Rinnai Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

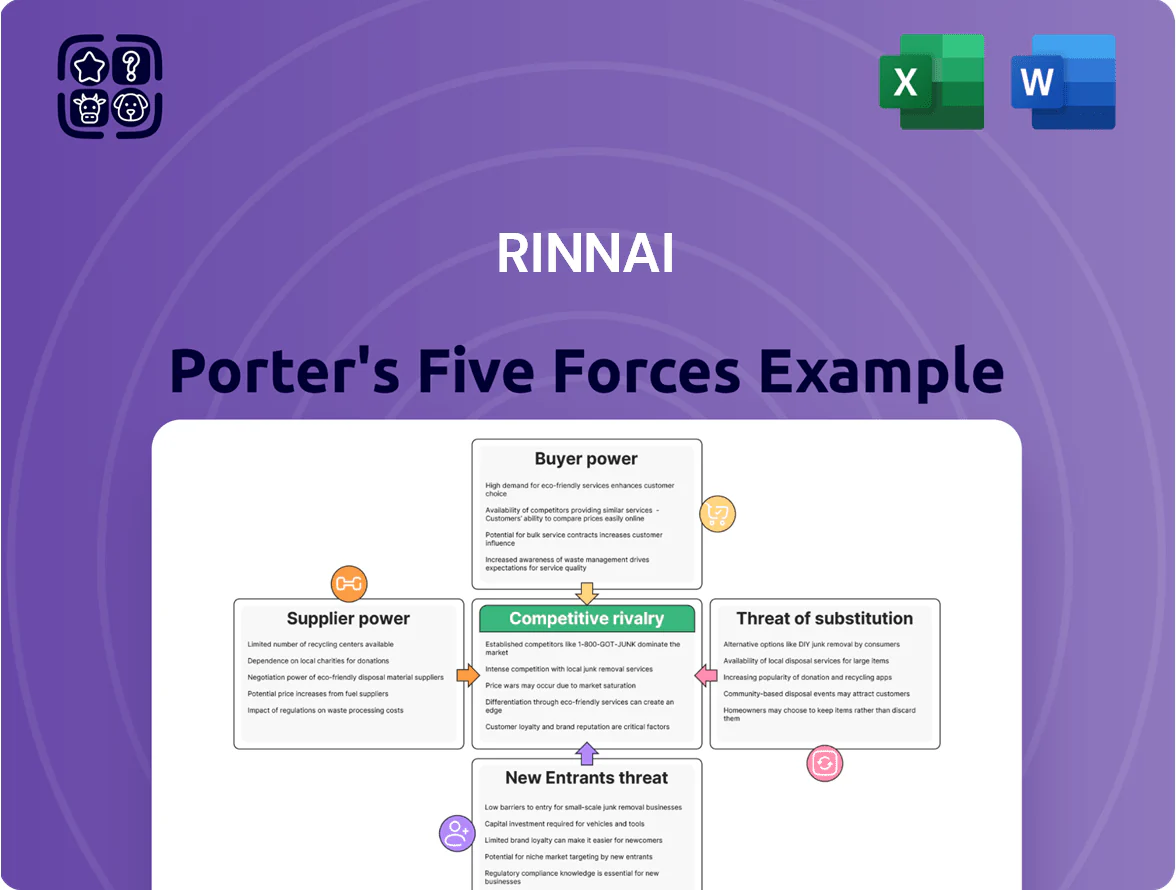

Rinnai faces moderate rivalry from established HVAC and water-heating brands, tempered by its strong product differentiation and global distribution network; supplier power is contained but component shortages pose periodic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Rinnai’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic Component Dependency

As Rinnai shifts to smart, connected appliances, reliance on semiconductor and sensor makers rose sharply by late 2025, with procurement spend on high-tech parts up ~38% year-over-year to an estimated ¥45 billion (about $330M), heightening supplier leverage.

These specialized chips and sensors are key to energy-efficiency and IoT features and remain hard to commoditize, so suppliers can demand premium prices and priority allocation.

To avoid production delays and a projected 12% hit to rollout timelines if supply tightens, Rinnai must lock multi-year contracts, co-design agreements, and dual-sourcing with strategic partners.

Raw Material Price Volatility

Rinnai relies heavily on copper, steel, and aluminum; LME copper rose 18% in 2024 and stayed volatile into 2025, forcing Rinnai to absorb cost swings to keep quality.

Despite Rinnai’s scale and FY2024 COGS discipline, a small pool of high‑grade metal suppliers gives those suppliers pricing leverage.

By end‑2025, geopolitical tensions and tighter mining rules in Chile and Indonesia keep supplier bargaining power relatively high, pressuring margins.

Proprietary Technology and Patents

Proprietary third-party patents and specialized engineering for Rinnai high-efficiency tankless units limit supplier switching, raising supplier bargaining power and risking performance loss or IP infringement.

Suppliers of hydrogen-combustion components and advanced heat exchangers can charge premiums; industry data shows specialty component markups of 15–30% and supplier concentration ratios where top 3 vendors control ~60% of niche parts supply (2024).

Logistics and Energy Costs

Suppliers of logistics and transportation services exert strong bargaining power over Rinnai by controlling global distribution of bulky heaters and heavy components, making freight rates a key cost lever; in 2025 average ocean freight rates remained ~60% above 2019 levels per Drewry and peak BAF surcharges rose 10–15% as carriers shift to green fuels.

Rising energy prices and the move to green shipping fuels let logistics providers add fuel surcharges that directly compress Rinnai’s margins; with Rinnai’s export share near 40% of revenue, exposure to volatile freight and bunker-cost pass-through is significant.

- Global freight ~60% above 2019 (Drewry, 2025)

- BAF surcharges +10–15% in 2025

- Rinnai export share ≈40% of revenue

- Energy-driven surcharges directly hit gross margin

Supplier Consolidation Trends

The consolidation of industrial part makers has cut suppliers for heating elements and gas valves by ~40% since 2018, leaving 3–4 global suppliers with pricing leverage over OEMs like Rinnai as of 2025.

With fewer vendors, suppliers set longer lead times (often 16–24 weeks) and tighter minimum orders, pushing Rinnai into multi-year contracts to guarantee priority allocation for its global boiler and water‑heater lines.

- ~40% fewer suppliers since 2018

- 3–4 dominant global suppliers by 2025

- Typical lead times 16–24 weeks

- Multi-year contracts common to secure supply

Supplier power squeezes margins: 60% niche control, 15–30% markups, +60% freight

Suppliers hold high bargaining power due to specialized semiconductors, metals volatility, and concentrated niche-part markets; supplier markups run 15–30% and top‑3 vendors control ~60% of niche supply (2024), while freight rates ~60% above 2019 and export exposure (~40% revenue) add cost pressure, forcing Rinnai into multi‑year contracts, dual‑sourcing, and co‑design to secure allocations.

| Metric | Value |

|---|---|

| Semiconductor spend (2025) | ¥45B (~$330M) |

| Niche supplier conc. | Top 3 ≈60% (2024) |

| Specialty markups | 15–30% |

| Freight vs 2019 | ≈+60% (2025) |

| Export share | ≈40% revenue |

What is included in the product

Tailored Porter's Five Forces analysis for Rinnai that uncovers competitive drivers, supplier and buyer influence, barriers to entry, and substitute threats, with strategic commentary on market positioning and disruption risks.

A concise Porter's Five Forces one-sheet for Rinnai—instantly highlights supplier, buyer, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Influence of Professional Installers

Retailer Concentration in Consumer Markets

Large home-improvement chains like The Home Depot and Lowe's control roughly 45–55% of US DIY/heavy‑appliance shelf space, giving them strong leverage over Rinnai; they demand lower wholesale prices, co‑op marketing funds, and tight JIT delivery windows that compress manufacturer margins by an estimated 150–300 basis points. In 2025 Rinnai risks losing several percentage points of national market share if a single major distributor contract is lost, given channel concentration and promotion control.

Price Sensitivity in Residential Segments

At end-2025, rising living costs and mortgage rates near 6.5% in key markets make individual homeowners highly price-sensitive, shifting purchase decisions toward lower upfront cost tank heaters despite Rinnai’s reputation for premium quality.

Customers compare total cost of ownership; a Rinnai tankless unit saving ~30% on annual energy bills versus a tank model must offset a typical price premium of US$600–1,200 within 3–6 years to justify purchase.

Availability of Information and Reviews

The rise of digital platforms and review systems lets buyers use real-world performance data to make choices; 72% of US appliance shoppers referenced online reviews in 2024, pressuring Rinnai on perceived value.

Customers can compare Rinnai efficiency and reliability scores versus Rheem and Navien in real time, limiting price increases unless Rinnai shows clear, measurable tech or service gains.

- 72% of shoppers used reviews (US, 2024)

- Real-time comparisons vs Rheem/Navien

- Price hikes need visible tech/service gains

Government Incentives and Rebates

By 2025, over 40 countries and 120 subnational jurisdictions offered rebates or tax credits for high-efficiency or electric-hybrid water heaters, letting buyers cut upfront costs by 20–50%, which raises customer leverage in price negotiations.

Customers use these subsidies to demand lower net prices and faster delivery; Rinnai’s bargaining position weakens unless net prices match post-rebate competitors.

Rinnai must align product mix to qualifying models—electric-hybrid and >95% AFUE gas units—and track regional rebate rules to stay a financially attractive choice.

- 40+ countries, 120 jurisdictions with rebates

- 20–50% typical upfront cost reduction

- Requirement: >95% AFUE or electric-hybrid models

- Action: map incentives by market quarterly

Installer & Retail Power Squeezes Margins; Rebates, Reviews Drive Tank vs Tankless Shift

| Metric | Value |

|---|---|

| Installer control | 60–70% |

| Retail shelf share | 45–55% |

| Installer margin | 8–12% |

| Homeowner mortgage (2025) | ~6.5% |

| Review usage (US, 2024) | 72% |

| Rebate coverage | 40+ countries, 120 jurisdictions (20–50%) |

Preview the Actual Deliverable

Rinnai Porter's Five Forces Analysis

This preview shows the exact Rinnai Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups; it's the full, professionally formatted document ready for immediate download and use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Rinnai faces moderate rivalry from established HVAC and water-heating brands, tempered by its strong product differentiation and global distribution network; supplier power is contained but component shortages pose periodic risks.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Rinnai’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Electronic Component Dependency

As Rinnai shifts to smart, connected appliances, reliance on semiconductor and sensor makers rose sharply by late 2025, with procurement spend on high-tech parts up ~38% year-over-year to an estimated ¥45 billion (about $330M), heightening supplier leverage.

These specialized chips and sensors are key to energy-efficiency and IoT features and remain hard to commoditize, so suppliers can demand premium prices and priority allocation.

To avoid production delays and a projected 12% hit to rollout timelines if supply tightens, Rinnai must lock multi-year contracts, co-design agreements, and dual-sourcing with strategic partners.

Raw Material Price Volatility

Rinnai relies heavily on copper, steel, and aluminum; LME copper rose 18% in 2024 and stayed volatile into 2025, forcing Rinnai to absorb cost swings to keep quality.

Despite Rinnai’s scale and FY2024 COGS discipline, a small pool of high‑grade metal suppliers gives those suppliers pricing leverage.

By end‑2025, geopolitical tensions and tighter mining rules in Chile and Indonesia keep supplier bargaining power relatively high, pressuring margins.

Proprietary Technology and Patents

Proprietary third-party patents and specialized engineering for Rinnai high-efficiency tankless units limit supplier switching, raising supplier bargaining power and risking performance loss or IP infringement.

Suppliers of hydrogen-combustion components and advanced heat exchangers can charge premiums; industry data shows specialty component markups of 15–30% and supplier concentration ratios where top 3 vendors control ~60% of niche parts supply (2024).

Logistics and Energy Costs

Suppliers of logistics and transportation services exert strong bargaining power over Rinnai by controlling global distribution of bulky heaters and heavy components, making freight rates a key cost lever; in 2025 average ocean freight rates remained ~60% above 2019 levels per Drewry and peak BAF surcharges rose 10–15% as carriers shift to green fuels.

Rising energy prices and the move to green shipping fuels let logistics providers add fuel surcharges that directly compress Rinnai’s margins; with Rinnai’s export share near 40% of revenue, exposure to volatile freight and bunker-cost pass-through is significant.

- Global freight ~60% above 2019 (Drewry, 2025)

- BAF surcharges +10–15% in 2025

- Rinnai export share ≈40% of revenue

- Energy-driven surcharges directly hit gross margin

Supplier Consolidation Trends

The consolidation of industrial part makers has cut suppliers for heating elements and gas valves by ~40% since 2018, leaving 3–4 global suppliers with pricing leverage over OEMs like Rinnai as of 2025.

With fewer vendors, suppliers set longer lead times (often 16–24 weeks) and tighter minimum orders, pushing Rinnai into multi-year contracts to guarantee priority allocation for its global boiler and water‑heater lines.

- ~40% fewer suppliers since 2018

- 3–4 dominant global suppliers by 2025

- Typical lead times 16–24 weeks

- Multi-year contracts common to secure supply

Supplier power squeezes margins: 60% niche control, 15–30% markups, +60% freight

Suppliers hold high bargaining power due to specialized semiconductors, metals volatility, and concentrated niche-part markets; supplier markups run 15–30% and top‑3 vendors control ~60% of niche supply (2024), while freight rates ~60% above 2019 and export exposure (~40% revenue) add cost pressure, forcing Rinnai into multi‑year contracts, dual‑sourcing, and co‑design to secure allocations.

| Metric | Value |

|---|---|

| Semiconductor spend (2025) | ¥45B (~$330M) |

| Niche supplier conc. | Top 3 ≈60% (2024) |

| Specialty markups | 15–30% |

| Freight vs 2019 | ≈+60% (2025) |

| Export share | ≈40% revenue |

What is included in the product

Tailored Porter's Five Forces analysis for Rinnai that uncovers competitive drivers, supplier and buyer influence, barriers to entry, and substitute threats, with strategic commentary on market positioning and disruption risks.

A concise Porter's Five Forces one-sheet for Rinnai—instantly highlights supplier, buyer, and competitive pressures to speed strategic decisions.

Customers Bargaining Power

Influence of Professional Installers

Retailer Concentration in Consumer Markets

Large home-improvement chains like The Home Depot and Lowe's control roughly 45–55% of US DIY/heavy‑appliance shelf space, giving them strong leverage over Rinnai; they demand lower wholesale prices, co‑op marketing funds, and tight JIT delivery windows that compress manufacturer margins by an estimated 150–300 basis points. In 2025 Rinnai risks losing several percentage points of national market share if a single major distributor contract is lost, given channel concentration and promotion control.

Price Sensitivity in Residential Segments

At end-2025, rising living costs and mortgage rates near 6.5% in key markets make individual homeowners highly price-sensitive, shifting purchase decisions toward lower upfront cost tank heaters despite Rinnai’s reputation for premium quality.

Customers compare total cost of ownership; a Rinnai tankless unit saving ~30% on annual energy bills versus a tank model must offset a typical price premium of US$600–1,200 within 3–6 years to justify purchase.

Availability of Information and Reviews

The rise of digital platforms and review systems lets buyers use real-world performance data to make choices; 72% of US appliance shoppers referenced online reviews in 2024, pressuring Rinnai on perceived value.

Customers can compare Rinnai efficiency and reliability scores versus Rheem and Navien in real time, limiting price increases unless Rinnai shows clear, measurable tech or service gains.

- 72% of shoppers used reviews (US, 2024)

- Real-time comparisons vs Rheem/Navien

- Price hikes need visible tech/service gains

Government Incentives and Rebates

By 2025, over 40 countries and 120 subnational jurisdictions offered rebates or tax credits for high-efficiency or electric-hybrid water heaters, letting buyers cut upfront costs by 20–50%, which raises customer leverage in price negotiations.

Customers use these subsidies to demand lower net prices and faster delivery; Rinnai’s bargaining position weakens unless net prices match post-rebate competitors.

Rinnai must align product mix to qualifying models—electric-hybrid and >95% AFUE gas units—and track regional rebate rules to stay a financially attractive choice.

- 40+ countries, 120 jurisdictions with rebates

- 20–50% typical upfront cost reduction

- Requirement: >95% AFUE or electric-hybrid models

- Action: map incentives by market quarterly

Installer & Retail Power Squeezes Margins; Rebates, Reviews Drive Tank vs Tankless Shift

| Metric | Value |

|---|---|

| Installer control | 60–70% |

| Retail shelf share | 45–55% |

| Installer margin | 8–12% |

| Homeowner mortgage (2025) | ~6.5% |

| Review usage (US, 2024) | 72% |

| Rebate coverage | 40+ countries, 120 jurisdictions (20–50%) |

Preview the Actual Deliverable

Rinnai Porter's Five Forces Analysis

This preview shows the exact Rinnai Porter's Five Forces analysis you'll receive after purchase—no placeholders, no mockups; it's the full, professionally formatted document ready for immediate download and use.