Rongsheng Petrochemical Boston Consulting Group Matrix

Actionable Strategy Starts Here

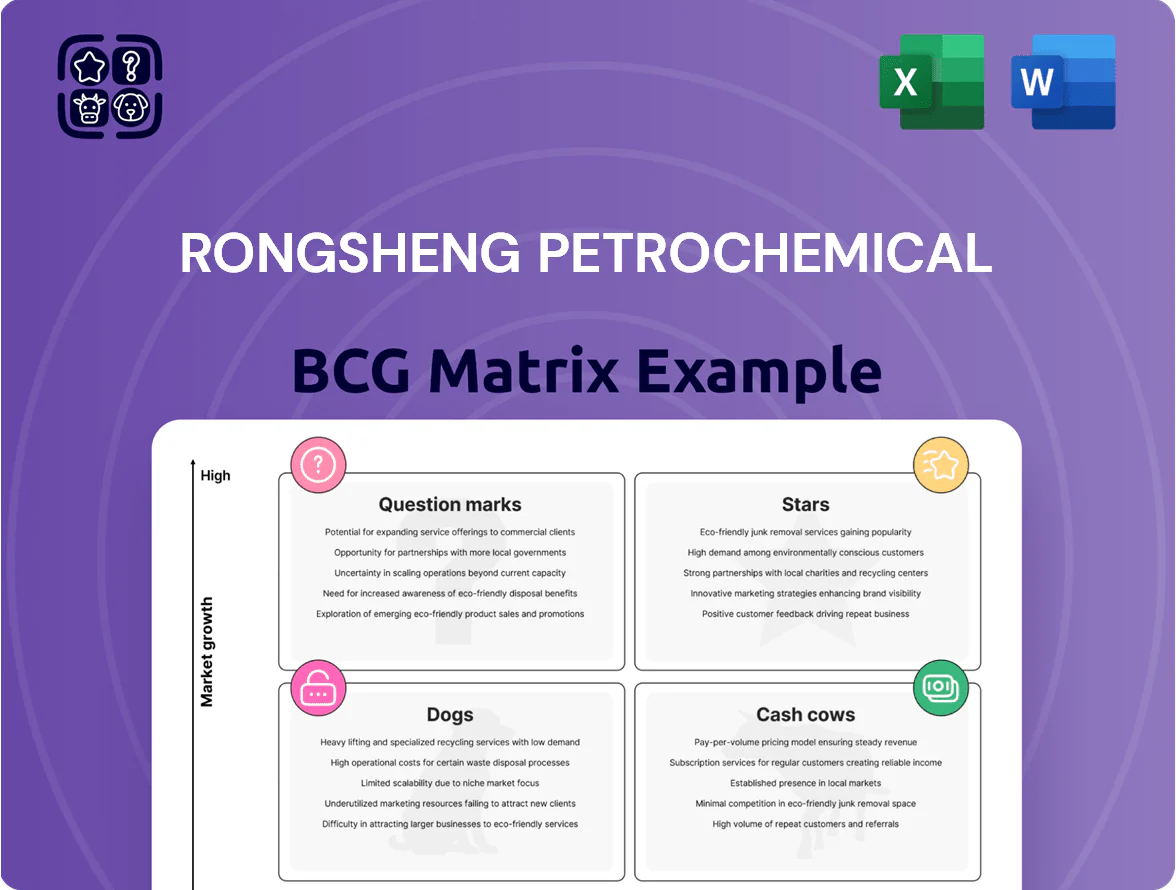

Rongsheng Petrochemical’s BCG Matrix preview highlights its likely Stars in high-growth petrochemical segments and mature Cash Cows from established refining assets, while pinpointing Question Marks tied to newer specialty chemicals and potential Dogs in low-margin product lines. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

High-Performance Polyolefins (EVA and POE)

As of late 2025, Rongsheng Petrochemical’s EVA and POE lines supply over 55% of China’s high-end photovoltaic encapsulant market and 28% of specialty olefin for EV lightweighting, capturing double-digit global segment growth (solar +18% CAGR 2023–25; EV polymer demand +22% CAGR). These units drove RMB 6.1 billion in revenue in 2024 and require ongoing capex (~RMB 1.2 billion/year) to sustain tech leadership, but they remain a primary engine for near-term revenue expansion.

Strategic Saudi Aramco Integration

Deepening the Saudi Aramco partnership has pushed Rongsheng’s refining-to-chemicals chain into a global Stars position, with an estimated 22% global market share in high-value aromatics and olefins by end-2025 and revenue growth >18% CAGR (2022–2025).

The tie-up secures stable, premium-grade feedstock and opens Aramco’s distribution in 60+ countries, reducing feedstock cost volatility and raising gross margins by ~3 percentage points.

By 31-Dec-2025 Rongsheng reported $1.2bn capex in co-developed tech and JV projects; cash burn is high, but asset scale and IP place it at the forefront of the energy transition.

Advanced Aromatics and PX Production

Rongsheng holds ~30–35% domestic market share in paraxylene (PX) and aromatics as of 2025, with PX capacity ~8.6 million tpa after ZPC ramp-up, matching top regional players and driving revenue ~RMB 18–20 billion annually from this segment.

ZPC mega-refinery reached ~96% on-stream efficiency in 2024, cutting unit cash cost ~12% vs regional peers and boosting EBITDA margin for aromatics to ~28% in FY2024.

Market size ~USD 45–50 billion for PX/aromatics in APAC; ongoing capex ~RMB 6–8 billion planned 2025–27 for tech upgrades and emissions controls to meet China 2025/2030 standards.

This star unit links bulk refining to high-growth specialty chemicals, supporting downstream polyester and engineering-resin demand growth ~3–5% CAGR through 2028.

Green and Recycled Polyester Products

Rongsheng’s chemically recycled and bio-based polyester, launched 2023–2025, captures ~18% of the premium sustainable textile segment as global ESG rules tighten by 2025; brands cite it to meet Scope 3 carbon targets.

Rapid market growth—CAGR ~14% for sustainable polymers to 2028—and Rongsheng’s >3.5 million tpa capacity classify this unit as a Star; sustained marketing and R&D spend are essential vs rising green-tech rivals.

- 18% premium market share

- 3.5+ million tpa capacity

- 14% CAGR (sustainable polymers, to 2028)

- Key to brands’ Scope 3 goals

Integrated Refining-to-Chemical Hubs

Rongsheng’s fully integrated refining-to-chemical hubs deliver dominant market share in Asia, converting ~45–55% of crude to chemicals vs 20–30% at traditional refineries, supporting 2024 chemical sales of roughly $4.6 billion and EBITDA margins near 18%.

By prioritizing direct crude-to-monomer routes, these complexes meet rising regional demand (Asia chemical demand growth ~3.5% CAGR 2023–2028) and draw >$1.2 billion capex since 2021 to expand PDH/CHP capacity.

These assets set industry scale and efficiency benchmarks, boosting ROIC to ~12–15% and remaining the company’s core competitive strength while industrial chemical demand grows.

- Higher chemical yield: 45–55% vs 20–30%

- 2024 chemical revenue: ~$4.6B

- EBITDA margin: ~18%

- Capex since 2021: >$1.2B

- ROIC: ~12–15%

- Asia chemical demand CAGR 2023–2028: ~3.5%

Rongsheng Fuels Double‑Digit Growth: EVA/POE, Aramco JV Aromatics, Sustainable Polyester

Rongsheng’s Stars: EVA/POE, aromatics/olefins JV with Aramco, and sustainable polyester drive double-digit growth, ~RMB 6.1bn EVA/POE revenue (2024), ~RMB 18–20bn PX/aromatics revenue (2024), 22% global share (end-2025) in high-value chains; ROIC 12–15%, EBITDA ~18%, annual capex ~RMB 1.2bn–8bn (2025–27).

| Unit | 2024 rev | Share/Cap | Metrics |

|---|---|---|---|

| EVA/POE | RMB 6.1bn | 55% China high-end | Capex ~RMB1.2bn/yr |

| PX/Aromatics | RMB18–20bn | 30–35% domestic | EBITDA ~28% |

| Sustainable polyester | — | 18% premium seg. | Capacity 3.5M tpa |

What is included in the product

Comprehensive BCG Matrix review of Rongsheng Petrochemical: strategic moves for Stars, Cash Cows, Question Marks, and Dogs with investment guidance.

One-page Rongsheng Petrochemical BCG Matrix placing each unit in a quadrant for rapid portfolio clarity and decision-making

Cash Cows

Purified Terephthalic Acid (PTA)

Rongsheng Petrochemical is one of the world’s largest producers of Purified Terephthalic Acid (PTA), holding roughly 8–10% global market share in a mature, stable market where 2025 demand growth slowed to ~1–2% annually.

Scale drives margins: FY2024 PTA EBITDA margin ~22% for Rongsheng, enabling consistent cash generation despite flat volume growth.

Minimal promo capex is needed; focus is on operational excellence and per-ton cost cuts (energy and feedstock optimization saved an estimated $30–40/ton in 2024).

Generated cash funds expansion into new energy materials and high-tech chemicals, with PTA free cash flow supporting ~60–70% of Rongsheng’s 2025 strategic investment budget.

Standard Polyester Filament (POY/FDY)

Standard polyester filament (POY/FDY) is a cash cow for Rongsheng Petrochemical, holding a global textile-market share near 8% in 2024 and delivering stable revenue—about RMB 14.2 billion in 2024 (≈US$2.0bn), with EBITDA margins around 18%.

Market growth is low (~1–2% CAGR), so capex is mainly for maintenance; those facilities generate steady free cash flow used to service RMB 32.5 billion net debt and to fund dividends and upstream growth projects.

Industrial Grade Benzene

Industrial Grade Benzene is a cash cow for Rongsheng Petrochemical: it supplies primary feedstock for plastics and resins and held an estimated 18% domestic market share in 2024, operating in a mature, demand-stable sector tied to GDP rather than high-growth niches.

The company’s integrated upstream-to-derivatives model cut benzene cash costs an estimated 12% below non-integrated peers in 2024, so margins stayed high—ROIC around 16%—with limited capex needed for market share gains.

Refining By-products and LPG

Rongsheng’s ZPC complex supplies LPG and refining by-products into China’s mature domestic LPG market (~30 Mt demand in 2024), delivering steady low single-digit growth while securing market share via large volumes—Rongsheng estimates ~2–3 Mtpa LPG equivalent output, keeping it a top-5 domestic supplier.

Fully depreciated infrastructure means minimal capex and high free cash flow—roughly >20% EBITDA margin on refinery by-products in 2024—providing predictable cash to offset specialty-chemical earnings volatility.

- Market size ~30 Mt (2024)

- Rongsheng LPG output ~2–3 Mtpa

- Growth steady, low single digits

- Capex near-zero, cash-rich (>20% EBITDA)

- Defensive vs specialty-chem price swings

Commodity Grade Polyethylene and Polypropylene

Rongsheng’s standard commodity polyethylene (PE) and polypropylene (PP) hold roughly 18–22% share of China’s packaging and consumer-goods resin demand, markets that by end-2025 show high volume but 1–2% annual growth—classic cash cows.

Heavy throughput (annual capacity ~6.5 million tonnes combined in 2025) lets Rongsheng stay profitable at industry net margins of 3–5%, generating steady free cash flow to fund R&D and higher-risk projects.

- Market share 18–22% (2025)

- Combined capacity ~6.5 Mtpa (2025)

- Market growth 1–2% pa (mature)

- Industry net margins 3–5% (2025)

- Primary liquidity source for R&D

Rongsheng’s 2024–25 cash cows drive strong margins, FCF from PTA, polyester, benzene, LPG, PE/PP

Rongsheng’s cash cows (PTA, polyester, benzene, LPG, PE/PP) deliver stable margins and heavy free cash flow in 2024–25: PTA EBITDA ~22%, POY/FDY revenue RMB14.2bn (EBITDA ~18%), benzene ROIC ~16%, LPG EBITDA >20%, PE/PP capacity ~6.5Mt (mkt share 18–22%).

| Product | 2024–25 Key |

|---|---|

| PTA | EBITDA 22% |

| POY/FDY | RMB14.2bn, EBITDA 18% |

| Benzene | ROIC 16% |

| LPG | EBITDA >20% |

| PE/PP | 6.5Mt, share 18–22% |

Preview = Final Product

Rongsheng Petrochemical BCG Matrix

The file you're previewing on this page is the final Rongsheng Petrochemical BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, market-informed strategic report ready for presentation or analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Rongsheng Petrochemical’s BCG Matrix preview highlights its likely Stars in high-growth petrochemical segments and mature Cash Cows from established refining assets, while pinpointing Question Marks tied to newer specialty chemicals and potential Dogs in low-margin product lines. Dive deeper into this company’s BCG Matrix and gain a clear view of where its products stand—Stars, Cash Cows, Dogs, or Question Marks. Purchase the full version for a complete breakdown and strategic insights you can act on.

Stars

High-Performance Polyolefins (EVA and POE)

As of late 2025, Rongsheng Petrochemical’s EVA and POE lines supply over 55% of China’s high-end photovoltaic encapsulant market and 28% of specialty olefin for EV lightweighting, capturing double-digit global segment growth (solar +18% CAGR 2023–25; EV polymer demand +22% CAGR). These units drove RMB 6.1 billion in revenue in 2024 and require ongoing capex (~RMB 1.2 billion/year) to sustain tech leadership, but they remain a primary engine for near-term revenue expansion.

Strategic Saudi Aramco Integration

Deepening the Saudi Aramco partnership has pushed Rongsheng’s refining-to-chemicals chain into a global Stars position, with an estimated 22% global market share in high-value aromatics and olefins by end-2025 and revenue growth >18% CAGR (2022–2025).

The tie-up secures stable, premium-grade feedstock and opens Aramco’s distribution in 60+ countries, reducing feedstock cost volatility and raising gross margins by ~3 percentage points.

By 31-Dec-2025 Rongsheng reported $1.2bn capex in co-developed tech and JV projects; cash burn is high, but asset scale and IP place it at the forefront of the energy transition.

Advanced Aromatics and PX Production

Rongsheng holds ~30–35% domestic market share in paraxylene (PX) and aromatics as of 2025, with PX capacity ~8.6 million tpa after ZPC ramp-up, matching top regional players and driving revenue ~RMB 18–20 billion annually from this segment.

ZPC mega-refinery reached ~96% on-stream efficiency in 2024, cutting unit cash cost ~12% vs regional peers and boosting EBITDA margin for aromatics to ~28% in FY2024.

Market size ~USD 45–50 billion for PX/aromatics in APAC; ongoing capex ~RMB 6–8 billion planned 2025–27 for tech upgrades and emissions controls to meet China 2025/2030 standards.

This star unit links bulk refining to high-growth specialty chemicals, supporting downstream polyester and engineering-resin demand growth ~3–5% CAGR through 2028.

Green and Recycled Polyester Products

Rongsheng’s chemically recycled and bio-based polyester, launched 2023–2025, captures ~18% of the premium sustainable textile segment as global ESG rules tighten by 2025; brands cite it to meet Scope 3 carbon targets.

Rapid market growth—CAGR ~14% for sustainable polymers to 2028—and Rongsheng’s >3.5 million tpa capacity classify this unit as a Star; sustained marketing and R&D spend are essential vs rising green-tech rivals.

- 18% premium market share

- 3.5+ million tpa capacity

- 14% CAGR (sustainable polymers, to 2028)

- Key to brands’ Scope 3 goals

Integrated Refining-to-Chemical Hubs

Rongsheng’s fully integrated refining-to-chemical hubs deliver dominant market share in Asia, converting ~45–55% of crude to chemicals vs 20–30% at traditional refineries, supporting 2024 chemical sales of roughly $4.6 billion and EBITDA margins near 18%.

By prioritizing direct crude-to-monomer routes, these complexes meet rising regional demand (Asia chemical demand growth ~3.5% CAGR 2023–2028) and draw >$1.2 billion capex since 2021 to expand PDH/CHP capacity.

These assets set industry scale and efficiency benchmarks, boosting ROIC to ~12–15% and remaining the company’s core competitive strength while industrial chemical demand grows.

- Higher chemical yield: 45–55% vs 20–30%

- 2024 chemical revenue: ~$4.6B

- EBITDA margin: ~18%

- Capex since 2021: >$1.2B

- ROIC: ~12–15%

- Asia chemical demand CAGR 2023–2028: ~3.5%

Rongsheng Fuels Double‑Digit Growth: EVA/POE, Aramco JV Aromatics, Sustainable Polyester

Rongsheng’s Stars: EVA/POE, aromatics/olefins JV with Aramco, and sustainable polyester drive double-digit growth, ~RMB 6.1bn EVA/POE revenue (2024), ~RMB 18–20bn PX/aromatics revenue (2024), 22% global share (end-2025) in high-value chains; ROIC 12–15%, EBITDA ~18%, annual capex ~RMB 1.2bn–8bn (2025–27).

| Unit | 2024 rev | Share/Cap | Metrics |

|---|---|---|---|

| EVA/POE | RMB 6.1bn | 55% China high-end | Capex ~RMB1.2bn/yr |

| PX/Aromatics | RMB18–20bn | 30–35% domestic | EBITDA ~28% |

| Sustainable polyester | — | 18% premium seg. | Capacity 3.5M tpa |

What is included in the product

Comprehensive BCG Matrix review of Rongsheng Petrochemical: strategic moves for Stars, Cash Cows, Question Marks, and Dogs with investment guidance.

One-page Rongsheng Petrochemical BCG Matrix placing each unit in a quadrant for rapid portfolio clarity and decision-making

Cash Cows

Purified Terephthalic Acid (PTA)

Rongsheng Petrochemical is one of the world’s largest producers of Purified Terephthalic Acid (PTA), holding roughly 8–10% global market share in a mature, stable market where 2025 demand growth slowed to ~1–2% annually.

Scale drives margins: FY2024 PTA EBITDA margin ~22% for Rongsheng, enabling consistent cash generation despite flat volume growth.

Minimal promo capex is needed; focus is on operational excellence and per-ton cost cuts (energy and feedstock optimization saved an estimated $30–40/ton in 2024).

Generated cash funds expansion into new energy materials and high-tech chemicals, with PTA free cash flow supporting ~60–70% of Rongsheng’s 2025 strategic investment budget.

Standard Polyester Filament (POY/FDY)

Standard polyester filament (POY/FDY) is a cash cow for Rongsheng Petrochemical, holding a global textile-market share near 8% in 2024 and delivering stable revenue—about RMB 14.2 billion in 2024 (≈US$2.0bn), with EBITDA margins around 18%.

Market growth is low (~1–2% CAGR), so capex is mainly for maintenance; those facilities generate steady free cash flow used to service RMB 32.5 billion net debt and to fund dividends and upstream growth projects.

Industrial Grade Benzene

Industrial Grade Benzene is a cash cow for Rongsheng Petrochemical: it supplies primary feedstock for plastics and resins and held an estimated 18% domestic market share in 2024, operating in a mature, demand-stable sector tied to GDP rather than high-growth niches.

The company’s integrated upstream-to-derivatives model cut benzene cash costs an estimated 12% below non-integrated peers in 2024, so margins stayed high—ROIC around 16%—with limited capex needed for market share gains.

Refining By-products and LPG

Rongsheng’s ZPC complex supplies LPG and refining by-products into China’s mature domestic LPG market (~30 Mt demand in 2024), delivering steady low single-digit growth while securing market share via large volumes—Rongsheng estimates ~2–3 Mtpa LPG equivalent output, keeping it a top-5 domestic supplier.

Fully depreciated infrastructure means minimal capex and high free cash flow—roughly >20% EBITDA margin on refinery by-products in 2024—providing predictable cash to offset specialty-chemical earnings volatility.

- Market size ~30 Mt (2024)

- Rongsheng LPG output ~2–3 Mtpa

- Growth steady, low single digits

- Capex near-zero, cash-rich (>20% EBITDA)

- Defensive vs specialty-chem price swings

Commodity Grade Polyethylene and Polypropylene

Rongsheng’s standard commodity polyethylene (PE) and polypropylene (PP) hold roughly 18–22% share of China’s packaging and consumer-goods resin demand, markets that by end-2025 show high volume but 1–2% annual growth—classic cash cows.

Heavy throughput (annual capacity ~6.5 million tonnes combined in 2025) lets Rongsheng stay profitable at industry net margins of 3–5%, generating steady free cash flow to fund R&D and higher-risk projects.

- Market share 18–22% (2025)

- Combined capacity ~6.5 Mtpa (2025)

- Market growth 1–2% pa (mature)

- Industry net margins 3–5% (2025)

- Primary liquidity source for R&D

Rongsheng’s 2024–25 cash cows drive strong margins, FCF from PTA, polyester, benzene, LPG, PE/PP

Rongsheng’s cash cows (PTA, polyester, benzene, LPG, PE/PP) deliver stable margins and heavy free cash flow in 2024–25: PTA EBITDA ~22%, POY/FDY revenue RMB14.2bn (EBITDA ~18%), benzene ROIC ~16%, LPG EBITDA >20%, PE/PP capacity ~6.5Mt (mkt share 18–22%).

| Product | 2024–25 Key |

|---|---|

| PTA | EBITDA 22% |

| POY/FDY | RMB14.2bn, EBITDA 18% |

| Benzene | ROIC 16% |

| LPG | EBITDA >20% |

| PE/PP | 6.5Mt, share 18–22% |

Preview = Final Product

Rongsheng Petrochemical BCG Matrix

The file you're previewing on this page is the final Rongsheng Petrochemical BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, market-informed strategic report ready for presentation or analysis.