RioCan Porter's Five Forces Analysis

From Overview to Strategy Blueprint

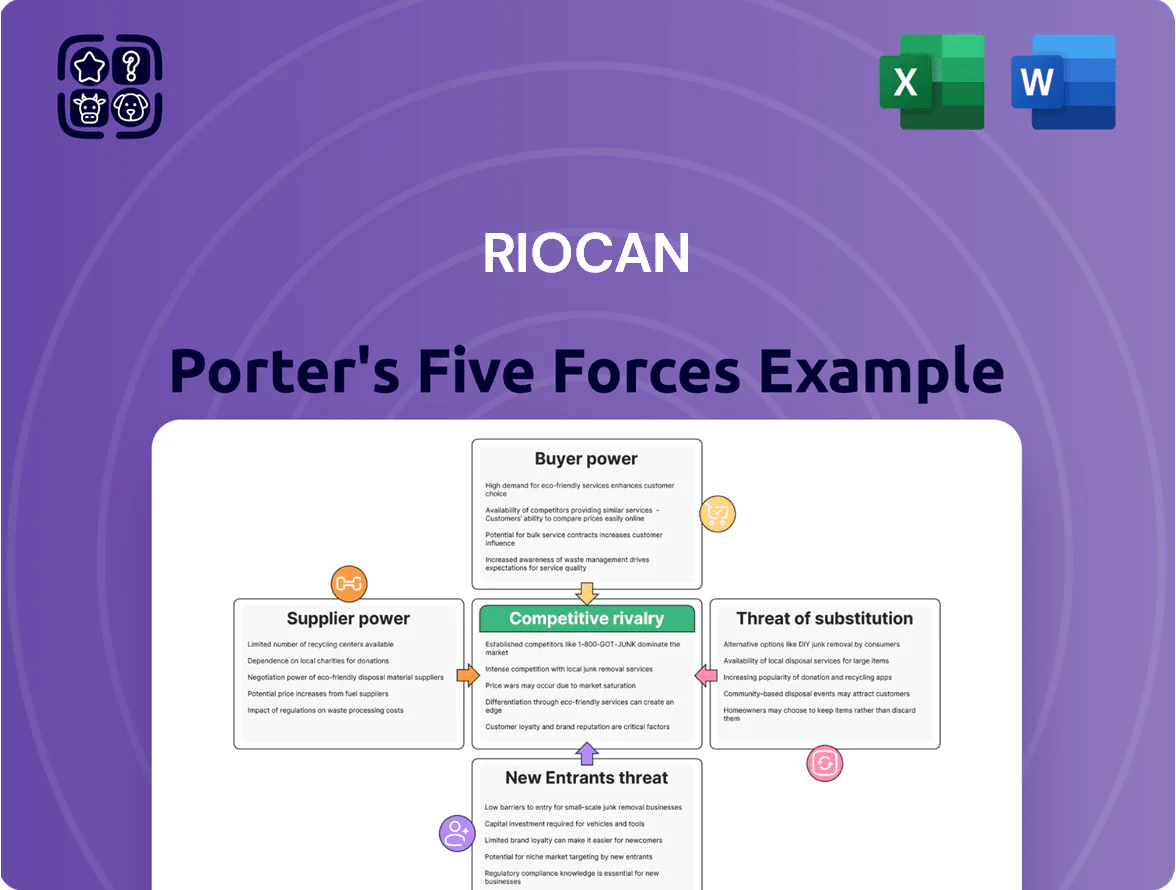

RioCan faces moderate buyer power and steady supplier relationships, while competition from other REITs and shifting retail trends raise rivalry and substitution risks; new entrants face high capital and scale barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RioCan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Construction and Trade Labor

The supply of specialized construction and trade labor for large mixed-use projects in Canada is concentrated among a few Tier-1 firms, raising supplier leverage as RioCan pivots to high-density residential work.

Reliance on these contractors increases bargaining power: Tier-1 firms can push prices and extend timelines, affecting margins and delivery risk.

In Toronto and Vancouver demand outstrips supply; Toronto added 50,000 housing starts in 2024 while skilled-trades shortages grew 8% year-over-year, amplifying supplier influence.

Limited Availability of Prime Urban Land

Landowners and municipalities control scarce prime urban land—RioCan’s key input—especially near transit nodes; in Toronto alone land near major transit saw site availability fall by ~18% from 2019–2024, boosting seller leverage.

Scarcity forces RioCan into joint ventures or paying premiums; RioCan reported $1.2B of JV investments and spent ~12% higher land costs on mixed-use sites in 2024 versus 2019 to secure its development pipeline.

Cost of Capital and Financial Institutional Influence

RioCan, as a REIT, depends on debt markets and banks to fund redevelopments; as of Q4 2025 its gross debt was about CAD 5.2bn and weighted average interest was ~3.9%, so lenders materially shape project costs. Major Canadian banks and pension funds set interest and covenant terms that restrict payout and leverage; RioCan’s scale gives negotiating room, but 2024–25 credit tightening and elevated bond yields limited capital recycling cadence.

Utility and Municipal Infrastructure Dependency

Municipalities and utility providers are non-substitutable suppliers for zoning, permits, and services; in 2024 Canadian municipalities collected roughly CAD 10.5B in development charges, raising project costs and timelines.

City planning departments can impose permit delays and fees that add 6–12 months and 5–15% to mixed-use project budgets, hitting RioCan Living rollout.

RioCan’s execution depends on strong relations with these monopolistic entities to secure timely approvals and utility hookups, reducing holdbacks and carrying costs.

- Municipal development charges ~CAD 10.5B (2024)

- Permit delays add 6–12 months

- Typical budget impact 5–15%

- Utility providers act as monopolistic suppliers

Material Price Volatility and Global Supply Chains

Suppliers of steel, concrete and specialized glass push pricing via global commodity markets; steel futures rose ~18% in 2024 and concrete input indexes climbed 9% year-over-year, forcing contractors to pass costs to RioCan during build phases.

Restricted domestic sources for high-tech façades mean shipping delays and tariffs (2023–24 container rates spiked 120%) can cut development margins by several percentage points on large projects.

- Steel futures +18% (2024)

- Concrete inputs +9% YoY

- Container rates +120% (2023–24)

- Margin hit: several percentage points on major developments

Supplier power forces RioCan to pay premiums, absorb input shocks and inject CAD1.2B

Supplier power is high: concentrated Tier‑1 contractors, scarce urban land, monopolistic utilities, and volatile commodity prices pushed RioCan to pay ~12% higher land premiums, absorb 2024 input price shocks (steel +18%, concrete +9%), and record CAD 1.2B JV equity in 2024 to secure pipeline.

| Metric | 2024/2025 |

|---|---|

| Land premium vs 2019 | +12% |

| JV investments | CAD 1.2B (2024) |

| Steel futures | +18% (2024) |

| Concrete inputs | +9% YoY |

| Permit delay impact | 6–12 months; +5–15% cost |

| Gross debt (Q4 2025) | CAD 5.2B; WAC ~3.9% |

What is included in the product

Tailored Porter’s Five Forces for RioCan, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and strategic pressures shaping its retail-focused REIT profitability and growth prospects.

A concise Porter's Five Forces one-sheet for RioCan that highlights bargaining power, competitive rivalry, and regulatory risks—ideal for swift investment or strategy decisions.

Customers Bargaining Power

Concentration of Anchor National Tenants

Residential Tenant Rights and Regulatory Protection

As RioCan grows its residential holdings, tenants gain outsized bargaining power via provincial rules: Ontario’s 2023 rent control covers most units and the Tenant Protection Act caps annual increases (guideline 2.5% for 2024), constraining RioCan’s rent growth and lease changes; in 2024 Ontario eviction applications rose 8%, signaling stronger tenant enforcement. This regulatory tilt reduces landlord pricing flexibility and raises revenue predictability risks for RioCan.

Low Switching Costs for Small Retailers

SMEs in RioCan’s malls face low switching costs versus anchors, so roughly 60–70% of non-anchor retail leases (2024 RioCan data) show higher churn risk if rents rise; many can move to e-commerce or local pop-ups. This mobility pushed RioCan to increase tenant improvement allowances—reported up to $30–50 per sq ft in 2024—and to add amenities, keeping national vacancy for non-anchor units near 6% in 2024.

Demand for Flexible Lease Structures

Post-pandemic shifts push tenants toward shorter leases and turnover-based rent, and in 2024 about 28% of new retail leases in Canada included variable rent components, eroding RioCan’s income predictability.

Large chains leverage scale to demand concessions—RioCan noted increased tenant requests for flexibility across 2023–2025, raising rollover risk and vacancy management costs.

Top-tier tenants face many mall options, so bargaining power grows and RioCan must trade fixed cash flow for occupancy and tenant mix.

- ~28% variable rent in 2024 new leases

- Higher lease turnover risk

- Scale favors large tenants

Sophistication of Institutional Joint Venture Partners

Institutional joint-venture partners—often Canadian pension funds and insurers—are RioCan’s customers in major mixed-use projects and wield strong bargaining power by demanding transparency, specific IRR hurdles (commonly 8–12% real), and board-level influence over development and disposition decisions.

These partners bring large capital pools (individual commitments often $50m–$500m) and governance standards, forcing RioCan to accept tighter reporting, clawbacks, and staggered capital calls that compress RioCan’s decision latitude and margin capture.

Anchors Drive Power: 28% Rent, 96% Occupancy; JVs Seek 8–12% IRR

| Metric | 2024 |

|---|---|

| Anchor share of base rent | ~28% |

| Anchor occupancy | ~96% |

| Non-anchor vacancy | ~6% |

| New leases with variable rent | ~28% |

| JV IRR demand | 8–12% real |

Full Version Awaits

RioCan Porter's Five Forces Analysis

This preview shows the exact RioCan Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; the full document is fully formatted, professionally written, and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

RioCan faces moderate buyer power and steady supplier relationships, while competition from other REITs and shifting retail trends raise rivalry and substitution risks; new entrants face high capital and scale barriers. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore RioCan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Construction and Trade Labor

The supply of specialized construction and trade labor for large mixed-use projects in Canada is concentrated among a few Tier-1 firms, raising supplier leverage as RioCan pivots to high-density residential work.

Reliance on these contractors increases bargaining power: Tier-1 firms can push prices and extend timelines, affecting margins and delivery risk.

In Toronto and Vancouver demand outstrips supply; Toronto added 50,000 housing starts in 2024 while skilled-trades shortages grew 8% year-over-year, amplifying supplier influence.

Limited Availability of Prime Urban Land

Landowners and municipalities control scarce prime urban land—RioCan’s key input—especially near transit nodes; in Toronto alone land near major transit saw site availability fall by ~18% from 2019–2024, boosting seller leverage.

Scarcity forces RioCan into joint ventures or paying premiums; RioCan reported $1.2B of JV investments and spent ~12% higher land costs on mixed-use sites in 2024 versus 2019 to secure its development pipeline.

Cost of Capital and Financial Institutional Influence

RioCan, as a REIT, depends on debt markets and banks to fund redevelopments; as of Q4 2025 its gross debt was about CAD 5.2bn and weighted average interest was ~3.9%, so lenders materially shape project costs. Major Canadian banks and pension funds set interest and covenant terms that restrict payout and leverage; RioCan’s scale gives negotiating room, but 2024–25 credit tightening and elevated bond yields limited capital recycling cadence.

Utility and Municipal Infrastructure Dependency

Municipalities and utility providers are non-substitutable suppliers for zoning, permits, and services; in 2024 Canadian municipalities collected roughly CAD 10.5B in development charges, raising project costs and timelines.

City planning departments can impose permit delays and fees that add 6–12 months and 5–15% to mixed-use project budgets, hitting RioCan Living rollout.

RioCan’s execution depends on strong relations with these monopolistic entities to secure timely approvals and utility hookups, reducing holdbacks and carrying costs.

- Municipal development charges ~CAD 10.5B (2024)

- Permit delays add 6–12 months

- Typical budget impact 5–15%

- Utility providers act as monopolistic suppliers

Material Price Volatility and Global Supply Chains

Suppliers of steel, concrete and specialized glass push pricing via global commodity markets; steel futures rose ~18% in 2024 and concrete input indexes climbed 9% year-over-year, forcing contractors to pass costs to RioCan during build phases.

Restricted domestic sources for high-tech façades mean shipping delays and tariffs (2023–24 container rates spiked 120%) can cut development margins by several percentage points on large projects.

- Steel futures +18% (2024)

- Concrete inputs +9% YoY

- Container rates +120% (2023–24)

- Margin hit: several percentage points on major developments

Supplier power forces RioCan to pay premiums, absorb input shocks and inject CAD1.2B

Supplier power is high: concentrated Tier‑1 contractors, scarce urban land, monopolistic utilities, and volatile commodity prices pushed RioCan to pay ~12% higher land premiums, absorb 2024 input price shocks (steel +18%, concrete +9%), and record CAD 1.2B JV equity in 2024 to secure pipeline.

| Metric | 2024/2025 |

|---|---|

| Land premium vs 2019 | +12% |

| JV investments | CAD 1.2B (2024) |

| Steel futures | +18% (2024) |

| Concrete inputs | +9% YoY |

| Permit delay impact | 6–12 months; +5–15% cost |

| Gross debt (Q4 2025) | CAD 5.2B; WAC ~3.9% |

What is included in the product

Tailored Porter’s Five Forces for RioCan, uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes, and strategic pressures shaping its retail-focused REIT profitability and growth prospects.

A concise Porter's Five Forces one-sheet for RioCan that highlights bargaining power, competitive rivalry, and regulatory risks—ideal for swift investment or strategy decisions.

Customers Bargaining Power

Concentration of Anchor National Tenants

Residential Tenant Rights and Regulatory Protection

As RioCan grows its residential holdings, tenants gain outsized bargaining power via provincial rules: Ontario’s 2023 rent control covers most units and the Tenant Protection Act caps annual increases (guideline 2.5% for 2024), constraining RioCan’s rent growth and lease changes; in 2024 Ontario eviction applications rose 8%, signaling stronger tenant enforcement. This regulatory tilt reduces landlord pricing flexibility and raises revenue predictability risks for RioCan.

Low Switching Costs for Small Retailers

SMEs in RioCan’s malls face low switching costs versus anchors, so roughly 60–70% of non-anchor retail leases (2024 RioCan data) show higher churn risk if rents rise; many can move to e-commerce or local pop-ups. This mobility pushed RioCan to increase tenant improvement allowances—reported up to $30–50 per sq ft in 2024—and to add amenities, keeping national vacancy for non-anchor units near 6% in 2024.

Demand for Flexible Lease Structures

Post-pandemic shifts push tenants toward shorter leases and turnover-based rent, and in 2024 about 28% of new retail leases in Canada included variable rent components, eroding RioCan’s income predictability.

Large chains leverage scale to demand concessions—RioCan noted increased tenant requests for flexibility across 2023–2025, raising rollover risk and vacancy management costs.

Top-tier tenants face many mall options, so bargaining power grows and RioCan must trade fixed cash flow for occupancy and tenant mix.

- ~28% variable rent in 2024 new leases

- Higher lease turnover risk

- Scale favors large tenants

Sophistication of Institutional Joint Venture Partners

Institutional joint-venture partners—often Canadian pension funds and insurers—are RioCan’s customers in major mixed-use projects and wield strong bargaining power by demanding transparency, specific IRR hurdles (commonly 8–12% real), and board-level influence over development and disposition decisions.

These partners bring large capital pools (individual commitments often $50m–$500m) and governance standards, forcing RioCan to accept tighter reporting, clawbacks, and staggered capital calls that compress RioCan’s decision latitude and margin capture.

Anchors Drive Power: 28% Rent, 96% Occupancy; JVs Seek 8–12% IRR

| Metric | 2024 |

|---|---|

| Anchor share of base rent | ~28% |

| Anchor occupancy | ~96% |

| Non-anchor vacancy | ~6% |

| New leases with variable rent | ~28% |

| JV IRR demand | 8–12% real |

Full Version Awaits

RioCan Porter's Five Forces Analysis

This preview shows the exact RioCan Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups; the full document is fully formatted, professionally written, and ready for download and use the moment you buy.