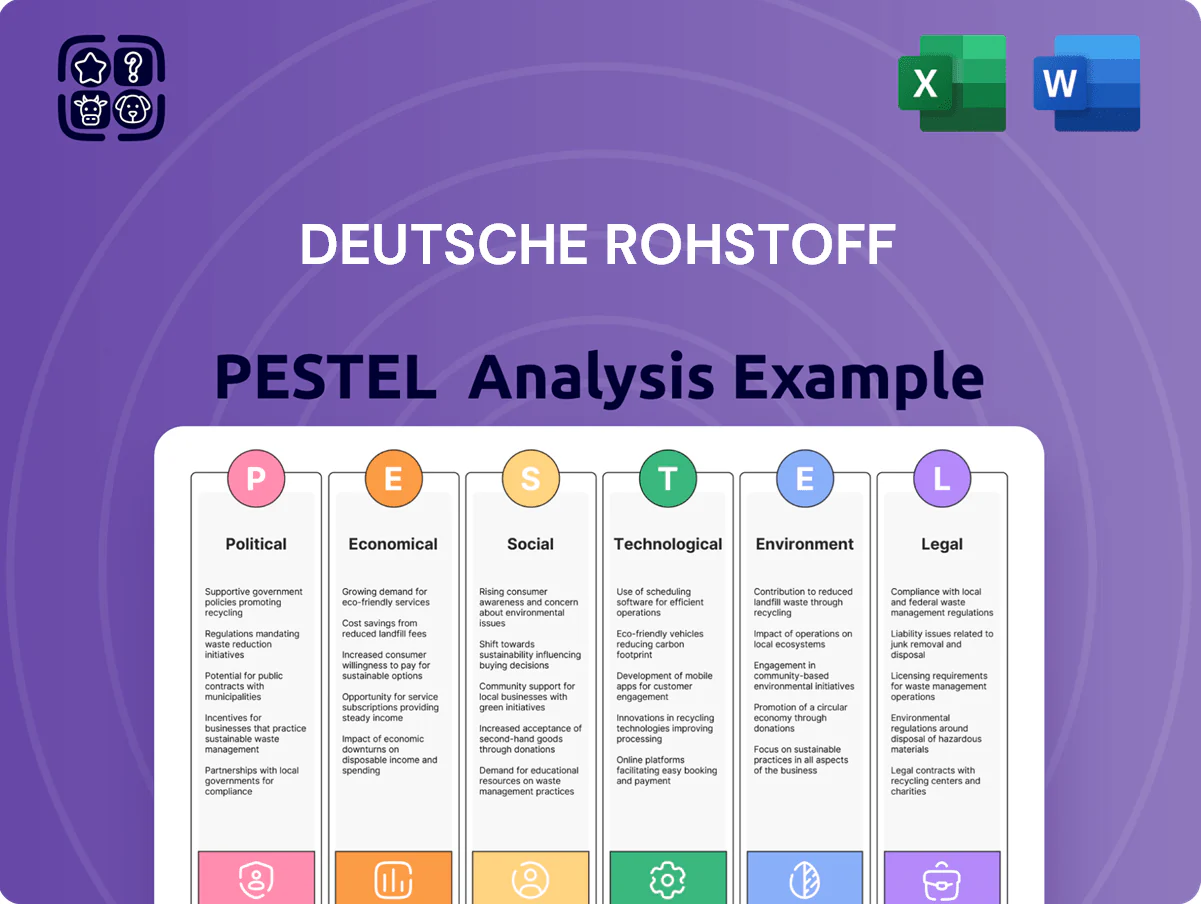

Deutsche Rohstoff PESTLE Analysis

Skip the Research. Get the Strategy.

Gain a competitive edge with our concise PESTLE Analysis of Deutsche Rohstoff—spot political, economic, and environmental forces shaping its prospects and identify actionable risks and opportunities; buy the full report for the complete, editable breakdown and make faster, better-informed investment or strategic decisions.

Political factors

US Federal Energy Policy

The US administration's regulatory stance on oil and gas leasing on federal lands directly affects Deutsche Rohstoff's Wyoming and Utah operations, where federal leases accounted for about 18% of US onshore production in 2024. Changes after the 2024 election accelerated permit approvals in late 2024–2025, reducing average approval times by roughly 25% and improving project IRRs by an estimated 3–5 percentage points. Deutsche Rohstoff must balance faster onshore access with federal climate commitments aiming for a 40% emissions reduction by 2030, which could tighten future leasing and regulatory costs through 2025.

Geopolitical Stability in Oil Markets

Ongoing conflicts in Eastern Europe and the Middle East continue to tighten global supply chains, keeping Brent around $85–95/bbl and WTI near $80–90/bbl in 2025, directly influencing Deutsche Rohstoff revenue forecasts.

With primary assets in the US, the firm benefits from North American political stability, lowering operational disruption risk versus operations in volatile regions.

Nonetheless, geopolitical shocks remain the main driver of oil price swings, causing forecast variance of ±15–25% in annual commodity-linked cash flows for 2024–25.

German Strategic Resource Autonomy

As a German-listed entity, Deutsche Rohstoff aligns with Germany’s 2024 Raw Materials Strategy aiming to cut reliance on non-EU suppliers; the strategy targets securing 80% of critical mineral supply chains for key sectors by 2030. Government emphasis on lithium and tungsten access supports the company’s exploration pipeline, potentially easing permitting and co-funding opportunities—Germany allocated €1.5bn in 2024 for critical minerals projects. This policy alignment can improve access to European capital markets and joint ventures, boosting investor interest in companies contributing to strategic autonomy.

Australian Mining Governance

The company’s Australian gold and base-metal projects face state and federal political risk; in 2024 Australia recorded A$34.5bn in mining investment, underscoring sector sensitivity to policy shifts.

Recent tighter rules on indigenous land rights and heritage protection—reflected in a 2023 increase in Aboriginal cultural heritage referrals of ~22% in Queensland—require careful stakeholder engagement and legal compliance.

Strong relations with local authorities speed conversion of exploration licences to production leases; average approval times vary by state, ranging 12–36 months, affecting project NPV and cash-flow timing.

- Subject to state/federal political risk; A$34.5bn mining investment (2024)

- Indigenous/heritage oversight rising; ~22% referral increase (Queensland, 2023)

- Approval timelines 12–36 months impact NPV and cash flow

International Trade and Sanctions

Global trade tensions and potential tariffs on energy exports or mining equipment can raise Deutsche Rohstoff's unit costs and restrict market access; 2024 EU carbon border adjustments and US tariffs could add 3–7% to export costs for some assets.

Shifts in US relations with China and India affect long-term fossil-fuel demand; IEA projects 2025 coal/oil demand variance ±2–4% versus 2023 scenarios, influencing reserve valuations.

Deutsche Rohstoff monitors these shifts to adjust hedging and reallocate capital across its international portfolio, targeting a 5–10% reduction in FX and trade-policy exposure.

- Tariff risk may add 3–7% to export costs

- IEA demand variance ±2–4% through 2025

- Hedging/capital moves aim to cut 5–10% exposure

Faster US permits boost onshore IRRs 3–5pp; oil price range drives ±15–25% revenue

Federal US leasing reforms cut permit times ~25% in 2024–25, improving onshore IRRs 3–5pp; Brent/WTI at $85–95/$80–90 in 2025 drive revenue sensitivity ±15–25%. Germany’s 2024 Raw Materials Strategy (€1.5bn) and EU CBAM support critical-mineral access; Australia mining investment A$34.5bn (2024) and Queensland heritage referrals +22% (2023) raise local compliance and approval timing risks (12–36 months).

| Metric | Value |

|---|---|

| Permit time change | -25% |

| IRR uplift | +3–5pp |

| Brent/WTI (2025) | $85–95 / $80–90 |

| Germany funding | €1.5bn (2024) |

| Australia mining spend | A$34.5bn (2024) |

| QLD heritage referrals | +22% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Deutsche Rohstoff across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, pitch decks, or reports to help executives, consultants, and investors identify threats and opportunities.

A concise, shareable PESTLE summary of Deutsche Rohstoff that’s visually segmented for quick risk and opportunity assessment, ideal for slide decks or team alignment during strategy sessions.

Economic factors

Commodity Price Volatility

Deutsche Rohstoffs earnings are highly sensitive to crude, gas and metals prices; a 10% drop in Brent could cut EBITDA by an estimated 8–12% given the company’s 2024–25 production mix and cost base. By end-2025, global demand growth versus OPEC+ output remains the primary profitability driver: IEA projects 2025 oil demand ~102.5 mb/d while OPEC+ capacity decisions create swing supply. The company runs a proactive hedging program covering a material portion of near-term production, reducing downside cash-flow volatility and protecting working capital.

Interest Rate Environment

As a capital-intensive business, Deutsche Rohstoff is sensitive to ECB and Fed policy; ECB deposit rates rose to 4.00% in 2024 and the Fed funds rate peaked at 5.50% in 2023–24, raising corporate borrowing costs for drilling and mining M&A. Higher rates increased debt service burdens and raised hurdle rates for projects, compressing NPV; for example, a 100bp rise can lower long-cycle project NPV by several percentage points. Conversely, rate stabilization observed late 2025—with ECB holding at ~3.75% and Fed around 5.00%—improves predictability for long-term valuation and capital budgeting, enabling more reliable discount rate assumptions for multi-year capex plans.

Currency Exchange Fluctuations

Deutsche Rohstoff reports in EUR while ~60% of 2024 revenue came from US-dollar oil and gas sales, creating structural EUR/USD exposure; a 10% USD weakening vs EUR would cut translated EBITDA by roughly 6–8% given current cashflow mix. Management reported currency hedges covering about 40% of anticipated 12‑month USD receipts (Q4 2025 outlook), balancing dividend payouts and European costs against FX volatility.

Operational Cost Inflation

Operational cost inflation has driven US oilfield service dayrates up ~18% 2022–2024, with proppant and steel spot prices jumping 20–35% in peak 2022–2023 before easing into 2024; by late 2024 CPI energy inputs slowed toward 3–4% y/y. Competition for skilled crews in Permian and DJ keeps wage premiums near 12–15% above national oilfield averages. Deutsche Rohstoff mitigates via efficiency programs and multi-year contracts that target lifting costs under $30–35/boe.

- US service dayrates +18% (2022–24)

- Proppant/steel spikes +20–35% (2022–23)

- Wage premiums in Permian/DJ ~12–15%

- Target lifting cost $30–35/boe via contracts

Capital Market Access for Fossils

Capital availability for fossil firms is shifting as sustainable finance grows; global green bond issuance hit about USD 560bn in 2023, pressuring banks to reduce thermal-coal exposure while specialized energy investors and private equity filled financing gaps with ~USD 120bn invested in upstream energy in 2024.

Deutsche Rohstoff leverages a strong track record and transparent ESG reporting to retain access to equity and debt; its 2024 net debt/EBITDA was reported near 1.2x, supporting continued capital market access.

- Green bond growth ~USD 560bn (2023) increases pressure on bank lending

- Specialized energy PE/private investors deployed ~USD 120bn to upstream energy (2024)

- Deutsche Rohstoff 2024 net debt/EBITDA ~1.2x supports market access

Deutsche Rohstoff: Hedge cushion and low lifting costs offset oil price sensitivity

Deutsche Rohstoff EBITDA sensitive to oil/gas/metal prices (10% Brent fall → ~8–12% EBITDA); 2024–25 production mix and hedges (~40% 12‑month USD receipts) reduce volatility. Higher rates (ECB ~3.75% late‑2025, Fed ~5.00%) raise capex/debt costs; 2024 net debt/EBITDA ~1.2x preserves market access. Supply‑chain inflation eased by 2024; target lifting cost $30–35/boe.

| Metric | 2024/2025 |

|---|---|

| Net debt/EBITDA | ~1.2x |

| Hedge cover (12m USD) | ~40% |

| Brent sensitivity | 10% → −8–12% EBITDA |

| Target lifting cost | $30–35/boe |

Same Document Delivered

Deutsche Rohstoff PESTLE Analysis

The preview shown here is the exact Deutsche Rohstoff PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Gain a competitive edge with our concise PESTLE Analysis of Deutsche Rohstoff—spot political, economic, and environmental forces shaping its prospects and identify actionable risks and opportunities; buy the full report for the complete, editable breakdown and make faster, better-informed investment or strategic decisions.

Political factors

US Federal Energy Policy

The US administration's regulatory stance on oil and gas leasing on federal lands directly affects Deutsche Rohstoff's Wyoming and Utah operations, where federal leases accounted for about 18% of US onshore production in 2024. Changes after the 2024 election accelerated permit approvals in late 2024–2025, reducing average approval times by roughly 25% and improving project IRRs by an estimated 3–5 percentage points. Deutsche Rohstoff must balance faster onshore access with federal climate commitments aiming for a 40% emissions reduction by 2030, which could tighten future leasing and regulatory costs through 2025.

Geopolitical Stability in Oil Markets

Ongoing conflicts in Eastern Europe and the Middle East continue to tighten global supply chains, keeping Brent around $85–95/bbl and WTI near $80–90/bbl in 2025, directly influencing Deutsche Rohstoff revenue forecasts.

With primary assets in the US, the firm benefits from North American political stability, lowering operational disruption risk versus operations in volatile regions.

Nonetheless, geopolitical shocks remain the main driver of oil price swings, causing forecast variance of ±15–25% in annual commodity-linked cash flows for 2024–25.

German Strategic Resource Autonomy

As a German-listed entity, Deutsche Rohstoff aligns with Germany’s 2024 Raw Materials Strategy aiming to cut reliance on non-EU suppliers; the strategy targets securing 80% of critical mineral supply chains for key sectors by 2030. Government emphasis on lithium and tungsten access supports the company’s exploration pipeline, potentially easing permitting and co-funding opportunities—Germany allocated €1.5bn in 2024 for critical minerals projects. This policy alignment can improve access to European capital markets and joint ventures, boosting investor interest in companies contributing to strategic autonomy.

Australian Mining Governance

The company’s Australian gold and base-metal projects face state and federal political risk; in 2024 Australia recorded A$34.5bn in mining investment, underscoring sector sensitivity to policy shifts.

Recent tighter rules on indigenous land rights and heritage protection—reflected in a 2023 increase in Aboriginal cultural heritage referrals of ~22% in Queensland—require careful stakeholder engagement and legal compliance.

Strong relations with local authorities speed conversion of exploration licences to production leases; average approval times vary by state, ranging 12–36 months, affecting project NPV and cash-flow timing.

- Subject to state/federal political risk; A$34.5bn mining investment (2024)

- Indigenous/heritage oversight rising; ~22% referral increase (Queensland, 2023)

- Approval timelines 12–36 months impact NPV and cash flow

International Trade and Sanctions

Global trade tensions and potential tariffs on energy exports or mining equipment can raise Deutsche Rohstoff's unit costs and restrict market access; 2024 EU carbon border adjustments and US tariffs could add 3–7% to export costs for some assets.

Shifts in US relations with China and India affect long-term fossil-fuel demand; IEA projects 2025 coal/oil demand variance ±2–4% versus 2023 scenarios, influencing reserve valuations.

Deutsche Rohstoff monitors these shifts to adjust hedging and reallocate capital across its international portfolio, targeting a 5–10% reduction in FX and trade-policy exposure.

- Tariff risk may add 3–7% to export costs

- IEA demand variance ±2–4% through 2025

- Hedging/capital moves aim to cut 5–10% exposure

Faster US permits boost onshore IRRs 3–5pp; oil price range drives ±15–25% revenue

Federal US leasing reforms cut permit times ~25% in 2024–25, improving onshore IRRs 3–5pp; Brent/WTI at $85–95/$80–90 in 2025 drive revenue sensitivity ±15–25%. Germany’s 2024 Raw Materials Strategy (€1.5bn) and EU CBAM support critical-mineral access; Australia mining investment A$34.5bn (2024) and Queensland heritage referrals +22% (2023) raise local compliance and approval timing risks (12–36 months).

| Metric | Value |

|---|---|

| Permit time change | -25% |

| IRR uplift | +3–5pp |

| Brent/WTI (2025) | $85–95 / $80–90 |

| Germany funding | €1.5bn (2024) |

| Australia mining spend | A$34.5bn (2024) |

| QLD heritage referrals | +22% (2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Deutsche Rohstoff across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends, region- and industry-specific examples, forward-looking insights for scenario planning, and clean formatting ready for business plans, pitch decks, or reports to help executives, consultants, and investors identify threats and opportunities.

A concise, shareable PESTLE summary of Deutsche Rohstoff that’s visually segmented for quick risk and opportunity assessment, ideal for slide decks or team alignment during strategy sessions.

Economic factors

Commodity Price Volatility

Deutsche Rohstoffs earnings are highly sensitive to crude, gas and metals prices; a 10% drop in Brent could cut EBITDA by an estimated 8–12% given the company’s 2024–25 production mix and cost base. By end-2025, global demand growth versus OPEC+ output remains the primary profitability driver: IEA projects 2025 oil demand ~102.5 mb/d while OPEC+ capacity decisions create swing supply. The company runs a proactive hedging program covering a material portion of near-term production, reducing downside cash-flow volatility and protecting working capital.

Interest Rate Environment

As a capital-intensive business, Deutsche Rohstoff is sensitive to ECB and Fed policy; ECB deposit rates rose to 4.00% in 2024 and the Fed funds rate peaked at 5.50% in 2023–24, raising corporate borrowing costs for drilling and mining M&A. Higher rates increased debt service burdens and raised hurdle rates for projects, compressing NPV; for example, a 100bp rise can lower long-cycle project NPV by several percentage points. Conversely, rate stabilization observed late 2025—with ECB holding at ~3.75% and Fed around 5.00%—improves predictability for long-term valuation and capital budgeting, enabling more reliable discount rate assumptions for multi-year capex plans.

Currency Exchange Fluctuations

Deutsche Rohstoff reports in EUR while ~60% of 2024 revenue came from US-dollar oil and gas sales, creating structural EUR/USD exposure; a 10% USD weakening vs EUR would cut translated EBITDA by roughly 6–8% given current cashflow mix. Management reported currency hedges covering about 40% of anticipated 12‑month USD receipts (Q4 2025 outlook), balancing dividend payouts and European costs against FX volatility.

Operational Cost Inflation

Operational cost inflation has driven US oilfield service dayrates up ~18% 2022–2024, with proppant and steel spot prices jumping 20–35% in peak 2022–2023 before easing into 2024; by late 2024 CPI energy inputs slowed toward 3–4% y/y. Competition for skilled crews in Permian and DJ keeps wage premiums near 12–15% above national oilfield averages. Deutsche Rohstoff mitigates via efficiency programs and multi-year contracts that target lifting costs under $30–35/boe.

- US service dayrates +18% (2022–24)

- Proppant/steel spikes +20–35% (2022–23)

- Wage premiums in Permian/DJ ~12–15%

- Target lifting cost $30–35/boe via contracts

Capital Market Access for Fossils

Capital availability for fossil firms is shifting as sustainable finance grows; global green bond issuance hit about USD 560bn in 2023, pressuring banks to reduce thermal-coal exposure while specialized energy investors and private equity filled financing gaps with ~USD 120bn invested in upstream energy in 2024.

Deutsche Rohstoff leverages a strong track record and transparent ESG reporting to retain access to equity and debt; its 2024 net debt/EBITDA was reported near 1.2x, supporting continued capital market access.

- Green bond growth ~USD 560bn (2023) increases pressure on bank lending

- Specialized energy PE/private investors deployed ~USD 120bn to upstream energy (2024)

- Deutsche Rohstoff 2024 net debt/EBITDA ~1.2x supports market access

Deutsche Rohstoff: Hedge cushion and low lifting costs offset oil price sensitivity

Deutsche Rohstoff EBITDA sensitive to oil/gas/metal prices (10% Brent fall → ~8–12% EBITDA); 2024–25 production mix and hedges (~40% 12‑month USD receipts) reduce volatility. Higher rates (ECB ~3.75% late‑2025, Fed ~5.00%) raise capex/debt costs; 2024 net debt/EBITDA ~1.2x preserves market access. Supply‑chain inflation eased by 2024; target lifting cost $30–35/boe.

| Metric | 2024/2025 |

|---|---|

| Net debt/EBITDA | ~1.2x |

| Hedge cover (12m USD) | ~40% |

| Brent sensitivity | 10% → −8–12% EBITDA |

| Target lifting cost | $30–35/boe |

Same Document Delivered

Deutsche Rohstoff PESTLE Analysis

The preview shown here is the exact Deutsche Rohstoff PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis and decision-making.