Republic National Distributing Company PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

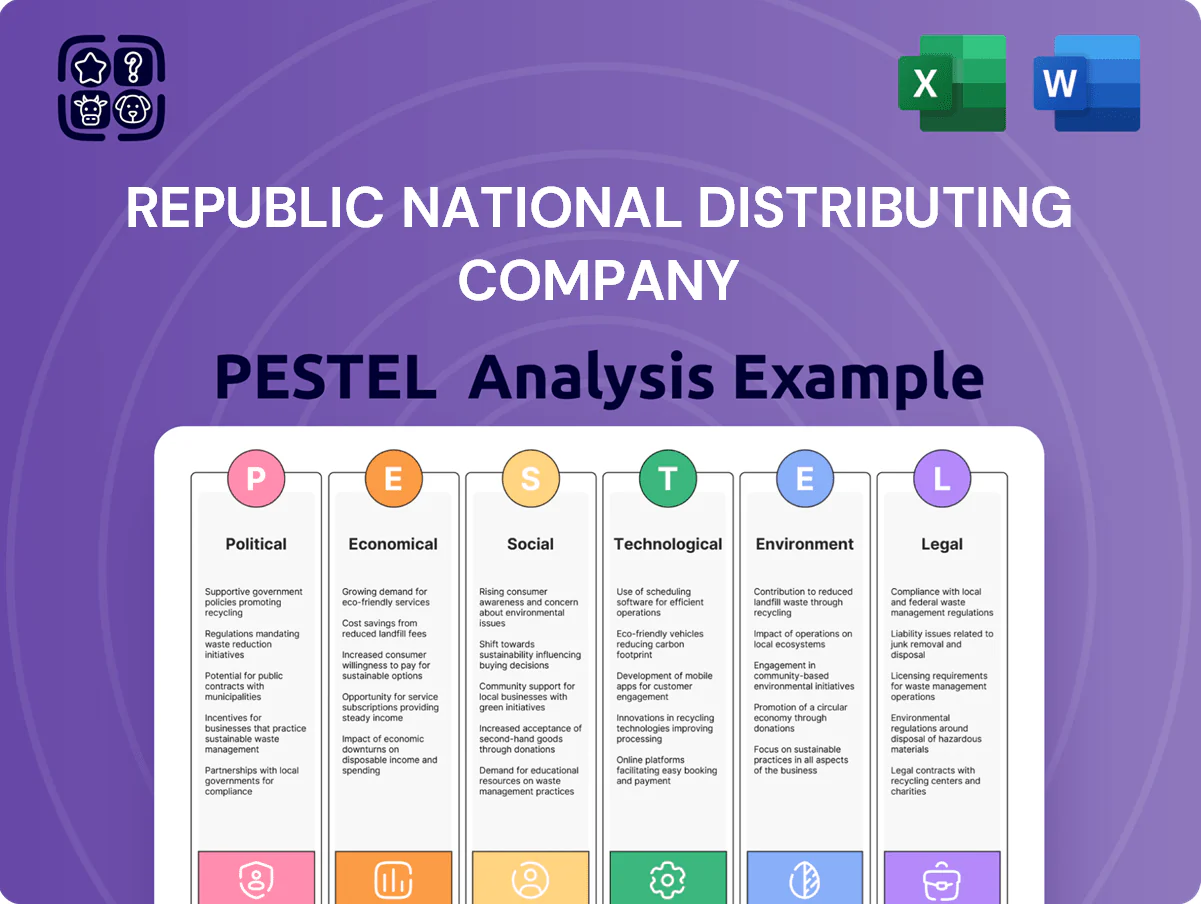

Gain strategic clarity with our PESTLE Analysis of Republic National Distributing Company—uncover how political, economic, social, technological, legal, and environmental forces shape its market position and risk profile; buy the full report to access deep-dive insights, ready-to-use data, and actionable recommendations for investors, consultants, and executives.

Political factors

Three-Tier System Support

RNDC operates within the entrenched three-tier system, backed by state lobbying that protected distributors holding roughly 70% of U.S. beverage alcohol wholesale volume in 2024; this political stability keeps distributors as the required middleman between producers and 230,000+ retailers nationwide. Shifts toward direct-to-consumer shipping—already a $3.5 billion segment in 2023 and growing—could materially disrupt RNDCs model and compress gross margins if legislatures loosen tier protections.

Trade Policy and Tariffs

International trade relations and tariffs on imported wines and spirits from the EU directly raise RNDC’s cost base—EU tariffs rose in retaliatory measures in 2023, adding up to 25% on certain spirits, squeezing margins on premium labels that represent ~30% of RNDC’s imported portfolio. Political shifts in 2024–25 created tariff volatility, forcing price adjustments that can cut gross margins by several percentage points; management must hedge supply chains and renegotiate terms to protect retail pricing and margin stability.

State Excise Tax Volatility

State excise tax volatility is acute as states raised alcohol excise rates to plug budget gaps—between 2020–2024, 18 states adjusted rates, with average hike ~6–8%, forcing RNDC to monitor each of its 46-state operating footprints for shifts that could cut volume; CPG studies show a 1% price increase can reduce alcohol demand 0.3–0.7%, implying material impact on margins and EBITDA. Political lobbying remains active: the beverage industry spent over $120m on federal and state lobbying in 2023–2024 to influence tax outcomes.

Interstate Commerce Regulations

Political debates over the commerce clause and state shipment restrictions shape RNDCs market dominance: after the 2018 South Dakota v. Wayfair decision, states collected $14.6B in remote sales taxes in 2023, prompting mixed state laws that both constrain out-of-state spirits sellers and protect RNDCs local networks.

Recent supreme court rulings and varied state responses create a patchwork of compliance costs—RNDC faces differing licensing, shipment and tax regimes across 50 states, affecting margins and logistics spending estimated at several percent of revenue (RNDC revenue: $18.5B in FY2024).

RNDC benefits when political alignment favors licensed in-state distributors over unrestricted national e-commerce spirits platforms, preserving its regional market share (top three U.S. distributors control roughly 70% of on-premise/off-premise distribution).

- Wayfair-era remote tax collection: $14.6B nationwide (2023)

- RNDC FY2024 revenue: $18.5B

- Top 3 distributors market share: ~70%

- State-by-state licensing raises compliance/logistics costs several percent of revenue

Alcohol Control Board Relations

In control states RNDC must maintain strong political ties and strict compliance with government-run alcohol agencies that set listing and pricing; roughly 17 US states retain control systems affecting about 25% of on‑premise alcohol sales (2024).

Political appointments to liquor boards can swiftly change which brands are allowed or favored, impacting revenue; a single listing change can alter distributor margins by several percentage points.

Active political engagement and lobbying help RNDC protect market access and influence administrative rulemaking that affects product flow and margins.

- ~17 control states; ~25% of on‑premise sales (2024)

- Board appointments can shift brand listings and margins

- Political engagement preserves market access and pricing influence

RNDC’s 70% grip vs. DTC surge and excise hikes threaten margins despite $18.5B revenue

RNDC’s dominance is protected by the three‑tier system and favorable state lobbying, preserving ~70% distributor market share in 2024, but DTC growth ($3.5B in 2023) and tariff volatility (EU duties up to 25% in 2023) threaten margins; state excise hikes (18 states 2020–24, avg +6–8%) and patchwork licensing/compliance raise costs against FY2024 revenue $18.5B.

| Metric | Value |

|---|---|

| FY2024 revenue | $18.5B |

| Top-3 distributor share | ~70% |

| DTC segment (2023) | $3.5B |

| States raised excise (2020–24) | 18 (avg +6–8%) |

| Control states | ~17 (25% on-premise sales) |

What is included in the product

Explores how macro-environmental factors uniquely affect Republic National Distributing Company across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors.

A concise PESTLE summary for Republic National Distributing Company that distills regulatory, economic, social, technological, legal, and environmental factors into an easily shareable slide or handout to streamline risk discussions and strategic planning.

Economic factors

Inflationary Pressure on Discretionary Income

Persistent inflation—U.S. CPI running near 3.4% annual in 2025—has curtailed discretionary spend, pushing consumers from premium spirits and luxury wines toward value labels, forcing RNDC to rebalance assortments to protect share.

RNDC must manage margin compression as high-margin on-premise sales slump while retail and e-commerce volumes rise; off-premise growth (up ~4–6% in 2024–25) favors lower-priced SKUs.

To retain price-sensitive shoppers RNDC blends premium offerings with expanded value portfolios and targeted promotions, mitigating revenue risks while preserving supplier relationships and gross margin dollars.

Interest Rate Impact on Inventory Financing

As a capital-intensive distributor, RNDC depends on credit lines to finance $3–5 billion in annual inventory; a 100 bp rise in US prime rates (2024 peak ~8.25% Fed funds) raises carrying costs materially, squeezing margins. Higher rates force focus on faster inventory turnover and lower DSI—RNDC targets industry DSI ~30–45 days to limit interest expense. Rising cost of capital in 2024–25 constrains funding for M&A and warehouse capex, increasing leverage sensitivity and refinancing risk.

Labor Market Dynamics and Costs

The logistics and warehousing sector saw average hourly wages rise 6.3% year-over-year in 2024, with driver shortages causing vacancy rates near 12%; RNDC must boost compensation and benefits to retain drivers and warehouse staff crucial to daily distribution. Increased labor costs—adding an estimated $40–60 million annually if RNDC raises wages to market—will compress margins unless offset by automation, route optimization, or passing roughly 2–3% price increases to retail customers.

Consolidation in the Retail Sector

Economic pressures are driving consolidation among retail giants and national restaurant chains, boosting buyer concentration; in the US the top 5 grocery chains now account for roughly 40% of market share and restaurant group rollups increased by 12% in 2024, raising RNDC customers’ bargaining power.

Large-scale buyers demand steeper discounts and tailored logistics—national accounts seek 5–10% better pricing and just-in-time delivery—compressing distributor margins and requiring RNDC to optimize cost-to-serve.

RNDC must exploit its own scale—>$14 billion revenue in 2024—and investments in tech and distribution to remain the preferred supplier for economically dominant retail partners.

- Top 5 grocery chains ~40% US share (2024)

- Restaurant rollups +12% (2024)

- RNDC revenue >$14B (2024)

- Buyers seek 5–10% better pricing

Fuel and Logistics Cost Volatility

Fluctuations in global energy prices raise RNDC’s delivery costs; U.S. diesel averaged about 4.10 USD/gal in 2024 versus 3.88 USD/gal in 2023, pressuring margins on its ~6,000-vehicle fleet.

Economic instability in oil markets forces RNDC to use fuel hedging and route optimization; effective hedging reduced volatility exposure for many distributors by ~15–25% in 2023–2024.

Sharp diesel spikes often trigger fuel surcharges, which risk pushback from retailers and can suppress same-store sales growth during high-cost months.

- Diesel avg 2024 ~4.10 USD/gal

- Fleet ~6,000 vehicles

- Hedging cuts volatility ~15–25%

- Fuel surcharges risk retailer resistance

RNDC must speed turns, cut costs as inflation, wages, diesel squeeze margins

Inflation and higher rates in 2024–25 compress margins as consumers shift to value SKUs; RNDC (revenue >$14B in 2024) must speed inventory turns (DSI target 30–45) and cut cost-to-serve amid buyer consolidation (top‑5 grocers ~40% share). Rising wages (+6.3% y/y logistics 2024) and diesel (~$4.10/gal 2024) increase operating costs; hedging/automation and selective price passes mitigate pressure.

| Metric | 2024–25 |

|---|---|

| RNDC revenue | >$14B |

| Top 5 grocers US | ~40% |

| Diesel avg | $4.10/gal |

| Logistics wage rise | +6.3% y/y |

| DSI target | 30–45 days |

Full Version Awaits

Republic National Distributing Company PESTLE Analysis

The preview shown here is the exact Republic National Distributing Company PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis of Republic National Distributing Company—uncover how political, economic, social, technological, legal, and environmental forces shape its market position and risk profile; buy the full report to access deep-dive insights, ready-to-use data, and actionable recommendations for investors, consultants, and executives.

Political factors

Three-Tier System Support

RNDC operates within the entrenched three-tier system, backed by state lobbying that protected distributors holding roughly 70% of U.S. beverage alcohol wholesale volume in 2024; this political stability keeps distributors as the required middleman between producers and 230,000+ retailers nationwide. Shifts toward direct-to-consumer shipping—already a $3.5 billion segment in 2023 and growing—could materially disrupt RNDCs model and compress gross margins if legislatures loosen tier protections.

Trade Policy and Tariffs

International trade relations and tariffs on imported wines and spirits from the EU directly raise RNDC’s cost base—EU tariffs rose in retaliatory measures in 2023, adding up to 25% on certain spirits, squeezing margins on premium labels that represent ~30% of RNDC’s imported portfolio. Political shifts in 2024–25 created tariff volatility, forcing price adjustments that can cut gross margins by several percentage points; management must hedge supply chains and renegotiate terms to protect retail pricing and margin stability.

State Excise Tax Volatility

State excise tax volatility is acute as states raised alcohol excise rates to plug budget gaps—between 2020–2024, 18 states adjusted rates, with average hike ~6–8%, forcing RNDC to monitor each of its 46-state operating footprints for shifts that could cut volume; CPG studies show a 1% price increase can reduce alcohol demand 0.3–0.7%, implying material impact on margins and EBITDA. Political lobbying remains active: the beverage industry spent over $120m on federal and state lobbying in 2023–2024 to influence tax outcomes.

Interstate Commerce Regulations

Political debates over the commerce clause and state shipment restrictions shape RNDCs market dominance: after the 2018 South Dakota v. Wayfair decision, states collected $14.6B in remote sales taxes in 2023, prompting mixed state laws that both constrain out-of-state spirits sellers and protect RNDCs local networks.

Recent supreme court rulings and varied state responses create a patchwork of compliance costs—RNDC faces differing licensing, shipment and tax regimes across 50 states, affecting margins and logistics spending estimated at several percent of revenue (RNDC revenue: $18.5B in FY2024).

RNDC benefits when political alignment favors licensed in-state distributors over unrestricted national e-commerce spirits platforms, preserving its regional market share (top three U.S. distributors control roughly 70% of on-premise/off-premise distribution).

- Wayfair-era remote tax collection: $14.6B nationwide (2023)

- RNDC FY2024 revenue: $18.5B

- Top 3 distributors market share: ~70%

- State-by-state licensing raises compliance/logistics costs several percent of revenue

Alcohol Control Board Relations

In control states RNDC must maintain strong political ties and strict compliance with government-run alcohol agencies that set listing and pricing; roughly 17 US states retain control systems affecting about 25% of on‑premise alcohol sales (2024).

Political appointments to liquor boards can swiftly change which brands are allowed or favored, impacting revenue; a single listing change can alter distributor margins by several percentage points.

Active political engagement and lobbying help RNDC protect market access and influence administrative rulemaking that affects product flow and margins.

- ~17 control states; ~25% of on‑premise sales (2024)

- Board appointments can shift brand listings and margins

- Political engagement preserves market access and pricing influence

RNDC’s 70% grip vs. DTC surge and excise hikes threaten margins despite $18.5B revenue

RNDC’s dominance is protected by the three‑tier system and favorable state lobbying, preserving ~70% distributor market share in 2024, but DTC growth ($3.5B in 2023) and tariff volatility (EU duties up to 25% in 2023) threaten margins; state excise hikes (18 states 2020–24, avg +6–8%) and patchwork licensing/compliance raise costs against FY2024 revenue $18.5B.

| Metric | Value |

|---|---|

| FY2024 revenue | $18.5B |

| Top-3 distributor share | ~70% |

| DTC segment (2023) | $3.5B |

| States raised excise (2020–24) | 18 (avg +6–8%) |

| Control states | ~17 (25% on-premise sales) |

What is included in the product

Explores how macro-environmental factors uniquely affect Republic National Distributing Company across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific regulatory context to identify threats and opportunities for executives and investors.

A concise PESTLE summary for Republic National Distributing Company that distills regulatory, economic, social, technological, legal, and environmental factors into an easily shareable slide or handout to streamline risk discussions and strategic planning.

Economic factors

Inflationary Pressure on Discretionary Income

Persistent inflation—U.S. CPI running near 3.4% annual in 2025—has curtailed discretionary spend, pushing consumers from premium spirits and luxury wines toward value labels, forcing RNDC to rebalance assortments to protect share.

RNDC must manage margin compression as high-margin on-premise sales slump while retail and e-commerce volumes rise; off-premise growth (up ~4–6% in 2024–25) favors lower-priced SKUs.

To retain price-sensitive shoppers RNDC blends premium offerings with expanded value portfolios and targeted promotions, mitigating revenue risks while preserving supplier relationships and gross margin dollars.

Interest Rate Impact on Inventory Financing

As a capital-intensive distributor, RNDC depends on credit lines to finance $3–5 billion in annual inventory; a 100 bp rise in US prime rates (2024 peak ~8.25% Fed funds) raises carrying costs materially, squeezing margins. Higher rates force focus on faster inventory turnover and lower DSI—RNDC targets industry DSI ~30–45 days to limit interest expense. Rising cost of capital in 2024–25 constrains funding for M&A and warehouse capex, increasing leverage sensitivity and refinancing risk.

Labor Market Dynamics and Costs

The logistics and warehousing sector saw average hourly wages rise 6.3% year-over-year in 2024, with driver shortages causing vacancy rates near 12%; RNDC must boost compensation and benefits to retain drivers and warehouse staff crucial to daily distribution. Increased labor costs—adding an estimated $40–60 million annually if RNDC raises wages to market—will compress margins unless offset by automation, route optimization, or passing roughly 2–3% price increases to retail customers.

Consolidation in the Retail Sector

Economic pressures are driving consolidation among retail giants and national restaurant chains, boosting buyer concentration; in the US the top 5 grocery chains now account for roughly 40% of market share and restaurant group rollups increased by 12% in 2024, raising RNDC customers’ bargaining power.

Large-scale buyers demand steeper discounts and tailored logistics—national accounts seek 5–10% better pricing and just-in-time delivery—compressing distributor margins and requiring RNDC to optimize cost-to-serve.

RNDC must exploit its own scale—>$14 billion revenue in 2024—and investments in tech and distribution to remain the preferred supplier for economically dominant retail partners.

- Top 5 grocery chains ~40% US share (2024)

- Restaurant rollups +12% (2024)

- RNDC revenue >$14B (2024)

- Buyers seek 5–10% better pricing

Fuel and Logistics Cost Volatility

Fluctuations in global energy prices raise RNDC’s delivery costs; U.S. diesel averaged about 4.10 USD/gal in 2024 versus 3.88 USD/gal in 2023, pressuring margins on its ~6,000-vehicle fleet.

Economic instability in oil markets forces RNDC to use fuel hedging and route optimization; effective hedging reduced volatility exposure for many distributors by ~15–25% in 2023–2024.

Sharp diesel spikes often trigger fuel surcharges, which risk pushback from retailers and can suppress same-store sales growth during high-cost months.

- Diesel avg 2024 ~4.10 USD/gal

- Fleet ~6,000 vehicles

- Hedging cuts volatility ~15–25%

- Fuel surcharges risk retailer resistance

RNDC must speed turns, cut costs as inflation, wages, diesel squeeze margins

Inflation and higher rates in 2024–25 compress margins as consumers shift to value SKUs; RNDC (revenue >$14B in 2024) must speed inventory turns (DSI target 30–45) and cut cost-to-serve amid buyer consolidation (top‑5 grocers ~40% share). Rising wages (+6.3% y/y logistics 2024) and diesel (~$4.10/gal 2024) increase operating costs; hedging/automation and selective price passes mitigate pressure.

| Metric | 2024–25 |

|---|---|

| RNDC revenue | >$14B |

| Top 5 grocers US | ~40% |

| Diesel avg | $4.10/gal |

| Logistics wage rise | +6.3% y/y |

| DSI target | 30–45 days |

Full Version Awaits

Republic National Distributing Company PESTLE Analysis

The preview shown here is the exact Republic National Distributing Company PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use without placeholders or edits.