Ryan Specialty Group PESTLE Analysis

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Ryan Specialty Group—spot regulatory, economic, and technological forces shaping its competitive edge and risk profile. Ideal for investors and strategists, this brief highlights actionable trends; purchase the full report for a complete, editable breakdown and immediate insights to steer smarter decisions.

Political factors

US Federal and State Regulatory Shifts

The post-2024 election regulatory landscape has increased variability for specialty brokers; 22 states saw insurance commissioner turnover in 2024–25, driving divergent compliance directives that affect non-admitted market access and filings.

Ryan Specialty must adapt processes—its 2025 Q1 reported 8% growth in wholesale premiums—while aligning underwriting and surplus lines placement with state-by-state rule changes to avoid fines and market disruption.

International Trade and Geopolitical Stability

As Ryan Specialty grows in the UK and Europe—markets where Ryan Group reported over $1.2bn revenue in fiscal 2024—geopolitical stability is critical for continuity; Brexit-related regulatory divergence and Russia-Ukraine spillovers raised cross-border placement costs by an estimated 5–8% in 2023–24 for specialty insurers.

Government Backstops and Public-Private Partnerships

Ryan Specialty’s demand for private specialty insurance is tied to government backstops for catastrophic risks; U.S. Terrorism Risk Insurance Program (TRIPRA) extensions and federal cyber backstop proposals (e.g., 2024 congressional estimates of $50–100bn modeled losses for systemic cyber events) shape market capacity.

Political moves to extend or alter backstops directly affect Ryan’s product development and pricing, prompting adjustments in capital allocation and reinsurance buying, given industry loss volatility.

The firm must align offerings with federal safety nets to cover high‑severity, low‑frequency events, coordinating limits and exclusions so combined private/public coverage addresses modeled tail risks.

Corporate Tax Reform and Fiscal Policy

Changes in federal corporate tax rates—such as the 21% rate under current law and any proposed adjustments—directly affect Ryan Specialty Group’s net income and free cash flow, impacting earnings per share and dividend capacity through 2025.

Political debates over targeted tax incentives for sectors like construction and cyber risk reshape client demand for specialty insurance products, potentially altering premium mix and loss exposure.

Active monitoring of legislative proposals and fiscal policy shifts is essential for accurate forecasting and strategic capital allocation, with scenario modeling to reflect tax-change sensitivities through year-end 2025.

- 21% current federal rate; any +/- shifts materially affect net income

- Industry-specific incentives can change premium demand and risk profiles

- Scenario-based forecasts needed for capital allocation through 2025

National Security and Cyber Warfare Policies

Rising geopolitical tensions and a 38% increase in reported state-linked cyber incidents in 2023 have pushed governments to mandate critical infrastructure resilience, expanding market demand for advanced cyber risk transfer solutions that Ryan Specialty Group underwrites via its managing general agents.

Shifts in legislation and insurer guidance on acts of war/terrorism force Ryan Specialty to revise policy wordings and exclusions to remain enforceable and to price elevated accumulation risks—global cyber insurance premiums grew 24% in 2024, underscoring opportunity and exposure.

- 38% rise in state-linked cyber incidents (2023)

- Global cyber premiums +24% (2024)

- Need to update war/terror definitions to avoid coverage disputes

Regulatory churn, Brexit costs and cyber risk reshape Ryan Specialty’s pricing & capital

Political volatility since 2024 raised state regulator turnover (22 states) and variable non‑admitted rules, impacting Ryan Specialty’s 8% wholesale premium growth and compliance workload; UK/EU revenue exposure ($1.2bn FY2024) faces Brexit divergence and geopolitical spillovers (5–8% cross‑border cost rise); federal backstop changes (TRIPRA, cyber models $50–100bn) and 21% tax rate shifts drive pricing, capital and reinsurance strategy.

| Metric | Value |

|---|---|

| States with regulator turnover | 22 |

| Wholesale premium growth Q1 2025 | +8% |

| Ryan Group revenue UK/EU FY2024 | $1.2bn |

| Cross‑border cost rise | 5–8% |

| Cyber modeled loss range | $50–100bn |

| Federal corporate tax rate | 21% |

What is included in the product

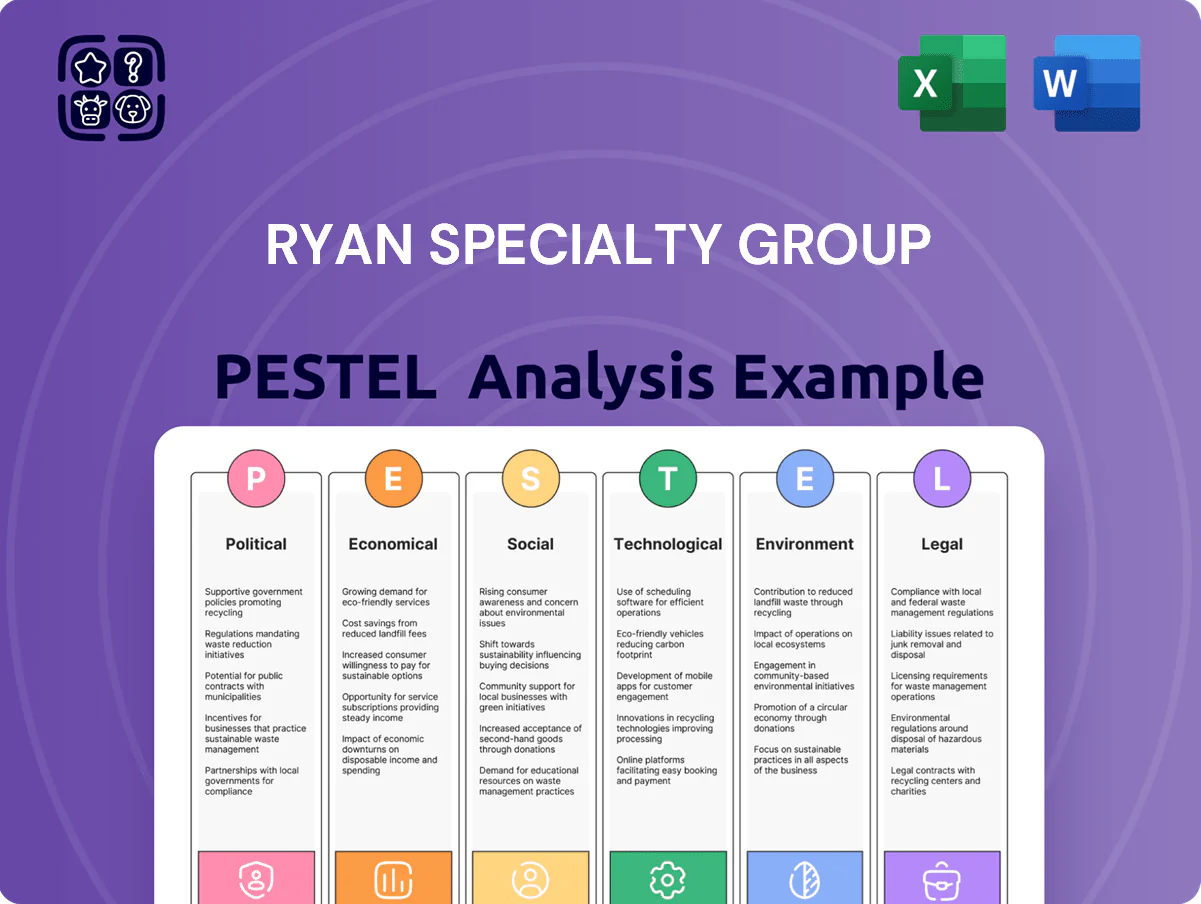

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Ryan Specialty Group, with data-driven trends, region- and industry-specific examples, and forward-looking insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, visually segmented PESTLE summary for Ryan Specialty Group that simplifies external risk and market-position insights for quick inclusion in presentations, team alignment, or client reports.

Economic factors

Interest Rate Volatility and Investment Income

Stabilization of U.S. policy rates through 2025 (Fed funds range ~5.25–5.50% as of Dec 2025) boosts Ryan Specialty’s fiduciary investment income from held-premium portfolios, improving yield on short-duration bonds and cash; higher rates also raise acquisition financing costs—12-month BAA corporate yields averaged ~5.6% in 2025—so debt management and interest-rate hedging are pivotal to preserve ROE and support M&A cadence.

Hard vs Soft Market Cycles in Excess and Surplus

The specialty insurance market is highly cyclical; hard markets push pricing up and Ryan Specialty benefits when risks are hard to place, contributing to its 2024-25 revenue resilience with brokered premium growth near industry-beating mid-teens levels. As select lines showed softening by late 2025—rate deceleration of roughly 5–8% in some commercial casualty segments—Ryan must lean on technical underwriting expertise and carrier relationships to protect margins. Strategic adjustments in volume mix and commission structures, including shifting toward higher-fee lines and performance-based commissions, are required to sustain EBITDA margins around the firm’s target range.

Inflationary Pressures on Claims Costs

Economic and social inflation raised US insured claim severity ~7–9% in 2023–2024, pushing Ryan Specialty to raise premiums and employ specialized underwriting to cover higher material, labor and settlement costs.

Sustained inflation—CPI ~3.4% in 2024 and construction cost indices up 6–8%—forces continuous recalibration of risk appetite and pricing models to protect broker margins and carrier profitability.

Global Economic Growth and Commercial Activity

The 2024 global economy expanded ~3.0% after 2023 weakness, supporting higher commercial activity and rising demand for business insurance across sectors.

Growth in tech, renewables and logistics increases demand for complex specialty coverage, aligning with Ryan Specialty’s risk solutions portfolio.

A GDP slowdown (e.g., IMF downside of 2.6% base case) could cut new business formation and premium growth, so continuous economic monitoring is critical.

- Global GDP ~3.0% (2024 est)

- Rising sectoral demand: tech, renewables, logistics

- GDP slowdown risks lower premiums/new firms

Consolidation and M&A Capital Availability

The availability of capital for M&A drives Ryan Specialty’s inorganic growth; global PE dry powder exceeded $2.2 trillion in 2024, supporting deal activity in specialty insurance. Favorable credit conditions enabled Ryan to acquire niche agencies and talent to broaden capabilities, while a tightening—US bank lending standards rose in 2024—could slow acquisitions. In that case, Ryan would emphasize organic growth and efficiency improvements.

- 2024 global PE dry powder: $2.2T+

- US bank lending standards: tightened in 2024

- Inorganic growth risk if credit tightens

- Shift to organic growth and efficiencies as mitigation

Higher rates lift yields and costs; insurers recalibrate amid rising claims and M&A firepower

Higher policy rates (Fed funds ~5.25–5.50% by Dec 2025) lift investment yields but raise acquisition financing costs; insured claim severity rose ~7–9% (2023–24) with CPI ~3.4% in 2024, forcing pricing and underwriting recalibration. Global GDP ~3.0% (2024) and sectoral demand (tech, renewables, logistics) support premium growth, while PE dry powder ~$2.2T (2024) underpins M&A; credit tightening risks slowing inorganic growth.

| Metric | Value |

|---|---|

| Fed funds (Dec 2025) | 5.25–5.50% |

| CPI (2024) | 3.4% |

| Claim severity rise | 7–9% |

| Global GDP (2024) | ~3.0% |

| PE dry powder (2024) | ~$2.2T |

Preview Before You Purchase

Ryan Specialty Group PESTLE Analysis

The preview shown here is the exact Ryan Specialty Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

This final document is professionally structured and ready for analysis, presentation, or integration into your due diligence materials.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Unlock strategic clarity with our concise PESTLE Analysis of Ryan Specialty Group—spot regulatory, economic, and technological forces shaping its competitive edge and risk profile. Ideal for investors and strategists, this brief highlights actionable trends; purchase the full report for a complete, editable breakdown and immediate insights to steer smarter decisions.

Political factors

US Federal and State Regulatory Shifts

The post-2024 election regulatory landscape has increased variability for specialty brokers; 22 states saw insurance commissioner turnover in 2024–25, driving divergent compliance directives that affect non-admitted market access and filings.

Ryan Specialty must adapt processes—its 2025 Q1 reported 8% growth in wholesale premiums—while aligning underwriting and surplus lines placement with state-by-state rule changes to avoid fines and market disruption.

International Trade and Geopolitical Stability

As Ryan Specialty grows in the UK and Europe—markets where Ryan Group reported over $1.2bn revenue in fiscal 2024—geopolitical stability is critical for continuity; Brexit-related regulatory divergence and Russia-Ukraine spillovers raised cross-border placement costs by an estimated 5–8% in 2023–24 for specialty insurers.

Government Backstops and Public-Private Partnerships

Ryan Specialty’s demand for private specialty insurance is tied to government backstops for catastrophic risks; U.S. Terrorism Risk Insurance Program (TRIPRA) extensions and federal cyber backstop proposals (e.g., 2024 congressional estimates of $50–100bn modeled losses for systemic cyber events) shape market capacity.

Political moves to extend or alter backstops directly affect Ryan’s product development and pricing, prompting adjustments in capital allocation and reinsurance buying, given industry loss volatility.

The firm must align offerings with federal safety nets to cover high‑severity, low‑frequency events, coordinating limits and exclusions so combined private/public coverage addresses modeled tail risks.

Corporate Tax Reform and Fiscal Policy

Changes in federal corporate tax rates—such as the 21% rate under current law and any proposed adjustments—directly affect Ryan Specialty Group’s net income and free cash flow, impacting earnings per share and dividend capacity through 2025.

Political debates over targeted tax incentives for sectors like construction and cyber risk reshape client demand for specialty insurance products, potentially altering premium mix and loss exposure.

Active monitoring of legislative proposals and fiscal policy shifts is essential for accurate forecasting and strategic capital allocation, with scenario modeling to reflect tax-change sensitivities through year-end 2025.

- 21% current federal rate; any +/- shifts materially affect net income

- Industry-specific incentives can change premium demand and risk profiles

- Scenario-based forecasts needed for capital allocation through 2025

National Security and Cyber Warfare Policies

Rising geopolitical tensions and a 38% increase in reported state-linked cyber incidents in 2023 have pushed governments to mandate critical infrastructure resilience, expanding market demand for advanced cyber risk transfer solutions that Ryan Specialty Group underwrites via its managing general agents.

Shifts in legislation and insurer guidance on acts of war/terrorism force Ryan Specialty to revise policy wordings and exclusions to remain enforceable and to price elevated accumulation risks—global cyber insurance premiums grew 24% in 2024, underscoring opportunity and exposure.

- 38% rise in state-linked cyber incidents (2023)

- Global cyber premiums +24% (2024)

- Need to update war/terror definitions to avoid coverage disputes

Regulatory churn, Brexit costs and cyber risk reshape Ryan Specialty’s pricing & capital

Political volatility since 2024 raised state regulator turnover (22 states) and variable non‑admitted rules, impacting Ryan Specialty’s 8% wholesale premium growth and compliance workload; UK/EU revenue exposure ($1.2bn FY2024) faces Brexit divergence and geopolitical spillovers (5–8% cross‑border cost rise); federal backstop changes (TRIPRA, cyber models $50–100bn) and 21% tax rate shifts drive pricing, capital and reinsurance strategy.

| Metric | Value |

|---|---|

| States with regulator turnover | 22 |

| Wholesale premium growth Q1 2025 | +8% |

| Ryan Group revenue UK/EU FY2024 | $1.2bn |

| Cross‑border cost rise | 5–8% |

| Cyber modeled loss range | $50–100bn |

| Federal corporate tax rate | 21% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Ryan Specialty Group, with data-driven trends, region- and industry-specific examples, and forward-looking insights to identify risks, opportunities, and strategic responses for executives, investors, and advisors.

A concise, visually segmented PESTLE summary for Ryan Specialty Group that simplifies external risk and market-position insights for quick inclusion in presentations, team alignment, or client reports.

Economic factors

Interest Rate Volatility and Investment Income

Stabilization of U.S. policy rates through 2025 (Fed funds range ~5.25–5.50% as of Dec 2025) boosts Ryan Specialty’s fiduciary investment income from held-premium portfolios, improving yield on short-duration bonds and cash; higher rates also raise acquisition financing costs—12-month BAA corporate yields averaged ~5.6% in 2025—so debt management and interest-rate hedging are pivotal to preserve ROE and support M&A cadence.

Hard vs Soft Market Cycles in Excess and Surplus

The specialty insurance market is highly cyclical; hard markets push pricing up and Ryan Specialty benefits when risks are hard to place, contributing to its 2024-25 revenue resilience with brokered premium growth near industry-beating mid-teens levels. As select lines showed softening by late 2025—rate deceleration of roughly 5–8% in some commercial casualty segments—Ryan must lean on technical underwriting expertise and carrier relationships to protect margins. Strategic adjustments in volume mix and commission structures, including shifting toward higher-fee lines and performance-based commissions, are required to sustain EBITDA margins around the firm’s target range.

Inflationary Pressures on Claims Costs

Economic and social inflation raised US insured claim severity ~7–9% in 2023–2024, pushing Ryan Specialty to raise premiums and employ specialized underwriting to cover higher material, labor and settlement costs.

Sustained inflation—CPI ~3.4% in 2024 and construction cost indices up 6–8%—forces continuous recalibration of risk appetite and pricing models to protect broker margins and carrier profitability.

Global Economic Growth and Commercial Activity

The 2024 global economy expanded ~3.0% after 2023 weakness, supporting higher commercial activity and rising demand for business insurance across sectors.

Growth in tech, renewables and logistics increases demand for complex specialty coverage, aligning with Ryan Specialty’s risk solutions portfolio.

A GDP slowdown (e.g., IMF downside of 2.6% base case) could cut new business formation and premium growth, so continuous economic monitoring is critical.

- Global GDP ~3.0% (2024 est)

- Rising sectoral demand: tech, renewables, logistics

- GDP slowdown risks lower premiums/new firms

Consolidation and M&A Capital Availability

The availability of capital for M&A drives Ryan Specialty’s inorganic growth; global PE dry powder exceeded $2.2 trillion in 2024, supporting deal activity in specialty insurance. Favorable credit conditions enabled Ryan to acquire niche agencies and talent to broaden capabilities, while a tightening—US bank lending standards rose in 2024—could slow acquisitions. In that case, Ryan would emphasize organic growth and efficiency improvements.

- 2024 global PE dry powder: $2.2T+

- US bank lending standards: tightened in 2024

- Inorganic growth risk if credit tightens

- Shift to organic growth and efficiencies as mitigation

Higher rates lift yields and costs; insurers recalibrate amid rising claims and M&A firepower

Higher policy rates (Fed funds ~5.25–5.50% by Dec 2025) lift investment yields but raise acquisition financing costs; insured claim severity rose ~7–9% (2023–24) with CPI ~3.4% in 2024, forcing pricing and underwriting recalibration. Global GDP ~3.0% (2024) and sectoral demand (tech, renewables, logistics) support premium growth, while PE dry powder ~$2.2T (2024) underpins M&A; credit tightening risks slowing inorganic growth.

| Metric | Value |

|---|---|

| Fed funds (Dec 2025) | 5.25–5.50% |

| CPI (2024) | 3.4% |

| Claim severity rise | 7–9% |

| Global GDP (2024) | ~3.0% |

| PE dry powder (2024) | ~$2.2T |

Preview Before You Purchase

Ryan Specialty Group PESTLE Analysis

The preview shown here is the exact Ryan Specialty Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use.

The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying, with no placeholders or surprises.

This final document is professionally structured and ready for analysis, presentation, or integration into your due diligence materials.