Roche Porter's Five Forces Analysis

From Overview to Strategy Blueprint

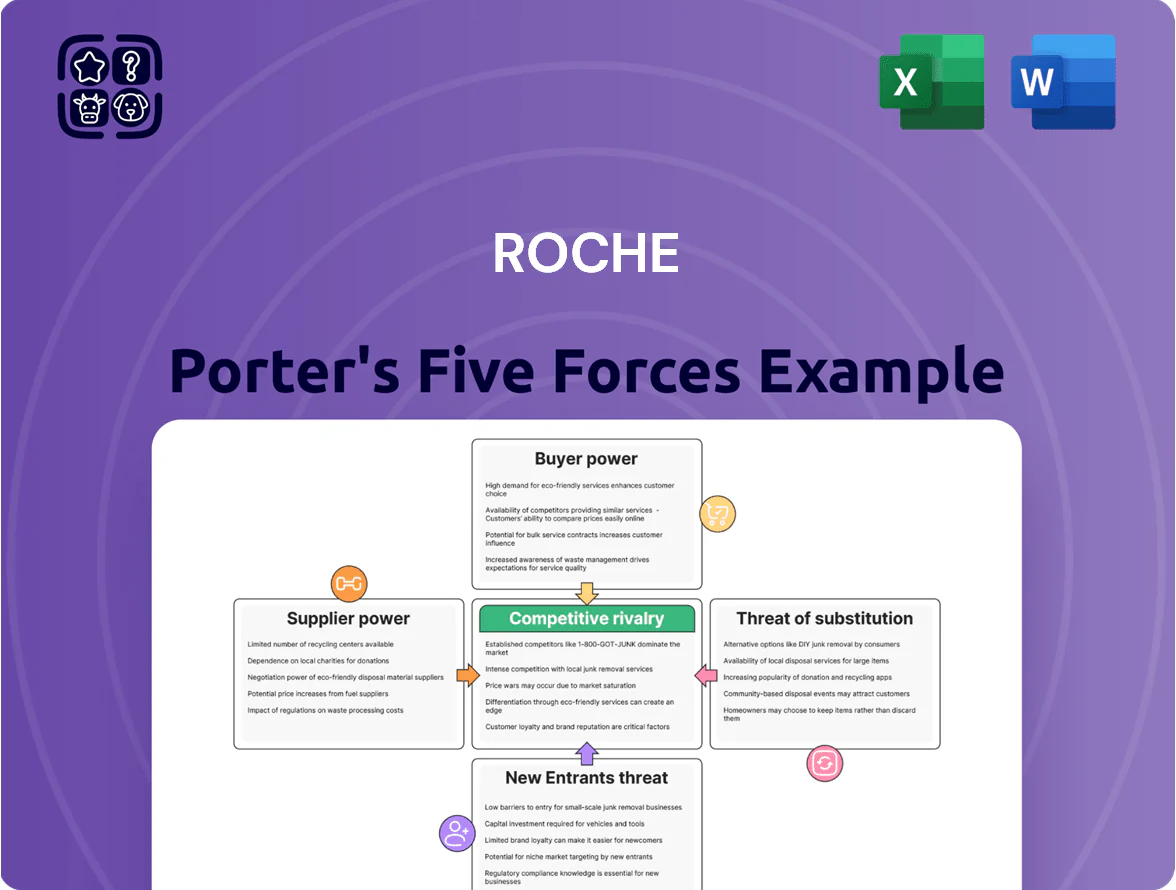

Roche faces strong buyer scrutiny, high supplier complexity, and intense rivalry driven by innovation and patent cliffs, while regulatory hurdles and moderate threats from new biologics shape its competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Roche’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

Roche depends on scarce biologics and GMP-grade chemicals for oncology and immunology drugs; around 60–70% of these inputs come from a handful of certified suppliers, driving supplier leverage on pricing and lead times. In 2024 Roche reported supply-chain constraints that delayed some drug launches and raised COGS by ~2.1 percentage points, showing how niche dependency can affect margins and timelines.

High Switching Costs for Biologics

Switching biologics suppliers triggers costly regulatory re-validation and batch comparability studies—often taking 12–24 months and costing $5–20M per product—so Roche rarely swaps partners, which strengthens incumbent suppliers.

High switching costs push Roche toward multi-year contracts; in 2024 Roche reported over 60% of COGS tied to long-term supplier agreements, lowering price risk and securing capacity for high-margin biologics.

Consolidation of Contract Research Organizations

The pharmaceutical industry now depends on a handful of large contract research organizations (CROs); the top 10 CROs captured about 68% of global clinical trial spending in 2024, per industry estimates. As CROs consolidate through deals like Thermo Fisher’s 2021 LabCorp buyout and Parexel’s private equity moves, their bargaining power versus Roche rises. Roche must negotiate sharply to secure access to specialized trial sites and biostatistics teams, or face 5–10% higher trial costs and longer timelines. This raises strategic risk to pipeline timing and R&D margins.

Global Supply Chain Diversification

Roche reduces supplier bargaining power by diversifying sourcing across regions—in 2024 over 40% of procurement spend was split across Europe, North America, and Asia, lowering single-territory exposure.

Keeping many vendors for non-critical parts creates redundancy so localized shocks (eg, 2023 Taiwan port delays) don’t halt production; this trims supplier leverage and shortens recovery time.

- 2024 procurement: >40% geographically diversified

- Multiple vendors for non-critical components

- Redundancy limits single-supplier disruption

Integration of Diagnostic Component Manufacturing

Roche’s diagnostics division has vertically integrated reagent and hardware production, cutting supplier reliance and lowering supplier bargaining power; in 2024 Roche Diagnostics reported ~CHF 18.6 billion revenue, helping absorb upstream costs and protect margins.

Owning key components ensures steady input supply for platforms like Cobas and Accu‑Chek, reducing supply disruption risk and improving gross margins versus peers who outsource.

- 2024 Diagnostics revenue: CHF 18.6bn

- Vertical integration lowers supplier dependence

- Improves input security for Cobas/Accu‑Chek

- Supports margin protection versus outsourced peers

Roche Faces Supplier Leverage Despite Diagnostics Scale and Diversified Procurement

Suppliers hold moderate-to-high power: 60–70% of GMP biologics from few certified vendors; 2024 supply issues raised COGS ~2.1ppt and delayed launches. Switching costs (12–24 months, $5–20M) keep Roche tied to incumbents; Diagnostics vertical integration (2024 revenue CHF 18.6bn) and >40% geographically diversified procurement cut supplier leverage.

| Metric | 2024 |

|---|---|

| GMP supplier concentration | 60–70% |

| COGS impact (supply issues) | +2.1 ppt |

| Switch cost per product | $5–20M |

| Diagnostics revenue | CHF 18.6bn |

| Procurement geographic split | >40% |

What is included in the product

Tailored Porter's Five Forces analysis for Roche uncovering competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and strategic barriers protecting its market position—ideal for investor reports, strategy decks, and academic use.

Concise Porter's Five Forces summary for Roche—quickly spot competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

Centralized Government Procurement and Payers

National health systems and big insurers are Roche’s main buyers for high-cost drugs; in 2024 public payers accounted for roughly 60% of global pharma spending, giving them huge leverage.

These buyers use volume to extract steep discounts and outcome-based rebates—procurement contracts often cut list prices by 20–40% in EU markets in 2023–24.

With global healthcare spending growth slowing to ~3.8% in 2024 and median payer cost-effectiveness thresholds tightening, Roche faces rising demand to prove value per QALY and accept risk-sharing deals.

Influence of Pharmacy Benefit Managers

In the US, pharmacy benefit managers (PBMs) control formularies for ~70% of commercially insured lives, giving them power to exclude or place Roche drugs in high-cost tiers and sharply reduce volumes.

PBM leverage forces Roche to offer steep rebates—industry median rebates hit ~30% in 2024—plus robust Phase III evidence to secure preferred placement.

Loss of formulary access can cut peak sales by 40–60% for specific oncology and immunology therapies, so Roche must price competitively and show real-world outcomes to keep access.

Shift Toward Value-Based Pricing Models

The global move to value-based pricing—estimated at a 12% annual adoption rate in OECD markets by 2024—means payers increasingly reimburse for outcomes, not volume, directly boosting customer leverage over Roche’s oncology and rare-disease drugs; Roche must therefore tie prices to survival, response rates, or patient-reported outcomes. To support these contracts Roche needs major analytics spend—roughly $500–700m annually in real-world evidence and data platforms by 2025—to validate performance-linked pricing.

Consolidation of Diagnostic Laboratory Chains

Consolidation of diagnostic lab chains (eg, Labcorp, Quest Diagnostics) concentrates buying power: the top 5 US lab chains handle ~60% of outpatient tests, letting them push for 5–15% price concessions on instruments and high-volume reagents in 2024–25.

Roche faces pressure to offer integrated, high-throughput platforms and service bundles; losing scale discounts risks volume shrinkage as chains negotiate multi-vendor tenders.

- Top 5 chains ≈60% outpatient test share

- Price concessions commonly 5–15%

- Demand for integrated platforms up since 2023

Patient Advocacy and Informed Decision Making

Patient advocacy groups now guide treatment priorities; 68% of EU health tech coverage decisions in 2023 cited patient input, shifting demand toward patient-centered Roche offerings.

These groups influence policy and pricing—public campaigns helped secure higher reimbursement in 2022 oncology cases, changing Roche’s market-access tactics and launch sequencing.

Roche must engage advocacy stakeholders to protect reputation and align R&D with needs; patient-led trials rose 22% globally in 2024, showing the trend.

- 68% EU coverage decisions cited patient input (2023)

- Oncology reimbursement wins tied to advocacy (2022)

- Patient-led trials +22% globally (2024)

Payers, PBMs & labs squeeze Roche: 20–40% discounts, ~30% rebates; formulary loss cuts sales 40–60%

Large public payers and PBMs wield strong leverage over Roche, extracting 20–40% discounts and ~30% rebates in 2024 and pushing outcome-based contracts as value thresholds tighten; loss of formulary access can cut peak sales 40–60%. Consolidated lab chains (top 5 ≈60% outpatient share) demand 5–15% concessions on instruments/reagents, while patient advocacy now influences coverage (68% EU decisions in 2023).

| Metric | 2023–24 Value |

|---|---|

| Payer share of pharma spend (public) | ~60% |

| Typical EU procurement discounts | 20–40% |

| Industry median rebates (2024) | ~30% |

| Formulary loss sales impact | 40–60% |

| Top 5 US lab outpatient share | ~60% |

| Lab price concessions | 5–15% |

| EU coverage decisions citing patients (2023) | 68% |

Preview the Actual Deliverable

Roche Porter's Five Forces Analysis

This preview shows the exact Roche Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

You're viewing the complete, final document: the same deliverable will be available for instant access post-purchase and requires no further setup or customization.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Roche faces strong buyer scrutiny, high supplier complexity, and intense rivalry driven by innovation and patent cliffs, while regulatory hurdles and moderate threats from new biologics shape its competitive landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Roche’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Requirements

Roche depends on scarce biologics and GMP-grade chemicals for oncology and immunology drugs; around 60–70% of these inputs come from a handful of certified suppliers, driving supplier leverage on pricing and lead times. In 2024 Roche reported supply-chain constraints that delayed some drug launches and raised COGS by ~2.1 percentage points, showing how niche dependency can affect margins and timelines.

High Switching Costs for Biologics

Switching biologics suppliers triggers costly regulatory re-validation and batch comparability studies—often taking 12–24 months and costing $5–20M per product—so Roche rarely swaps partners, which strengthens incumbent suppliers.

High switching costs push Roche toward multi-year contracts; in 2024 Roche reported over 60% of COGS tied to long-term supplier agreements, lowering price risk and securing capacity for high-margin biologics.

Consolidation of Contract Research Organizations

The pharmaceutical industry now depends on a handful of large contract research organizations (CROs); the top 10 CROs captured about 68% of global clinical trial spending in 2024, per industry estimates. As CROs consolidate through deals like Thermo Fisher’s 2021 LabCorp buyout and Parexel’s private equity moves, their bargaining power versus Roche rises. Roche must negotiate sharply to secure access to specialized trial sites and biostatistics teams, or face 5–10% higher trial costs and longer timelines. This raises strategic risk to pipeline timing and R&D margins.

Global Supply Chain Diversification

Roche reduces supplier bargaining power by diversifying sourcing across regions—in 2024 over 40% of procurement spend was split across Europe, North America, and Asia, lowering single-territory exposure.

Keeping many vendors for non-critical parts creates redundancy so localized shocks (eg, 2023 Taiwan port delays) don’t halt production; this trims supplier leverage and shortens recovery time.

- 2024 procurement: >40% geographically diversified

- Multiple vendors for non-critical components

- Redundancy limits single-supplier disruption

Integration of Diagnostic Component Manufacturing

Roche’s diagnostics division has vertically integrated reagent and hardware production, cutting supplier reliance and lowering supplier bargaining power; in 2024 Roche Diagnostics reported ~CHF 18.6 billion revenue, helping absorb upstream costs and protect margins.

Owning key components ensures steady input supply for platforms like Cobas and Accu‑Chek, reducing supply disruption risk and improving gross margins versus peers who outsource.

- 2024 Diagnostics revenue: CHF 18.6bn

- Vertical integration lowers supplier dependence

- Improves input security for Cobas/Accu‑Chek

- Supports margin protection versus outsourced peers

Roche Faces Supplier Leverage Despite Diagnostics Scale and Diversified Procurement

Suppliers hold moderate-to-high power: 60–70% of GMP biologics from few certified vendors; 2024 supply issues raised COGS ~2.1ppt and delayed launches. Switching costs (12–24 months, $5–20M) keep Roche tied to incumbents; Diagnostics vertical integration (2024 revenue CHF 18.6bn) and >40% geographically diversified procurement cut supplier leverage.

| Metric | 2024 |

|---|---|

| GMP supplier concentration | 60–70% |

| COGS impact (supply issues) | +2.1 ppt |

| Switch cost per product | $5–20M |

| Diagnostics revenue | CHF 18.6bn |

| Procurement geographic split | >40% |

What is included in the product

Tailored Porter's Five Forces analysis for Roche uncovering competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and strategic barriers protecting its market position—ideal for investor reports, strategy decks, and academic use.

Concise Porter's Five Forces summary for Roche—quickly spot competitive threats and bargaining pressures to streamline strategic decisions.

Customers Bargaining Power

Centralized Government Procurement and Payers

National health systems and big insurers are Roche’s main buyers for high-cost drugs; in 2024 public payers accounted for roughly 60% of global pharma spending, giving them huge leverage.

These buyers use volume to extract steep discounts and outcome-based rebates—procurement contracts often cut list prices by 20–40% in EU markets in 2023–24.

With global healthcare spending growth slowing to ~3.8% in 2024 and median payer cost-effectiveness thresholds tightening, Roche faces rising demand to prove value per QALY and accept risk-sharing deals.

Influence of Pharmacy Benefit Managers

In the US, pharmacy benefit managers (PBMs) control formularies for ~70% of commercially insured lives, giving them power to exclude or place Roche drugs in high-cost tiers and sharply reduce volumes.

PBM leverage forces Roche to offer steep rebates—industry median rebates hit ~30% in 2024—plus robust Phase III evidence to secure preferred placement.

Loss of formulary access can cut peak sales by 40–60% for specific oncology and immunology therapies, so Roche must price competitively and show real-world outcomes to keep access.

Shift Toward Value-Based Pricing Models

The global move to value-based pricing—estimated at a 12% annual adoption rate in OECD markets by 2024—means payers increasingly reimburse for outcomes, not volume, directly boosting customer leverage over Roche’s oncology and rare-disease drugs; Roche must therefore tie prices to survival, response rates, or patient-reported outcomes. To support these contracts Roche needs major analytics spend—roughly $500–700m annually in real-world evidence and data platforms by 2025—to validate performance-linked pricing.

Consolidation of Diagnostic Laboratory Chains

Consolidation of diagnostic lab chains (eg, Labcorp, Quest Diagnostics) concentrates buying power: the top 5 US lab chains handle ~60% of outpatient tests, letting them push for 5–15% price concessions on instruments and high-volume reagents in 2024–25.

Roche faces pressure to offer integrated, high-throughput platforms and service bundles; losing scale discounts risks volume shrinkage as chains negotiate multi-vendor tenders.

- Top 5 chains ≈60% outpatient test share

- Price concessions commonly 5–15%

- Demand for integrated platforms up since 2023

Patient Advocacy and Informed Decision Making

Patient advocacy groups now guide treatment priorities; 68% of EU health tech coverage decisions in 2023 cited patient input, shifting demand toward patient-centered Roche offerings.

These groups influence policy and pricing—public campaigns helped secure higher reimbursement in 2022 oncology cases, changing Roche’s market-access tactics and launch sequencing.

Roche must engage advocacy stakeholders to protect reputation and align R&D with needs; patient-led trials rose 22% globally in 2024, showing the trend.

- 68% EU coverage decisions cited patient input (2023)

- Oncology reimbursement wins tied to advocacy (2022)

- Patient-led trials +22% globally (2024)

Payers, PBMs & labs squeeze Roche: 20–40% discounts, ~30% rebates; formulary loss cuts sales 40–60%

Large public payers and PBMs wield strong leverage over Roche, extracting 20–40% discounts and ~30% rebates in 2024 and pushing outcome-based contracts as value thresholds tighten; loss of formulary access can cut peak sales 40–60%. Consolidated lab chains (top 5 ≈60% outpatient share) demand 5–15% concessions on instruments/reagents, while patient advocacy now influences coverage (68% EU decisions in 2023).

| Metric | 2023–24 Value |

|---|---|

| Payer share of pharma spend (public) | ~60% |

| Typical EU procurement discounts | 20–40% |

| Industry median rebates (2024) | ~30% |

| Formulary loss sales impact | 40–60% |

| Top 5 US lab outpatient share | ~60% |

| Lab price concessions | 5–15% |

| EU coverage decisions citing patients (2023) | 68% |

Preview the Actual Deliverable

Roche Porter's Five Forces Analysis

This preview shows the exact Roche Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or mockups.

You're viewing the complete, final document: the same deliverable will be available for instant access post-purchase and requires no further setup or customization.