Ryan Companies Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

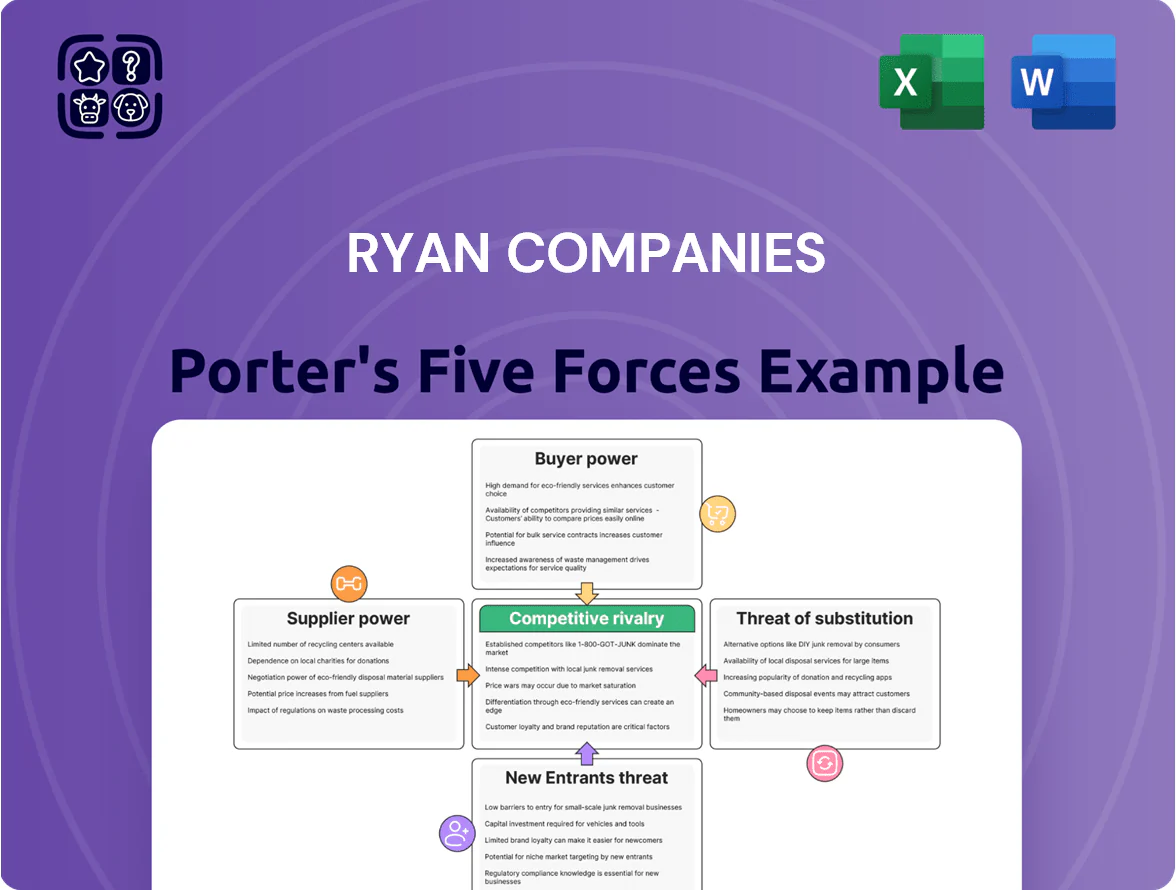

Ryan Companies faces moderate supplier power, steady buyer negotiation in commercial real estate, rising substitute threats from modular construction, and significant rivalry among established developers—regulatory and capital barriers temper new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ryan Companies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of specialized skilled labor

As of late 2025 the US construction sector reports a 20% shortfall in skilled trades (National Association of Home Builders), giving electricians, plumbers and specialist technicians stronger bargaining power; unions and niche subcontractors can push up bids by 8–12% on large projects. Ryan Companies needs multi-year preferred subcontractor agreements and labor pipelines to keep schedules and margins intact.

Volatility in raw material pricing

Suppliers of structural steel, concrete, and advanced glass exert strong pricing power after 2020 supply shocks; global steel prices rose ~40% 2020–2022 and averaged $900/ton in 2024, raising project input costs.

Specialized sustainable materials stay costly—low-carbon cement premiums ran ~15–30% in 2024—so demand for green buildings keeps upward pressure on prices.

Ryan Companies uses early procurement and bulk buys; locking prices on ~25–40% of materials per project in 2024 cut material-cost volatility for sampled projects by ~6–10%.

Limited availability of prime land parcels

As a developer, Ryan Companies depends on landowners who hold scarce prime parcels in urban centers and industrial hubs, giving sellers outsized leverage; in 2024, U.S. urban infill vacancy fell to 3.8%, pushing land premiums up 12% year-over-year.

The finite supply drives bidding wars and complex entitlements, raising acquisition costs—average Chicago land sale prices rose ~18% in 2023–24 for transit-accessible sites.

Ryan counters by using internal development expertise and early pipelines to source off-market or underpriced lots; 40% of its 2024 projects began via pre-market agreements, cutting competition and margin pressure.

Influence of specialized technology providers

The integration of BIM and advanced property-management software makes Ryan Companies dependent on a few key vendors; these platforms drive design-build efficiency and create high switching costs—industry data shows 70% of large US design-build firms report vendor lock-in as a top tech risk in 2024.

Ryan offsets supplier power by building internal tech teams and keeping flexible SLAs with principal software developers, reducing potential downtime and saving an estimated $3–5m annually in integration costs.

- High vendor power: vendor lock-in cited by 70% of peers

- Financial impact: $3–5m annual integration savings from internal tools

- Mitigation: internal tech + flexible SLAs

Consolidation of large-scale subcontractors

Consolidation among regional and national subcontractors has cut the pool of firms able to take on billion-dollar projects by roughly 25% since 2018, concentrating pricing power in a few large players.

As scale rises, top subcontractors demand stricter terms and favor developers with strong payment records; late payments can raise subcontractor margins by 150–300 basis points.

Ryan Companies offsets this by using its integrated design-build model and strong balance sheet—$1.2B liquidity reported in 2024—to secure priority access and better contract terms.

- Fewer firms: −25% capable of mega-projects since 2018

- Higher subcontractor margins: +150–300 bps with payment risk

- Ryan advantage: integrated delivery + $1.2B liquidity (2024)

Ryan counters soaring supplier power with pre-market deals, early buy-ins and $1.2B liquidity

Supplier power is high: skilled-labor shortfall ~20% (2025), steel averaged $900/ton (2024), low-carbon cement premium 15–30% (2024), urban land vacancy 3.8% (2024) pushed land premiums +12% YoY; Ryan mitigates via preferred subs (40% pre-market deals in 2024), early procurement (locked 25–40% materials), internal tech and $1.2B liquidity (2024).

| Metric | Value |

|---|---|

| Skilled-trade shortfall | 20% (2025) |

| Steel price | $900/ton (2024) |

| Land vacancy (urban) | 3.8% (2024) |

| Pre-market deals | 40% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Ryan Companies that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and disruptive threats to assess pricing power and strategic positioning.

A concise Ryan Companies Porter's Five Forces one-sheet that quickly highlights competitive pressures and strategic levers, ready to drop into decks for faster decision-making.

Customers Bargaining Power

Concentration of institutional capital

A large share of Ryan Companies’ revenue comes from institutional investors and REITs—about 60% of development fees in 2024—buyers with deep market knowledge and capital who push for lower management fees and higher performance hurdles; they negotiated fee cuts of ~10–25% on major 2023 mandates. To retain these clients, Ryan must show multi-cycle performance: target returns of 12%+ IRR on development and sub-5% volatility on income assets over 5–10 years.

Demand for high-performance ESG standards

Corporate tenants and institutional buyers now require strict ESG standards, with 78% of S&P 500 firms reporting net-zero targets by 2030–2050, letting customers demand energy-efficient design and sustainable materials that can raise development costs by 5–12% per project.

Low switching costs for development services

While real estate assets are long-term, selecting a developer is low-cost pre-contract, so clients can switch easily between national firms; a 2024 CRE survey found 42% of owners would change developers for 10% better total project value.

Information transparency in the digital age

Customers now use real-time market data and benchmarking tools—CBRE showed 2024 construction cost indices rose 6.2% YoY—letting investors pinpoint fair values and cut information asymmetry that once favored Ryan Companies.

Ryan combats this by publishing transparent, data-driven reports and project dashboards; in 2025 it cited a 15% reduction in pricing disputes after rolling out investor reporting.

- Real-time data reduces seller info advantage

- 2024 construction cost index +6.2% YoY (CBRE)

- Ryan’s reporting cut disputes ~15% in 2025

Customization requirements for build-to-suit projects

Major corporate clients for Ryan Companies’ build-to-suit projects hold strong bargaining power, since single tenants can account for multi-year leases worth hundreds of millions—2024 industrial BTS deals averaged $45–75M per project in the US Midwest, raising stake for landlords.

These tenants demand exacting architectural specs and infrastructure (e.g., 50–60 ft clear heights, 200–500 kW power), which reduces reuse value if they vacate, forcing Ryan to weigh customization against resale or re-lease timelines.

Ryan must negotiate concessions—longer lease terms, tenant improvement cost-sharing, or higher rents—to protect asset marketability while securing large, stable cash flows.

- Typical BTS deal size: $45–75M (2024 Midwest)

- Common specs: 50–60 ft clear height; 200–500 kW power

- Mitigation: longer leases, TI sharing, higher rents

Institutional Pressure, Rising ESG Costs & BTS Specs Squeeze Development Margins

Large institutional clients hold strong leverage—~60% of Ryan’s 2024 development fees—pressing fee cuts of 10–25% on big mandates; investors demand 12%+ IRR and low volatility over 5–10 years. ESG and efficiency rules raise build costs 5–12%, while real-time data (CBRE 2024 construction cost +6.2% YoY) lowers information asymmetry; Ryan’s 2025 reporting cut disputes ~15%. BTS tenants (2024 Midwest avg deal $45–75M) require heavy specs, reducing reuse value.

| Metric | Value |

|---|---|

| Share of fees from institutions (2024) | ~60% |

| Fee cuts on mandates (2023) | 10–25% |

| Construction cost change (CBRE 2024) | +6.2% YoY |

| ESG cost premium | 5–12% per project |

| Ryan dispute reduction (2025) | ~15% |

| Avg BTS deal (2024 Midwest) | $45–75M |

Preview the Actual Deliverable

Ryan Companies Porter's Five Forces Analysis

This preview shows the exact Ryan Companies Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Ryan Companies faces moderate supplier power, steady buyer negotiation in commercial real estate, rising substitute threats from modular construction, and significant rivalry among established developers—regulatory and capital barriers temper new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ryan Companies’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarcity of specialized skilled labor

As of late 2025 the US construction sector reports a 20% shortfall in skilled trades (National Association of Home Builders), giving electricians, plumbers and specialist technicians stronger bargaining power; unions and niche subcontractors can push up bids by 8–12% on large projects. Ryan Companies needs multi-year preferred subcontractor agreements and labor pipelines to keep schedules and margins intact.

Volatility in raw material pricing

Suppliers of structural steel, concrete, and advanced glass exert strong pricing power after 2020 supply shocks; global steel prices rose ~40% 2020–2022 and averaged $900/ton in 2024, raising project input costs.

Specialized sustainable materials stay costly—low-carbon cement premiums ran ~15–30% in 2024—so demand for green buildings keeps upward pressure on prices.

Ryan Companies uses early procurement and bulk buys; locking prices on ~25–40% of materials per project in 2024 cut material-cost volatility for sampled projects by ~6–10%.

Limited availability of prime land parcels

As a developer, Ryan Companies depends on landowners who hold scarce prime parcels in urban centers and industrial hubs, giving sellers outsized leverage; in 2024, U.S. urban infill vacancy fell to 3.8%, pushing land premiums up 12% year-over-year.

The finite supply drives bidding wars and complex entitlements, raising acquisition costs—average Chicago land sale prices rose ~18% in 2023–24 for transit-accessible sites.

Ryan counters by using internal development expertise and early pipelines to source off-market or underpriced lots; 40% of its 2024 projects began via pre-market agreements, cutting competition and margin pressure.

Influence of specialized technology providers

The integration of BIM and advanced property-management software makes Ryan Companies dependent on a few key vendors; these platforms drive design-build efficiency and create high switching costs—industry data shows 70% of large US design-build firms report vendor lock-in as a top tech risk in 2024.

Ryan offsets supplier power by building internal tech teams and keeping flexible SLAs with principal software developers, reducing potential downtime and saving an estimated $3–5m annually in integration costs.

- High vendor power: vendor lock-in cited by 70% of peers

- Financial impact: $3–5m annual integration savings from internal tools

- Mitigation: internal tech + flexible SLAs

Consolidation of large-scale subcontractors

Consolidation among regional and national subcontractors has cut the pool of firms able to take on billion-dollar projects by roughly 25% since 2018, concentrating pricing power in a few large players.

As scale rises, top subcontractors demand stricter terms and favor developers with strong payment records; late payments can raise subcontractor margins by 150–300 basis points.

Ryan Companies offsets this by using its integrated design-build model and strong balance sheet—$1.2B liquidity reported in 2024—to secure priority access and better contract terms.

- Fewer firms: −25% capable of mega-projects since 2018

- Higher subcontractor margins: +150–300 bps with payment risk

- Ryan advantage: integrated delivery + $1.2B liquidity (2024)

Ryan counters soaring supplier power with pre-market deals, early buy-ins and $1.2B liquidity

Supplier power is high: skilled-labor shortfall ~20% (2025), steel averaged $900/ton (2024), low-carbon cement premium 15–30% (2024), urban land vacancy 3.8% (2024) pushed land premiums +12% YoY; Ryan mitigates via preferred subs (40% pre-market deals in 2024), early procurement (locked 25–40% materials), internal tech and $1.2B liquidity (2024).

| Metric | Value |

|---|---|

| Skilled-trade shortfall | 20% (2025) |

| Steel price | $900/ton (2024) |

| Land vacancy (urban) | 3.8% (2024) |

| Pre-market deals | 40% (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Ryan Companies that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and disruptive threats to assess pricing power and strategic positioning.

A concise Ryan Companies Porter's Five Forces one-sheet that quickly highlights competitive pressures and strategic levers, ready to drop into decks for faster decision-making.

Customers Bargaining Power

Concentration of institutional capital

A large share of Ryan Companies’ revenue comes from institutional investors and REITs—about 60% of development fees in 2024—buyers with deep market knowledge and capital who push for lower management fees and higher performance hurdles; they negotiated fee cuts of ~10–25% on major 2023 mandates. To retain these clients, Ryan must show multi-cycle performance: target returns of 12%+ IRR on development and sub-5% volatility on income assets over 5–10 years.

Demand for high-performance ESG standards

Corporate tenants and institutional buyers now require strict ESG standards, with 78% of S&P 500 firms reporting net-zero targets by 2030–2050, letting customers demand energy-efficient design and sustainable materials that can raise development costs by 5–12% per project.

Low switching costs for development services

While real estate assets are long-term, selecting a developer is low-cost pre-contract, so clients can switch easily between national firms; a 2024 CRE survey found 42% of owners would change developers for 10% better total project value.

Information transparency in the digital age

Customers now use real-time market data and benchmarking tools—CBRE showed 2024 construction cost indices rose 6.2% YoY—letting investors pinpoint fair values and cut information asymmetry that once favored Ryan Companies.

Ryan combats this by publishing transparent, data-driven reports and project dashboards; in 2025 it cited a 15% reduction in pricing disputes after rolling out investor reporting.

- Real-time data reduces seller info advantage

- 2024 construction cost index +6.2% YoY (CBRE)

- Ryan’s reporting cut disputes ~15% in 2025

Customization requirements for build-to-suit projects

Major corporate clients for Ryan Companies’ build-to-suit projects hold strong bargaining power, since single tenants can account for multi-year leases worth hundreds of millions—2024 industrial BTS deals averaged $45–75M per project in the US Midwest, raising stake for landlords.

These tenants demand exacting architectural specs and infrastructure (e.g., 50–60 ft clear heights, 200–500 kW power), which reduces reuse value if they vacate, forcing Ryan to weigh customization against resale or re-lease timelines.

Ryan must negotiate concessions—longer lease terms, tenant improvement cost-sharing, or higher rents—to protect asset marketability while securing large, stable cash flows.

- Typical BTS deal size: $45–75M (2024 Midwest)

- Common specs: 50–60 ft clear height; 200–500 kW power

- Mitigation: longer leases, TI sharing, higher rents

Institutional Pressure, Rising ESG Costs & BTS Specs Squeeze Development Margins

Large institutional clients hold strong leverage—~60% of Ryan’s 2024 development fees—pressing fee cuts of 10–25% on big mandates; investors demand 12%+ IRR and low volatility over 5–10 years. ESG and efficiency rules raise build costs 5–12%, while real-time data (CBRE 2024 construction cost +6.2% YoY) lowers information asymmetry; Ryan’s 2025 reporting cut disputes ~15%. BTS tenants (2024 Midwest avg deal $45–75M) require heavy specs, reducing reuse value.

| Metric | Value |

|---|---|

| Share of fees from institutions (2024) | ~60% |

| Fee cuts on mandates (2023) | 10–25% |

| Construction cost change (CBRE 2024) | +6.2% YoY |

| ESG cost premium | 5–12% per project |

| Ryan dispute reduction (2025) | ~15% |

| Avg BTS deal (2024 Midwest) | $45–75M |

Preview the Actual Deliverable

Ryan Companies Porter's Five Forces Analysis

This preview shows the exact Ryan Companies Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.