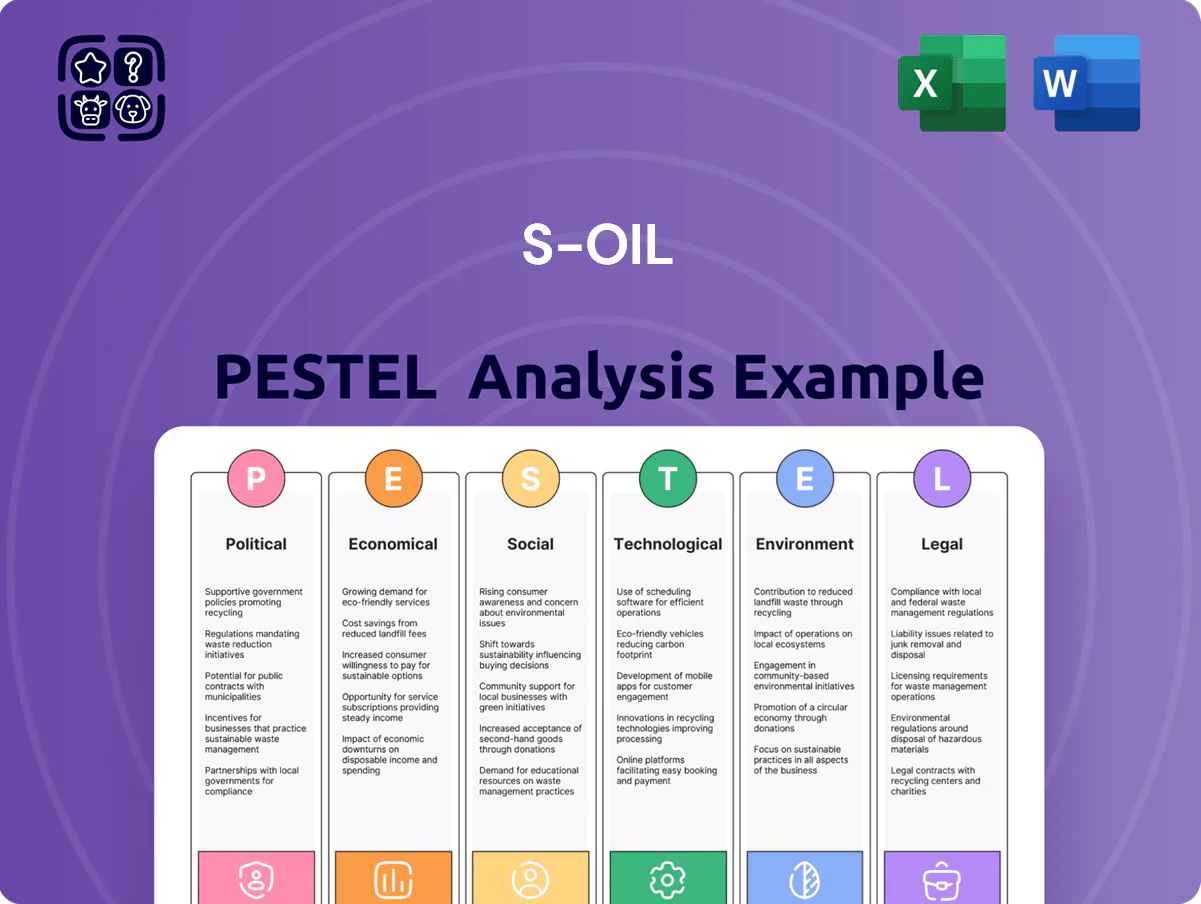

S-Oil PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Navigate S-Oil’s external landscape with our concise PESTLE snapshot—highlighting regulatory shifts, oil-price sensitivity, technological upgrades in refining, social expectations on sustainability, and geopolitical risks affecting supply chains; perfect for investors and strategists needing quick, actionable context. Purchase the full PESTLE for a detailed, ready-to-use report that powers smarter decisions and strategic planning.

Political factors

Geopolitical instability in the Middle East

S-Oil depends on Saudi crude via Aramco, sourcing roughly 45–55% of feedstock from Saudi volumes; late-2025 escalations in the Middle East risk supply disruptions and drove tanker war-risk premiums up ~30%, raising transport costs and insurance outlays. Monitoring Strait of Hormuz transit and diplomatic ties is essential as even short closure scenarios can cut shipments and affect refining margins and working capital.

South Korean energy security policy

The South Korean government prioritizes stable energy supply for its $1.7 trillion export-driven economy, making S-Oil (2024 revenue KRW 42.3 trillion) critical to national reserves and domestic price stability; regulators have pressured refiners to limit retail fuel increases during 2022–24 inflation spikes, affecting margins. State-led diversification—targeting 20% renewables and 30% LNG growth by 2030—shapes S-Oil’s long-term capital allocation toward low-carbon projects.

Trade relations and export tariffs

S-Oil exports roughly 40% of its refined products and petrochemicals to China and Southeast Asia, making it highly exposed to changing trade agreements and protectionist tariffs; a 1% tariff rise in key markets could erode margins by an estimated $30–50 million annually based on 2024 export volumes. Regional trade bloc shifts or China–ROK tensions may reduce competitiveness versus Middle Eastern or Chinese refiners. Management must actively engage in diplomacy and hedging strategies to protect market share in economies growing at 4–6% annually.

Saudi Aramco strategic influence

As majority shareholder, Saudi Aramco secures S-Oil with steady crude volumes—Aramco supplied around 60–70% of S-Oil feedstock in 2024—while aligning S-Oil strategy with Saudi Vision 2030, driving downstream investment and tech transfer.

This political-economic tie offers a dependable upstream link but exposes S-Oil to Saudi geopolitical priorities and oil policy shifts, affecting margins and export routes.

- Aramco stake: majority (post-2023 acquisition)

- Feedstock share: ~60–70% in 2024

- Impact: enhanced refining competitiveness; geopolitical exposure

Government subsidies for green energy

The South Korean government pledged 73.4 trillion KRW for green transition through 2025, with targeted subsidies for hydrogen and EV charging; S-Oil’s downstream renewables and hydrogen project economics depend on continuation of such fiscal support.

Changes in ruling party priorities can reverse incentives quickly, raising regulatory risk that could delay S-Oil’s planned investments and affect NPV of new-energy projects.

- 73.4 trillion KRW green fund to 2025

- S-Oil capex exposure tied to subsidy continuity

- Political shifts increase regulatory uncertainty

S-Oil: Aramco Reliance, Export Risks & Tariff Threats Could Slash Margins

S-Oil relies on Aramco for ~60–70% of feedstock (2024), making it vulnerable to Middle East disruptions that raised tanker war-risk premiums ~30% in late-2025; South Korea’s 2024 revenue KRW 42.3T and export dependence tie S-Oil to state energy security policies and 73.4T KRW green funds to 2025, while ~40% export exposure to China/SE Asia risks tariff/geo tensions that could cut margins by $30–50M per 1% tariff rise.

| Metric | Value (latest) |

|---|---|

| Aramco feedstock share | 60–70% (2024) |

| 2024 revenue | KRW 42.3 trillion |

| Export share | ~40% |

| Tankers war-risk premium change | ~+30% (late-2025) |

| Green transition fund | KRW 73.4 trillion to 2025 |

| Margin impact per 1% tariff | $30–50 million/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect S-Oil across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region- and industry-specific data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for S-Oil that clarifies external risks and opportunities for quick insertion into presentations, team briefings, or client reports.

Economic factors

Global crude oil price volatility

Fluctuations in Brent (averaging about 85–95 USD/bbl in 2024) and Dubai crude directly swing S-Oil’s inventory valuation and refining margins, with a ~USD 10–15/bbl crude spread often shifting quarterly EBIT by meaningful tens of billions KRW. As a pure-play refiner, S-Oil’s profitability is highly sensitive to the crack spread between feedstock and product prices. Economic cooling in 2025 prompted management to report tightened margin guidance and pursue ~5–8% cost-efficiency targets and higher refinery utilization to protect margins.

Exchange rate fluctuations

S-Oil buys crude in US dollars while selling much of its refined products in Korean won, exposing margins to FX swings; a 10% won depreciation versus the dollar would raise import costs proportionally and, given S-Oil’s 2024 net foreign-currency debt of about $1.1 billion, would materially increase KRW-denominated debt servicing pressure. A weak won also compresses local margins and raised S-Oil’s 2024 crude procurement cost by roughly 8–12% year-over-year. Robust hedging—forward contracts, FX swaps and natural hedges—remains essential to stabilize earnings and protect cash flow.

Shaheen Project capital expenditure

The Shaheen petrochemical project, with capex reported around KRW 3.5 trillion (≈ USD 2.6 billion) by S-Oil in 2024, materially increases leverage and shapes the company’s debt maturity profile; syndicated loans and bonds raised to fund construction pushed net debt/EBITDA toward higher single digits in 2024. The facility targets a rise in high-value petrochemicals output—projected to add several hundred thousand tons annually—shifting revenue mix away from fuel refining. Timely commissioning is critical: delays would strain cash flow and postpone diversification benefits tied to higher-margin petrochemical sales.

Interest rate environment

- Bank of Korea rate 3.5% (Dec 2025); 10-yr yields ~4.2%

- S-Oil net debt/EBITDA ~1.8x (2024)

- Higher rates raise CAPEX hurdle, delaying low-carbon projects

Regional demand for petrochemicals

China and India accounted for roughly 45% of global paraxylene and benzene demand in 2024, with China GDP growth ~5.2% and India ~7.4%, underpinning S-Oil's feedstock exports and refined-chemical margins.

Weakness in global manufacturing (PMIs dipping below 50 in parts of 2024) risks oversupply, pushing petrochemical spot prices down ~8–12% YoY; S-Oil adjusts runs and export mix accordingly.

S-Oil tracks GDP, PMI, and regional inventory data to time production cuts or boosts, aiming to protect margins and control inventory days.

- China GDP 2024 ~5.2%, India ~7.4%

- China+India ~45% share of paraxylene/benzene demand

- Petrochemical spot prices fell ~8–12% YoY in 2024

- S-Oil uses GDP, PMI, inventory metrics to optimize runs

Macro & energy mix: Brent $85–95, 3.5% BOK, net leverage ~1.8x, capex $2.6bn

Brent at 85–95 USD/bbl (2024), BOK rate 3.5% (Dec 2025), 10y ~4.2%, net debt/EBITDA ~1.8x (2024), Shaheen capex ≈ KRW 3.5tn (~USD 2.6bn), FX exposure with $1.1bn net FC debt (2024), China GDP 5.2% & India 7.4% (2024), petrochemical spot prices -8–12% YoY (2024).

| Metric | Value |

|---|---|

| Brent (2024) | 85–95 USD/bbl |

| BOK rate | 3.5% |

| Net debt/EBITDA | ~1.8x |

Preview Before You Purchase

S-Oil PESTLE Analysis

The preview shown here is the exact S-Oil PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Navigate S-Oil’s external landscape with our concise PESTLE snapshot—highlighting regulatory shifts, oil-price sensitivity, technological upgrades in refining, social expectations on sustainability, and geopolitical risks affecting supply chains; perfect for investors and strategists needing quick, actionable context. Purchase the full PESTLE for a detailed, ready-to-use report that powers smarter decisions and strategic planning.

Political factors

Geopolitical instability in the Middle East

S-Oil depends on Saudi crude via Aramco, sourcing roughly 45–55% of feedstock from Saudi volumes; late-2025 escalations in the Middle East risk supply disruptions and drove tanker war-risk premiums up ~30%, raising transport costs and insurance outlays. Monitoring Strait of Hormuz transit and diplomatic ties is essential as even short closure scenarios can cut shipments and affect refining margins and working capital.

South Korean energy security policy

The South Korean government prioritizes stable energy supply for its $1.7 trillion export-driven economy, making S-Oil (2024 revenue KRW 42.3 trillion) critical to national reserves and domestic price stability; regulators have pressured refiners to limit retail fuel increases during 2022–24 inflation spikes, affecting margins. State-led diversification—targeting 20% renewables and 30% LNG growth by 2030—shapes S-Oil’s long-term capital allocation toward low-carbon projects.

Trade relations and export tariffs

S-Oil exports roughly 40% of its refined products and petrochemicals to China and Southeast Asia, making it highly exposed to changing trade agreements and protectionist tariffs; a 1% tariff rise in key markets could erode margins by an estimated $30–50 million annually based on 2024 export volumes. Regional trade bloc shifts or China–ROK tensions may reduce competitiveness versus Middle Eastern or Chinese refiners. Management must actively engage in diplomacy and hedging strategies to protect market share in economies growing at 4–6% annually.

Saudi Aramco strategic influence

As majority shareholder, Saudi Aramco secures S-Oil with steady crude volumes—Aramco supplied around 60–70% of S-Oil feedstock in 2024—while aligning S-Oil strategy with Saudi Vision 2030, driving downstream investment and tech transfer.

This political-economic tie offers a dependable upstream link but exposes S-Oil to Saudi geopolitical priorities and oil policy shifts, affecting margins and export routes.

- Aramco stake: majority (post-2023 acquisition)

- Feedstock share: ~60–70% in 2024

- Impact: enhanced refining competitiveness; geopolitical exposure

Government subsidies for green energy

The South Korean government pledged 73.4 trillion KRW for green transition through 2025, with targeted subsidies for hydrogen and EV charging; S-Oil’s downstream renewables and hydrogen project economics depend on continuation of such fiscal support.

Changes in ruling party priorities can reverse incentives quickly, raising regulatory risk that could delay S-Oil’s planned investments and affect NPV of new-energy projects.

- 73.4 trillion KRW green fund to 2025

- S-Oil capex exposure tied to subsidy continuity

- Political shifts increase regulatory uncertainty

S-Oil: Aramco Reliance, Export Risks & Tariff Threats Could Slash Margins

S-Oil relies on Aramco for ~60–70% of feedstock (2024), making it vulnerable to Middle East disruptions that raised tanker war-risk premiums ~30% in late-2025; South Korea’s 2024 revenue KRW 42.3T and export dependence tie S-Oil to state energy security policies and 73.4T KRW green funds to 2025, while ~40% export exposure to China/SE Asia risks tariff/geo tensions that could cut margins by $30–50M per 1% tariff rise.

| Metric | Value (latest) |

|---|---|

| Aramco feedstock share | 60–70% (2024) |

| 2024 revenue | KRW 42.3 trillion |

| Export share | ~40% |

| Tankers war-risk premium change | ~+30% (late-2025) |

| Green transition fund | KRW 73.4 trillion to 2025 |

| Margin impact per 1% tariff | $30–50 million/yr |

What is included in the product

Explores how external macro-environmental factors uniquely affect S-Oil across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—using region- and industry-specific data and trends to identify risks and opportunities.

A concise, visually segmented PESTLE summary for S-Oil that clarifies external risks and opportunities for quick insertion into presentations, team briefings, or client reports.

Economic factors

Global crude oil price volatility

Fluctuations in Brent (averaging about 85–95 USD/bbl in 2024) and Dubai crude directly swing S-Oil’s inventory valuation and refining margins, with a ~USD 10–15/bbl crude spread often shifting quarterly EBIT by meaningful tens of billions KRW. As a pure-play refiner, S-Oil’s profitability is highly sensitive to the crack spread between feedstock and product prices. Economic cooling in 2025 prompted management to report tightened margin guidance and pursue ~5–8% cost-efficiency targets and higher refinery utilization to protect margins.

Exchange rate fluctuations

S-Oil buys crude in US dollars while selling much of its refined products in Korean won, exposing margins to FX swings; a 10% won depreciation versus the dollar would raise import costs proportionally and, given S-Oil’s 2024 net foreign-currency debt of about $1.1 billion, would materially increase KRW-denominated debt servicing pressure. A weak won also compresses local margins and raised S-Oil’s 2024 crude procurement cost by roughly 8–12% year-over-year. Robust hedging—forward contracts, FX swaps and natural hedges—remains essential to stabilize earnings and protect cash flow.

Shaheen Project capital expenditure

The Shaheen petrochemical project, with capex reported around KRW 3.5 trillion (≈ USD 2.6 billion) by S-Oil in 2024, materially increases leverage and shapes the company’s debt maturity profile; syndicated loans and bonds raised to fund construction pushed net debt/EBITDA toward higher single digits in 2024. The facility targets a rise in high-value petrochemicals output—projected to add several hundred thousand tons annually—shifting revenue mix away from fuel refining. Timely commissioning is critical: delays would strain cash flow and postpone diversification benefits tied to higher-margin petrochemical sales.

Interest rate environment

- Bank of Korea rate 3.5% (Dec 2025); 10-yr yields ~4.2%

- S-Oil net debt/EBITDA ~1.8x (2024)

- Higher rates raise CAPEX hurdle, delaying low-carbon projects

Regional demand for petrochemicals

China and India accounted for roughly 45% of global paraxylene and benzene demand in 2024, with China GDP growth ~5.2% and India ~7.4%, underpinning S-Oil's feedstock exports and refined-chemical margins.

Weakness in global manufacturing (PMIs dipping below 50 in parts of 2024) risks oversupply, pushing petrochemical spot prices down ~8–12% YoY; S-Oil adjusts runs and export mix accordingly.

S-Oil tracks GDP, PMI, and regional inventory data to time production cuts or boosts, aiming to protect margins and control inventory days.

- China GDP 2024 ~5.2%, India ~7.4%

- China+India ~45% share of paraxylene/benzene demand

- Petrochemical spot prices fell ~8–12% YoY in 2024

- S-Oil uses GDP, PMI, inventory metrics to optimize runs

Macro & energy mix: Brent $85–95, 3.5% BOK, net leverage ~1.8x, capex $2.6bn

Brent at 85–95 USD/bbl (2024), BOK rate 3.5% (Dec 2025), 10y ~4.2%, net debt/EBITDA ~1.8x (2024), Shaheen capex ≈ KRW 3.5tn (~USD 2.6bn), FX exposure with $1.1bn net FC debt (2024), China GDP 5.2% & India 7.4% (2024), petrochemical spot prices -8–12% YoY (2024).

| Metric | Value |

|---|---|

| Brent (2024) | 85–95 USD/bbl |

| BOK rate | 3.5% |

| Net debt/EBITDA | ~1.8x |

Preview Before You Purchase

S-Oil PESTLE Analysis

The preview shown here is the exact S-Oil PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic or investment decisions.