Royal Gold PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Royal Gold’s outlook—our concise PESTLE highlights key external drivers and strategic implications to inform investment and planning decisions. Purchase the full analysis for the complete, actionable breakdown and ready-to-use charts you can apply instantly.

Political factors

Geopolitical Stability in Tier-1 Jurisdictions

Royal Gold concentrates ~78% of 2024 revenue-linked assets in Canada, Australia and the US, reducing expropriation risk while exposing cash flows to stable-tier political environments.

Even in these jurisdictions, 2023–2025 state/provincial tax changes and land-use rulings—e.g., Western Australia royalty reviews and US state-level permitting shifts—have altered partner mine economics by up to mid-single-digit percentage points.

As of late 2025 decision-makers should assess each asset's regional political volatility scores and two- to five-year tax/policy outlooks to safeguard projected NAV and distributable cash flow.

Resource Nationalism in Emerging Markets

Operations in emerging markets face rising resource nationalism; by 2025 at least 15 countries raised mining royalties or imposed carried state interests, seeking revenue from elevated commodity prices—gold averaged about 1,950 USD/oz in 2024—heightening fiscal grabs.

Royal Gold's royalty/streaming model and 2024 revenue diversification (over 60% from North American and low‑risk assets) mitigates exposure, but analysts flag abrupt host‑country code changes as a primary operational risk.

Permitting and Regulatory Delays

The tightening political landscape has increased permitting complexity as regulators juggle growth and conservation; in 2024 average federal permitting timelines for major mining projects in the US and Canada stretched to 3–7 years, up ~20% vs 2019, raising policy risk for Royal Gold.

Permitting delays that defer production by even 12–36 months can cut near-term royalty cash flows, moving expected revenue receipts and lowering project IRRs; a one-year delay typically reduces NPV by roughly 5–12% at a 6–8% discount rate for development-stage gold assets.

Analysts must build probabilistic permit timelines into DCFs and scenario models—assigning longer-tail distributions to approval dates and applying sensitivity tests—since delayed federal or provincial approvals materially shift Royal Gold’s projected free cash flow and valuation.

International Trade Policies and Sanctions

Global trade tensions and sanctions can disrupt precious metals flows and cross-border delivery of mining equipment, with 2024-25 WTO disputes up 12% year-over-year affecting export permits for key jurisdictions; delayed shipments have raised operational lead times by an estimated 8-15% for miners in sanction-prone regions.

Shifting alliances through late 2025 increase logistical complexity for Royal Gold partners in jurisdictions like Kazakhstan and West Africa, where 2024 trade restrictions led to at least two project delays exceeding six months.

These geopolitical frictions demand continuous monitoring to gauge indirect impacts on Royal Gold’s royalty and stream delivery schedules and potential revenue timing shifts of several million dollars per delayed project.

- WTO disputes +12% (2024 vs 2023)

- Equipment lead times +8–15% in restricted regions

- At least two partner project delays >6 months (2024, Kazakhstan/West Africa)

- Potential multi-million-dollar revenue timing risk per delayed project

Government Incentives for Critical Minerals

Government incentives for critical minerals in the US and EU—e.g., US IRA credits and EU Critical Raw Materials Act funding—raise demand for copper and battery metals produced alongside precious metals, indirectly boosting royalty streams for Royal Gold from polymetallic partners. North American and European subsidies (estimated billions annually; US CHIPS/IRA allocations >$300bn through 2024–25) accelerate mine development where Royal Gold holds secondary royalties, extending asset life and portfolio value.

- Royal Gold indirect exposure via secondary royalties on polymetallic mines

- US/EU incentives (> $300bn+ IRA/related allocations 2024–25) accelerate development

- Political support improves project longevity and potential royalty uplift

High revenue concentration, rising royalties and delays threaten project NPV—monitor policy

Concentrated 78% 2024 revenue in Canada/Australia/US limits expropriation risk; 2023–25 royalty/tax reviews (WA, US states) altered partner cash flows mid-single digits. Permitting delays (US/Canada 3–7 yrs in 2024, +20% vs 2019) and rising resource nationalism (15+ countries raised royalties by 2025) pose timing and NPV risks; monitor policy outlooks in DCFs.

| Metric | 2024–25 |

|---|---|

| Revenue concentration | ~78% |

| Permitting timeline | 3–7 yrs (+20%) |

| Countries raising royalties | 15+ |

| Gold price (2024 avg) | ~1,950 USD/oz |

What is included in the product

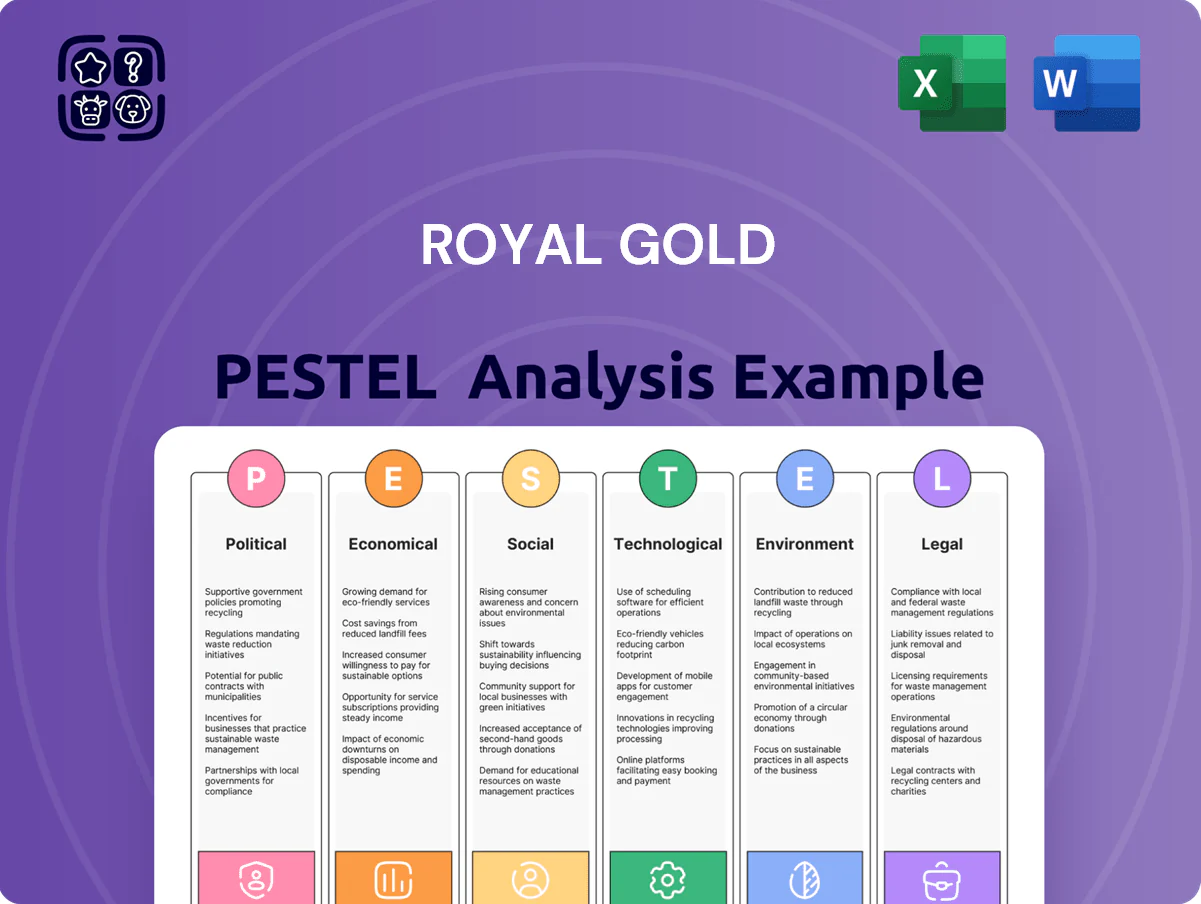

Explores how external macro-environmental factors uniquely affect Royal Gold across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify risks, opportunities, and strategic implications for executives, investors, and advisors.

A concise, PESTLE-segmented summary of Royal Gold that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory impacts, and market positioning for faster, aligned decision-making.

Economic factors

Precious Metal Price Volatility

The primary driver of Royal Gold's revenue is gold and silver prices; gold averaged about 2,120 USD/oz in 2025 YTD amid central bank buying, while silver averaged ~26 USD/oz, both reflecting safe-haven demand during geopolitical and macro uncertainty.

Price swings remain significant—gold moved ±15% in 2024–25—and investors should run sensitivity analyses showing how 5–20% price declines affect Royal Gold's cash flow and capacity to fund new royalty acquisitions, given its payout and acquisition model.

Inflationary Pressures on Mine Operators

While Royal Gold does not bear direct mine operating costs, US inflation running near 3.4% in 2024 raises input costs for operators, compressing margins and elevating risk of mine suspension that would stop royalty flows.

If inflation-driven higher diesel, labor and reagent costs push a mine above its cut‑off, operators may curtail production; in 2023 commodity‑linked cost inflation led to temporary suspensions at several higher‑cost gold mines.

Analysts must assess partner mines' cost‑curve positions—those in the top quartile of cash costs face the highest shutdown risk, directly threatening Royal Gold's revenue visibility.

Global Interest Rate Environment

Rising global rates raised Royal Gold's WACC, with US 10-year Treasury yields climbing to ~4.5% by Dec 2025, lifting discount rates used in DCFs and lowering present values of future streaming cash flows.

Higher borrowing costs increased the effective cost of financing new streams; industry commentary in late 2025 noted senior unsecured borrowing spreads for mining finance widened to ~250–350 bps.

As policy rates normalized, investors favored cash-yielding fixed income, pressuring yield-focused royalty multiples—Royal Gold's forward EV/EBITDA traded nearer to a 10–15% discount versus long-term averages in late 2025.

Currency Exchange Rate Fluctuations

Royal Gold reports in U.S. dollars while many partner mines operate in currencies like CAD and CLP; a 10% depreciation of the Chilean Peso in 2023 reduced local wage/energy costs for miners, often extending mine life and boosting royalty volumes.

A strong U.S. dollar—up ~6% vs a trade-weighted basket in 2024—can pressure gold prices (gold fell ~2% in periods of USD strength), creating valuation headwinds despite local cost advantages.

- USD reporting vs CAD/CLP exposure

- 10% CLP depreciation in 2023 lowered local costs

- USD +6% in 2024 correlated with ~2% gold weakness

Capital Market Accessibility for Junior Miners

Royal Gold frequently finances junior miners who face limited access to equity/debt; in 2025 the royalty/stream model benefits as alternative financing grew—royalty market deal value rose to about $4.2bn globally in 2024–25, easing project funding gaps.

When traditional capital is scarce or costly (global bond yields averaging ~4.5% in 2025), Royal Gold secures more favorable terms on new royalties/streams, boosting long-term NAV and shareholder value.

- Royalty/stream market ~ $4.2bn (2024–25)

- Global bond yields ~4.5% (2025)

- Royal Gold leverages scarcity to negotiate premium pricing and protections

Gold at $2,120, rates up, royalties $4.2B: higher WACC squeezes mining valuations

Gold ~2,120 USD/oz (2025 YTD); silver ~26 USD/oz; gold ±15% (2024–25) impacting cash flows. US inflation ~3.4% (2024) raises operator costs, risking mine suspensions. US 10y ~4.5% (Dec 2025) lifted WACC, compressing DCF values; royalty market ≈$4.2bn (2024–25), aiding deal flow.

| Metric | Value |

|---|---|

| Gold | 2,120 USD/oz |

| 10y Treasury | 4.5% |

| Royalty market | $4.2bn |

Preview Before You Purchase

Royal Gold PESTLE Analysis

The preview shown here is the exact Royal Gold PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or presentation.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, commodity cycles, and environmental regulations are reshaping Royal Gold’s outlook—our concise PESTLE highlights key external drivers and strategic implications to inform investment and planning decisions. Purchase the full analysis for the complete, actionable breakdown and ready-to-use charts you can apply instantly.

Political factors

Geopolitical Stability in Tier-1 Jurisdictions

Royal Gold concentrates ~78% of 2024 revenue-linked assets in Canada, Australia and the US, reducing expropriation risk while exposing cash flows to stable-tier political environments.

Even in these jurisdictions, 2023–2025 state/provincial tax changes and land-use rulings—e.g., Western Australia royalty reviews and US state-level permitting shifts—have altered partner mine economics by up to mid-single-digit percentage points.

As of late 2025 decision-makers should assess each asset's regional political volatility scores and two- to five-year tax/policy outlooks to safeguard projected NAV and distributable cash flow.

Resource Nationalism in Emerging Markets

Operations in emerging markets face rising resource nationalism; by 2025 at least 15 countries raised mining royalties or imposed carried state interests, seeking revenue from elevated commodity prices—gold averaged about 1,950 USD/oz in 2024—heightening fiscal grabs.

Royal Gold's royalty/streaming model and 2024 revenue diversification (over 60% from North American and low‑risk assets) mitigates exposure, but analysts flag abrupt host‑country code changes as a primary operational risk.

Permitting and Regulatory Delays

The tightening political landscape has increased permitting complexity as regulators juggle growth and conservation; in 2024 average federal permitting timelines for major mining projects in the US and Canada stretched to 3–7 years, up ~20% vs 2019, raising policy risk for Royal Gold.

Permitting delays that defer production by even 12–36 months can cut near-term royalty cash flows, moving expected revenue receipts and lowering project IRRs; a one-year delay typically reduces NPV by roughly 5–12% at a 6–8% discount rate for development-stage gold assets.

Analysts must build probabilistic permit timelines into DCFs and scenario models—assigning longer-tail distributions to approval dates and applying sensitivity tests—since delayed federal or provincial approvals materially shift Royal Gold’s projected free cash flow and valuation.

International Trade Policies and Sanctions

Global trade tensions and sanctions can disrupt precious metals flows and cross-border delivery of mining equipment, with 2024-25 WTO disputes up 12% year-over-year affecting export permits for key jurisdictions; delayed shipments have raised operational lead times by an estimated 8-15% for miners in sanction-prone regions.

Shifting alliances through late 2025 increase logistical complexity for Royal Gold partners in jurisdictions like Kazakhstan and West Africa, where 2024 trade restrictions led to at least two project delays exceeding six months.

These geopolitical frictions demand continuous monitoring to gauge indirect impacts on Royal Gold’s royalty and stream delivery schedules and potential revenue timing shifts of several million dollars per delayed project.

- WTO disputes +12% (2024 vs 2023)

- Equipment lead times +8–15% in restricted regions

- At least two partner project delays >6 months (2024, Kazakhstan/West Africa)

- Potential multi-million-dollar revenue timing risk per delayed project

Government Incentives for Critical Minerals

Government incentives for critical minerals in the US and EU—e.g., US IRA credits and EU Critical Raw Materials Act funding—raise demand for copper and battery metals produced alongside precious metals, indirectly boosting royalty streams for Royal Gold from polymetallic partners. North American and European subsidies (estimated billions annually; US CHIPS/IRA allocations >$300bn through 2024–25) accelerate mine development where Royal Gold holds secondary royalties, extending asset life and portfolio value.

- Royal Gold indirect exposure via secondary royalties on polymetallic mines

- US/EU incentives (> $300bn+ IRA/related allocations 2024–25) accelerate development

- Political support improves project longevity and potential royalty uplift

High revenue concentration, rising royalties and delays threaten project NPV—monitor policy

Concentrated 78% 2024 revenue in Canada/Australia/US limits expropriation risk; 2023–25 royalty/tax reviews (WA, US states) altered partner cash flows mid-single digits. Permitting delays (US/Canada 3–7 yrs in 2024, +20% vs 2019) and rising resource nationalism (15+ countries raised royalties by 2025) pose timing and NPV risks; monitor policy outlooks in DCFs.

| Metric | 2024–25 |

|---|---|

| Revenue concentration | ~78% |

| Permitting timeline | 3–7 yrs (+20%) |

| Countries raising royalties | 15+ |

| Gold price (2024 avg) | ~1,950 USD/oz |

What is included in the product

Explores how external macro-environmental factors uniquely affect Royal Gold across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trends to identify risks, opportunities, and strategic implications for executives, investors, and advisors.

A concise, PESTLE-segmented summary of Royal Gold that’s easily dropped into presentations or shared across teams, helping stakeholders quickly assess external risks, regulatory impacts, and market positioning for faster, aligned decision-making.

Economic factors

Precious Metal Price Volatility

The primary driver of Royal Gold's revenue is gold and silver prices; gold averaged about 2,120 USD/oz in 2025 YTD amid central bank buying, while silver averaged ~26 USD/oz, both reflecting safe-haven demand during geopolitical and macro uncertainty.

Price swings remain significant—gold moved ±15% in 2024–25—and investors should run sensitivity analyses showing how 5–20% price declines affect Royal Gold's cash flow and capacity to fund new royalty acquisitions, given its payout and acquisition model.

Inflationary Pressures on Mine Operators

While Royal Gold does not bear direct mine operating costs, US inflation running near 3.4% in 2024 raises input costs for operators, compressing margins and elevating risk of mine suspension that would stop royalty flows.

If inflation-driven higher diesel, labor and reagent costs push a mine above its cut‑off, operators may curtail production; in 2023 commodity‑linked cost inflation led to temporary suspensions at several higher‑cost gold mines.

Analysts must assess partner mines' cost‑curve positions—those in the top quartile of cash costs face the highest shutdown risk, directly threatening Royal Gold's revenue visibility.

Global Interest Rate Environment

Rising global rates raised Royal Gold's WACC, with US 10-year Treasury yields climbing to ~4.5% by Dec 2025, lifting discount rates used in DCFs and lowering present values of future streaming cash flows.

Higher borrowing costs increased the effective cost of financing new streams; industry commentary in late 2025 noted senior unsecured borrowing spreads for mining finance widened to ~250–350 bps.

As policy rates normalized, investors favored cash-yielding fixed income, pressuring yield-focused royalty multiples—Royal Gold's forward EV/EBITDA traded nearer to a 10–15% discount versus long-term averages in late 2025.

Currency Exchange Rate Fluctuations

Royal Gold reports in U.S. dollars while many partner mines operate in currencies like CAD and CLP; a 10% depreciation of the Chilean Peso in 2023 reduced local wage/energy costs for miners, often extending mine life and boosting royalty volumes.

A strong U.S. dollar—up ~6% vs a trade-weighted basket in 2024—can pressure gold prices (gold fell ~2% in periods of USD strength), creating valuation headwinds despite local cost advantages.

- USD reporting vs CAD/CLP exposure

- 10% CLP depreciation in 2023 lowered local costs

- USD +6% in 2024 correlated with ~2% gold weakness

Capital Market Accessibility for Junior Miners

Royal Gold frequently finances junior miners who face limited access to equity/debt; in 2025 the royalty/stream model benefits as alternative financing grew—royalty market deal value rose to about $4.2bn globally in 2024–25, easing project funding gaps.

When traditional capital is scarce or costly (global bond yields averaging ~4.5% in 2025), Royal Gold secures more favorable terms on new royalties/streams, boosting long-term NAV and shareholder value.

- Royalty/stream market ~ $4.2bn (2024–25)

- Global bond yields ~4.5% (2025)

- Royal Gold leverages scarcity to negotiate premium pricing and protections

Gold at $2,120, rates up, royalties $4.2B: higher WACC squeezes mining valuations

Gold ~2,120 USD/oz (2025 YTD); silver ~26 USD/oz; gold ±15% (2024–25) impacting cash flows. US inflation ~3.4% (2024) raises operator costs, risking mine suspensions. US 10y ~4.5% (Dec 2025) lifted WACC, compressing DCF values; royalty market ≈$4.2bn (2024–25), aiding deal flow.

| Metric | Value |

|---|---|

| Gold | 2,120 USD/oz |

| 10y Treasury | 4.5% |

| Royalty market | $4.2bn |

Preview Before You Purchase

Royal Gold PESTLE Analysis

The preview shown here is the exact Royal Gold PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for analysis or presentation.