Ryan Specialty Group Porter's Five Forces Analysis

Don't Miss the Bigger Picture

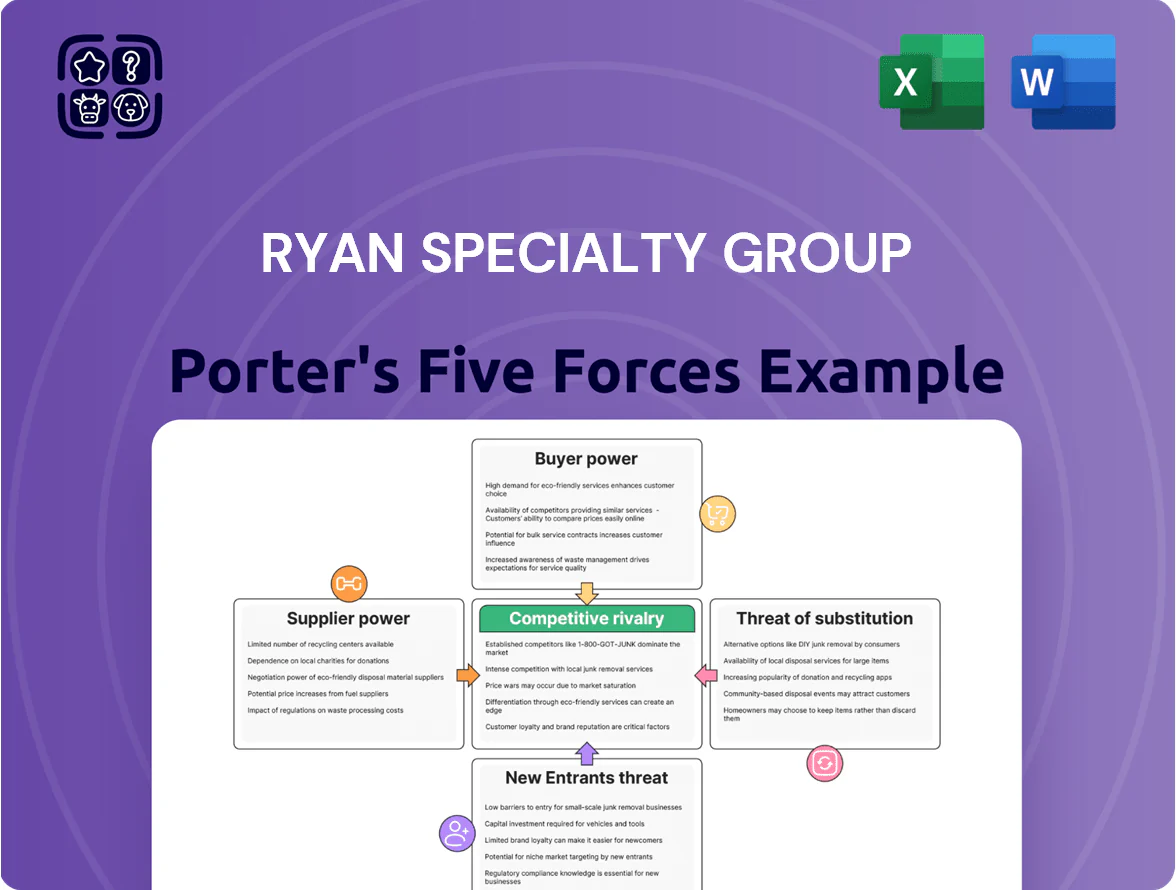

Ryan Specialty Group faces moderate buyer power, concentrated commercial clients, and differentiated specialty offerings that limit direct price pressure, while supplier leverage and regulatory complexity create operational constraints.

Competitive rivalry is intense among niche brokers and underwriting partners, with moderate threat from new entrants due to scale and compliance barriers, and substitution risk tied to insurtech innovations.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ryan Specialty Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Carrier capacity concentration

Primary suppliers are high-rated specialty carriers supplying underwriting capacity; by late 2025 roughly 60% of available excess & surplus (E&S) specialty capacity in key lines sat with a handful of firms, concentrating supplier power.

Ryan Specialty counters this concentration by using a diversified panel of 180+ carrier relationships and $1.2 billion of managed premium (2024 run-rate), letting it secure access and negotiate terms despite carrier limits.

Underwriting authority limitations

Suppliers exert power via binding-authority terms granted to Ryan Specialty’s Managing General Underwriters (MGUs); if carriers tighten appetite for high-risk classes, Ryan’s revenue in those niches falls—in 2024 MGUs produced ~28% of firm revenue, so restrictions matter.

Ryan mitigates by posting superior loss ratios (reported combined ratio 90.5% in 2024), encouraging carriers to keep or expand delegated authority and preserve underwriting capacity.

Reinsurance market volatility

The cost and availability of reinsurance act as a secondary supplier force that limits Ryan Specialty Group’s client capacity; global facultative reinsurance rates rose ~22% in 2023–24, tightening capacity in casualty and cyber lines. When reinsurer capital withdraws, primary carriers often reduce exposure in specialty segments, lowering Ryan’s placement options and pricing power. Ryan counters by using capital-markets risk transfer—ILS and sidecars—sourcing alternative capacity; in 2024 its ILS placements exceeded $250m.

Talent as a critical resource

In specialty insurance, elite underwriters and brokers are scarce human-capital suppliers with strong bargaining power, especially for complex, non-standard risks where global talent shortages persist.

Recruitment and retention costs stay high—industry surveys in 2024 showed 62% of specialty firms reported talent shortages and median producer compensation rose ~18% YoY; losing a top underwriter can cut business lines quickly.

Ryan Specialty counters this with an entrepreneurial culture and equity-based incentives that tie key producers to firm performance, supporting retention and aligning interests while managing cost through revenue-sharing models.

- 62% of specialty firms reported talent shortages (2024 survey)

- Median producer pay +18% YoY (2024 data)

- Equity incentives used to align producers with firm results

- Entrepreneurial culture reduces voluntary turnover

Technological infrastructure providers

The reliance on cloud policy platforms and advanced analytics gives tech vendors moderate bargaining power; IDC reported enterprise cloud spend in insurance rose 18% in 2024 to $13.6B, raising vendor influence.

As Ryan Specialty adds AI-driven underwriting and proprietary data tools, switching costs across major platforms rise, but RyanSG investment—capex ~ $45M in 2024—cuts third-party dependence.

- 2024 insurance cloud spend +18% to $13.6B

- RyanSG capex ~ $45M in 2024

- AI/tools increase switching costs

- Proprietary tech reduces vendor leverage

Ryan offsets carrier concentration with 180+ partners, $1.2B premium and tech/talent bets

Suppliers concentrated: ~60% of E&S specialty capacity sat with few carriers by late 2025, raising supplier leverage. Ryan offsets concentration via 180+ carrier relationships and $1.2B managed premium (2024 run‑rate) and ILS/sidecars ($250M+ in 2024). Talent and tech add pressure: 62% of firms reported shortages and median producer pay +18% YoY (2024); Ryan capex ~$45M (2024) and equity incentives reduce supplier risk.

| Metric | Value |

|---|---|

| Concentration | ~60% E&S capacity (late 2025) |

| Carrier panel | 180+ |

| Managed premium | $1.2B (2024) |

| ILS placements | $250M+ (2024) |

| Talent shortage | 62% firms (2024) |

| Producer pay | +18% YoY (2024) |

| Capex | $45M (2024) |

What is included in the product

Tailored exclusively for Ryan Specialty Group, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

A concise Porter's Five Forces one-sheet for Ryan Specialty Group—distills market power, supplier/buyer pressure, threat of substitutes/entrants, and competitive rivalry into actionable insights for faster strategic decisions.

Customers Bargaining Power

Consolidation of retail brokerages

Consolidation among retail brokerages—driven by 2023–2025 M&A—has produced global broker groups controlling an estimated 30–40% of U.S. retail placement volume, raising their leverage to demand higher commission splits from carriers like Ryan Specialty.

Ryan Specialty counters this customer bargaining power by offering niche products and access to specialist markets (excess casualty, political risk) that large retail brokers cannot easily replicate, preserving placement margins and strategic relationships.

Low switching costs for agents

Retail agents can shift specialty lines easily, pressuring Ryan Specialty to compete on price, speed, and ease; industry surveys in 2024 show 62% of retail brokers switched wholesalers at least once in two years.

That low switching cost forces Ryan to prove value via superior underwriting and service; Ryan reported 2024 digital submissions up 28%, supporting faster placement times.

Ryan’s platform creates a sticky ecosystem—integrations, portal analytics, and a 2024 retention lift estimate of ~15%—discouraging agents from moving business.

Demand for price transparency

As digital comparison tools grow, 62% of commercial buyers now check multiple platforms before buying, increasing price transparency and pressuring margins across wholesale channels.

Retail agents use visible market rates to push wholesalers to match lowest offers, contributing to reported industry underwriting margin compression of ~120 basis points in 2024.

Ryan Specialty counters by targeting complex, high-touch risks where bespoke wording and specialty expertise reduce price sensitivity and preserve higher loss-adjusted margins.

Sophistication of insured entities

Large corporate insureds are using advanced risk management and increasingly demand specific carriers or structures; in 2024 global captive insurance formations rose 8%, showing this trend.

When a client insists on a carrier, retail brokers must comply, shifting bargaining power away from wholesalers and pressuring margin and placement flexibility.

Ryan Specialty preserves leverage by cultivating direct relationships with complex end-insureds—over 120 strategic accounts in 2024—keeping its products preferred for bespoke risks.

- Corporate sophistication up; captive setups +8% (2024)

- Client-mandated carriers reduce wholesaler leverage

- Ryan: 120+ strategic accounts (2024) maintains preference

Access to alternative risk markets

Large buyers can bypass brokers via captives or digital direct platforms; captive insurers held about 7,000 risk-bearing entities globally in 2024, raising placement leverage for standard and semi-specialty lines.

Ryan Specialty targets distressed, complex E&S niches—areas where captives and direct platforms are usually impractical—preserving placement power and higher margins.

- Captives: ~7,000 entities (2024)

- Direct platforms: rapid growth, >20% annual uptake in commercial lines 2022–24

- Ryan focus: complex E&S where alternatives scarce

Ryan fights broker power with niche focus, digital growth and a ~15% retention boost

Customers’ bargaining power is high due to broker consolidation (30–40% U.S. retail volume, 2023–25), easy switching (62% switched wholesalers in 2 years, 2024), digital price transparency (62% check multiple platforms, 2024), and captive growth (+8%, 2024). Ryan defends margins via specialist niches, 120+ strategic accounts (2024), 28% digital submissions growth (2024), and estimated 15% retention lift from its platform.

| Metric | 2024/2025 |

|---|---|

| Broker concentration | 30–40% |

| Broker switching | 62% |

| Captives | +8% |

| Digital submissions | +28% |

| Retention lift | ~15% |

Preview Before You Purchase

Ryan Specialty Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Ryan Specialty Group you'll receive upon purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Ryan Specialty Group faces moderate buyer power, concentrated commercial clients, and differentiated specialty offerings that limit direct price pressure, while supplier leverage and regulatory complexity create operational constraints.

Competitive rivalry is intense among niche brokers and underwriting partners, with moderate threat from new entrants due to scale and compliance barriers, and substitution risk tied to insurtech innovations.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Ryan Specialty Group’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Carrier capacity concentration

Primary suppliers are high-rated specialty carriers supplying underwriting capacity; by late 2025 roughly 60% of available excess & surplus (E&S) specialty capacity in key lines sat with a handful of firms, concentrating supplier power.

Ryan Specialty counters this concentration by using a diversified panel of 180+ carrier relationships and $1.2 billion of managed premium (2024 run-rate), letting it secure access and negotiate terms despite carrier limits.

Underwriting authority limitations

Suppliers exert power via binding-authority terms granted to Ryan Specialty’s Managing General Underwriters (MGUs); if carriers tighten appetite for high-risk classes, Ryan’s revenue in those niches falls—in 2024 MGUs produced ~28% of firm revenue, so restrictions matter.

Ryan mitigates by posting superior loss ratios (reported combined ratio 90.5% in 2024), encouraging carriers to keep or expand delegated authority and preserve underwriting capacity.

Reinsurance market volatility

The cost and availability of reinsurance act as a secondary supplier force that limits Ryan Specialty Group’s client capacity; global facultative reinsurance rates rose ~22% in 2023–24, tightening capacity in casualty and cyber lines. When reinsurer capital withdraws, primary carriers often reduce exposure in specialty segments, lowering Ryan’s placement options and pricing power. Ryan counters by using capital-markets risk transfer—ILS and sidecars—sourcing alternative capacity; in 2024 its ILS placements exceeded $250m.

Talent as a critical resource

In specialty insurance, elite underwriters and brokers are scarce human-capital suppliers with strong bargaining power, especially for complex, non-standard risks where global talent shortages persist.

Recruitment and retention costs stay high—industry surveys in 2024 showed 62% of specialty firms reported talent shortages and median producer compensation rose ~18% YoY; losing a top underwriter can cut business lines quickly.

Ryan Specialty counters this with an entrepreneurial culture and equity-based incentives that tie key producers to firm performance, supporting retention and aligning interests while managing cost through revenue-sharing models.

- 62% of specialty firms reported talent shortages (2024 survey)

- Median producer pay +18% YoY (2024 data)

- Equity incentives used to align producers with firm results

- Entrepreneurial culture reduces voluntary turnover

Technological infrastructure providers

The reliance on cloud policy platforms and advanced analytics gives tech vendors moderate bargaining power; IDC reported enterprise cloud spend in insurance rose 18% in 2024 to $13.6B, raising vendor influence.

As Ryan Specialty adds AI-driven underwriting and proprietary data tools, switching costs across major platforms rise, but RyanSG investment—capex ~ $45M in 2024—cuts third-party dependence.

- 2024 insurance cloud spend +18% to $13.6B

- RyanSG capex ~ $45M in 2024

- AI/tools increase switching costs

- Proprietary tech reduces vendor leverage

Ryan offsets carrier concentration with 180+ partners, $1.2B premium and tech/talent bets

Suppliers concentrated: ~60% of E&S specialty capacity sat with few carriers by late 2025, raising supplier leverage. Ryan offsets concentration via 180+ carrier relationships and $1.2B managed premium (2024 run‑rate) and ILS/sidecars ($250M+ in 2024). Talent and tech add pressure: 62% of firms reported shortages and median producer pay +18% YoY (2024); Ryan capex ~$45M (2024) and equity incentives reduce supplier risk.

| Metric | Value |

|---|---|

| Concentration | ~60% E&S capacity (late 2025) |

| Carrier panel | 180+ |

| Managed premium | $1.2B (2024) |

| ILS placements | $250M+ (2024) |

| Talent shortage | 62% firms (2024) |

| Producer pay | +18% YoY (2024) |

| Capex | $45M (2024) |

What is included in the product

Tailored exclusively for Ryan Specialty Group, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier influence, entry barriers, substitutes, and emerging threats that shape its pricing power and strategic positioning.

A concise Porter's Five Forces one-sheet for Ryan Specialty Group—distills market power, supplier/buyer pressure, threat of substitutes/entrants, and competitive rivalry into actionable insights for faster strategic decisions.

Customers Bargaining Power

Consolidation of retail brokerages

Consolidation among retail brokerages—driven by 2023–2025 M&A—has produced global broker groups controlling an estimated 30–40% of U.S. retail placement volume, raising their leverage to demand higher commission splits from carriers like Ryan Specialty.

Ryan Specialty counters this customer bargaining power by offering niche products and access to specialist markets (excess casualty, political risk) that large retail brokers cannot easily replicate, preserving placement margins and strategic relationships.

Low switching costs for agents

Retail agents can shift specialty lines easily, pressuring Ryan Specialty to compete on price, speed, and ease; industry surveys in 2024 show 62% of retail brokers switched wholesalers at least once in two years.

That low switching cost forces Ryan to prove value via superior underwriting and service; Ryan reported 2024 digital submissions up 28%, supporting faster placement times.

Ryan’s platform creates a sticky ecosystem—integrations, portal analytics, and a 2024 retention lift estimate of ~15%—discouraging agents from moving business.

Demand for price transparency

As digital comparison tools grow, 62% of commercial buyers now check multiple platforms before buying, increasing price transparency and pressuring margins across wholesale channels.

Retail agents use visible market rates to push wholesalers to match lowest offers, contributing to reported industry underwriting margin compression of ~120 basis points in 2024.

Ryan Specialty counters by targeting complex, high-touch risks where bespoke wording and specialty expertise reduce price sensitivity and preserve higher loss-adjusted margins.

Sophistication of insured entities

Large corporate insureds are using advanced risk management and increasingly demand specific carriers or structures; in 2024 global captive insurance formations rose 8%, showing this trend.

When a client insists on a carrier, retail brokers must comply, shifting bargaining power away from wholesalers and pressuring margin and placement flexibility.

Ryan Specialty preserves leverage by cultivating direct relationships with complex end-insureds—over 120 strategic accounts in 2024—keeping its products preferred for bespoke risks.

- Corporate sophistication up; captive setups +8% (2024)

- Client-mandated carriers reduce wholesaler leverage

- Ryan: 120+ strategic accounts (2024) maintains preference

Access to alternative risk markets

Large buyers can bypass brokers via captives or digital direct platforms; captive insurers held about 7,000 risk-bearing entities globally in 2024, raising placement leverage for standard and semi-specialty lines.

Ryan Specialty targets distressed, complex E&S niches—areas where captives and direct platforms are usually impractical—preserving placement power and higher margins.

- Captives: ~7,000 entities (2024)

- Direct platforms: rapid growth, >20% annual uptake in commercial lines 2022–24

- Ryan focus: complex E&S where alternatives scarce

Ryan fights broker power with niche focus, digital growth and a ~15% retention boost

Customers’ bargaining power is high due to broker consolidation (30–40% U.S. retail volume, 2023–25), easy switching (62% switched wholesalers in 2 years, 2024), digital price transparency (62% check multiple platforms, 2024), and captive growth (+8%, 2024). Ryan defends margins via specialist niches, 120+ strategic accounts (2024), 28% digital submissions growth (2024), and estimated 15% retention lift from its platform.

| Metric | 2024/2025 |

|---|---|

| Broker concentration | 30–40% |

| Broker switching | 62% |

| Captives | +8% |

| Digital submissions | +28% |

| Retention lift | ~15% |

Preview Before You Purchase

Ryan Specialty Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Ryan Specialty Group you'll receive upon purchase—fully formatted, professionally written, and ready for immediate download with no placeholders or samples.