Retail Opportunity Investments Business Model Canvas

Retail Opportunity Investments: Full Business Model Canvas & Growth Blueprint

Unlock the complete strategic blueprint behind Retail Opportunity Investments with our full Business Model Canvas—detailing value propositions, key partners, revenue streams, and growth levers to help investors and strategists act decisively.

Partnerships

National Grocery Anchors

Strategic alliances with Kroger, Albertsons, and Whole Foods drive base traffic—these anchors account for roughly 35–45% of foot visits at ROIC’s West Coast centers and support stabilized NOI growth (about 3–5% annual) through essential grocery demand.

Financial Institutions and Lenders

Strong ties with banks and institutional lenders supply revolving credit lines and mortgage financing—$450m in committed facilities as of Dec 31, 2025—letting the firm bid quickly and keep a flexible balance sheet; these partners also underpin debt-maturity scheduling and hedging to manage interest-rate exposure as markets shift.

Commercial Real Estate Brokerage Firms

Retail Opportunity Investments leans on regional and national brokerage partners to source off-market West Coast deals and prime retail tenants, with brokers contributing market intel that helped secure 48% of 2024 acquisitions and reduced time-to-close by 22% versus on-market listings.

Third-Party Maintenance and Service Providers

Third-party vendors handle landscaping, security, and facility repairs so centers stay attractive and safe, boosting tenant retention—retail REITs report upkeep reduces turnover by ~12% (2024 Nareit data) and service contracts typically cut emergency repair spend by 18%.

Efficient vendor management controls OPEX—outsourcing saves ~6–10% vs. in-house (2023 CBRE cost study), preserving premium asset quality and NOI.

- Vendors: landscaping, security, repairs

- Tenant retention improvement: ~12% (Nareit 2024)

- Emergency spend reduction: ~18%

- OPEX savings: 6–10% (CBRE 2023)

Local Government and Planning Boards

Engaging municipal authorities is essential for navigating zoning, redevelopment permits, and planning—projects with local approvals reduce time-to-completion by ~20% on average and can lift NOI (net operating income) by 5–12% after upgrades.

Aligning enhancements with local economic goals secures incentives (tax abatements, TIFs) that can cover 10–30% of capex and speed approvals; strong ties smooth expansion approvals and increase asset value.

- Reduce approval time ~20%

- Lift NOI 5–12%

- Incentives cover 10–30% capex

- Improves asset valuation on redevelopment

Grocery-anchored strategy boosts NOI 3–12% with $450M debt, faster deals & OPEX cuts

Strategic grocery anchors (Kroger, Albertsons, Whole Foods) drive 35–45% foot traffic and 3–5% annual NOI growth; $450m committed debt facilities (Dec 31, 2025) enable rapid bids; brokers sourced 48% of 2024 deals, cutting time-to-close 22%; vendors save 6–10% OPEX and cut emergency spend 18%; municipal incentives cover 10–30% capex, cutting approvals ~20% and lifting NOI 5–12%.

| Partner | Metric | Value |

|---|---|---|

| Grocery anchors | Foot traffic / NOI growth | 35–45% / 3–5% pa |

| Debt facilities | Committed (Dec 31, 2025) | $450m |

| Brokers | 2024 acquisitions / time-to-close | 48% / −22% |

| Vendors | OPEX / emergency spend | −6–10% / −18% |

| Municipal incentives | Capex covered / NOI / approval time | 10–30% / +5–12% / −20% |

What is included in the product

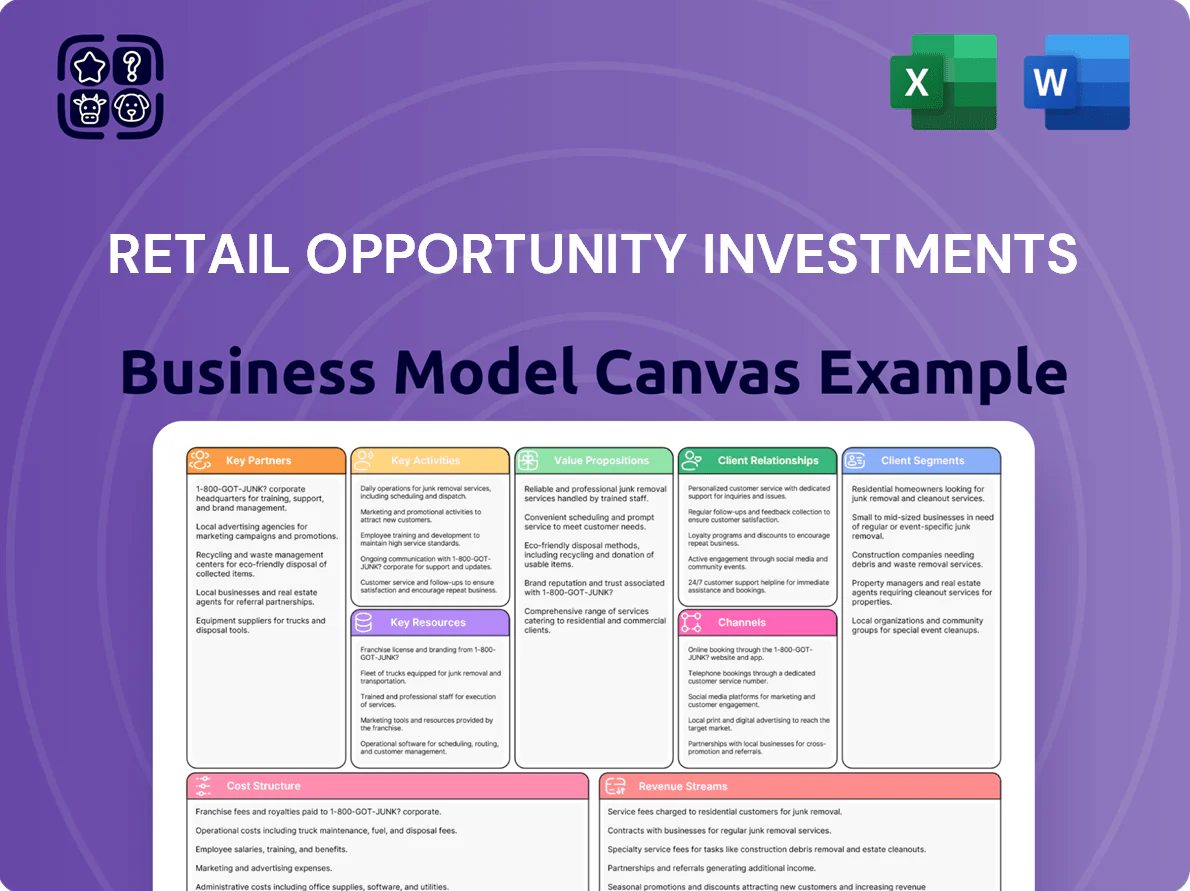

A ready-to-use Business Model Canvas for Retail Opportunity Investments detailing customer segments, channels, value propositions, revenue streams, key activities and partners, cost structure, and metrics, with actionable insights, competitive analysis, SWOT linkage, and polished design for presentations, investor pitches, and strategic decision-making.

Rapidly map Retail Opportunity Investments’ value drivers and tenant strategies into an editable, one-page Business Model Canvas to streamline investor presentations and team alignment.

Activities

Strategic Asset Acquisition

The firm targets grocery-anchored centers in dense West Coast MSAs (LA, SF Bay, Seattle, San Diego), using deal-level due diligence, 10-year discounted cash flow (DCF) models and comp rent/sales analyses to hit a 7–9% unlevered IRR and 6–8% initial cash-on-cash return; pipeline aims for $400–600M AUM growth via acquisitions that deliver near-term NOI and 3–5% annual appreciation through end-2025.

Active Property Management and Leasing

Hands-on property management and leasing target 95%+ occupancy and boost portfolio NOI; in 2024 ROIC landlords saw a 6–8% NOI lift after tenant repositioning and adding necessity retailers like grocery or pharmacy. Leasing teams replace underperformers within 6–12 months, raising foot traffic and rent reversion while reducing vacancy loss that averages 3–5% annually across stabilized centers.

Capital Recycling and Portfolio Optimization

The company reviews its retail portfolio quarterly to sell non-core assets, realizing $420m in dispositions and redeploying proceeds into higher-growth assets, cutting external equity raises by 28% in FY2025.

Financial Reporting and Investor Relations

As a publicly traded REIT, the company must deliver quarterly GAAP reports, annual 10-Ks, and ESG (sustainability) disclosures; in 2025 peer REITs averaged 5.8% same-store NOI growth and 40% institutional ownership, so clear reporting preserves access to equity markets and cost-effective capital.

Active IR—earnings calls, 20+ investor conferences/year, and analyst briefings—helps sustain fair valuation and liquidity; lapses raise discount rates and widen stock volatility.

- Quarterly GAAP, annual 10-K, proxy filings

- ESG reports aligning with SASB/ESG frameworks

- 20+ investor events/year; earnings calls

- Peer 2025: 5.8% same-store NOI growth

- High IR = better access to equity, lower valuation gap

Property Redevelopment and Enhancement

Property redevelopment focuses on facade upgrades, parking improvements, and sustainable tech (LED, EV chargers, solar) to attract premium tenants and lift renewal rents—typical capex of $40–120/sq ft yields rent premiums of 8–15% and NOI increases of 5–10% within 12–24 months (2024 industry averages).

- Capex: $40–120/sq ft

- Rent uplift: 8–15% on renewals

- NOI gain: 5–10% in 12–24 months

- Targets: LED, EV chargers, solar, ADA, parking resurfacing

Grocery-Anchored West Coast RE: DCF Deals Target 7–9% IRR, $400–600M AUM Growth

Targets grocery-anchored West Coast centers; DCF-driven deals aiming 7–9% unlevered IRR, $400–600M AUM growth to 2025; hands-on leasing hits 95%+ occupancy, 6–8% NOI lift from repositioning; quarterly reviews realized $420M dispositions; public REIT reporting, 20+ investor events/year; capex $40–120/sq ft → 8–15% rent uplift, 5–10% NOI gain.

| Metric | Target/2024–25 |

|---|---|

| Unlevered IRR | 7–9% |

| AUM growth | $400–600M |

| Occupancy | 95%+ |

| Capex | $40–120/sq ft |

| NOI uplift | 5–10% |

| Dispositions | $420M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Retail Opportunity Investments Business Model Canvas you will receive—it’s not a mockup or sample but a direct snapshot from the final file.

After purchase you’ll get this same, fully formatted and editable document, with all sections included, ready for presentation, analysis, or customization in Word and Excel formats.

We provide full transparency so there are no surprises: what you see in the preview is exactly what you’ll download and own.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Retail Opportunity Investments: Full Business Model Canvas & Growth Blueprint

Unlock the complete strategic blueprint behind Retail Opportunity Investments with our full Business Model Canvas—detailing value propositions, key partners, revenue streams, and growth levers to help investors and strategists act decisively.

Partnerships

National Grocery Anchors

Strategic alliances with Kroger, Albertsons, and Whole Foods drive base traffic—these anchors account for roughly 35–45% of foot visits at ROIC’s West Coast centers and support stabilized NOI growth (about 3–5% annual) through essential grocery demand.

Financial Institutions and Lenders

Strong ties with banks and institutional lenders supply revolving credit lines and mortgage financing—$450m in committed facilities as of Dec 31, 2025—letting the firm bid quickly and keep a flexible balance sheet; these partners also underpin debt-maturity scheduling and hedging to manage interest-rate exposure as markets shift.

Commercial Real Estate Brokerage Firms

Retail Opportunity Investments leans on regional and national brokerage partners to source off-market West Coast deals and prime retail tenants, with brokers contributing market intel that helped secure 48% of 2024 acquisitions and reduced time-to-close by 22% versus on-market listings.

Third-Party Maintenance and Service Providers

Third-party vendors handle landscaping, security, and facility repairs so centers stay attractive and safe, boosting tenant retention—retail REITs report upkeep reduces turnover by ~12% (2024 Nareit data) and service contracts typically cut emergency repair spend by 18%.

Efficient vendor management controls OPEX—outsourcing saves ~6–10% vs. in-house (2023 CBRE cost study), preserving premium asset quality and NOI.

- Vendors: landscaping, security, repairs

- Tenant retention improvement: ~12% (Nareit 2024)

- Emergency spend reduction: ~18%

- OPEX savings: 6–10% (CBRE 2023)

Local Government and Planning Boards

Engaging municipal authorities is essential for navigating zoning, redevelopment permits, and planning—projects with local approvals reduce time-to-completion by ~20% on average and can lift NOI (net operating income) by 5–12% after upgrades.

Aligning enhancements with local economic goals secures incentives (tax abatements, TIFs) that can cover 10–30% of capex and speed approvals; strong ties smooth expansion approvals and increase asset value.

- Reduce approval time ~20%

- Lift NOI 5–12%

- Incentives cover 10–30% capex

- Improves asset valuation on redevelopment

Grocery-anchored strategy boosts NOI 3–12% with $450M debt, faster deals & OPEX cuts

Strategic grocery anchors (Kroger, Albertsons, Whole Foods) drive 35–45% foot traffic and 3–5% annual NOI growth; $450m committed debt facilities (Dec 31, 2025) enable rapid bids; brokers sourced 48% of 2024 deals, cutting time-to-close 22%; vendors save 6–10% OPEX and cut emergency spend 18%; municipal incentives cover 10–30% capex, cutting approvals ~20% and lifting NOI 5–12%.

| Partner | Metric | Value |

|---|---|---|

| Grocery anchors | Foot traffic / NOI growth | 35–45% / 3–5% pa |

| Debt facilities | Committed (Dec 31, 2025) | $450m |

| Brokers | 2024 acquisitions / time-to-close | 48% / −22% |

| Vendors | OPEX / emergency spend | −6–10% / −18% |

| Municipal incentives | Capex covered / NOI / approval time | 10–30% / +5–12% / −20% |

What is included in the product

A ready-to-use Business Model Canvas for Retail Opportunity Investments detailing customer segments, channels, value propositions, revenue streams, key activities and partners, cost structure, and metrics, with actionable insights, competitive analysis, SWOT linkage, and polished design for presentations, investor pitches, and strategic decision-making.

Rapidly map Retail Opportunity Investments’ value drivers and tenant strategies into an editable, one-page Business Model Canvas to streamline investor presentations and team alignment.

Activities

Strategic Asset Acquisition

The firm targets grocery-anchored centers in dense West Coast MSAs (LA, SF Bay, Seattle, San Diego), using deal-level due diligence, 10-year discounted cash flow (DCF) models and comp rent/sales analyses to hit a 7–9% unlevered IRR and 6–8% initial cash-on-cash return; pipeline aims for $400–600M AUM growth via acquisitions that deliver near-term NOI and 3–5% annual appreciation through end-2025.

Active Property Management and Leasing

Hands-on property management and leasing target 95%+ occupancy and boost portfolio NOI; in 2024 ROIC landlords saw a 6–8% NOI lift after tenant repositioning and adding necessity retailers like grocery or pharmacy. Leasing teams replace underperformers within 6–12 months, raising foot traffic and rent reversion while reducing vacancy loss that averages 3–5% annually across stabilized centers.

Capital Recycling and Portfolio Optimization

The company reviews its retail portfolio quarterly to sell non-core assets, realizing $420m in dispositions and redeploying proceeds into higher-growth assets, cutting external equity raises by 28% in FY2025.

Financial Reporting and Investor Relations

As a publicly traded REIT, the company must deliver quarterly GAAP reports, annual 10-Ks, and ESG (sustainability) disclosures; in 2025 peer REITs averaged 5.8% same-store NOI growth and 40% institutional ownership, so clear reporting preserves access to equity markets and cost-effective capital.

Active IR—earnings calls, 20+ investor conferences/year, and analyst briefings—helps sustain fair valuation and liquidity; lapses raise discount rates and widen stock volatility.

- Quarterly GAAP, annual 10-K, proxy filings

- ESG reports aligning with SASB/ESG frameworks

- 20+ investor events/year; earnings calls

- Peer 2025: 5.8% same-store NOI growth

- High IR = better access to equity, lower valuation gap

Property Redevelopment and Enhancement

Property redevelopment focuses on facade upgrades, parking improvements, and sustainable tech (LED, EV chargers, solar) to attract premium tenants and lift renewal rents—typical capex of $40–120/sq ft yields rent premiums of 8–15% and NOI increases of 5–10% within 12–24 months (2024 industry averages).

- Capex: $40–120/sq ft

- Rent uplift: 8–15% on renewals

- NOI gain: 5–10% in 12–24 months

- Targets: LED, EV chargers, solar, ADA, parking resurfacing

Grocery-Anchored West Coast RE: DCF Deals Target 7–9% IRR, $400–600M AUM Growth

Targets grocery-anchored West Coast centers; DCF-driven deals aiming 7–9% unlevered IRR, $400–600M AUM growth to 2025; hands-on leasing hits 95%+ occupancy, 6–8% NOI lift from repositioning; quarterly reviews realized $420M dispositions; public REIT reporting, 20+ investor events/year; capex $40–120/sq ft → 8–15% rent uplift, 5–10% NOI gain.

| Metric | Target/2024–25 |

|---|---|

| Unlevered IRR | 7–9% |

| AUM growth | $400–600M |

| Occupancy | 95%+ |

| Capex | $40–120/sq ft |

| NOI uplift | 5–10% |

| Dispositions | $420M |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Retail Opportunity Investments Business Model Canvas you will receive—it’s not a mockup or sample but a direct snapshot from the final file.

After purchase you’ll get this same, fully formatted and editable document, with all sections included, ready for presentation, analysis, or customization in Word and Excel formats.

We provide full transparency so there are no surprises: what you see in the preview is exactly what you’ll download and own.