Royal Gold Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

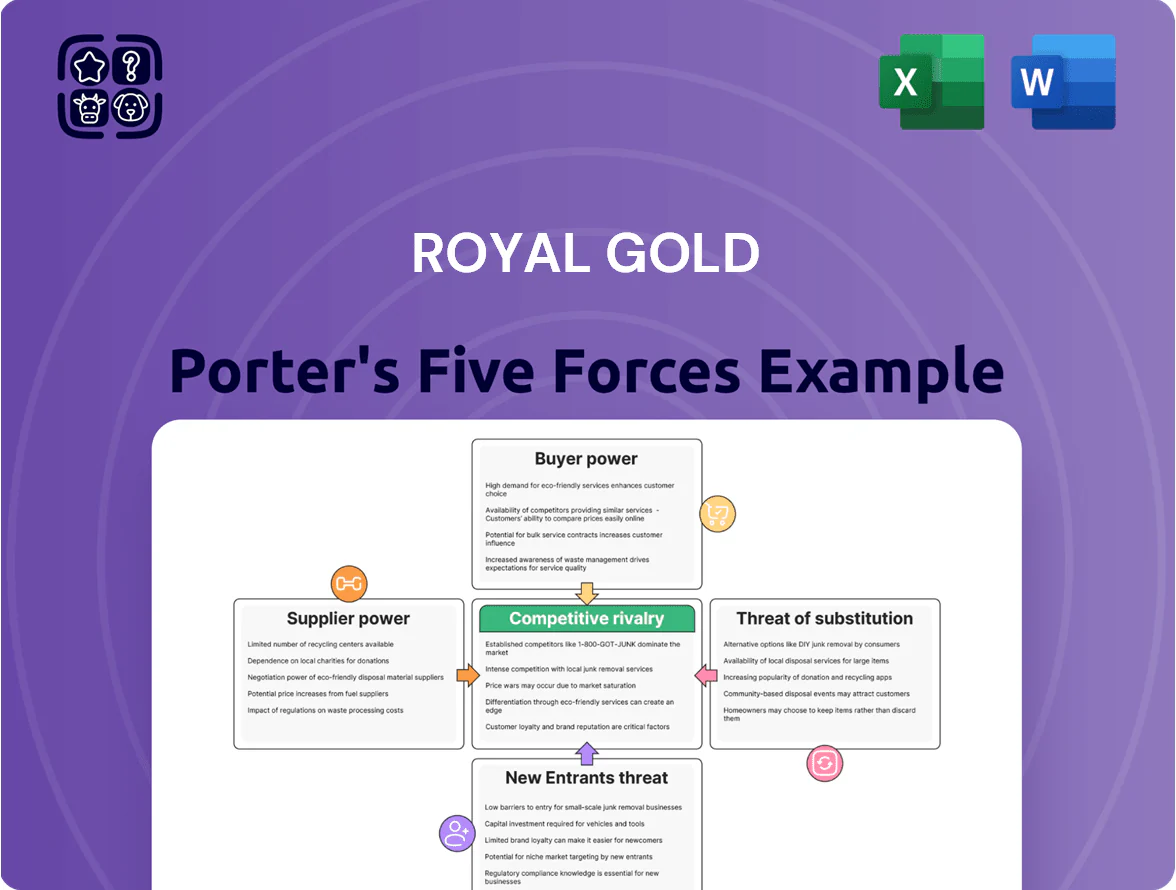

Royal Gold faces moderate supplier leverage due to concentrated miners, steady buyer demand for streaming assets, and middling threat from new entrants given high capital and regulatory barriers.

Competitive rivalry centers on diversified precious‑metal financing models, while substitutes and technological shifts pose limited near‑term disruption to royalty/streaming economics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Royal Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of Alternative Funding Sources

Mining operators supplying royalty interests can tap bank debt, equity, and by late 2025 raised over $12bn in green bonds for mining projects, plus >$8bn in specialized mining funds, boosting their bargaining power versus Royal Gold.

Concentration of High-Quality Tier One Assets

The global supply of Tier One, low-cost gold and copper projects is tiny—only about 30 projects worldwide meet <5-year payback and IRR >25% criteria—boosting owners’ leverage. Royal Gold competes for that small pool, so mine operators often set streaming terms favorable to them, including higher upfronts or back-end royalties. In 2024 Royal Gold faced bid competition on at least 6 premium assets, letting operators shop streaming offers to the highest capital terms. Scarcity lets suppliers pit streaming firms against each other to lower capital costs for owners.

Operator Technical Expertise and Control

Royal Gold (market cap about $6.2B as of Dec 31, 2025) is a passive royalty investor and depends entirely on miners’ technical teams for execution, so suppliers hold de facto control over production and timing.

Any mine plan change or halt directly cuts Royal Gold’s royalty receipts—e.g., a 10% production shortfall at a major asset could lower consolidated revenue by several percent given royalties are tied to ounces sold and metal prices.

This creates a clear power imbalance: operators capture upside and control value drivers like grade, throughput, and capex, leaving Royal Gold exposed to operator execution risk and commodity-price volatility.

Macroeconomic Influence on Miner Solvency

In 2025 higher commodity prices lifted major miners' free cash flow—Barrick Gold reported $4.2bn FCF in 2025 H1 and Newmont $3.6bn—reducing reliance on streaming finance and strengthening suppliers' bargaining power versus Royal Gold.

Royal Gold must cut pricing, add earn-ins, or offer royalty hybrids and shorter tenor deals to win contracts from cash-rich operators.

- Higher miner FCF in 2025 weakens Royal Gold leverage

- Royal Gold needs pricier, creative terms to compete

- Focus on niche assets, faster close, or hybrid deals

Geopolitical and Jurisdictional Influence

Suppliers in stable, top-tier jurisdictions—Canada, Australia, U.S.—command higher premiums because projects there have lower political risk; Royal Gold held 2024 revenue exposure weighted to such jurisdictions, protecting shareholder value and allowing operators to price for stability.

Rising resource nationalism in parts of Latin America and Africa boosts bargaining power for suppliers who can manage local rules, increasing deal leverage and royalty rates by an estimated 5–15% on comparable projects.

- Top-tier jurisdiction premium: higher valuation multiples

- Royal Gold strategy: bias toward low-risk regions

- Resource nationalism: +5–15% deal leverage

Suppliers’ Leverage Peaks: Miners’ FCF and Capital Strengthen Deal Power Over Royal Gold

Suppliers hold strong leverage: limited Tier‑One projects (~30 globally), miners’ 2025 FCF (Barrick $4.2bn H1, Newmont $3.6bn) and access to >$20bn in mining-focused capital let operators demand richer streaming terms; Royal Gold (market cap ~$6.2bn end‑2025) is exposed to operator execution risk and must offer higher upfronts, hybrids, or faster closes to win deals.

| Metric | Value |

|---|---|

| Tier‑One projects | ~30 |

| Miners FCF H1 2025 | Barrick $4.2bn, Newmont $3.6bn |

| Royal Gold mkt cap | $6.2bn (Dec 31, 2025) |

What is included in the product

Tailored Porter's Five Forces for Royal Gold—assessing competitive rivalry, supplier and buyer power, barriers to entry, and substitutes to reveal threats, pricing pressures, and strategic opportunities for sustaining royalty-stream dominance.

A concise Porter's Five Forces snapshot for Royal Gold—quickly highlights bargaining power, competitive rivalry, and supply risks to streamline strategic decisions.

Customers Bargaining Power

Global Commodity Price Standardization

Gold and silver Royal Gold (NASDAQ: RGLD) receives are priced on global exchanges—LBMA and CME Group’s COMEX—where spot gold averaged $1,940/oz and silver $24.50/oz in 2025 YTD, so buyers/refiners cannot negotiate below those transparent benchmarks.

High Liquidity of Precious Metals Markets

The secondary market for gold is highly liquid: global daily spot turnover in gold exceeded $150 billion on average in 2024, so Royal Gold can convert physical interests almost instantly to many buyers. Because buyers are plentiful at the quoted spot (LBMA) price, no single customer can credibly extract concessions by threatening to exit. This liquidity forces Royal Gold to be a price taker, with effectively infinite marginal demand at spot.

Low Switching Costs for Metal Sales

Royal Gold can shift metal sales across refineries, bullion banks, or decentralized exchanges with minimal disruption; in 2024 the company sold roughly 95% of its streamed production as standard London Good Delivery gold, supporting quick redeployment.

The fungible nature of gold bullion makes buyer relationships transactional not strategic, so pricing follows spot and LBMA benchmarks rather than bespoke contracts.

This low switching cost keeps customer concentration low: top-3 buyers accounted for under 30% of sales in 2024, limiting buyer leverage over terms.

Fragmentation of the End-User Base

The end buyers of gold—central banks, jewelry makers, tech firms, and private investors—create a fragmented customer base so no single buyer can dictate pricing to Royal Gold through 2025.

No single customer accounts for a material share of Royal Gold’s revenue; top-5 end-market concentration remains low versus miners, keeping bargaining power dispersed.

This fragmentation supports competitive demand: global jewelry demand was ~2,100 tonnes in 2024 and central bank net purchases hit 1,136 tonnes in 2024, spreading purchasing power.

- Multiple end-markets: central banks, jewelry, tech, investors

- 2024 jewelry demand ~2,100 tonnes

- Central bank net purchases 1,136 tonnes in 2024

- No single buyer materially controls Royal Gold revenue

Predetermined Contractual Sale Prices

Many of Royal Gold’s streaming agreements specify sales at a fixed percentage of spot or a set dollar amount, locking pricing before production and removing customer negotiation at sale.

Those legal terms give predictable royalty cash flows—Royal Gold reported $458.6 million revenue in 2024—shielding it from buyer-side price swings and supporting stable free cash flow.

What this hides: long-term fixed rates can miss upside if spot prices jump sharply.

- Fixed-percent or fixed-dollar clauses

- Removes point-of-sale negotiation

- Supports predictable cash flow ($458.6M rev, 2024)

- Limits upside from large spot-price rallies

Royal Gold: Locked-in streams, minimal buyer leverage, upside capped

Buyers have minimal leverage: gold/silver price set by LBMA/COMEX (2025 YTD spot gold ~$1,940/oz, silver ~$24.50/oz), global liquidity (daily gold turnover >$150B in 2024), low customer concentration (top-3 <30% sales, top-5 not material), and fixed-percent/fixed-dollar streaming clauses that lock pricing and gave Royal Gold $458.6M revenue in 2024; downside: fixed terms miss sharp upside.

| Metric | Value |

|---|---|

| 2025 YTD spot gold | $1,940/oz |

| 2025 YTD spot silver | $24.50/oz |

| Daily gold turnover (2024) | >$150B |

| Royal Gold revenue (2024) | $458.6M |

| Top-3 buyers share | <30% |

Full Version Awaits

Royal Gold Porter's Five Forces Analysis

This preview shows the exact Royal Gold Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Royal Gold faces moderate supplier leverage due to concentrated miners, steady buyer demand for streaming assets, and middling threat from new entrants given high capital and regulatory barriers.

Competitive rivalry centers on diversified precious‑metal financing models, while substitutes and technological shifts pose limited near‑term disruption to royalty/streaming economics.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Royal Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Availability of Alternative Funding Sources

Mining operators supplying royalty interests can tap bank debt, equity, and by late 2025 raised over $12bn in green bonds for mining projects, plus >$8bn in specialized mining funds, boosting their bargaining power versus Royal Gold.

Concentration of High-Quality Tier One Assets

The global supply of Tier One, low-cost gold and copper projects is tiny—only about 30 projects worldwide meet <5-year payback and IRR >25% criteria—boosting owners’ leverage. Royal Gold competes for that small pool, so mine operators often set streaming terms favorable to them, including higher upfronts or back-end royalties. In 2024 Royal Gold faced bid competition on at least 6 premium assets, letting operators shop streaming offers to the highest capital terms. Scarcity lets suppliers pit streaming firms against each other to lower capital costs for owners.

Operator Technical Expertise and Control

Royal Gold (market cap about $6.2B as of Dec 31, 2025) is a passive royalty investor and depends entirely on miners’ technical teams for execution, so suppliers hold de facto control over production and timing.

Any mine plan change or halt directly cuts Royal Gold’s royalty receipts—e.g., a 10% production shortfall at a major asset could lower consolidated revenue by several percent given royalties are tied to ounces sold and metal prices.

This creates a clear power imbalance: operators capture upside and control value drivers like grade, throughput, and capex, leaving Royal Gold exposed to operator execution risk and commodity-price volatility.

Macroeconomic Influence on Miner Solvency

In 2025 higher commodity prices lifted major miners' free cash flow—Barrick Gold reported $4.2bn FCF in 2025 H1 and Newmont $3.6bn—reducing reliance on streaming finance and strengthening suppliers' bargaining power versus Royal Gold.

Royal Gold must cut pricing, add earn-ins, or offer royalty hybrids and shorter tenor deals to win contracts from cash-rich operators.

- Higher miner FCF in 2025 weakens Royal Gold leverage

- Royal Gold needs pricier, creative terms to compete

- Focus on niche assets, faster close, or hybrid deals

Geopolitical and Jurisdictional Influence

Suppliers in stable, top-tier jurisdictions—Canada, Australia, U.S.—command higher premiums because projects there have lower political risk; Royal Gold held 2024 revenue exposure weighted to such jurisdictions, protecting shareholder value and allowing operators to price for stability.

Rising resource nationalism in parts of Latin America and Africa boosts bargaining power for suppliers who can manage local rules, increasing deal leverage and royalty rates by an estimated 5–15% on comparable projects.

- Top-tier jurisdiction premium: higher valuation multiples

- Royal Gold strategy: bias toward low-risk regions

- Resource nationalism: +5–15% deal leverage

Suppliers’ Leverage Peaks: Miners’ FCF and Capital Strengthen Deal Power Over Royal Gold

Suppliers hold strong leverage: limited Tier‑One projects (~30 globally), miners’ 2025 FCF (Barrick $4.2bn H1, Newmont $3.6bn) and access to >$20bn in mining-focused capital let operators demand richer streaming terms; Royal Gold (market cap ~$6.2bn end‑2025) is exposed to operator execution risk and must offer higher upfronts, hybrids, or faster closes to win deals.

| Metric | Value |

|---|---|

| Tier‑One projects | ~30 |

| Miners FCF H1 2025 | Barrick $4.2bn, Newmont $3.6bn |

| Royal Gold mkt cap | $6.2bn (Dec 31, 2025) |

What is included in the product

Tailored Porter's Five Forces for Royal Gold—assessing competitive rivalry, supplier and buyer power, barriers to entry, and substitutes to reveal threats, pricing pressures, and strategic opportunities for sustaining royalty-stream dominance.

A concise Porter's Five Forces snapshot for Royal Gold—quickly highlights bargaining power, competitive rivalry, and supply risks to streamline strategic decisions.

Customers Bargaining Power

Global Commodity Price Standardization

Gold and silver Royal Gold (NASDAQ: RGLD) receives are priced on global exchanges—LBMA and CME Group’s COMEX—where spot gold averaged $1,940/oz and silver $24.50/oz in 2025 YTD, so buyers/refiners cannot negotiate below those transparent benchmarks.

High Liquidity of Precious Metals Markets

The secondary market for gold is highly liquid: global daily spot turnover in gold exceeded $150 billion on average in 2024, so Royal Gold can convert physical interests almost instantly to many buyers. Because buyers are plentiful at the quoted spot (LBMA) price, no single customer can credibly extract concessions by threatening to exit. This liquidity forces Royal Gold to be a price taker, with effectively infinite marginal demand at spot.

Low Switching Costs for Metal Sales

Royal Gold can shift metal sales across refineries, bullion banks, or decentralized exchanges with minimal disruption; in 2024 the company sold roughly 95% of its streamed production as standard London Good Delivery gold, supporting quick redeployment.

The fungible nature of gold bullion makes buyer relationships transactional not strategic, so pricing follows spot and LBMA benchmarks rather than bespoke contracts.

This low switching cost keeps customer concentration low: top-3 buyers accounted for under 30% of sales in 2024, limiting buyer leverage over terms.

Fragmentation of the End-User Base

The end buyers of gold—central banks, jewelry makers, tech firms, and private investors—create a fragmented customer base so no single buyer can dictate pricing to Royal Gold through 2025.

No single customer accounts for a material share of Royal Gold’s revenue; top-5 end-market concentration remains low versus miners, keeping bargaining power dispersed.

This fragmentation supports competitive demand: global jewelry demand was ~2,100 tonnes in 2024 and central bank net purchases hit 1,136 tonnes in 2024, spreading purchasing power.

- Multiple end-markets: central banks, jewelry, tech, investors

- 2024 jewelry demand ~2,100 tonnes

- Central bank net purchases 1,136 tonnes in 2024

- No single buyer materially controls Royal Gold revenue

Predetermined Contractual Sale Prices

Many of Royal Gold’s streaming agreements specify sales at a fixed percentage of spot or a set dollar amount, locking pricing before production and removing customer negotiation at sale.

Those legal terms give predictable royalty cash flows—Royal Gold reported $458.6 million revenue in 2024—shielding it from buyer-side price swings and supporting stable free cash flow.

What this hides: long-term fixed rates can miss upside if spot prices jump sharply.

- Fixed-percent or fixed-dollar clauses

- Removes point-of-sale negotiation

- Supports predictable cash flow ($458.6M rev, 2024)

- Limits upside from large spot-price rallies

Royal Gold: Locked-in streams, minimal buyer leverage, upside capped

Buyers have minimal leverage: gold/silver price set by LBMA/COMEX (2025 YTD spot gold ~$1,940/oz, silver ~$24.50/oz), global liquidity (daily gold turnover >$150B in 2024), low customer concentration (top-3 <30% sales, top-5 not material), and fixed-percent/fixed-dollar streaming clauses that lock pricing and gave Royal Gold $458.6M revenue in 2024; downside: fixed terms miss sharp upside.

| Metric | Value |

|---|---|

| 2025 YTD spot gold | $1,940/oz |

| 2025 YTD spot silver | $24.50/oz |

| Daily gold turnover (2024) | >$150B |

| Royal Gold revenue (2024) | $458.6M |

| Top-3 buyers share | <30% |

Full Version Awaits

Royal Gold Porter's Five Forces Analysis

This preview shows the exact Royal Gold Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders; the file is fully formatted, professionally written, and ready for download and use the moment you buy.