Rubis Boston Consulting Group Matrix

Actionable Strategy Starts Here

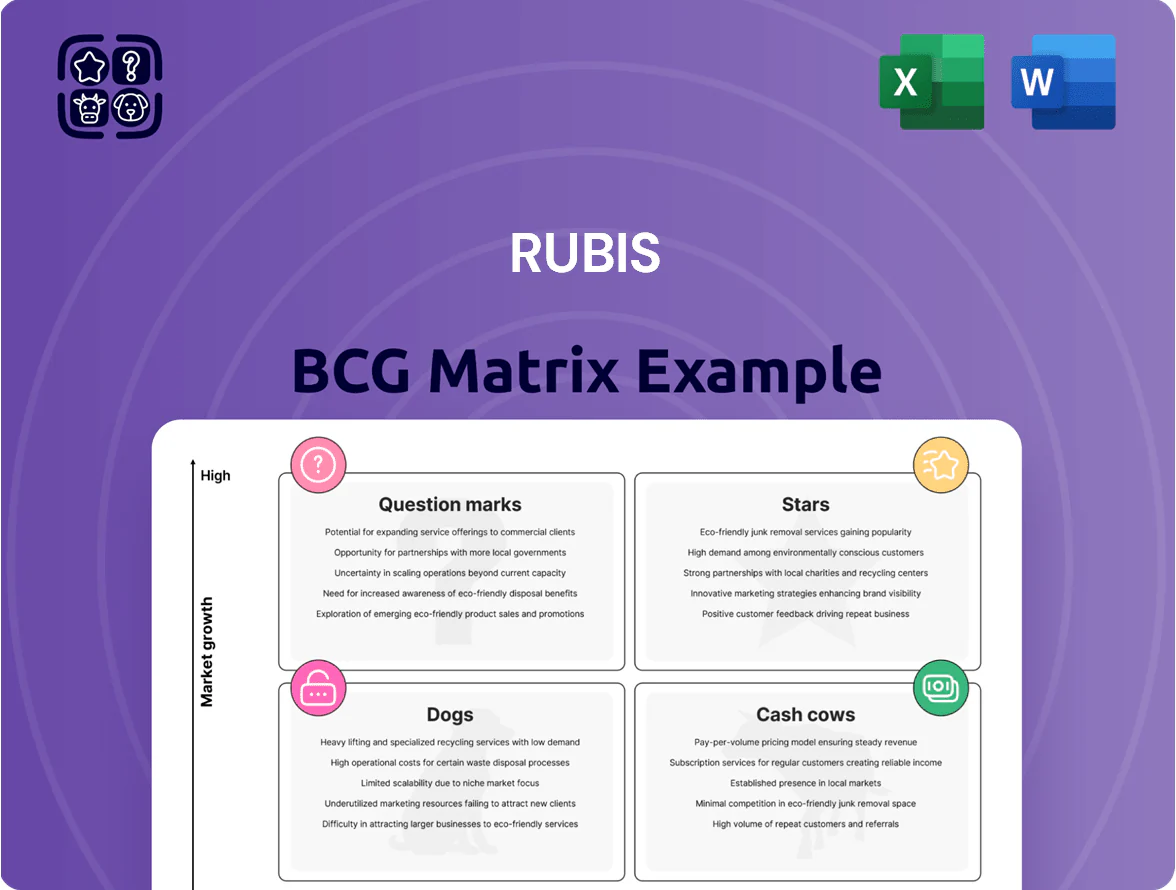

Rubis’s BCG Matrix snapshot highlights which business units are fueling growth versus which may be draining resources, offering a quick view of Stars, Cash Cows, Question Marks, and Dogs in its portfolio. This preview teases market-share dynamics and growth potential but stops short of the full strategic playbook. Purchase the complete BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that turn analysis into immediate action.

Stars

Rubis Photosol Solar Utility

As of late 2025, Rubis Photosol Solar Utility is the group's Stars quadrant: post-Photosol integration it drove group growth, with renewables revenue up ~45% YoY to €230m in 2025 and operating investments of €160m, funded by €120m project financing.

The segment benefits from Europe’s energy transition and strong French demand—Photosol captured ~18% of France’s newly commissioned utility solar capacity in 2024–25 (≈420 MW of 2.3 GW), securing long-term offtake and pipeline visibility.

Bitumen Distribution in West Africa

Rubis holds a dominant share in West Africa bitumen supply for large infrastructure, serving 60–70% of major road and port projects and driving roughly €120m revenue in 2024 from bitumen sales across Africa.

The sector posts high growth—CAGR ~7–9% to 2028—fueled by urbanization and $15bn+ annual international transport investment in the region.

As market leader with specialized maritime logistics and coastal terminals, Rubis is expanding into three emerging hubs (Ghana, Senegal, Côte d’Ivoire) to raise capacity 25% by 2026.

LPG Distribution in East Africa

LPG Distribution in East Africa is a Star: household LPG adoption in Kenya rose to ~32% in 2024 from 18% in 2018, creating ~8–12% CAGR market growth; Rubis captured ~28% market share in Kenya and Tanzania by 2024 via acquisitions and a $45m regional LPG infrastructure spend (2019–2024).

Aviation Fuel Recovery and Expansion

Following the 2025 rebound in global travel, Rubis’ aviation fuel unit in the Caribbean and Indian Ocean sits as a Star: air traffic recovery hit ~95% of 2019 levels by Q3 2025 and regional passenger volumes grew 18% year-over-year, feeding demand.

Rubis uses integrated supply (10+ storage sites, documented 2024 throughput ~1.2 Mtpa) and airport concessions to defend a high market share versus Shell and TotalEnergies, keeping gross margins above corporate average.

The tourism-driven high flight volumes and route concentration mean sustained high cash use but strong growth potential and continued top-line contributions to Rubis’ downstream segment.

- 2025 regional passenger recovery ~95% vs 2019

- Passenger growth +18% YoY in 2025

- Throughput ~1.2 million tonnes per annum (2024)

- Multiple airport concessions; higher-than-average downstream margins

HVO and Biofuel Distribution

HVO and biofuel distribution sits in Rubis’s BCG Matrix as a star: tightening EU rules by Dec 31, 2025 pushed HVO demand up 28% YoY in 2024, and Rubis redirected 42% of its French network capacity to low-carbon fuels, capturing premium margins ~€0.12–0.18/liter above diesel in 2025.

The segment shows high growth and strong market share, using existing storage and logistics to serve commercial fleets and expected CAGR ~22% through 2028, so Rubis is scaling supply contracts and blend capabilities now.

- 2024 demand +28% YoY

- 42% network capacity repurposed

- Price premium €0.12–0.18/liter

- Projected CAGR 22% to 2028

Rubis Stars: Photosol-led renewables surge, strong LPG, bitumen, aviation & HVO growth

Rubis Stars: Photosol-driven renewables (€230m rev 2025, +45% YoY; €160m capex), West Africa bitumen (€120m rev 2024; 60–70% proj. share), East Africa LPG (28% share; 8–12% CAGR), Aviation fuels (throughput 1.2 Mtpa 2024; passenger recovery ~95% 2025), HVO/biofuels (demand +28% 2024; 42% capacity repurposed).

| Segment | Key metric | 2024–25 |

|---|---|---|

| Photosol | Revenue / Capex | €230m / €160m |

| Bitumen | Revenue / Market share | €120m / 60–70% |

| LPG | Share / CAGR | 28% / 8–12% |

| Aviation | Throughput / Pax | 1.2 Mtpa / 95% |

| HVO | Demand / Capacity | +28% / 42% |

What is included in the product

Comprehensive BCG Matrix review of Rubis: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment, hold, divest recommendations.

One-page Rubis BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

LPG Distribution in France and Europe

Rubis’ Vitogaz LPG distribution in France and Europe is a cash cow: mature market with ~1–2% annual volume decline but stable EBITDA margins around 10–12% (2024 pro forma), delivering predictable free cash flow and low capex needs for new infrastructure.

As market leader Vitogaz funds Rubis’ 2025 renewables push and supports steady dividends—group FCF conversion ~60% in 2024—while paying out consistent shareholder distributions.

High regulatory and logistical barriers, plus long-term customer contracts and brand loyalty, protect margins and deter new entrants, sustaining defensive cash generation.

Retail Fuel Network in the Caribbean

Rubis Caribbean retail fuel network—over 600 service stations across 12 islands—holds dominant shares (30–70% by island) and delivers stable volumes ~1.2 billion liters in 2024, classifying it as a cash cow in the BCG matrix.

These markets show low CAGR (~1% demand growth) and high free cash flow conversion; Rubis reported Caribbean fuel EBITDA margin ~8.5% and operating cash flow €210m in 2024, fueling group investments.

Management squeezes costs and grows non-fuel retail (convenience, LPG, lubricants), where margins exceed fuel by ~3–6 percentage points, raising overall network profitability.

Support and Services Logistics

The midstream and logistics arm provides shipping and trading services that underpin Rubis’s distribution, handling about 1.8 million m3 of refined products in 2024 and supporting 85% of group volumes.

By controlling the supply chain Rubis lowers external fees and captures extra margin—roughly €0.03–€0.06 per liter in 2024—boosting segment EBITDA margin to about 12.5%.

This unit needs low maintenance capex (≈€40m in 2024), generates stable free cash flow, and acts as a reliable financial backbone for the group.

Fuel Distribution in Reunion and French Guiana

Rubis holds dominant fuel distribution in Réunion and French Guiana, with market shares around 60–80% and stable volumes; combined EBITDA margin about 12–15% in 2024, making growth low but cash returns steady.

Regulation and isolation limit competition and cap growth, yet low marketing costs and high freight pass-through keep operating cash flow high, funding corporate debt—net debt/EBITDA ~1.5x in 2024.

- High market share: 60–80%

- EBITDA margin: 12–15% (2024)

- Net debt/EBITDA: ~1.5x (2024)

- Low promo spend, steady volumes

Industrial Fuel Oil for Mature Markets

Providing heavy fuel oil and distillates to established industrial clients remains a high-share activity in several traditional regions, with Rubis reporting fuel trading and distribution revenues of €1.2bn in 2024 for downstream segments that include these products.

While demand is flat—global heavy fuel oil consumption fell ~3% from 2019–2023—long-term contracts and specialized handling make the customer base sticky, supporting stable margins near Rubis’s downstream average of ~8–10% in 2024.

These assets generate strong cash flow now, allowing Rubis to milk them while the industry shifts toward cleaner fuels; capex for transitioning is modest versus cash from legacy sales, and estimated free cash flow contribution from industrial fuel oil was ~€150–200m in 2024.

- High share in traditional regions; €1.2bn downstream revenue 2024

- Sticky customers via long-term contracts and handling needs

- Flat/slowly declining demand; HFO consumption down ~3% (2019–2023)

- Estimated FCF from these assets ~€150–200m in 2024

Rubis: cash-generating LPG, Caribbean retail & midstream funding renewables/dividends

Rubis cash cows: Vitogaz LPG (France/EU) + Caribbean retail + midstream logistics + HFO/distillates — 2024: group FCF conv ~60%, operating cash €210m (Caribbean), downstream revenue €1.2bn, midstream volume 1.8m m3, EBITDA margins 8–15%, net debt/EBITDA ~1.5x; stable low-growth markets, high shares, low capex (~€40m midstream) funding renewables and dividends.

| Asset | 2024 key metric |

|---|---|

| Vitogaz LPG | EBITDA 10–12% / stable volumes |

| Caribbean retail | OCF €210m / volumes 1.2bn L |

| Midstream | 1.8m m3 / capex €40m |

| HFO/distillates | Revenue €1.2bn / FCF €150–200m |

Full Transparency, Always

Rubis BCG Matrix

The file you're previewing on this page is the final Rubis BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clear portfolio assessment and decision-making.

This preview is the exact same Rubis BCG Matrix report you’ll download after buying; crafted with market-backed analysis and strategic insight, the complete document is sent directly to your inbox with no surprises.

What you see is the actual Rubis BCG Matrix file available post-purchase—immediately editable, printable, and presentation-ready for stakeholders, advisors, or internal planning.

You're viewing the genuine Rubis BCG Matrix that becomes yours with a one-time purchase—professionally designed by strategy experts and formatted for direct integration into business plans, decks, or competitive reviews.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Rubis’s BCG Matrix snapshot highlights which business units are fueling growth versus which may be draining resources, offering a quick view of Stars, Cash Cows, Question Marks, and Dogs in its portfolio. This preview teases market-share dynamics and growth potential but stops short of the full strategic playbook. Purchase the complete BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that turn analysis into immediate action.

Stars

Rubis Photosol Solar Utility

As of late 2025, Rubis Photosol Solar Utility is the group's Stars quadrant: post-Photosol integration it drove group growth, with renewables revenue up ~45% YoY to €230m in 2025 and operating investments of €160m, funded by €120m project financing.

The segment benefits from Europe’s energy transition and strong French demand—Photosol captured ~18% of France’s newly commissioned utility solar capacity in 2024–25 (≈420 MW of 2.3 GW), securing long-term offtake and pipeline visibility.

Bitumen Distribution in West Africa

Rubis holds a dominant share in West Africa bitumen supply for large infrastructure, serving 60–70% of major road and port projects and driving roughly €120m revenue in 2024 from bitumen sales across Africa.

The sector posts high growth—CAGR ~7–9% to 2028—fueled by urbanization and $15bn+ annual international transport investment in the region.

As market leader with specialized maritime logistics and coastal terminals, Rubis is expanding into three emerging hubs (Ghana, Senegal, Côte d’Ivoire) to raise capacity 25% by 2026.

LPG Distribution in East Africa

LPG Distribution in East Africa is a Star: household LPG adoption in Kenya rose to ~32% in 2024 from 18% in 2018, creating ~8–12% CAGR market growth; Rubis captured ~28% market share in Kenya and Tanzania by 2024 via acquisitions and a $45m regional LPG infrastructure spend (2019–2024).

Aviation Fuel Recovery and Expansion

Following the 2025 rebound in global travel, Rubis’ aviation fuel unit in the Caribbean and Indian Ocean sits as a Star: air traffic recovery hit ~95% of 2019 levels by Q3 2025 and regional passenger volumes grew 18% year-over-year, feeding demand.

Rubis uses integrated supply (10+ storage sites, documented 2024 throughput ~1.2 Mtpa) and airport concessions to defend a high market share versus Shell and TotalEnergies, keeping gross margins above corporate average.

The tourism-driven high flight volumes and route concentration mean sustained high cash use but strong growth potential and continued top-line contributions to Rubis’ downstream segment.

- 2025 regional passenger recovery ~95% vs 2019

- Passenger growth +18% YoY in 2025

- Throughput ~1.2 million tonnes per annum (2024)

- Multiple airport concessions; higher-than-average downstream margins

HVO and Biofuel Distribution

HVO and biofuel distribution sits in Rubis’s BCG Matrix as a star: tightening EU rules by Dec 31, 2025 pushed HVO demand up 28% YoY in 2024, and Rubis redirected 42% of its French network capacity to low-carbon fuels, capturing premium margins ~€0.12–0.18/liter above diesel in 2025.

The segment shows high growth and strong market share, using existing storage and logistics to serve commercial fleets and expected CAGR ~22% through 2028, so Rubis is scaling supply contracts and blend capabilities now.

- 2024 demand +28% YoY

- 42% network capacity repurposed

- Price premium €0.12–0.18/liter

- Projected CAGR 22% to 2028

Rubis Stars: Photosol-led renewables surge, strong LPG, bitumen, aviation & HVO growth

Rubis Stars: Photosol-driven renewables (€230m rev 2025, +45% YoY; €160m capex), West Africa bitumen (€120m rev 2024; 60–70% proj. share), East Africa LPG (28% share; 8–12% CAGR), Aviation fuels (throughput 1.2 Mtpa 2024; passenger recovery ~95% 2025), HVO/biofuels (demand +28% 2024; 42% capacity repurposed).

| Segment | Key metric | 2024–25 |

|---|---|---|

| Photosol | Revenue / Capex | €230m / €160m |

| Bitumen | Revenue / Market share | €120m / 60–70% |

| LPG | Share / CAGR | 28% / 8–12% |

| Aviation | Throughput / Pax | 1.2 Mtpa / 95% |

| HVO | Demand / Capacity | +28% / 42% |

What is included in the product

Comprehensive BCG Matrix review of Rubis: strategic guidance on Stars, Cash Cows, Question Marks, and Dogs with investment, hold, divest recommendations.

One-page Rubis BCG Matrix placing each business unit in a quadrant for quick strategic decisions

Cash Cows

LPG Distribution in France and Europe

Rubis’ Vitogaz LPG distribution in France and Europe is a cash cow: mature market with ~1–2% annual volume decline but stable EBITDA margins around 10–12% (2024 pro forma), delivering predictable free cash flow and low capex needs for new infrastructure.

As market leader Vitogaz funds Rubis’ 2025 renewables push and supports steady dividends—group FCF conversion ~60% in 2024—while paying out consistent shareholder distributions.

High regulatory and logistical barriers, plus long-term customer contracts and brand loyalty, protect margins and deter new entrants, sustaining defensive cash generation.

Retail Fuel Network in the Caribbean

Rubis Caribbean retail fuel network—over 600 service stations across 12 islands—holds dominant shares (30–70% by island) and delivers stable volumes ~1.2 billion liters in 2024, classifying it as a cash cow in the BCG matrix.

These markets show low CAGR (~1% demand growth) and high free cash flow conversion; Rubis reported Caribbean fuel EBITDA margin ~8.5% and operating cash flow €210m in 2024, fueling group investments.

Management squeezes costs and grows non-fuel retail (convenience, LPG, lubricants), where margins exceed fuel by ~3–6 percentage points, raising overall network profitability.

Support and Services Logistics

The midstream and logistics arm provides shipping and trading services that underpin Rubis’s distribution, handling about 1.8 million m3 of refined products in 2024 and supporting 85% of group volumes.

By controlling the supply chain Rubis lowers external fees and captures extra margin—roughly €0.03–€0.06 per liter in 2024—boosting segment EBITDA margin to about 12.5%.

This unit needs low maintenance capex (≈€40m in 2024), generates stable free cash flow, and acts as a reliable financial backbone for the group.

Fuel Distribution in Reunion and French Guiana

Rubis holds dominant fuel distribution in Réunion and French Guiana, with market shares around 60–80% and stable volumes; combined EBITDA margin about 12–15% in 2024, making growth low but cash returns steady.

Regulation and isolation limit competition and cap growth, yet low marketing costs and high freight pass-through keep operating cash flow high, funding corporate debt—net debt/EBITDA ~1.5x in 2024.

- High market share: 60–80%

- EBITDA margin: 12–15% (2024)

- Net debt/EBITDA: ~1.5x (2024)

- Low promo spend, steady volumes

Industrial Fuel Oil for Mature Markets

Providing heavy fuel oil and distillates to established industrial clients remains a high-share activity in several traditional regions, with Rubis reporting fuel trading and distribution revenues of €1.2bn in 2024 for downstream segments that include these products.

While demand is flat—global heavy fuel oil consumption fell ~3% from 2019–2023—long-term contracts and specialized handling make the customer base sticky, supporting stable margins near Rubis’s downstream average of ~8–10% in 2024.

These assets generate strong cash flow now, allowing Rubis to milk them while the industry shifts toward cleaner fuels; capex for transitioning is modest versus cash from legacy sales, and estimated free cash flow contribution from industrial fuel oil was ~€150–200m in 2024.

- High share in traditional regions; €1.2bn downstream revenue 2024

- Sticky customers via long-term contracts and handling needs

- Flat/slowly declining demand; HFO consumption down ~3% (2019–2023)

- Estimated FCF from these assets ~€150–200m in 2024

Rubis: cash-generating LPG, Caribbean retail & midstream funding renewables/dividends

Rubis cash cows: Vitogaz LPG (France/EU) + Caribbean retail + midstream logistics + HFO/distillates — 2024: group FCF conv ~60%, operating cash €210m (Caribbean), downstream revenue €1.2bn, midstream volume 1.8m m3, EBITDA margins 8–15%, net debt/EBITDA ~1.5x; stable low-growth markets, high shares, low capex (~€40m midstream) funding renewables and dividends.

| Asset | 2024 key metric |

|---|---|

| Vitogaz LPG | EBITDA 10–12% / stable volumes |

| Caribbean retail | OCF €210m / volumes 1.2bn L |

| Midstream | 1.8m m3 / capex €40m |

| HFO/distillates | Revenue €1.2bn / FCF €150–200m |

Full Transparency, Always

Rubis BCG Matrix

The file you're previewing on this page is the final Rubis BCG Matrix you'll receive after purchase—no watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clear portfolio assessment and decision-making.

This preview is the exact same Rubis BCG Matrix report you’ll download after buying; crafted with market-backed analysis and strategic insight, the complete document is sent directly to your inbox with no surprises.

What you see is the actual Rubis BCG Matrix file available post-purchase—immediately editable, printable, and presentation-ready for stakeholders, advisors, or internal planning.

You're viewing the genuine Rubis BCG Matrix that becomes yours with a one-time purchase—professionally designed by strategy experts and formatted for direct integration into business plans, decks, or competitive reviews.