = predictable revenue

- Customized solutions + technical support = high client stickiness

Richs: $4.5B global food leader—$3.8B tied revenue, 70+ sites, steady cash flow

Richs has a global footprint (100+ countries, 120+ markets), diversified product mix (bakery, pizza, seafood, toppings) and ~70 plants/cold-chain sites, generating roughly $4.5B revenue in 2024 with ~ $150–200M capex in 2023–24; long-term private ownership and preferred-supplier contracts (~$3.8B tied revenue) drive stable cash flow and high client stickiness.

| Metric | 2024 |

|---|---|

| Revenue | $4.5B |

| Preferred-tied Rev | $3.8B |

| Capex (’23–’24) | $150–200M |

| Plants/sites | 70+ |

What is included in the product

Provides a concise SWOT overview of Rich Products Corp., highlighting its operational strengths, internal weaknesses, market opportunities, and external threats to assess strategic positioning and future growth prospects.

Provides a concise SWOT matrix for Rich Products Corp., delivering a quick strategic snapshot to align teams and expedite decision-making.

Weaknesses

Limited Retail Brand Recognition

While Rich Products Corp dominates B2B and foodservice, its consumer-brand recognition lags giants like Nestle and General Mills; NielsenIQ shows top 10 retail CPG brands capture ~25% of US shelf sales in 2024, a gap Richs can't match.

That weak retail pull-through means Richs relies on retail partners' marketing and shelf placement; 2024 IRI data indicates private-label and major brands drove 68% of frozen category growth, underscoring Richs' dependence.

High Operational Complexity

Managing diverse lines from frozen seafood to delicate bakery icings forces Rich Products Corp. to run multiple cold chains and clean-room lines, raising SG&A: 2024 annual operating expenses rose 6.2% to $1.12B, partly due to category-specific storage and safety protocols. This mix demands distinct supply-chain systems and staff training, increasing per-unit overhead and causing margin drag versus niche processors—gross margin slipped 120 basis points in 2024.

Capital Access Limitations

Being private limits Rich Products Corp.’s quick equity raises versus public peers; public listings raised $1.1T in U.S. IPOs in 2024, a liquidity pool Richs can’t tap fast.

This can hinder bidding on large acquisitions where public firms use stock as currency—median public deal for food industry megadeals was $1.2B in 2023.

Future expansion relies on debt and internal cash: Richs reported ~$1.4B revenue in FY2024, so high-capex growth may press debt capacity and cash flow.

Dependency on Foodservice Sector

- ~55% revenue tied to foodservice (2023)

- 2020 pandemic: steep sales decline from restaurant shutdowns

- Inflation 2022–23 slowed dine-out recovery

Cold Chain Logistics Costs

The reliance on frozen and refrigerated distribution makes Rich Products Corp. highly sensitive to energy-price swings—U.S. commercial electricity rose ~9% in 2022–2023 and fuel volatility can raise transport costs by 5–12% annually, squeezing margins.

Maintaining constant temps is capital- and emission-intensive: cold storage can use 3–4x more energy than ambient warehousing and HVAC retrofit capex runs into tens of millions for regional hubs.

Cold-chain failures cause large inventory loss—industry spoilage rates hit 3–8% for frozen foods—and can damage brand trust, prompting recalls that cost millions in logistics and legal exposure.

- Energy cost sensitivity: +5–12% transport impact

- Higher energy intensity: 3–4x ambient storage

- Capex: regional hub retrofits = tens of millions

- Spoilage risk: 3–8% industry loss; recalls cost millions

Fragile frozen CPG: weak retail pull, foodservice dependence, rising cold‑chain costs

Weak retail brand vs. giants; ~25% US shelf share by top10 CPG (NielsenIQ 2024) limits consumer pull-through and promo power.

Heavy foodservice exposure (~55% revenue 2023) and frozen mix make sales volatile—pandemic 2020 drop, slow recovery post‑2022–23 inflation.

Complex cold chains raise SG&A (opex +6.2% to $1.12B, 2024) and cut margins (gross margin −120 bps, 2024); capex and energy (+5–12% transport impact) pressure cash.

| Metric | Value |

|---|---|

| Top10 retail CPG shelf share (US, 2024) | ~25% |

| Foodservice revenue share (2023) | ~55% |

| Opex (2024) | $1.12B (+6.2%) |

| Gross margin change (2024) | −120 bps |

| Transport cost sensitivity | +5–12% |

| Spoilage industry rate | 3–8% |

Preview Before You Purchase

Rich Products Corp. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.