RPC, Inc. Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

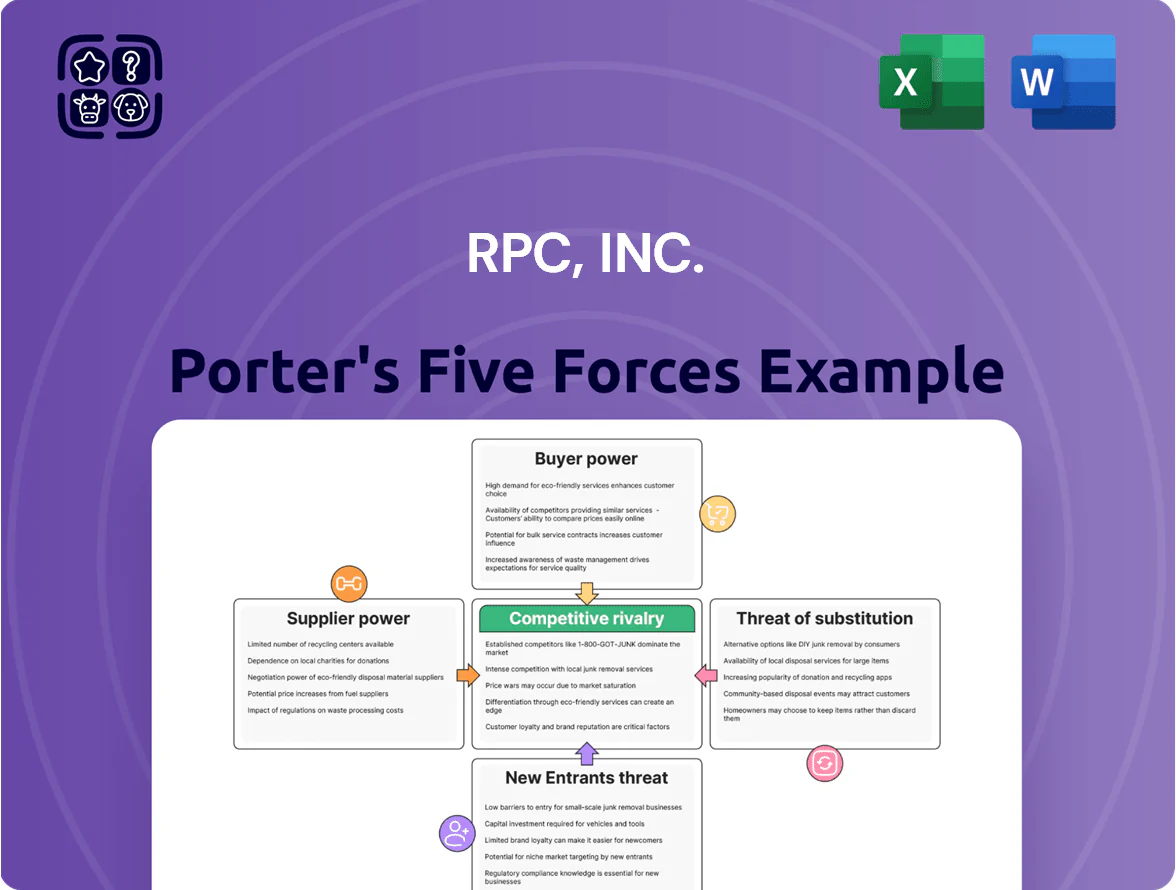

RPC, Inc.'s competitive landscape is shaped by intense rivalry among established players and the constant threat of new entrants, impacting pricing power and profitability. Understanding the influence of powerful suppliers and the availability of substitute services is crucial for strategic positioning.

The complete report reveals the real forces shaping RPC, Inc.’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Specialized Equipment and Technology

RPC, Inc. depends on specialized manufacturers for critical oilfield equipment like advanced pressure pumping units and downhole tools. This reliance means suppliers of these unique components hold significant sway.

The industry's shift towards lower-emission equipment, such as Tier 4 DGB and electric fleets, further amplifies supplier power. RPC must secure these advanced technologies, potentially increasing the leverage of those who provide them.

This dependence on specific manufacturers for technologically advanced machinery directly impacts RPC's operational flexibility and capital expenditure decisions, as acquiring or maintaining access to these specialized assets is paramount.

Availability of Key Raw Materials

The availability and cost of frac sand, a vital proppant for RPC's hydraulic fracturing services, significantly influence supplier bargaining power. Despite the move towards in-basin sand to cut transportation expenses, the robust demand for frac sand in unconventional oil and gas extraction grants suppliers considerable leverage.

Logistical challenges within the frac sand supply chain can disrupt consistent deliveries, directly impacting RPC's operational efficiency and overall costs. For instance, in early 2024, disruptions in rail and trucking capacity led to increased lead times and higher prices for sand, a key input for RPC's completion services.

Skilled Labor Shortages

The oilfield services sector, where RPC, Inc. operates, grapples with ongoing shortages of skilled labor and critical skill gaps in technical and operational positions. This scarcity directly impacts labor costs, forcing companies to offer higher wages to attract and retain qualified personnel. For instance, in early 2024, the industry continued to experience difficulties filling roles requiring specialized expertise, a trend that began to intensify following the pandemic-induced employment downturn.

This difficulty in staffing projects adequately translates into increased bargaining power for skilled workers and the companies that can supply them. The uneven recovery of employment in oil and gas extraction occupations, as noted by various industry reports throughout 2023 and into 2024, highlights the persistent demand for experienced professionals, further empowering these labor sources.

Supplier Concentration and Differentiation

The bargaining power of suppliers for RPC, Inc. is influenced by the concentration and differentiation of their offerings within the oilfield services sector. Suppliers providing highly specialized components or unique technologies, especially those that are proprietary or lack close substitutes, can wield considerable influence over pricing and terms. This is particularly relevant for critical parts or software that are essential for RPC's specialized service delivery, such as advanced drilling or completion technologies.

For instance, if a supplier offers a patented chemical additive that significantly improves well productivity or a unique piece of downhole equipment with no direct alternatives, RPC's reliance on that supplier increases their leverage. This situation is amplified when the supplier's product is vital for meeting stringent environmental regulations or achieving operational efficiencies that are key competitive advantages for RPC.

- Supplier Concentration: A limited number of suppliers for critical raw materials or specialized equipment can lead to higher bargaining power for those suppliers.

- Technological Differentiation: Suppliers offering unique, patented, or highly advanced technologies that are essential for RPC's service offerings possess greater leverage.

- Switching Costs: High costs associated with changing suppliers for specialized components or software can solidify a supplier's bargaining power.

- Importance of Input: When a supplier's product represents a significant portion of RPC's cost structure or is critical to service performance, the supplier's power is enhanced.

Switching Costs for RPC

Switching suppliers for RPC, Inc. can be a costly endeavor. For instance, the expense of retooling manufacturing lines to accommodate new equipment or retraining staff on different operational procedures can easily run into millions of dollars. This financial barrier significantly limits RPC's ability to readily change its suppliers, giving existing vendors more leverage.

These substantial switching costs directly enhance the bargaining power of RPC's current suppliers. When a company like RPC faces significant disruption and expense in finding and integrating a new supplier, the existing supplier can often dictate terms more effectively. This dynamic is a key factor in assessing supplier power.

Furthermore, long-term supply agreements and deeply integrated supply chain relationships can further solidify RPC's reliance on its existing vendors. These arrangements create a sticky situation, making it even more challenging and expensive for RPC to explore alternative sourcing options, thereby reinforcing supplier influence.

- High Retooling Costs: Implementing new specialized equipment can require substantial capital investment for RPC, potentially millions of dollars depending on the technology.

- Personnel Training Expenses: Educating employees on new machinery or processes associated with a different supplier adds to the overall switching cost burden.

- Operational Downtime: The transition period between suppliers can lead to production halts, resulting in lost revenue and increased operational expenses for RPC.

- Contractual Lock-ins: Existing long-term contracts with suppliers may include penalties for early termination, further increasing the cost of switching.

Supplier Power Shapes Oilfield Services Landscape

RPC, Inc. faces significant bargaining power from its suppliers, particularly for specialized oilfield equipment and essential materials like frac sand. The industry's move towards advanced, lower-emission technologies further concentrates power among suppliers who can provide these critical components. For instance, in early 2024, disruptions in logistics for frac sand led to increased lead times and prices, directly impacting RPC's completion services.

The scarcity of skilled labor in the oilfield services sector also empowers labor suppliers and skilled workers, driving up costs for RPC. This trend, noted throughout 2023 and into 2024, highlights the persistent demand for experienced professionals. Furthermore, high switching costs, including retooling and training, can run into millions of dollars, solidifying the leverage of existing vendors.

| Supplier Factor | Impact on RPC, Inc. | 2024 Data/Trend |

|---|---|---|

| Specialized Equipment Reliance | High dependence on unique manufacturers | Continued demand for advanced pressure pumping units and downhole tools |

| Technological Advancements | Need to secure lower-emission technologies | Increased leverage for suppliers of Tier 4 DGB and electric fleet components |

| Frac Sand Availability | Critical input for hydraulic fracturing | Robust demand in early 2024 led to higher prices and longer lead times due to logistical challenges |

| Skilled Labor Shortages | Increased labor costs and operational challenges | Persistent difficulty in filling specialized roles throughout 2023-2024 |

| Switching Costs | Millions in retooling and training | Significant financial barriers limit RPC's ability to change suppliers |

What is included in the product

This analysis evaluates the competitive landscape for RPC, Inc., examining the intensity of rivalry, buyer and supplier power, threat of new entrants and substitutes.

RPC, Inc.'s Porter's Five Forces analysis offers a clear, one-sheet summary, pinpointing strategic pressures to relieve the pain of complex market assessments.

Customers Bargaining Power

Customer Concentration and Purchasing Volume

RPC, Inc.'s customer base is largely concentrated within the independent and major oil and gas sectors. This concentration is highlighted by its 2024 financial disclosures, which revealed that two private exploration and production (E&P) companies individually contributed around 13% and 11% to its total revenue.

This significant customer concentration translates directly into enhanced bargaining power for these large clients. Their substantial purchasing volumes and critical importance to RPC's revenue streams empower them to negotiate more favorable pricing structures and contract terms, thereby influencing RPC's profitability and operational flexibility.

Sensitivity to Oil and Gas Prices and E&P Capex

RPC, Inc.'s revenue is closely tied to the capital expenditure (Capex) decisions of oil and gas exploration and production (E&P) companies. These decisions are heavily influenced by fluctuating oil and natural gas prices. When energy prices dip, customers tend to cut back on drilling and new well development, directly impacting RPC's service demand.

For instance, a significant slowdown in US E&P Capex was observed throughout 2024. Projections for 2025 also indicated continued declines in this spending. This environment inherently strengthens the bargaining power of RPC's customers, as they have fewer alternatives and are more cost-conscious during periods of reduced energy commodity prices.

Oversupply of Oilfield Services Capacity

The oilfield services sector has seen a significant oversupply of capacity. This is partly because exploration and production (E&P) companies are now more efficient, needing fewer rigs to meet their production goals. This surplus of available services means customers have more choices and can push for lower prices and improved service.

This dynamic directly impacts companies like RPC, Inc. In 2024, RPC specifically cited these competitive pricing pressures as a contributing factor to its revenue decline. The bargaining power of customers is amplified when there's more capacity than demand, forcing service providers to compete more aggressively on price.

Consolidation Among E&P Companies

The ongoing consolidation within the exploration and production (E&P) sector is a significant factor impacting the bargaining power of RPC, Inc.'s customers. As fewer, larger entities emerge, their collective buying power intensifies, allowing them to demand more favorable terms from service providers like RPC.

These consolidated E&P companies are better positioned to negotiate lower prices and seek integrated service packages, putting pressure on RPC’s margins. This trend has already manifested in customer attrition for RPC, highlighting the direct impact of this industry consolidation on its client base.

- Increased Buyer Power: Larger E&P companies resulting from consolidation can leverage their scale to negotiate better pricing and terms with oilfield service providers.

- Demand for Integrated Services: Consolidated entities often prefer fewer, more comprehensive service providers, potentially squeezing out smaller or specialized firms.

- Customer Loss Impact: RPC has directly experienced a reduction in its customer base due to this consolidation trend, indicating a tangible loss of business.

Low Switching Costs for Customers

Customers of RPC, Inc. often experience low switching costs. This is largely due to the short lead times between ordering oilfield services and their actual delivery. This means clients can readily explore other providers if they find better pricing or terms elsewhere.

This ease of switching significantly enhances customer bargaining power. In 2024, the oilfield services sector continued to see a dynamic competitive landscape, with numerous players vying for contracts. This competitive environment naturally provides customers with a wide array of choices, reinforcing their ability to negotiate favorable terms with companies like RPC.

- Short Lead Times: Services are often delivered quickly, reducing commitment.

- Price Sensitivity: Customers can easily shop around for the best deals.

- Competitive Market: Numerous providers mean customers have ample alternatives.

Powerful Customers Drive RPC's 2024 Revenue Challenges

RPC, Inc.'s customers, particularly large independent and major oil and gas companies, wield significant bargaining power. This is evident in their substantial revenue contribution, with two private E&P companies alone accounting for approximately 13% and 11% of RPC's total revenue in 2024. This concentration allows these clients to negotiate favorable pricing and contract terms, directly impacting RPC's profitability.

The oilfield services market in 2024 was characterized by oversupply and increased efficiency from E&P companies, meaning fewer rigs are needed. This surplus of capacity strengthens customer bargaining power, as they have more options and are more cost-conscious, especially during periods of lower energy prices. This competitive pressure was a cited reason for RPC's revenue decline in 2024.

Consolidation within the E&P sector further amplifies customer bargaining power. Larger, merged entities can leverage their increased scale to demand better terms and integrated service packages, leading to customer attrition for RPC. Additionally, low switching costs due to short lead times for services allow customers to easily move to competitors, reinforcing their negotiating leverage in a dynamic market.

| Customer Factor | Impact on RPC, Inc. | 2024 Data/Observation |

|---|---|---|

| Customer Concentration | Increased bargaining power for large clients | Two private E&P companies contributed ~13% and ~11% of total revenue. |

| Market Oversupply & Efficiency | Customers can demand lower prices and better terms | Oversupply of capacity; E&P companies require fewer rigs. |

| E&P Sector Consolidation | Larger buyers exert greater influence | Leading to customer attrition for RPC. |

| Low Switching Costs | Customers can easily switch providers | Short lead times for services in a competitive market. |

Preview Before You Purchase

RPC, Inc. Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for RPC, Inc., offering a detailed examination of industry competitiveness. The document you see here is the exact, professionally formatted analysis you'll receive immediately after purchase, ensuring full transparency and immediate utility for your strategic planning.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

RPC, Inc.'s competitive landscape is shaped by intense rivalry among established players and the constant threat of new entrants, impacting pricing power and profitability. Understanding the influence of powerful suppliers and the availability of substitute services is crucial for strategic positioning.

The complete report reveals the real forces shaping RPC, Inc.’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Access to Specialized Equipment and Technology

RPC, Inc. depends on specialized manufacturers for critical oilfield equipment like advanced pressure pumping units and downhole tools. This reliance means suppliers of these unique components hold significant sway.

The industry's shift towards lower-emission equipment, such as Tier 4 DGB and electric fleets, further amplifies supplier power. RPC must secure these advanced technologies, potentially increasing the leverage of those who provide them.

This dependence on specific manufacturers for technologically advanced machinery directly impacts RPC's operational flexibility and capital expenditure decisions, as acquiring or maintaining access to these specialized assets is paramount.

Availability of Key Raw Materials

The availability and cost of frac sand, a vital proppant for RPC's hydraulic fracturing services, significantly influence supplier bargaining power. Despite the move towards in-basin sand to cut transportation expenses, the robust demand for frac sand in unconventional oil and gas extraction grants suppliers considerable leverage.

Logistical challenges within the frac sand supply chain can disrupt consistent deliveries, directly impacting RPC's operational efficiency and overall costs. For instance, in early 2024, disruptions in rail and trucking capacity led to increased lead times and higher prices for sand, a key input for RPC's completion services.

Skilled Labor Shortages

The oilfield services sector, where RPC, Inc. operates, grapples with ongoing shortages of skilled labor and critical skill gaps in technical and operational positions. This scarcity directly impacts labor costs, forcing companies to offer higher wages to attract and retain qualified personnel. For instance, in early 2024, the industry continued to experience difficulties filling roles requiring specialized expertise, a trend that began to intensify following the pandemic-induced employment downturn.

This difficulty in staffing projects adequately translates into increased bargaining power for skilled workers and the companies that can supply them. The uneven recovery of employment in oil and gas extraction occupations, as noted by various industry reports throughout 2023 and into 2024, highlights the persistent demand for experienced professionals, further empowering these labor sources.

Supplier Concentration and Differentiation

The bargaining power of suppliers for RPC, Inc. is influenced by the concentration and differentiation of their offerings within the oilfield services sector. Suppliers providing highly specialized components or unique technologies, especially those that are proprietary or lack close substitutes, can wield considerable influence over pricing and terms. This is particularly relevant for critical parts or software that are essential for RPC's specialized service delivery, such as advanced drilling or completion technologies.

For instance, if a supplier offers a patented chemical additive that significantly improves well productivity or a unique piece of downhole equipment with no direct alternatives, RPC's reliance on that supplier increases their leverage. This situation is amplified when the supplier's product is vital for meeting stringent environmental regulations or achieving operational efficiencies that are key competitive advantages for RPC.

- Supplier Concentration: A limited number of suppliers for critical raw materials or specialized equipment can lead to higher bargaining power for those suppliers.

- Technological Differentiation: Suppliers offering unique, patented, or highly advanced technologies that are essential for RPC's service offerings possess greater leverage.

- Switching Costs: High costs associated with changing suppliers for specialized components or software can solidify a supplier's bargaining power.

- Importance of Input: When a supplier's product represents a significant portion of RPC's cost structure or is critical to service performance, the supplier's power is enhanced.

Switching Costs for RPC

Switching suppliers for RPC, Inc. can be a costly endeavor. For instance, the expense of retooling manufacturing lines to accommodate new equipment or retraining staff on different operational procedures can easily run into millions of dollars. This financial barrier significantly limits RPC's ability to readily change its suppliers, giving existing vendors more leverage.

These substantial switching costs directly enhance the bargaining power of RPC's current suppliers. When a company like RPC faces significant disruption and expense in finding and integrating a new supplier, the existing supplier can often dictate terms more effectively. This dynamic is a key factor in assessing supplier power.

Furthermore, long-term supply agreements and deeply integrated supply chain relationships can further solidify RPC's reliance on its existing vendors. These arrangements create a sticky situation, making it even more challenging and expensive for RPC to explore alternative sourcing options, thereby reinforcing supplier influence.

- High Retooling Costs: Implementing new specialized equipment can require substantial capital investment for RPC, potentially millions of dollars depending on the technology.

- Personnel Training Expenses: Educating employees on new machinery or processes associated with a different supplier adds to the overall switching cost burden.

- Operational Downtime: The transition period between suppliers can lead to production halts, resulting in lost revenue and increased operational expenses for RPC.

- Contractual Lock-ins: Existing long-term contracts with suppliers may include penalties for early termination, further increasing the cost of switching.

Supplier Power Shapes Oilfield Services Landscape

RPC, Inc. faces significant bargaining power from its suppliers, particularly for specialized oilfield equipment and essential materials like frac sand. The industry's move towards advanced, lower-emission technologies further concentrates power among suppliers who can provide these critical components. For instance, in early 2024, disruptions in logistics for frac sand led to increased lead times and prices, directly impacting RPC's completion services.

The scarcity of skilled labor in the oilfield services sector also empowers labor suppliers and skilled workers, driving up costs for RPC. This trend, noted throughout 2023 and into 2024, highlights the persistent demand for experienced professionals. Furthermore, high switching costs, including retooling and training, can run into millions of dollars, solidifying the leverage of existing vendors.

| Supplier Factor | Impact on RPC, Inc. | 2024 Data/Trend |

|---|---|---|

| Specialized Equipment Reliance | High dependence on unique manufacturers | Continued demand for advanced pressure pumping units and downhole tools |

| Technological Advancements | Need to secure lower-emission technologies | Increased leverage for suppliers of Tier 4 DGB and electric fleet components |

| Frac Sand Availability | Critical input for hydraulic fracturing | Robust demand in early 2024 led to higher prices and longer lead times due to logistical challenges |

| Skilled Labor Shortages | Increased labor costs and operational challenges | Persistent difficulty in filling specialized roles throughout 2023-2024 |

| Switching Costs | Millions in retooling and training | Significant financial barriers limit RPC's ability to change suppliers |

What is included in the product

This analysis evaluates the competitive landscape for RPC, Inc., examining the intensity of rivalry, buyer and supplier power, threat of new entrants and substitutes.

RPC, Inc.'s Porter's Five Forces analysis offers a clear, one-sheet summary, pinpointing strategic pressures to relieve the pain of complex market assessments.

Customers Bargaining Power

Customer Concentration and Purchasing Volume

RPC, Inc.'s customer base is largely concentrated within the independent and major oil and gas sectors. This concentration is highlighted by its 2024 financial disclosures, which revealed that two private exploration and production (E&P) companies individually contributed around 13% and 11% to its total revenue.

This significant customer concentration translates directly into enhanced bargaining power for these large clients. Their substantial purchasing volumes and critical importance to RPC's revenue streams empower them to negotiate more favorable pricing structures and contract terms, thereby influencing RPC's profitability and operational flexibility.

Sensitivity to Oil and Gas Prices and E&P Capex

RPC, Inc.'s revenue is closely tied to the capital expenditure (Capex) decisions of oil and gas exploration and production (E&P) companies. These decisions are heavily influenced by fluctuating oil and natural gas prices. When energy prices dip, customers tend to cut back on drilling and new well development, directly impacting RPC's service demand.

For instance, a significant slowdown in US E&P Capex was observed throughout 2024. Projections for 2025 also indicated continued declines in this spending. This environment inherently strengthens the bargaining power of RPC's customers, as they have fewer alternatives and are more cost-conscious during periods of reduced energy commodity prices.

Oversupply of Oilfield Services Capacity

The oilfield services sector has seen a significant oversupply of capacity. This is partly because exploration and production (E&P) companies are now more efficient, needing fewer rigs to meet their production goals. This surplus of available services means customers have more choices and can push for lower prices and improved service.

This dynamic directly impacts companies like RPC, Inc. In 2024, RPC specifically cited these competitive pricing pressures as a contributing factor to its revenue decline. The bargaining power of customers is amplified when there's more capacity than demand, forcing service providers to compete more aggressively on price.

Consolidation Among E&P Companies

The ongoing consolidation within the exploration and production (E&P) sector is a significant factor impacting the bargaining power of RPC, Inc.'s customers. As fewer, larger entities emerge, their collective buying power intensifies, allowing them to demand more favorable terms from service providers like RPC.

These consolidated E&P companies are better positioned to negotiate lower prices and seek integrated service packages, putting pressure on RPC’s margins. This trend has already manifested in customer attrition for RPC, highlighting the direct impact of this industry consolidation on its client base.

- Increased Buyer Power: Larger E&P companies resulting from consolidation can leverage their scale to negotiate better pricing and terms with oilfield service providers.

- Demand for Integrated Services: Consolidated entities often prefer fewer, more comprehensive service providers, potentially squeezing out smaller or specialized firms.

- Customer Loss Impact: RPC has directly experienced a reduction in its customer base due to this consolidation trend, indicating a tangible loss of business.

Low Switching Costs for Customers

Customers of RPC, Inc. often experience low switching costs. This is largely due to the short lead times between ordering oilfield services and their actual delivery. This means clients can readily explore other providers if they find better pricing or terms elsewhere.

This ease of switching significantly enhances customer bargaining power. In 2024, the oilfield services sector continued to see a dynamic competitive landscape, with numerous players vying for contracts. This competitive environment naturally provides customers with a wide array of choices, reinforcing their ability to negotiate favorable terms with companies like RPC.

- Short Lead Times: Services are often delivered quickly, reducing commitment.

- Price Sensitivity: Customers can easily shop around for the best deals.

- Competitive Market: Numerous providers mean customers have ample alternatives.

Powerful Customers Drive RPC's 2024 Revenue Challenges

RPC, Inc.'s customers, particularly large independent and major oil and gas companies, wield significant bargaining power. This is evident in their substantial revenue contribution, with two private E&P companies alone accounting for approximately 13% and 11% of RPC's total revenue in 2024. This concentration allows these clients to negotiate favorable pricing and contract terms, directly impacting RPC's profitability.

The oilfield services market in 2024 was characterized by oversupply and increased efficiency from E&P companies, meaning fewer rigs are needed. This surplus of capacity strengthens customer bargaining power, as they have more options and are more cost-conscious, especially during periods of lower energy prices. This competitive pressure was a cited reason for RPC's revenue decline in 2024.

Consolidation within the E&P sector further amplifies customer bargaining power. Larger, merged entities can leverage their increased scale to demand better terms and integrated service packages, leading to customer attrition for RPC. Additionally, low switching costs due to short lead times for services allow customers to easily move to competitors, reinforcing their negotiating leverage in a dynamic market.

| Customer Factor | Impact on RPC, Inc. | 2024 Data/Observation |

|---|---|---|

| Customer Concentration | Increased bargaining power for large clients | Two private E&P companies contributed ~13% and ~11% of total revenue. |

| Market Oversupply & Efficiency | Customers can demand lower prices and better terms | Oversupply of capacity; E&P companies require fewer rigs. |

| E&P Sector Consolidation | Larger buyers exert greater influence | Leading to customer attrition for RPC. |

| Low Switching Costs | Customers can easily switch providers | Short lead times for services in a competitive market. |

Preview Before You Purchase

RPC, Inc. Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for RPC, Inc., offering a detailed examination of industry competitiveness. The document you see here is the exact, professionally formatted analysis you'll receive immediately after purchase, ensuring full transparency and immediate utility for your strategic planning.