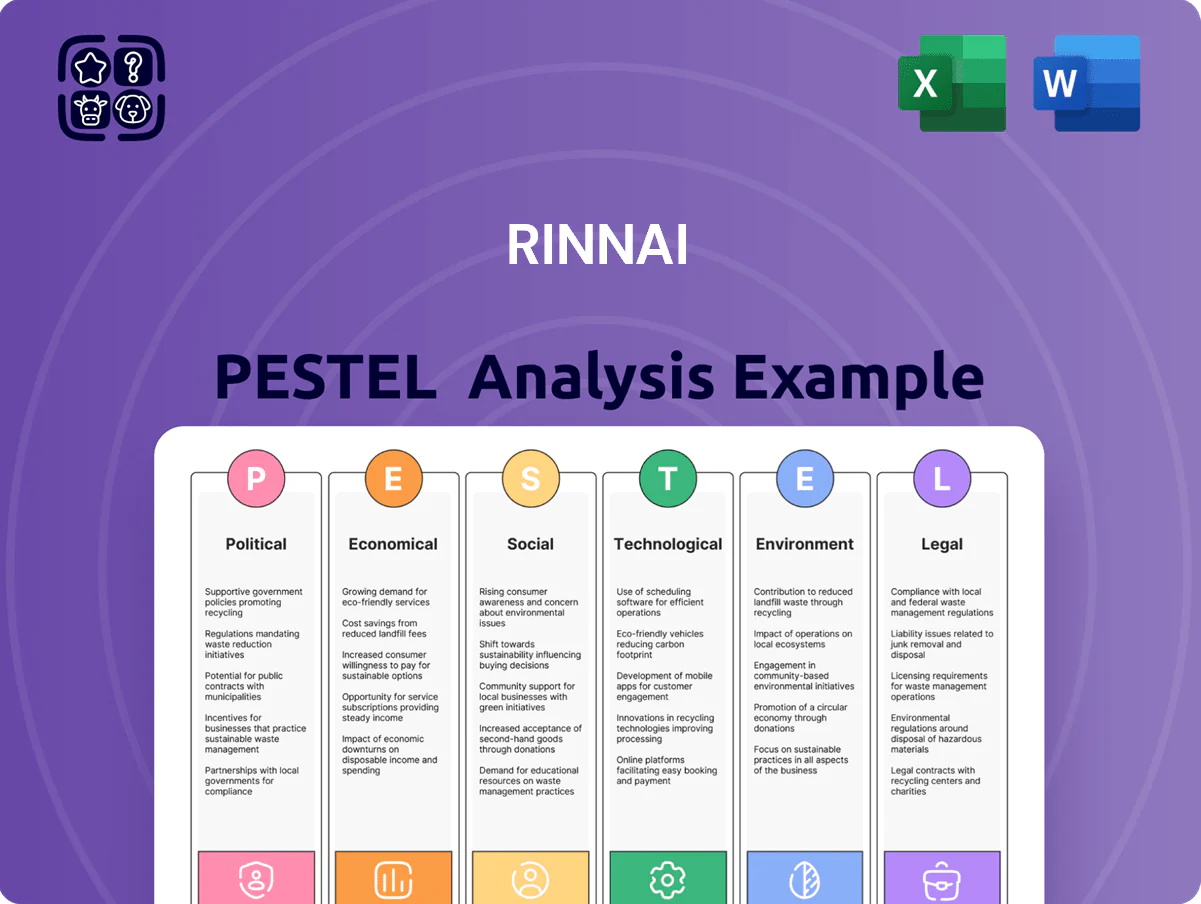

Rinnai PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech innovation are reshaping Rinnai’s market position with our concise PESTLE snapshot—then dive deeper with the full, actionable report designed for investors and strategists. Purchase the complete analysis to get ready-to-use insights, editable formats, and clear implications for risk and growth.

Political factors

Geopolitical Trade Relations

Stability of trade agreements between Japan and major markets such as the US and Australia affects Rinnai’s supply chain and export costs; Japan–US goods trade totaled $280.8 billion in 2024, so tariff shifts could materially affect margins. Recent protectionist talks and Australia’s 2024 review of gas appliance standards risk raising barriers, while tariff changes of even 2–5% would alter competitive pricing of Japanese-made units internationally; management must monitor diplomatic shifts for preferential treatment of domestic rivals.

Government Decarbonization Policies

National net-zero pledges (over 130 countries by 2050/2060) are tightening rules for gas appliances; EU Ecodesign/MEPS updates and UK local gas connection bans for new homes by 2025–2028 push electrification. Subsidy programs—e.g., EU Recovery funds, UK Boiler Upgrade Scheme (£450m to 2028), and US IRA tax credits—favor heat pumps, reducing gas boiler demand ~10–20% in targeted markets. Rinnai must pivot R&D, sales and supply chains toward electrified and hydrogen-ready products to retain market share and revenue.

Energy Security Initiatives

Political instability in energy-exporting regions has driven spot natural gas price volatility—European TTF rose ~65% in 2022 and remained 30% above 2019 averages through 2024—dampening consumer confidence in pure-gas appliances.

Governments are pushing diversification: EU member states target 45% renewables and 25% hydrogen-ready heating by 2030, increasing likelihood of mandates for hybrid gas-electric systems.

Rinnai must align R&D and product roadmaps with national energy security frameworks—allocating CAPEX toward hybrid/hydrogen-ready units and targeting markets with supportive regulation to retain market share.

Subsidy Programs for Energy Efficiency

Political funding of rebates for high-efficiency tankless water heaters and boilers directly boosts demand for Rinnai’s premium units; U.S. federal and state programs allocated roughly $9–12 billion for residential energy-efficiency rebates in 2024–2025, supporting higher ASPs and volumes.

These incentives vary with budget cycles and elections, causing year-over-year demand swings—some states cut or expanded rebates by 30–60% within two-year windows, increasing forecasting risk for Rinnai.

Assessing policy durability across markets (U.S., Japan, Australia, EU) is critical: a 1-year rebate lapse can reduce regional unit sales 15–25% per industry estimates, affecting revenue visibility.

- Rebate funding boosts premium-unit demand; 2024–25 U.S. EE rebates ~$9–12B

- Political cycles cause 30–60% regional incentive swings

- 1-year rebate lapse may cut regional sales 15–25%

- Policy longevity essential for accurate segment-level revenue forecasts

Regional Housing Regulations

Regional building codes increasingly restrict on-site fossil fuel appliances; in 2024 over 120 US cities enacted fossil-fuel-free or gas-ban policies, which can reduce demand for Rinnai's residential gas units.

High-density urban plans often prefer centralized systems, potentially cutting commercial unit sales; globally district heating serves 12% of heat demand, pressuring unitized offerings.

Varying mandates force Rinnai to adopt flexible manufacturing and distribution; in 2025 adaptive product lines and localized inventory reduced lead times by up to 20% for some HVAC firms.

- 120+ US cities with gas restrictions (2024)

Policy shocks push Rinnai into hybrid/hydrogen R&D and stable-incentive markets

Political shifts—trade/tariff volatility (Japan–US goods trade $280.8B in 2024), subsidy flows (~$9–12B US EE rebates 2024–25), 120+ US city gas bans (2024), and EU/UK electrification mandates—drive Rinnai to reallocate CAPEX to hybrid/hydrogen-ready R&D and target markets with stable incentives to protect margins and volumes.

| Factor | 2024–25 data |

|---|---|

| Japan–US trade | $280.8B |

| US EE rebates | $9–12B |

| US gas bans | 120+ cities |

What is included in the product

Explores how external macro-environmental factors uniquely affect Rinnai across six dimensions—Political, Economic, Social, Technological, Environmental, Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and entrepreneurs.

A concise Rinnai PESTLE snapshot that distills regulatory, economic, social, technological, environmental and legal factors into a single, shareable slide for fast decision-making.

Economic factors

Global Inflation and Material Costs

Fluctuations in copper, stainless steel and semiconductors have lifted Rinnai's input costs; copper rose ~35% from 2020–2023 and global semiconductor shortages pushed component premiums of 10–25% in 2021–2022, squeezing gross margins reported at 22.8% in FY2023. Persistent inflation—global CPI ~6.8% in 2022, easing to ~3.2% in 2024—dampens household purchasing power and delays appliance upgrades. Rinnai uses forward contracts, commodity hedges and targeted price increases to protect margins while monitoring elasticities in key markets.

Interest Rate Volatility

Rising interest rates curb new residential and commercial construction—Japan's housing starts fell 8.6% y/y in 2024 H1—reducing demand for Rinnai's residential and commercial boilers and water heaters.

Higher borrowing costs also raise financing expenses for industrial heating projects, with global project finance spreads up ~120–150 bps in 2024, increasing cancellations or delays.

Investors track BOJ and Fed signals closely; a 25–50 bps shift in policy rates historically precedes 3–6 month changes in Rinnai's domestic and export order volumes.

Currency Exchange Rate Fluctuations

As a Japanese firm with ~70% revenue from overseas in FY2024, Rinnai is highly sensitive to JPY/USD, JPY/EUR and JPY/AUD moves; a weak yen in 2024 (JPY ~155/USD mid-2024 vs ~130 in 2021) improved export competitiveness but raised imported energy and material costs, squeezing gross margins.

Currency volatility drove Rinnai to expand hedging: FY2024 disclosures show forward contracts covering a significant portion of projected receivables/payables to limit translation and transaction losses, preserving consolidated operating income.

Labor Market Dynamics

Rising labor costs and shortages of skilled technicians raise consumer total cost of ownership; in Japan average hourly manufacturing wages rose ~3.2% in 2024, while tech vacancies in construction/appliances climbed ~12% year-on-year, increasing installation/maintenance expenses.

Shrinking workforce — Japan's working-age population fell ~1.0% in 2024 — pushes wages up, raising Rinnai's manufacturing overhead and benefits costs.

Rinnai likely must boost automation and simplify installation; capital expenditure on automation in Japan's appliance sector rose ~8% in 2024, signaling industry shift.

- Higher wages: +3.2% avg manufacturing wage (2024)

- Tech shortages: +12% vacancies (2024)

- Workforce decline: −1.0% working-age pop (2024)

- Capex trend: automation spend +8% (2024)

Consumer Disposable Income Trends

The demand for Rinnai’s premium, energy-efficient gas appliances tracks middle and upper-class disposable income; US median household disposable income rose ~3.1% in 2024 while consumer confidence averaged 96.1, supporting durable goods spending in higher-income brackets.

In downturns buyers favor repairs over replacements, reducing tankless uptake—US HVAC replacement volumes fell ~6% in 2023; Rinnai monitors confidence and retail sales to cut inventory and pivot marketing to value propositions.

- Disposable income +3.1% (2024 US)

- Consumer confidence avg 96.1 (2024)

- HVAC replacement volumes -6% (2023)

- Adjust marketing/inventory to spending shifts

Supply-cost surge, weaker yen and wage rise squeeze margins as automation ramps

Input-cost inflation (copper +35% 2020–23; semiconductor premiums 10–25% in 2021–22) and FY2023 gross margin 22.8%; global CPI peaked ~6.8% (2022) eased to ~3.2% (2024). FY2024: ~70% revenue overseas; JPY ~155/USD mid-2024 vs ~130 (2021). Japan manufacturing wages +3.2% (2024); working-age pop −1.0% (2024); automation capex +8% (2024).

| Metric | Value |

|---|---|

| Gross margin FY2023 | 22.8% |

| Copper 2020–23 | +35% |

| JPY/USD mid-2024 | ~155 |

| Wage growth Japan 2024 | +3.2% |

Preview Before You Purchase

Rinnai PESTLE Analysis

The preview shown here is the exact Rinnai PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock how political shifts, economic cycles, and tech innovation are reshaping Rinnai’s market position with our concise PESTLE snapshot—then dive deeper with the full, actionable report designed for investors and strategists. Purchase the complete analysis to get ready-to-use insights, editable formats, and clear implications for risk and growth.

Political factors

Geopolitical Trade Relations

Stability of trade agreements between Japan and major markets such as the US and Australia affects Rinnai’s supply chain and export costs; Japan–US goods trade totaled $280.8 billion in 2024, so tariff shifts could materially affect margins. Recent protectionist talks and Australia’s 2024 review of gas appliance standards risk raising barriers, while tariff changes of even 2–5% would alter competitive pricing of Japanese-made units internationally; management must monitor diplomatic shifts for preferential treatment of domestic rivals.

Government Decarbonization Policies

National net-zero pledges (over 130 countries by 2050/2060) are tightening rules for gas appliances; EU Ecodesign/MEPS updates and UK local gas connection bans for new homes by 2025–2028 push electrification. Subsidy programs—e.g., EU Recovery funds, UK Boiler Upgrade Scheme (£450m to 2028), and US IRA tax credits—favor heat pumps, reducing gas boiler demand ~10–20% in targeted markets. Rinnai must pivot R&D, sales and supply chains toward electrified and hydrogen-ready products to retain market share and revenue.

Energy Security Initiatives

Political instability in energy-exporting regions has driven spot natural gas price volatility—European TTF rose ~65% in 2022 and remained 30% above 2019 averages through 2024—dampening consumer confidence in pure-gas appliances.

Governments are pushing diversification: EU member states target 45% renewables and 25% hydrogen-ready heating by 2030, increasing likelihood of mandates for hybrid gas-electric systems.

Rinnai must align R&D and product roadmaps with national energy security frameworks—allocating CAPEX toward hybrid/hydrogen-ready units and targeting markets with supportive regulation to retain market share.

Subsidy Programs for Energy Efficiency

Political funding of rebates for high-efficiency tankless water heaters and boilers directly boosts demand for Rinnai’s premium units; U.S. federal and state programs allocated roughly $9–12 billion for residential energy-efficiency rebates in 2024–2025, supporting higher ASPs and volumes.

These incentives vary with budget cycles and elections, causing year-over-year demand swings—some states cut or expanded rebates by 30–60% within two-year windows, increasing forecasting risk for Rinnai.

Assessing policy durability across markets (U.S., Japan, Australia, EU) is critical: a 1-year rebate lapse can reduce regional unit sales 15–25% per industry estimates, affecting revenue visibility.

- Rebate funding boosts premium-unit demand; 2024–25 U.S. EE rebates ~$9–12B

- Political cycles cause 30–60% regional incentive swings

- 1-year rebate lapse may cut regional sales 15–25%

- Policy longevity essential for accurate segment-level revenue forecasts

Regional Housing Regulations

Regional building codes increasingly restrict on-site fossil fuel appliances; in 2024 over 120 US cities enacted fossil-fuel-free or gas-ban policies, which can reduce demand for Rinnai's residential gas units.

High-density urban plans often prefer centralized systems, potentially cutting commercial unit sales; globally district heating serves 12% of heat demand, pressuring unitized offerings.

Varying mandates force Rinnai to adopt flexible manufacturing and distribution; in 2025 adaptive product lines and localized inventory reduced lead times by up to 20% for some HVAC firms.

- 120+ US cities with gas restrictions (2024)

Policy shocks push Rinnai into hybrid/hydrogen R&D and stable-incentive markets

Political shifts—trade/tariff volatility (Japan–US goods trade $280.8B in 2024), subsidy flows (~$9–12B US EE rebates 2024–25), 120+ US city gas bans (2024), and EU/UK electrification mandates—drive Rinnai to reallocate CAPEX to hybrid/hydrogen-ready R&D and target markets with stable incentives to protect margins and volumes.

| Factor | 2024–25 data |

|---|---|

| Japan–US trade | $280.8B |

| US EE rebates | $9–12B |

| US gas bans | 120+ cities |

What is included in the product

Explores how external macro-environmental factors uniquely affect Rinnai across six dimensions—Political, Economic, Social, Technological, Environmental, Legal—backed by current data and trends to identify risks and opportunities for executives, consultants, and entrepreneurs.

A concise Rinnai PESTLE snapshot that distills regulatory, economic, social, technological, environmental and legal factors into a single, shareable slide for fast decision-making.

Economic factors

Global Inflation and Material Costs

Fluctuations in copper, stainless steel and semiconductors have lifted Rinnai's input costs; copper rose ~35% from 2020–2023 and global semiconductor shortages pushed component premiums of 10–25% in 2021–2022, squeezing gross margins reported at 22.8% in FY2023. Persistent inflation—global CPI ~6.8% in 2022, easing to ~3.2% in 2024—dampens household purchasing power and delays appliance upgrades. Rinnai uses forward contracts, commodity hedges and targeted price increases to protect margins while monitoring elasticities in key markets.

Interest Rate Volatility

Rising interest rates curb new residential and commercial construction—Japan's housing starts fell 8.6% y/y in 2024 H1—reducing demand for Rinnai's residential and commercial boilers and water heaters.

Higher borrowing costs also raise financing expenses for industrial heating projects, with global project finance spreads up ~120–150 bps in 2024, increasing cancellations or delays.

Investors track BOJ and Fed signals closely; a 25–50 bps shift in policy rates historically precedes 3–6 month changes in Rinnai's domestic and export order volumes.

Currency Exchange Rate Fluctuations

As a Japanese firm with ~70% revenue from overseas in FY2024, Rinnai is highly sensitive to JPY/USD, JPY/EUR and JPY/AUD moves; a weak yen in 2024 (JPY ~155/USD mid-2024 vs ~130 in 2021) improved export competitiveness but raised imported energy and material costs, squeezing gross margins.

Currency volatility drove Rinnai to expand hedging: FY2024 disclosures show forward contracts covering a significant portion of projected receivables/payables to limit translation and transaction losses, preserving consolidated operating income.

Labor Market Dynamics

Rising labor costs and shortages of skilled technicians raise consumer total cost of ownership; in Japan average hourly manufacturing wages rose ~3.2% in 2024, while tech vacancies in construction/appliances climbed ~12% year-on-year, increasing installation/maintenance expenses.

Shrinking workforce — Japan's working-age population fell ~1.0% in 2024 — pushes wages up, raising Rinnai's manufacturing overhead and benefits costs.

Rinnai likely must boost automation and simplify installation; capital expenditure on automation in Japan's appliance sector rose ~8% in 2024, signaling industry shift.

- Higher wages: +3.2% avg manufacturing wage (2024)

- Tech shortages: +12% vacancies (2024)

- Workforce decline: −1.0% working-age pop (2024)

- Capex trend: automation spend +8% (2024)

Consumer Disposable Income Trends

The demand for Rinnai’s premium, energy-efficient gas appliances tracks middle and upper-class disposable income; US median household disposable income rose ~3.1% in 2024 while consumer confidence averaged 96.1, supporting durable goods spending in higher-income brackets.

In downturns buyers favor repairs over replacements, reducing tankless uptake—US HVAC replacement volumes fell ~6% in 2023; Rinnai monitors confidence and retail sales to cut inventory and pivot marketing to value propositions.

- Disposable income +3.1% (2024 US)

- Consumer confidence avg 96.1 (2024)

- HVAC replacement volumes -6% (2023)

- Adjust marketing/inventory to spending shifts

Supply-cost surge, weaker yen and wage rise squeeze margins as automation ramps

Input-cost inflation (copper +35% 2020–23; semiconductor premiums 10–25% in 2021–22) and FY2023 gross margin 22.8%; global CPI peaked ~6.8% (2022) eased to ~3.2% (2024). FY2024: ~70% revenue overseas; JPY ~155/USD mid-2024 vs ~130 (2021). Japan manufacturing wages +3.2% (2024); working-age pop −1.0% (2024); automation capex +8% (2024).

| Metric | Value |

|---|---|

| Gross margin FY2023 | 22.8% |

| Copper 2020–23 | +35% |

| JPY/USD mid-2024 | ~155 |

| Wage growth Japan 2024 | +3.2% |

Preview Before You Purchase

Rinnai PESTLE Analysis

The preview shown here is the exact Rinnai PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning and decision-making.