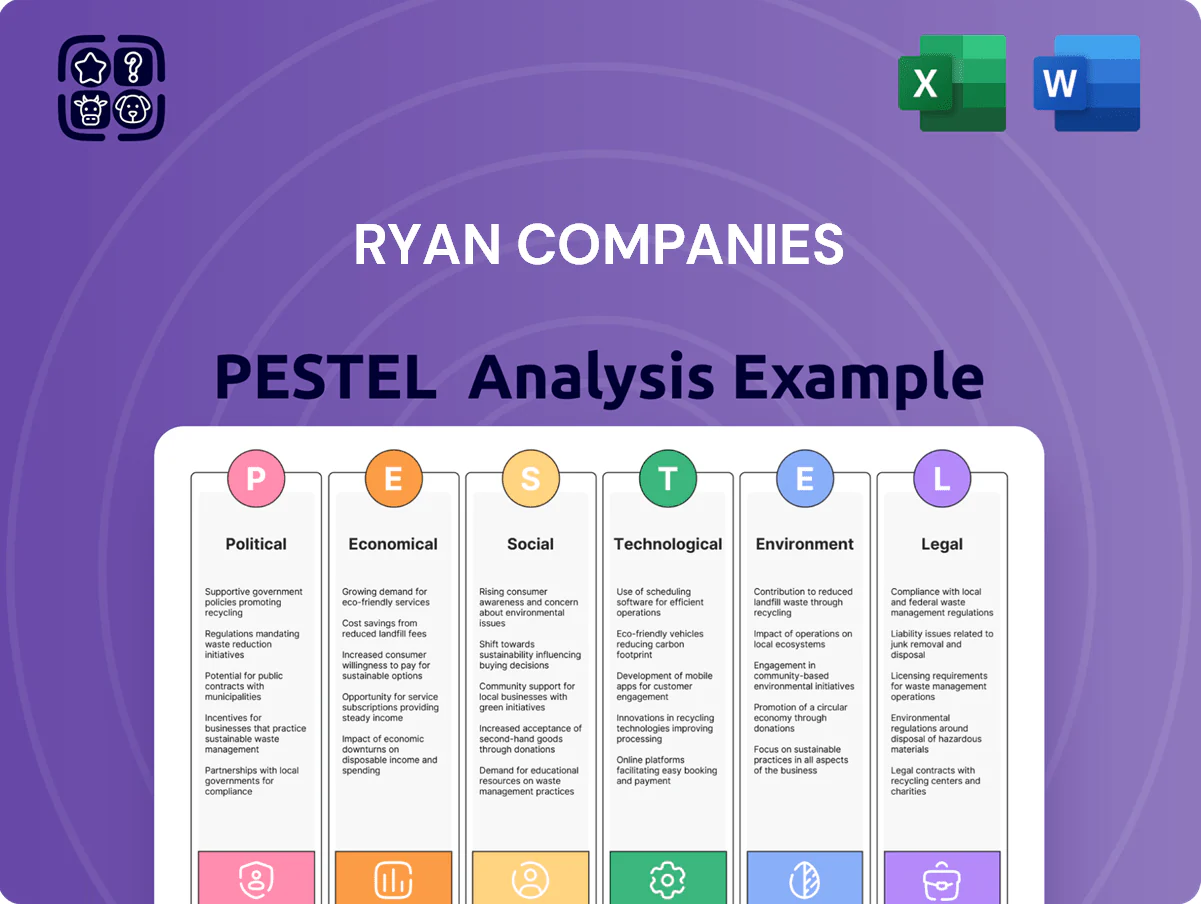

Ryan Companies PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis tailored to Ryan Companies—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and risks; purchase the full report for a comprehensive, ready-to-use briefing to inform investments, strategic planning, or competitive analysis.

Political factors

Federal Infrastructure and Housing Policy

The 2025 federal agenda maintains a focus on infrastructure and affordable housing, with the Bipartisan Infrastructure Law follow-ons and a $65 billion affordable housing tax credit expansion proposal affecting Ryan Companies' pipeline and increasing potential project funding. Changes to tax credits for mixed-use projects alter IRR thresholds, impacting feasibility of urban redevelopments valued at $100M+; Ryan must pursue PPPs and compete for HUD and DOT grants to secure capital.

Local Zoning and Land Use Regulations

Municipal political climates across Ryan Companies’ national footprint significantly affect permit and rezoning timelines, with average local approval delays adding 3–6 months and increasing soft costs by an estimated 5–12% per project.

Local elections regularly shift growth management policies—between 2022–2024, 28% of major U.S. metro zoning changes correlated with election cycles—forcing Ryan to invest in community relations and lobbying, typically 0.5–1% of project budgets.

Local regulatory hurdles remain a primary risk to timelines and budgets: 42% of Ryan’s recent commercial projects experienced scope or schedule changes due to municipal requirements, driving contingency reserves up by about 7%.

Geopolitical Trade Relations

Ongoing US tariffs on steel and aluminum (25% and 10% since 2018, with targeted adjustments into 2024–25) raise Ryan Companies’ design-build material costs, squeezing margins on projects where steel accounts for ~8–12% of build costs; global supply-chain disruptions in 2022–23 increased lead times by 20–40%, requiring strategic procurement to avoid delays; monitoring US-China and EU-Russia relations is essential to anticipate commodity price volatility—steel futures rose ~30% YoY in 2021–22.

Public-Private Partnership Incentives

State and local governments increasingly deploy tax increment financing and subsidies—$6.5B in TIF allocations nationally in 2023—to attract developers to underserved zones; Ryan Companies strategically taps these incentives to lower project risk and boost IRRs on urban infill and brownfield redevelopments.

Access to such funds varies by region and hinges on local fiscal health and political priorities; e.g., Midwest municipal bond downgrades in 2024 tightened TIF availability in several metros, altering deal pipelines.

- 2023 US TIF allocations: $6.5B

- Ryan uses incentives to de-risk and improve project IRRs

- Regional availability tied to fiscal health and 2024 municipal bond trends

Taxation and Fiscal Policy

Changes in corporate tax rates and new depreciation schedules for real estate—such as bonus depreciation reductions after 2023—can swing IRRs on Ryan Companies’ projects by several hundred basis points; for example, a 5% corporate tax rise could reduce after-tax returns materially on multi-year developments.

Ongoing policy debates over capital gains rates and potential limits to 1031 like-kind exchanges threaten Ryan’s capital recycling; historically, 1031 usage facilitated liquidity for ~20–30% of U.S. commercial transactions in active markets.

Broader fiscal shifts influence institutional demand: higher deficits and tightening fiscal outlooks in 2024–2025 correlate with lower pension and REIT allocations to new commercial development, compressing new-project funding availability.

- Corporate tax and depreciation changes can move IRRs by hundreds of bps

- 1031 exchange and capital gains rule changes risk impairing capital recycling

- Fiscal tightening in 2024–2025 linked to reduced institutional deployment into new commercial development

Policy shifts, tariffs & zoning drag Ryan Cos. IRRs—TIF/PPPs mitigate, tax reforms swing returns

Federal infrastructure and affordable-housing funding (2025 proposals incl. $65B tax credit expansion) plus tariffs (steel +25%, aluminum +10%) and municipal zoning delays (avg +3–6 months; +5–12% soft costs) materially affect Ryan Companies’ IRRs and timelines; use of $6.5B TIF (2023) and PPPs mitigates risk, while tax/depreciation and 1031 reforms could swing returns by hundreds of bps.

| Metric | Value |

|---|---|

| Affordable housing credit | $65B proposal (2025) |

| 2023 TIF | $6.5B |

| Zoning delay | +3–6 months |

| Soft cost rise | +5–12% |

| Steel tariff | +25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Ryan Companies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to inform executives and investors.

A concise, visually segmented PESTLE summary for Ryan Companies that can be dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment

As of late 2025, U.S. benchmark rates have stabilized near 5.25–5.50%, easing from 2022–23 volatility; this reduces average construction loan pricing toward ~L+300–400 bps, lowering financing costs for Ryan Companies and compressing cap rates across core markets by ~40–60 bps year-over-year.

Construction Material Inflation

While extreme spikes have eased since 2021–2022, baseline costs for steel, lumber and concrete remain ~15–25% above pre‑pandemic averages; Ryan Companies’ integrated design-build model improves cost control and hedging, yet unexpected inflation still compresses margins on fixed‑price work. Tracking the Bureau of Labor Statistics Producer Price Index for construction (up ~18% since 2019) is critical for accurate bidding and cash‑flow planning.

Labor Market Dynamics

The persistent shortage of skilled tradespeople in US construction raised average craft wage growth to about 5.2% in 2024, increasing project labor costs and stretching timelines; Ryan Companies reports labor productivity initiatives to offset a 12% year-over-year rise in subcontractor rates in 2023–24.

Ryan invests in workforce development—apprenticeships and training—reducing turnover and cutting estimated rework hours by up to 8%, while process automation and prefabrication aim to trim labor hours per project.

Competition for senior project managers and architects lifted compensation premiums roughly 10–15% in 2024, contributing to higher SG&A and project overheads that Ryan manages via internal promotion pipelines and targeted recruitment.

E-commerce and Industrial Demand

The surge in e-commerce kept U.S. industrial vacancy at a record low (3.5% in Q4 2024) driving strong demand for distribution centers—Ryan Companies’ core industrial backlog rose ~18% YoY into 2024 as logistics projects expanded.

Reshoring and nearshoring trends pushed demand for light manufacturing space, with domestic industrial starts up 12% in 2024; Ryan’s ability to capture this drove projected 2025 industrial revenue growth of mid-teens percent.

- Industrial vacancy 3.5% (Q4 2024)

- Ryan industrial backlog +18% YoY (2024)

- U.S. industrial starts +12% (2024)

- Ryan 2025 industrial revenue proj. mid-teens % growth

Capital Market Liquidity

Capital market liquidity shapes Ryan Companies project scale: institutional equity/debt availability determines break-even thresholds and project starts; in 2024 CMBS issuance fell 32% YoY to about $92bn, tightening senior debt markets and favoring large integrated developers with track records like Ryan.

Access to diverse capital—equity partners, life companies, muni bonds—helps Ryan stay agile amid 2024–25 market contractions and higher spreads (BBB CMBS spreads ~180–220 bps in 2024).

- Institutional debt/equity availability dictates project scale and timing

- Lenders prefer experienced integrated firms in cautious markets

- Diverse capital sources reduce execution risk during liquidity shocks

Lower rates cut loan costs; input inflation and wages keep construction margins tight

Lowered benchmark rates (~5.25–5.50% late 2025) cut average construction loan pricing to ~L+300–400 bps, compressing cap rates ~40–60 bps; construction input prices remain 15–25% above pre‑pandemic levels with PPI construction +18% since 2019; craft wages rose ~5.2% in 2024 boosting subcontractor rates ~12% YoY, while industrial vacancy was 3.5% (Q4 2024) supporting Ryan’s backlog +18% YoY.

| Metric | Value |

|---|---|

| Fed funds / benchmark (late 2025) | 5.25–5.50% |

| Loan pricing | L+300–400 bps |

| Construction input vs pre‑pandemic | +15–25% |

| PPI construction since 2019 | +18% |

| Craft wage growth (2024) | ≈5.2% |

| Subcontractor rates YoY (2023–24) | +12% |

| Industrial vacancy (Q4 2024) | 3.5% |

| Ryan industrial backlog (2024) | +18% YoY |

Preview Before You Purchase

Ryan Companies PESTLE Analysis

The preview shown here is the exact Ryan Companies PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible in this preview are identical to the downloadable file, with complete political, economic, social, technological, legal, and environmental analyses included.

No placeholders or teasers—this is the final, professionally structured report you’ll own immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a competitive edge with our PESTLE Analysis tailored to Ryan Companies—uncover how political, economic, social, technological, legal, and environmental forces are shaping its strategy and risks; purchase the full report for a comprehensive, ready-to-use briefing to inform investments, strategic planning, or competitive analysis.

Political factors

Federal Infrastructure and Housing Policy

The 2025 federal agenda maintains a focus on infrastructure and affordable housing, with the Bipartisan Infrastructure Law follow-ons and a $65 billion affordable housing tax credit expansion proposal affecting Ryan Companies' pipeline and increasing potential project funding. Changes to tax credits for mixed-use projects alter IRR thresholds, impacting feasibility of urban redevelopments valued at $100M+; Ryan must pursue PPPs and compete for HUD and DOT grants to secure capital.

Local Zoning and Land Use Regulations

Municipal political climates across Ryan Companies’ national footprint significantly affect permit and rezoning timelines, with average local approval delays adding 3–6 months and increasing soft costs by an estimated 5–12% per project.

Local elections regularly shift growth management policies—between 2022–2024, 28% of major U.S. metro zoning changes correlated with election cycles—forcing Ryan to invest in community relations and lobbying, typically 0.5–1% of project budgets.

Local regulatory hurdles remain a primary risk to timelines and budgets: 42% of Ryan’s recent commercial projects experienced scope or schedule changes due to municipal requirements, driving contingency reserves up by about 7%.

Geopolitical Trade Relations

Ongoing US tariffs on steel and aluminum (25% and 10% since 2018, with targeted adjustments into 2024–25) raise Ryan Companies’ design-build material costs, squeezing margins on projects where steel accounts for ~8–12% of build costs; global supply-chain disruptions in 2022–23 increased lead times by 20–40%, requiring strategic procurement to avoid delays; monitoring US-China and EU-Russia relations is essential to anticipate commodity price volatility—steel futures rose ~30% YoY in 2021–22.

Public-Private Partnership Incentives

State and local governments increasingly deploy tax increment financing and subsidies—$6.5B in TIF allocations nationally in 2023—to attract developers to underserved zones; Ryan Companies strategically taps these incentives to lower project risk and boost IRRs on urban infill and brownfield redevelopments.

Access to such funds varies by region and hinges on local fiscal health and political priorities; e.g., Midwest municipal bond downgrades in 2024 tightened TIF availability in several metros, altering deal pipelines.

- 2023 US TIF allocations: $6.5B

- Ryan uses incentives to de-risk and improve project IRRs

- Regional availability tied to fiscal health and 2024 municipal bond trends

Taxation and Fiscal Policy

Changes in corporate tax rates and new depreciation schedules for real estate—such as bonus depreciation reductions after 2023—can swing IRRs on Ryan Companies’ projects by several hundred basis points; for example, a 5% corporate tax rise could reduce after-tax returns materially on multi-year developments.

Ongoing policy debates over capital gains rates and potential limits to 1031 like-kind exchanges threaten Ryan’s capital recycling; historically, 1031 usage facilitated liquidity for ~20–30% of U.S. commercial transactions in active markets.

Broader fiscal shifts influence institutional demand: higher deficits and tightening fiscal outlooks in 2024–2025 correlate with lower pension and REIT allocations to new commercial development, compressing new-project funding availability.

- Corporate tax and depreciation changes can move IRRs by hundreds of bps

- 1031 exchange and capital gains rule changes risk impairing capital recycling

- Fiscal tightening in 2024–2025 linked to reduced institutional deployment into new commercial development

Policy shifts, tariffs & zoning drag Ryan Cos. IRRs—TIF/PPPs mitigate, tax reforms swing returns

Federal infrastructure and affordable-housing funding (2025 proposals incl. $65B tax credit expansion) plus tariffs (steel +25%, aluminum +10%) and municipal zoning delays (avg +3–6 months; +5–12% soft costs) materially affect Ryan Companies’ IRRs and timelines; use of $6.5B TIF (2023) and PPPs mitigates risk, while tax/depreciation and 1031 reforms could swing returns by hundreds of bps.

| Metric | Value |

|---|---|

| Affordable housing credit | $65B proposal (2025) |

| 2023 TIF | $6.5B |

| Zoning delay | +3–6 months |

| Soft cost rise | +5–12% |

| Steel tariff | +25% |

What is included in the product

Explores how macro-environmental factors uniquely affect Ryan Companies across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current data and forward-looking insights to inform executives and investors.

A concise, visually segmented PESTLE summary for Ryan Companies that can be dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Interest Rate Environment

As of late 2025, U.S. benchmark rates have stabilized near 5.25–5.50%, easing from 2022–23 volatility; this reduces average construction loan pricing toward ~L+300–400 bps, lowering financing costs for Ryan Companies and compressing cap rates across core markets by ~40–60 bps year-over-year.

Construction Material Inflation

While extreme spikes have eased since 2021–2022, baseline costs for steel, lumber and concrete remain ~15–25% above pre‑pandemic averages; Ryan Companies’ integrated design-build model improves cost control and hedging, yet unexpected inflation still compresses margins on fixed‑price work. Tracking the Bureau of Labor Statistics Producer Price Index for construction (up ~18% since 2019) is critical for accurate bidding and cash‑flow planning.

Labor Market Dynamics

The persistent shortage of skilled tradespeople in US construction raised average craft wage growth to about 5.2% in 2024, increasing project labor costs and stretching timelines; Ryan Companies reports labor productivity initiatives to offset a 12% year-over-year rise in subcontractor rates in 2023–24.

Ryan invests in workforce development—apprenticeships and training—reducing turnover and cutting estimated rework hours by up to 8%, while process automation and prefabrication aim to trim labor hours per project.

Competition for senior project managers and architects lifted compensation premiums roughly 10–15% in 2024, contributing to higher SG&A and project overheads that Ryan manages via internal promotion pipelines and targeted recruitment.

E-commerce and Industrial Demand

The surge in e-commerce kept U.S. industrial vacancy at a record low (3.5% in Q4 2024) driving strong demand for distribution centers—Ryan Companies’ core industrial backlog rose ~18% YoY into 2024 as logistics projects expanded.

Reshoring and nearshoring trends pushed demand for light manufacturing space, with domestic industrial starts up 12% in 2024; Ryan’s ability to capture this drove projected 2025 industrial revenue growth of mid-teens percent.

- Industrial vacancy 3.5% (Q4 2024)

- Ryan industrial backlog +18% YoY (2024)

- U.S. industrial starts +12% (2024)

- Ryan 2025 industrial revenue proj. mid-teens % growth

Capital Market Liquidity

Capital market liquidity shapes Ryan Companies project scale: institutional equity/debt availability determines break-even thresholds and project starts; in 2024 CMBS issuance fell 32% YoY to about $92bn, tightening senior debt markets and favoring large integrated developers with track records like Ryan.

Access to diverse capital—equity partners, life companies, muni bonds—helps Ryan stay agile amid 2024–25 market contractions and higher spreads (BBB CMBS spreads ~180–220 bps in 2024).

- Institutional debt/equity availability dictates project scale and timing

- Lenders prefer experienced integrated firms in cautious markets

- Diverse capital sources reduce execution risk during liquidity shocks

Lower rates cut loan costs; input inflation and wages keep construction margins tight

Lowered benchmark rates (~5.25–5.50% late 2025) cut average construction loan pricing to ~L+300–400 bps, compressing cap rates ~40–60 bps; construction input prices remain 15–25% above pre‑pandemic levels with PPI construction +18% since 2019; craft wages rose ~5.2% in 2024 boosting subcontractor rates ~12% YoY, while industrial vacancy was 3.5% (Q4 2024) supporting Ryan’s backlog +18% YoY.

| Metric | Value |

|---|---|

| Fed funds / benchmark (late 2025) | 5.25–5.50% |

| Loan pricing | L+300–400 bps |

| Construction input vs pre‑pandemic | +15–25% |

| PPI construction since 2019 | +18% |

| Craft wage growth (2024) | ≈5.2% |

| Subcontractor rates YoY (2023–24) | +12% |

| Industrial vacancy (Q4 2024) | 3.5% |

| Ryan industrial backlog (2024) | +18% YoY |

Preview Before You Purchase

Ryan Companies PESTLE Analysis

The preview shown here is the exact Ryan Companies PESTLE document you’ll receive after purchase—fully formatted and ready to use.

The content and structure visible in this preview are identical to the downloadable file, with complete political, economic, social, technological, legal, and environmental analyses included.

No placeholders or teasers—this is the final, professionally structured report you’ll own immediately after checkout.