Rocket Internet Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

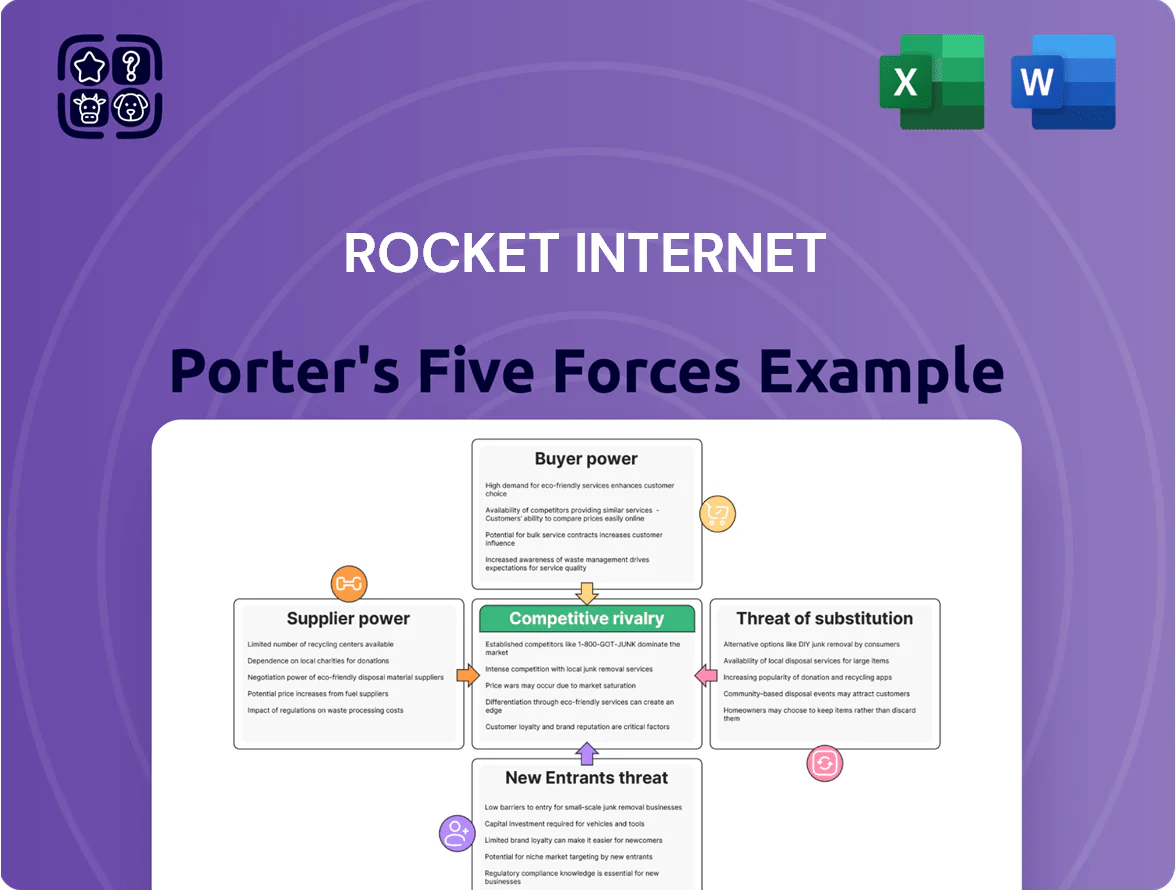

Rocket Internet faces intense rivalry as it scales fast across markets, while moderate supplier leverage and evolving buyer expectations shape pricing power; digital substitutes and new tech entrants add pressure on margins and growth prospects. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Rocket Internet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Tech Talent

The demand for senior software engineers and product managers stayed high through 2025, with global vacancy rates for software roles up 12% year‑over‑year and median FAANG-level base salaries in Europe reaching €130k in 2024; Rocket Internet’s need for elite talent across 30+ portfolio startups boosts supplier leverage.

Cloud Infrastructure Providers

Major cloud providers—Amazon Web Services (AWS) and Microsoft Azure—control about 62% of global IaaS/PaaS market in 2024 (Synergy Research), giving them strong supplier leverage over Rocket Internet ventures.

High switching costs—data egress fees often >0.09 USD/GB and multi-month migration projects—lock startups into existing architectures and raise operational risk.

As a result, Rocket Internet must largely accept pricing, SLAs, and contract terms set by these global infrastructure giants, limiting negotiation scope.

Financial Capital Markets

As an investment-heavy group, Rocket Internet depends on institutional capital and bank credit; in 2025 European corporate loan yields averaged ~4.1% and venture funding deal count fell 22% YoY, raising financing costs and selectivity for lenders.

Capital providers gained leverage via rate volatility and stricter due diligence—banks tightened covenant terms and VCs pushed later-stage milestones—so Rocket must show ARR growth, 30%+ EBITDA margin paths, or strong unit economics to secure liquidity.

Third Party Logistics

For e-commerce and marketplace ventures, Rocket Internet relies on local and international third-party logistics (3PL) to fulfill orders; in 2024, last-mile costs rose ~12% in emerging markets, squeezing margins for logistics-heavy portfolios.

In underserved regions with weak infrastructure, 3PLs gain bargaining power since few reliable alternatives exist; a single carrier disruption can add 3–7 percentage points to unit delivery cost and delay revenue recognition.

Price hikes or service failures from 3PLs directly hit operating margins—Rocket-style startups with thin gross margins (often 15–25%) see profit volatility when logistics costs jump unexpectedly.

- 3PL dependence higher in emerging markets

- Last-mile costs up ~12% (2024)

- Disruptions add 3–7 pp to delivery cost

- Gross margins typically 15–25%

Proprietary Data Sources

The effectiveness of Rocket Internet’s fintech and marketing ventures depends on high-quality consumer and credit-scoring data; in 2024, third-party credit bureaus and data vendors saw average license fee increases of 8–12%, raising costs for data-driven startups.

Suppliers can restrict access or raise fees, impairing risk pricing and customer targeting; without proprietary data, default-rate models and CAC estimates for new regions become significantly less reliable.

Supplier power squeezes Rocket Internet: cloud, talent, logistics, data and capital risks

Suppliers (cloud, talent, 3PL, data, capital) hold strong leverage over Rocket Internet: AWS/Azure 62% IaaS share (2024), FAANG‑level EU median senior pay €130k (2024), last‑mile costs +12% (2024), venture deal count −22% YoY (2025), European corporate loan yields ~4.1% (2025); switching costs, limited local 3PLs, and data‑access fees (+~10%) constrain pricing and raise operating risk.

| Supplier | Key metric |

|---|---|

| Cloud | AWS/Azure 62% (2024) |

| Talent | Senior median €130k (EU, 2024) |

| Logistics | Last‑mile +12% (2024) |

| Capital | Loan yields ~4.1% (EU, 2025) |

| Data | Fees +10% (2024) |

What is included in the product

Concise Porter's Five Forces assessment tailored to Rocket Internet, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic levers to protect market share and guide investor or management decisions.

A concise Rocket Internet Porter’s Five Forces snapshot—accelerates strategic decisions by highlighting competitive intensity and investment risks at a glance.

Customers Bargaining Power

Price Sensitive Consumers

In emerging markets where Rocket Internet operates, low brand loyalty and high price sensitivity mean many users switch for small discounts; McKinsey found 62% of Southeast Asian shoppers prioritized price in 2023. This drives ventures into frequent promotions—GMV-driving flash sales and 10–30% discounting—that compress margins. In 2024, regional price wars pushed average take-rates down ~3–5 percentage points for several Rocket-backed marketplaces, forcing heavy marketing spend to retain users.

Institutional Exit Buyers

Rocket Internet relies on institutional exit buyers—strategic acquirers and public markets—to monetize mature startups; in 2024-25 global M&A deal value fell ~18% to $3.9 trillion, raising buyer leverage. These buyers assess long-term unit economics and EBITDA margins, and if IPO windows tighten or deal pipelines slow, acquirers can insist on discounts; average acquisition multiples for tech firms slid from ~6.8x EV/EBITDA in 2021 to ~5.2x in 2024, cutting exit proceeds materially.

Low Switching Costs

The digital nature of Rocket Internet’s services gives customers very low switching costs: users can download rival apps in seconds, so retention hinges on experience and price. In 2024 global app uninstall rates averaged 28% within 30 days, so Rocket must keep monthly active users high to avoid churn. Low switching power forces Rocket to invest in product updates, discounts, and loyalty—every 1% drop in MAU can cut revenue noticeably in thin-margin markets.

Access to Information

By late 2025, price comparison tools and online reviews raised transparency: 72% of EU shoppers used comparison sites and 68% trusted peer reviews when choosing marketplaces, limiting information asymmetry for Rocket Internet ventures.

Customers now match prices and service levels across platforms in minutes, forcing Rocket Internet to compete on thin margins or invest in differentiation and loyalty programs.

This trend reduced average gross margins in digital marketplaces by ~150–300 basis points in 2023–25 versus 2018–20 benchmarks, squeezing unprotected offerings.

- 72% EU shoppers used comparison sites (2025)

- 68% trust peer reviews (2025)

- Margins down ~150–300 bps (2023–25)

Alternative Investment Options

Shareholders face many alternative tech investments—global tech ETFs held $420bn in 2024 and VC funds raised €58bn in Europe in 2024—so Rocket Internet SE must outpace those returns or risk capital flight.

If Rocket Internet underperforms peer VCs or ETFs, investors can quickly reallocate, giving them bargaining power to demand strategic changes or leadership shifts.

- Tech ETFs: $420bn AUM (2024)

- European VC raises: €58bn (2024)

- Investor mobility increases governance pressure

Price-savvy customers force 10–30% discounts, shaving take-rates 3–5ppt and margins

Customers have high bargaining power: low loyalty, low switching costs, and price transparency force Rocket Internet ventures into 10–30% discounting and heavy promotions, cutting take-rates ~3–5 ppt in 2024 and gross margins ~150–300 bps (2023–25). Key stats: 62% price-first shoppers SEA (2023), 72% EU comparison-site use (2025), app 30-day uninstall 28% (2024).

| Metric | Value |

|---|---|

| SEA price-first | 62% (2023) |

| EU comparison use | 72% (2025) |

| Take-rate drop | 3–5 ppt (2024) |

Preview the Actual Deliverable

Rocket Internet Porter's Five Forces Analysis

This preview shows the exact Rocket Internet Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written deliverable; once payment is complete, you’ll get instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Rocket Internet faces intense rivalry as it scales fast across markets, while moderate supplier leverage and evolving buyer expectations shape pricing power; digital substitutes and new tech entrants add pressure on margins and growth prospects. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Rocket Internet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Tech Talent

The demand for senior software engineers and product managers stayed high through 2025, with global vacancy rates for software roles up 12% year‑over‑year and median FAANG-level base salaries in Europe reaching €130k in 2024; Rocket Internet’s need for elite talent across 30+ portfolio startups boosts supplier leverage.

Cloud Infrastructure Providers

Major cloud providers—Amazon Web Services (AWS) and Microsoft Azure—control about 62% of global IaaS/PaaS market in 2024 (Synergy Research), giving them strong supplier leverage over Rocket Internet ventures.

High switching costs—data egress fees often >0.09 USD/GB and multi-month migration projects—lock startups into existing architectures and raise operational risk.

As a result, Rocket Internet must largely accept pricing, SLAs, and contract terms set by these global infrastructure giants, limiting negotiation scope.

Financial Capital Markets

As an investment-heavy group, Rocket Internet depends on institutional capital and bank credit; in 2025 European corporate loan yields averaged ~4.1% and venture funding deal count fell 22% YoY, raising financing costs and selectivity for lenders.

Capital providers gained leverage via rate volatility and stricter due diligence—banks tightened covenant terms and VCs pushed later-stage milestones—so Rocket must show ARR growth, 30%+ EBITDA margin paths, or strong unit economics to secure liquidity.

Third Party Logistics

For e-commerce and marketplace ventures, Rocket Internet relies on local and international third-party logistics (3PL) to fulfill orders; in 2024, last-mile costs rose ~12% in emerging markets, squeezing margins for logistics-heavy portfolios.

In underserved regions with weak infrastructure, 3PLs gain bargaining power since few reliable alternatives exist; a single carrier disruption can add 3–7 percentage points to unit delivery cost and delay revenue recognition.

Price hikes or service failures from 3PLs directly hit operating margins—Rocket-style startups with thin gross margins (often 15–25%) see profit volatility when logistics costs jump unexpectedly.

- 3PL dependence higher in emerging markets

- Last-mile costs up ~12% (2024)

- Disruptions add 3–7 pp to delivery cost

- Gross margins typically 15–25%

Proprietary Data Sources

The effectiveness of Rocket Internet’s fintech and marketing ventures depends on high-quality consumer and credit-scoring data; in 2024, third-party credit bureaus and data vendors saw average license fee increases of 8–12%, raising costs for data-driven startups.

Suppliers can restrict access or raise fees, impairing risk pricing and customer targeting; without proprietary data, default-rate models and CAC estimates for new regions become significantly less reliable.

Supplier power squeezes Rocket Internet: cloud, talent, logistics, data and capital risks

Suppliers (cloud, talent, 3PL, data, capital) hold strong leverage over Rocket Internet: AWS/Azure 62% IaaS share (2024), FAANG‑level EU median senior pay €130k (2024), last‑mile costs +12% (2024), venture deal count −22% YoY (2025), European corporate loan yields ~4.1% (2025); switching costs, limited local 3PLs, and data‑access fees (+~10%) constrain pricing and raise operating risk.

| Supplier | Key metric |

|---|---|

| Cloud | AWS/Azure 62% (2024) |

| Talent | Senior median €130k (EU, 2024) |

| Logistics | Last‑mile +12% (2024) |

| Capital | Loan yields ~4.1% (EU, 2025) |

| Data | Fees +10% (2024) |

What is included in the product

Concise Porter's Five Forces assessment tailored to Rocket Internet, revealing competitive intensity, buyer/supplier leverage, entry barriers, substitute threats, and strategic levers to protect market share and guide investor or management decisions.

A concise Rocket Internet Porter’s Five Forces snapshot—accelerates strategic decisions by highlighting competitive intensity and investment risks at a glance.

Customers Bargaining Power

Price Sensitive Consumers

In emerging markets where Rocket Internet operates, low brand loyalty and high price sensitivity mean many users switch for small discounts; McKinsey found 62% of Southeast Asian shoppers prioritized price in 2023. This drives ventures into frequent promotions—GMV-driving flash sales and 10–30% discounting—that compress margins. In 2024, regional price wars pushed average take-rates down ~3–5 percentage points for several Rocket-backed marketplaces, forcing heavy marketing spend to retain users.

Institutional Exit Buyers

Rocket Internet relies on institutional exit buyers—strategic acquirers and public markets—to monetize mature startups; in 2024-25 global M&A deal value fell ~18% to $3.9 trillion, raising buyer leverage. These buyers assess long-term unit economics and EBITDA margins, and if IPO windows tighten or deal pipelines slow, acquirers can insist on discounts; average acquisition multiples for tech firms slid from ~6.8x EV/EBITDA in 2021 to ~5.2x in 2024, cutting exit proceeds materially.

Low Switching Costs

The digital nature of Rocket Internet’s services gives customers very low switching costs: users can download rival apps in seconds, so retention hinges on experience and price. In 2024 global app uninstall rates averaged 28% within 30 days, so Rocket must keep monthly active users high to avoid churn. Low switching power forces Rocket to invest in product updates, discounts, and loyalty—every 1% drop in MAU can cut revenue noticeably in thin-margin markets.

Access to Information

By late 2025, price comparison tools and online reviews raised transparency: 72% of EU shoppers used comparison sites and 68% trusted peer reviews when choosing marketplaces, limiting information asymmetry for Rocket Internet ventures.

Customers now match prices and service levels across platforms in minutes, forcing Rocket Internet to compete on thin margins or invest in differentiation and loyalty programs.

This trend reduced average gross margins in digital marketplaces by ~150–300 basis points in 2023–25 versus 2018–20 benchmarks, squeezing unprotected offerings.

- 72% EU shoppers used comparison sites (2025)

- 68% trust peer reviews (2025)

- Margins down ~150–300 bps (2023–25)

Alternative Investment Options

Shareholders face many alternative tech investments—global tech ETFs held $420bn in 2024 and VC funds raised €58bn in Europe in 2024—so Rocket Internet SE must outpace those returns or risk capital flight.

If Rocket Internet underperforms peer VCs or ETFs, investors can quickly reallocate, giving them bargaining power to demand strategic changes or leadership shifts.

- Tech ETFs: $420bn AUM (2024)

- European VC raises: €58bn (2024)

- Investor mobility increases governance pressure

Price-savvy customers force 10–30% discounts, shaving take-rates 3–5ppt and margins

Customers have high bargaining power: low loyalty, low switching costs, and price transparency force Rocket Internet ventures into 10–30% discounting and heavy promotions, cutting take-rates ~3–5 ppt in 2024 and gross margins ~150–300 bps (2023–25). Key stats: 62% price-first shoppers SEA (2023), 72% EU comparison-site use (2025), app 30-day uninstall 28% (2024).

| Metric | Value |

|---|---|

| SEA price-first | 62% (2023) |

| EU comparison use | 72% (2025) |

| Take-rate drop | 3–5 ppt (2024) |

Preview the Actual Deliverable

Rocket Internet Porter's Five Forces Analysis

This preview shows the exact Rocket Internet Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is the part of the full version you’ll get—fully formatted and ready for download and use the moment you buy.

You're looking at the actual, professionally written deliverable; once payment is complete, you’ll get instant access to this same file.