S-Oil Boston Consulting Group Matrix

Actionable Strategy Starts Here

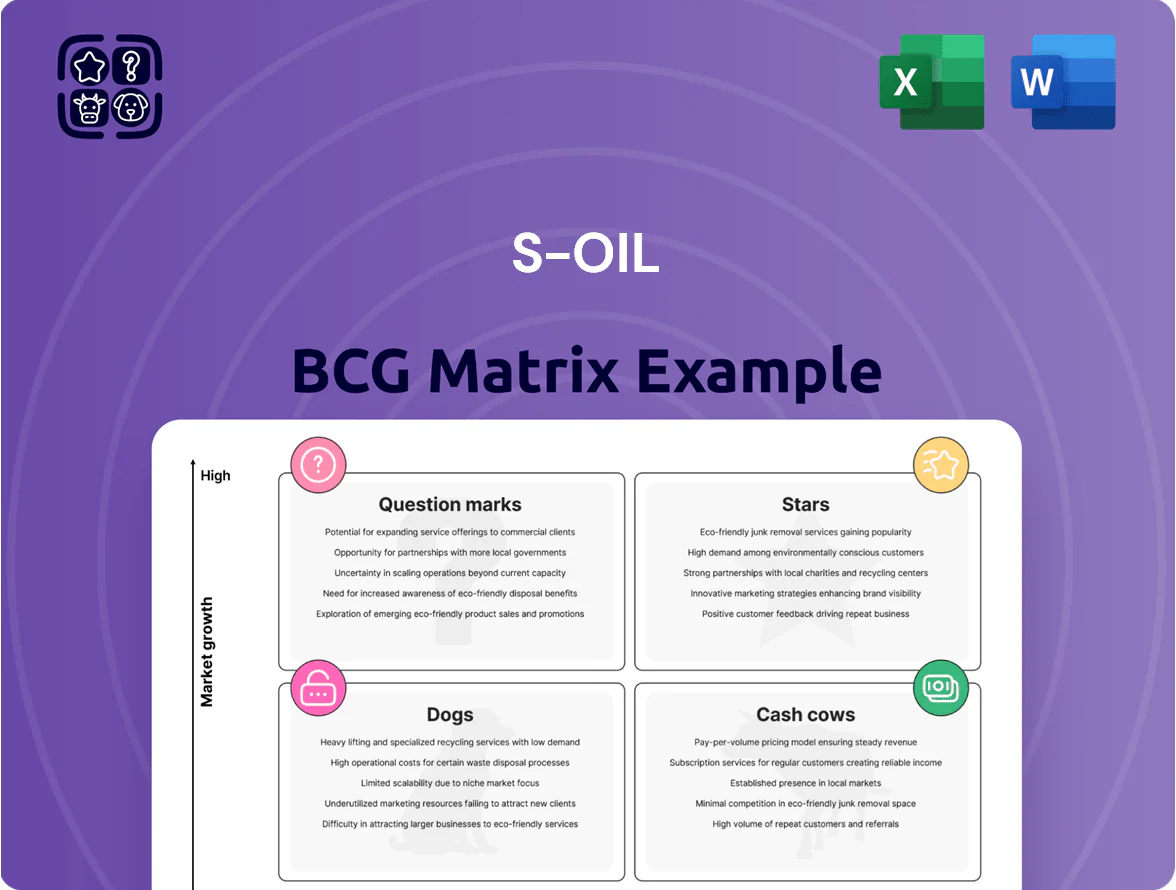

S-Oil’s BCG Matrix snapshot highlights its refining and petrochemical segments’ market positions—identifying which units drive cash flow, which require investment, and which may be phased out as market dynamics shift. This preview outlines key quadrant trends and strategic implications for margin management and capital allocation. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that turn analysis into actionable strategy.

Stars

Shaheen Project Petrochemicals

The Shaheen Project Petrochemicals is a Star: a steam cracker investment (~$3.8bn capex) reaching operational maturity by end-2025, adding ~1.2 million tonnes/year of ethylene and propylene capacity to S-Oil’s portfolio.

By converting crude to high-value feedstocks at scale, the unit boosts S-Oil’s integrated margin; management projects incremental EBITDA of ~$350–450m/year post-stabilization (2026–27).

With global ethylene demand forecast +3.2% CAGR to 2030 and tight propylene markets, Shaheen strengthens S-Oil’s market share and growth prospects in advanced materials.

Sustainable Aviation Fuel

With ICAO CORSIA tightening and regional mandates by late 2025, S-Oil scaled SAF (sustainable aviation fuel) via co-processing to ~120 kbpd renewable feedstock capacity by Q4 2025, driving 45% year-on-year segment volume growth as APAC airlines pursue 2030 carbon targets.

Group III Lubricant Base Oils

S-Oil leads global production of premium Group III lubricant base oils, supplying >1.2 million tonnes/year and capturing roughly 8% of the 2025 global market for hydrotreated base oils (IEA + industry reports). These oils power modern high-efficiency engines and meet stricter fuel-economy and emissions rules, driving synthetic adoption at ~6–7% CAGR (2020–25). The segment posts high operating cash flow—estimated EBITDA margin ~22% in 2024—yet stays a star because synthetic lubricant penetration is still expanding worldwide.

High-Octane Export Gasoline

S-Oil has become a star in export high-octane gasoline, holding an estimated 28% market share in premium gasoline exports to Southeast Asia and Oceania as of 2025, driven by rising vehicle ownership (+6.5% CAGR 2020–25) and stricter fuel standards.

The company is boosting refining complexity (RRR upgrade completed 2024) and logistics spend, investing about $450m 2023–25 to secure offtake and cut delivery times, preserving margins in fast-growing markets.

- 28% premium gasoline export share (2025)

- 6.5% vehicle ownership CAGR 2020–25

- $450m logistics/refining investment 2023–25

- RRR upgrade finished 2024, higher diesel/gasoline yields

Paraxylene Production Capacity

As a major global producer of paraxylene, S-Oil holds a ~6% global market share (2024) in PX feedstock for polyester and PET bottles, anchoring its Star position in the BCG matrix.

Demand growth in developing markets—projected PX consumption CAGR ~3.5% to 2030—keeps the segment high-growth and cash-generative.

Integrated upstream aromatics and refinery-to-PTA operations lift PX yield to ~42% and cut energy intensity 12% vs peers, sustaining leadership.

- ~6% global PX market share (2024)

- PX demand CAGR ~3.5% to 2030

- PX yield ~42%; energy intensity −12% vs peers

Shaheen boost: $3.8bn cracker adds 1.2Mtpa, lifts EBITDA $350–450m; SAF & base oils growth

Shaheen steam cracker (≈$3.8bn, online end-2025) adds ~1.2 Mtpa C2/C3; +$350–450m incremental EBITDA (2026–27); ethylene demand +3.2% CAGR to 2030; propylene tightness. SAF co-processing ~120 kbpd renewables by Q4 2025, 45% YoY volume growth. Group III base oils >1.2 Mtpa, ~8% global share (2025), EBITDA margin ~22% (2024). Premium gasoline export share 28% (2025); PX ~6% global (2024), yield ~42%.

| Metric | Value |

|---|---|

| Shaheen capex | $3.8bn |

| Shaheen capacity | 1.2 Mtpa |

| Shaheen EBITDA | $350–450m |

| Ethylene CAGR | +3.2% to 2030 |

| SAF capacity | ~120 kbpd (Q4 2025) |

| Base oils volume | >1.2 Mtpa |

| Base oils margin | ~22% (2024) |

| Premium gasoline export share | 28% (2025) |

| PX global share | ~6% (2024) |

| PX yield | ~42% |

What is included in the product

Comprehensive BCG analysis of S-Oil’s product units with quadrant strategies, investment recommendations, and trend-driven risks and opportunities.

One-page BCG matrix placing S-Oil business units in clear quadrants for quick strategic decisions and stakeholder briefings

Cash Cows

Domestic Retail Fuel Network

S-Oil’s Domestic Retail Fuel Network spans about 1,300 branded stations in South Korea (2025), anchoring a mature market with ~0–1% annual volume growth but stable demand.

That network generated roughly KRW 1.1 trillion in operating cash flow in 2024, a predictable source used to service ~KRW 4.5 trillion corporate debt and pay dividends.

These cash flows fund the company’s energy transition—S-Oil earmarked KRW 400 billion for low-carbon projects in its 2025–2027 plan—making the retail arm a classic cash cow.

Ultra-Low Sulfur Diesel

Ultra-low sulfur diesel (ULSD) is a cornerstone of S-Oil’s refining portfolio, accounting for roughly 30% of refinery throughput and supporting a domestic diesel market share near 28% as of 2025.

Demand from heavy transport and industry stayed steady: South Korea’s diesel consumption fell only 1.2% YoY in 2024, reflecting slow electrification in freight and construction.

ULSD requires minimal capex—maintenance and desulfurization upgrades—letting S-Oil extract ~USD 110/ton refining margin in 2024 and redeploy cash to petrochemical growth and low‑carbon projects.

Standard Refining Operations

S-Oil’s core crude distillation units processed about 440 kbpd (thousand barrels per day) in 2025, running at >95% utilization and delivering high-margin feedstocks for petrochemicals and fuel blending.

Refining is a mature, structurally declining sector, yet S-Oil’s Nelson Complexity Index ~11 keeps EBITDA margins resilient—roughly $7–9/boe in 2025—even during weak crack spreads.

These operations generated roughly KRW 1.2 trillion free cash flow in 2025, supplying the liquidity that funds S-Oil’s downstream investments and dividend policy.

Bunkering and Marine Fuels

S-Oil supplies compliant marine fuels from Ulsan and Dangjin, South Korea, serving global shipping with steady volumes; bunkering revenue contributed about 12% of consolidated sales in 2024 and shows low annual growth (~1–2% CAGR 2022–24).

High market share in Northeast Asian bunkering and long-term contracts with international lines secure margins; operating cash flow from marine fuels stayed resilient, funding capex and dividends in 2024 without major promotional spend.

- Low growth, high share: ~1–2% CAGR (2022–24)

- Revenue contribution: ~12% of 2024 sales

- Stable cash flow: supports capex/dividends in 2024

- Minimal promo spend due to long-term contracts

Industrial Fuel Oil Supply

S-Oil’s Industrial Fuel Oil Supply is a Cash Cow: it supplies heavy fuel oils and heating fuels to major South Korean industrial complexes, sustaining market leadership through long-term contracts and refinery-linked logistics.

Growth is low as industry shifts to natural gas and electricity; demand fell ~6% from 2019–2024 while segment revenue stayed high—roughly KRW 1.1 trillion in 2024—with EBITDA margins above 22% due to scale and fixed-cost leverage.

- Market leader with integrated refinery-to-distribution assets

- 2024 revenue ≈ KRW 1.1 trillion; EBITDA margin >22%

- Demand down ~6% (2019–2024) due to fuel switching

- Low growth, high cash generation for reinvestment

S-Oil: High‑margin, cash‑flowing assets fund debt, dividends & low‑carbon spend

S-Oil’s cash cows—1,300 domestic stations, ULSD refining, marine bunkers, industrial fuel—generated ~KRW 2.3–2.4 trillion free/operating cash flow in 2024–25, funding KRW 4.5 trillion debt service, KRW 400 billion 2025–27 low‑carbon spend, and dividends while showing low growth (0–2% CAGR) and high margins (EBITDA >22% for industrial fuel; ~$7–9/boe refinery).

| Asset | 2024–25 KPI |

|---|---|

| Retail stations | 1,300 stations; OCF ~KRW 1.1T |

| Refining (ULSD) | 440 kbpd; margin $7–9/boe; ~30% throughput |

| Marine bunkers | ~12% sales; 1–2% CAGR |

| Industrial fuel | Revenue ~KRW 1.1T; EBITDA >22% |

Delivered as Shown

S-Oil BCG Matrix

The file you're previewing is the exact S-Oil BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document tailored for strategic clarity and professional use.

This preview mirrors the final deliverable: a market-informed BCG Matrix complete with positioning, growth metrics, and actionable recommendations, sent directly to your inbox upon purchase.

What you see is immediately downloadable and editable after buying, suitable for presentations, internal strategy sessions, or client deliverables without further revisions.

Professionally designed by strategy analysts, the report is ready to integrate into your planning or investor materials—no surprises, only a one-time purchase for full access.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

S-Oil’s BCG Matrix snapshot highlights its refining and petrochemical segments’ market positions—identifying which units drive cash flow, which require investment, and which may be phased out as market dynamics shift. This preview outlines key quadrant trends and strategic implications for margin management and capital allocation. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed recommendations, and downloadable Word and Excel files that turn analysis into actionable strategy.

Stars

Shaheen Project Petrochemicals

The Shaheen Project Petrochemicals is a Star: a steam cracker investment (~$3.8bn capex) reaching operational maturity by end-2025, adding ~1.2 million tonnes/year of ethylene and propylene capacity to S-Oil’s portfolio.

By converting crude to high-value feedstocks at scale, the unit boosts S-Oil’s integrated margin; management projects incremental EBITDA of ~$350–450m/year post-stabilization (2026–27).

With global ethylene demand forecast +3.2% CAGR to 2030 and tight propylene markets, Shaheen strengthens S-Oil’s market share and growth prospects in advanced materials.

Sustainable Aviation Fuel

With ICAO CORSIA tightening and regional mandates by late 2025, S-Oil scaled SAF (sustainable aviation fuel) via co-processing to ~120 kbpd renewable feedstock capacity by Q4 2025, driving 45% year-on-year segment volume growth as APAC airlines pursue 2030 carbon targets.

Group III Lubricant Base Oils

S-Oil leads global production of premium Group III lubricant base oils, supplying >1.2 million tonnes/year and capturing roughly 8% of the 2025 global market for hydrotreated base oils (IEA + industry reports). These oils power modern high-efficiency engines and meet stricter fuel-economy and emissions rules, driving synthetic adoption at ~6–7% CAGR (2020–25). The segment posts high operating cash flow—estimated EBITDA margin ~22% in 2024—yet stays a star because synthetic lubricant penetration is still expanding worldwide.

High-Octane Export Gasoline

S-Oil has become a star in export high-octane gasoline, holding an estimated 28% market share in premium gasoline exports to Southeast Asia and Oceania as of 2025, driven by rising vehicle ownership (+6.5% CAGR 2020–25) and stricter fuel standards.

The company is boosting refining complexity (RRR upgrade completed 2024) and logistics spend, investing about $450m 2023–25 to secure offtake and cut delivery times, preserving margins in fast-growing markets.

- 28% premium gasoline export share (2025)

- 6.5% vehicle ownership CAGR 2020–25

- $450m logistics/refining investment 2023–25

- RRR upgrade finished 2024, higher diesel/gasoline yields

Paraxylene Production Capacity

As a major global producer of paraxylene, S-Oil holds a ~6% global market share (2024) in PX feedstock for polyester and PET bottles, anchoring its Star position in the BCG matrix.

Demand growth in developing markets—projected PX consumption CAGR ~3.5% to 2030—keeps the segment high-growth and cash-generative.

Integrated upstream aromatics and refinery-to-PTA operations lift PX yield to ~42% and cut energy intensity 12% vs peers, sustaining leadership.

- ~6% global PX market share (2024)

- PX demand CAGR ~3.5% to 2030

- PX yield ~42%; energy intensity −12% vs peers

Shaheen boost: $3.8bn cracker adds 1.2Mtpa, lifts EBITDA $350–450m; SAF & base oils growth

Shaheen steam cracker (≈$3.8bn, online end-2025) adds ~1.2 Mtpa C2/C3; +$350–450m incremental EBITDA (2026–27); ethylene demand +3.2% CAGR to 2030; propylene tightness. SAF co-processing ~120 kbpd renewables by Q4 2025, 45% YoY volume growth. Group III base oils >1.2 Mtpa, ~8% global share (2025), EBITDA margin ~22% (2024). Premium gasoline export share 28% (2025); PX ~6% global (2024), yield ~42%.

| Metric | Value |

|---|---|

| Shaheen capex | $3.8bn |

| Shaheen capacity | 1.2 Mtpa |

| Shaheen EBITDA | $350–450m |

| Ethylene CAGR | +3.2% to 2030 |

| SAF capacity | ~120 kbpd (Q4 2025) |

| Base oils volume | >1.2 Mtpa |

| Base oils margin | ~22% (2024) |

| Premium gasoline export share | 28% (2025) |

| PX global share | ~6% (2024) |

| PX yield | ~42% |

What is included in the product

Comprehensive BCG analysis of S-Oil’s product units with quadrant strategies, investment recommendations, and trend-driven risks and opportunities.

One-page BCG matrix placing S-Oil business units in clear quadrants for quick strategic decisions and stakeholder briefings

Cash Cows

Domestic Retail Fuel Network

S-Oil’s Domestic Retail Fuel Network spans about 1,300 branded stations in South Korea (2025), anchoring a mature market with ~0–1% annual volume growth but stable demand.

That network generated roughly KRW 1.1 trillion in operating cash flow in 2024, a predictable source used to service ~KRW 4.5 trillion corporate debt and pay dividends.

These cash flows fund the company’s energy transition—S-Oil earmarked KRW 400 billion for low-carbon projects in its 2025–2027 plan—making the retail arm a classic cash cow.

Ultra-Low Sulfur Diesel

Ultra-low sulfur diesel (ULSD) is a cornerstone of S-Oil’s refining portfolio, accounting for roughly 30% of refinery throughput and supporting a domestic diesel market share near 28% as of 2025.

Demand from heavy transport and industry stayed steady: South Korea’s diesel consumption fell only 1.2% YoY in 2024, reflecting slow electrification in freight and construction.

ULSD requires minimal capex—maintenance and desulfurization upgrades—letting S-Oil extract ~USD 110/ton refining margin in 2024 and redeploy cash to petrochemical growth and low‑carbon projects.

Standard Refining Operations

S-Oil’s core crude distillation units processed about 440 kbpd (thousand barrels per day) in 2025, running at >95% utilization and delivering high-margin feedstocks for petrochemicals and fuel blending.

Refining is a mature, structurally declining sector, yet S-Oil’s Nelson Complexity Index ~11 keeps EBITDA margins resilient—roughly $7–9/boe in 2025—even during weak crack spreads.

These operations generated roughly KRW 1.2 trillion free cash flow in 2025, supplying the liquidity that funds S-Oil’s downstream investments and dividend policy.

Bunkering and Marine Fuels

S-Oil supplies compliant marine fuels from Ulsan and Dangjin, South Korea, serving global shipping with steady volumes; bunkering revenue contributed about 12% of consolidated sales in 2024 and shows low annual growth (~1–2% CAGR 2022–24).

High market share in Northeast Asian bunkering and long-term contracts with international lines secure margins; operating cash flow from marine fuels stayed resilient, funding capex and dividends in 2024 without major promotional spend.

- Low growth, high share: ~1–2% CAGR (2022–24)

- Revenue contribution: ~12% of 2024 sales

- Stable cash flow: supports capex/dividends in 2024

- Minimal promo spend due to long-term contracts

Industrial Fuel Oil Supply

S-Oil’s Industrial Fuel Oil Supply is a Cash Cow: it supplies heavy fuel oils and heating fuels to major South Korean industrial complexes, sustaining market leadership through long-term contracts and refinery-linked logistics.

Growth is low as industry shifts to natural gas and electricity; demand fell ~6% from 2019–2024 while segment revenue stayed high—roughly KRW 1.1 trillion in 2024—with EBITDA margins above 22% due to scale and fixed-cost leverage.

- Market leader with integrated refinery-to-distribution assets

- 2024 revenue ≈ KRW 1.1 trillion; EBITDA margin >22%

- Demand down ~6% (2019–2024) due to fuel switching

- Low growth, high cash generation for reinvestment

S-Oil: High‑margin, cash‑flowing assets fund debt, dividends & low‑carbon spend

S-Oil’s cash cows—1,300 domestic stations, ULSD refining, marine bunkers, industrial fuel—generated ~KRW 2.3–2.4 trillion free/operating cash flow in 2024–25, funding KRW 4.5 trillion debt service, KRW 400 billion 2025–27 low‑carbon spend, and dividends while showing low growth (0–2% CAGR) and high margins (EBITDA >22% for industrial fuel; ~$7–9/boe refinery).

| Asset | 2024–25 KPI |

|---|---|

| Retail stations | 1,300 stations; OCF ~KRW 1.1T |

| Refining (ULSD) | 440 kbpd; margin $7–9/boe; ~30% throughput |

| Marine bunkers | ~12% sales; 1–2% CAGR |

| Industrial fuel | Revenue ~KRW 1.1T; EBITDA >22% |

Delivered as Shown

S-Oil BCG Matrix

The file you're previewing is the exact S-Oil BCG Matrix report you'll receive after purchase—no watermarks, no placeholders, just the fully formatted, analysis-ready document tailored for strategic clarity and professional use.

This preview mirrors the final deliverable: a market-informed BCG Matrix complete with positioning, growth metrics, and actionable recommendations, sent directly to your inbox upon purchase.

What you see is immediately downloadable and editable after buying, suitable for presentations, internal strategy sessions, or client deliverables without further revisions.

Professionally designed by strategy analysts, the report is ready to integrate into your planning or investor materials—no surprises, only a one-time purchase for full access.