Sabanci Holding Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

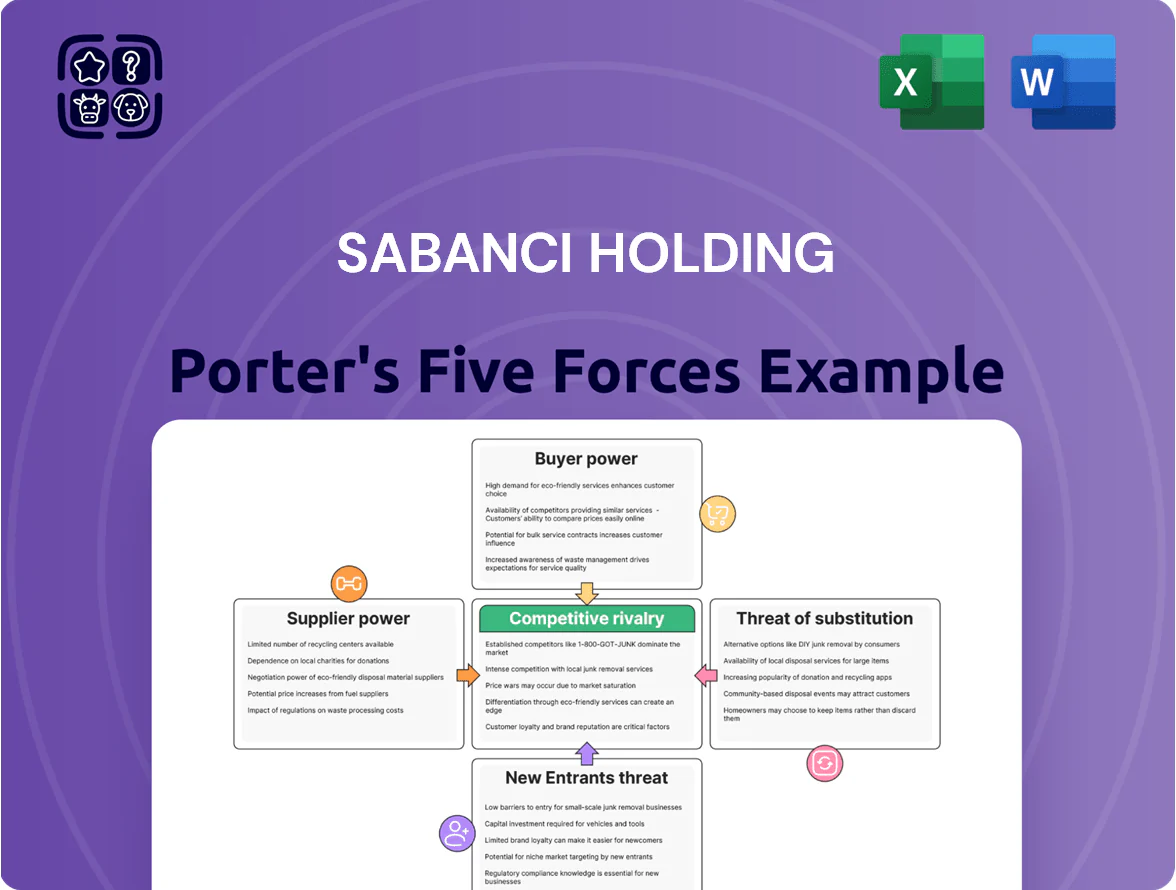

Sabanci Holding faces mixed competitive pressures: strong buyer demands in retail and energy, moderate supplier leverage in industrial units, and rising rivalry from regional conglomerates and renewables entrants threatening margins and growth paths—yet diversified assets and strategic partnerships provide resilience.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sabanci Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of energy inputs

Sabanci's energy arm depends on global natural gas markets and specialized renewables parts; in 2025 Turkey imported ~44 bcm of gas, keeping commodity exposure high.

By late 2025, tech providers for wind/solar and battery storage gained leverage—top OEMs control key components, pushing supplier power to moderate-high.

Sabanci's scale secures volume discounts (single-digit % procurement savings), but few high-tech suppliers for smart grids sustain supplier bargaining strength.

Raw material dependency in industrials

Suppliers wield notable power for Sabanci's industrials: Kordsa and Brisa depend on specialty polymers and high-grade steel, markets that saw a 12–18% price volatility in 2023–2024 due to supply-chain disruptions and capacity shifts. Quality affects tire and reinforcement performance, so Sabanci secures long-term contracts and diversified sourcing across Turkey, Brazil, and South Korea, lowering spot exposure to under 20% of purchases.

Technological infrastructure providers

For Akbank and Teknosa, dependence on global cloud and AI suppliers (AWS, Microsoft, Google) gives suppliers strong bargaining power due to high switching costs and certified ecosystems; McKinsey estimates 60–70% of banks’ tech budgets go to cloud/AI services, raising vendor leverage. Sabanci reduces this risk by boosting in-house R&D—SabanciDx and 1,200+ local tech hires—and reallocating ~€40m in 2024 to internal platforms to cut external spend.

Labor market for specialized talent

The demand for high-skilled labor in data science, renewable-energy engineering, and fintech rose ~28% in Turkey and 33% in Europe by 2025, lifting wages and benefits and raising suppliers’ bargaining power.

Sabanci leverages a strong corporate brand and 12+ graduate programs to steady hiring, but faces fierce competition from global consultancies and startups for top-tier experts.

- 28% demand rise Turkey 2025

- 33% demand rise Europe 2025

- 12+ graduate programs at Sabanci

- Higher wages and flexible work drive turnover

Impact of currency and import costs

Because Sabanci imports inputs, Turkish Lira volatility raises supplier leverage; in 2023 TL fell ~45% vs USD, pushing suppliers to price in hard currency or shorten terms.

Suppliers often demand USD/EUR invoicing or cash/30-day terms to hedge; this raises working capital needs for firms without hedges.

Sabanci’s net cash/credit access—moody-rated investment-grade and access to ~$2.5bn in committed facilities in 2024—lets it absorb FX-driven cost spikes better than smaller peers.

- 2023 TL -45% vs USD

- Suppliers prefer USD/EUR or <30-day terms

- Sabanci ~\$2.5bn committed facilities (2024)

Suppliers wield strong leverage over Sabanci despite scale and €40m tech buffer

Suppliers hold moderate-high power for Sabanci: energy imports (Turkey ~44 bcm gas 2025), top renewables OEMs and cloud providers (AWS/Microsoft/Google) concentrate supply, and TL volatility (‑45% vs USD in 2023) raises USD invoicing pressure; Sabanci's scale, ~\$2.5bn committed facilities (2024) and in-house tech spend (~€40m 2024) partially offsets risk.

| Metric | Value |

|---|---|

| Turkey gas imports 2025 | ~44 bcm |

| TL vs USD 2023 | -45% |

| Committed facilities 2024 | $2.5bn |

| In-house tech spend 2024 | €40m |

What is included in the product

Tailored exclusively for Sabanci Holding, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Sabancı Holding—quickly gauge competitive pressures and prioritize strategic moves to relieve pain points across conglomerate sectors.

Customers Bargaining Power

Retail consumer price sensitivity

In retail segments like CarrefourSA and Teknosa, customers have high bargaining power due to low switching costs and near-perfect price transparency; by end‑2025 price‑comparison apps and e‑marketplaces increased reported price sensitivity by ~18% vs 2022 per Turkish e‑commerce analytics. Sabanci counters with enhanced loyalty schemes—CarrefourSA Club upsell rates rose 12% in 2024—and a push into private‑label lines, which now account for about 9% of grocery sales, to retain customers.

Financial services switching costs

While traditional bank switching has friction, digital-only banks cut barriers—Turkey saw 25% growth in digital banking users in 2024, raising Akbank customer leverage to demand seamless apps and higher rates.

Customers expect instant onboarding and competitive yields, so price and UX sensitivity rise; 48% of Turkish retail customers say they would switch for better digital service (2024 BKM survey).

Akbank counters with a broad ecosystem—cards, payments, wealth and insurance—driving higher wallet share and making exit costs tangible; its digital active user base reached 14.2 million in 2024, lowering churn risk.

Industrial B2B contract negotiations

Energy market liberalization

Energy market liberalization in Turkey lets large industrial buyers pick suppliers by price and sustainability, raising their bargaining power and pressuring Enerjisa to cut costs and certify green power; in 2024 over 60% of industrial consumption could switch suppliers under new tariffs.

Sabanci counters by diversifying generation (solar, wind, natural gas) and selling energy-management services and guarantees of origin, with Enerjisa reporting a 2024 B2B contract growth of ~18% and 12% of generation tied to renewables.

- Industrial buyer choice boosts price/sustainability leverage

- 2024: ~60% industrial switching potential; 18% B2B contract growth

- Sabanci: diversified mix, energy-management services, green certificates

- Result: focus on cost efficiency and renewables to retain clients

Digital transparency and information access

Digital transparency in 2025 gives Turkish retail and institutional buyers realtime access to pricing, provenance, and ESG scores; 68% of global investors used ESG data in 2024 decisions and Turkish searches for supplier sustainability rose 42% year-over-year, raising customer bargaining power across Sabanci’s units.

Sabanci’s public ESG targets—net-zero by 2050 for energy affiliates and 25% reduction in Scope 1–2 emissions by 2027—help retain price-sensitive customers who now prefer verified low-impact products, reducing churn and softening raw-price bargaining.

Clear governance disclosures lower perceived supplier risk for corporate clients, enabling Sabanci to negotiate longer contracts and premium pricing in segments where verified sustainability gives competitive advantage.

- 68% of investors used ESG data in 2024

- Turkish sustainability searches +42% YoY

- Net-zero by 2050; 25% emissions cut target by 2027

Customers Gain Power: Price Sensitivity, Digital Growth & Big B2B Shifts Reshape Sabanci

Customers hold high bargaining power across Sabanci: retail price transparency raised sensitivity ~18% vs 2022 (2025 analytics); Akbank faces 25% digital‑user growth (2024) and 14.2m digital actives; industrial buyers place >$50m orders, trimming margins 200–400bps; Enerjisa sees ~60% industrial switching potential (2024) while B2B contracts grew ~18% in 2024.

| Area | Metric | 2024–25 |

|---|---|---|

| Retail | Price sensitivity ↑ | +18% |

| Banking | Digital users | +25% / 14.2m |

| Industry | Order size / margin hit | >$50m / 200–400bps |

| Energy | Switching potential | ~60% / B2B +18% |

Preview the Actual Deliverable

Sabanci Holding Porter's Five Forces Analysis

This preview shows the exact Sabanci Holding Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full version you’ll get—fully formatted, ready for download and immediate use the moment you buy.

No mockups or samples: this is the final, professionally written deliverable you’ll be able to download instantly after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Sabanci Holding faces mixed competitive pressures: strong buyer demands in retail and energy, moderate supplier leverage in industrial units, and rising rivalry from regional conglomerates and renewables entrants threatening margins and growth paths—yet diversified assets and strategic partnerships provide resilience.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sabanci Holding’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of energy inputs

Sabanci's energy arm depends on global natural gas markets and specialized renewables parts; in 2025 Turkey imported ~44 bcm of gas, keeping commodity exposure high.

By late 2025, tech providers for wind/solar and battery storage gained leverage—top OEMs control key components, pushing supplier power to moderate-high.

Sabanci's scale secures volume discounts (single-digit % procurement savings), but few high-tech suppliers for smart grids sustain supplier bargaining strength.

Raw material dependency in industrials

Suppliers wield notable power for Sabanci's industrials: Kordsa and Brisa depend on specialty polymers and high-grade steel, markets that saw a 12–18% price volatility in 2023–2024 due to supply-chain disruptions and capacity shifts. Quality affects tire and reinforcement performance, so Sabanci secures long-term contracts and diversified sourcing across Turkey, Brazil, and South Korea, lowering spot exposure to under 20% of purchases.

Technological infrastructure providers

For Akbank and Teknosa, dependence on global cloud and AI suppliers (AWS, Microsoft, Google) gives suppliers strong bargaining power due to high switching costs and certified ecosystems; McKinsey estimates 60–70% of banks’ tech budgets go to cloud/AI services, raising vendor leverage. Sabanci reduces this risk by boosting in-house R&D—SabanciDx and 1,200+ local tech hires—and reallocating ~€40m in 2024 to internal platforms to cut external spend.

Labor market for specialized talent

The demand for high-skilled labor in data science, renewable-energy engineering, and fintech rose ~28% in Turkey and 33% in Europe by 2025, lifting wages and benefits and raising suppliers’ bargaining power.

Sabanci leverages a strong corporate brand and 12+ graduate programs to steady hiring, but faces fierce competition from global consultancies and startups for top-tier experts.

- 28% demand rise Turkey 2025

- 33% demand rise Europe 2025

- 12+ graduate programs at Sabanci

- Higher wages and flexible work drive turnover

Impact of currency and import costs

Because Sabanci imports inputs, Turkish Lira volatility raises supplier leverage; in 2023 TL fell ~45% vs USD, pushing suppliers to price in hard currency or shorten terms.

Suppliers often demand USD/EUR invoicing or cash/30-day terms to hedge; this raises working capital needs for firms without hedges.

Sabanci’s net cash/credit access—moody-rated investment-grade and access to ~$2.5bn in committed facilities in 2024—lets it absorb FX-driven cost spikes better than smaller peers.

- 2023 TL -45% vs USD

- Suppliers prefer USD/EUR or <30-day terms

- Sabanci ~\$2.5bn committed facilities (2024)

Suppliers wield strong leverage over Sabanci despite scale and €40m tech buffer

Suppliers hold moderate-high power for Sabanci: energy imports (Turkey ~44 bcm gas 2025), top renewables OEMs and cloud providers (AWS/Microsoft/Google) concentrate supply, and TL volatility (‑45% vs USD in 2023) raises USD invoicing pressure; Sabanci's scale, ~\$2.5bn committed facilities (2024) and in-house tech spend (~€40m 2024) partially offsets risk.

| Metric | Value |

|---|---|

| Turkey gas imports 2025 | ~44 bcm |

| TL vs USD 2023 | -45% |

| Committed facilities 2024 | $2.5bn |

| In-house tech spend 2024 | €40m |

What is included in the product

Tailored exclusively for Sabanci Holding, this Porter's Five Forces overview uncovers key competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape its profitability and strategic positioning.

Concise Porter's Five Forces snapshot for Sabancı Holding—quickly gauge competitive pressures and prioritize strategic moves to relieve pain points across conglomerate sectors.

Customers Bargaining Power

Retail consumer price sensitivity

In retail segments like CarrefourSA and Teknosa, customers have high bargaining power due to low switching costs and near-perfect price transparency; by end‑2025 price‑comparison apps and e‑marketplaces increased reported price sensitivity by ~18% vs 2022 per Turkish e‑commerce analytics. Sabanci counters with enhanced loyalty schemes—CarrefourSA Club upsell rates rose 12% in 2024—and a push into private‑label lines, which now account for about 9% of grocery sales, to retain customers.

Financial services switching costs

While traditional bank switching has friction, digital-only banks cut barriers—Turkey saw 25% growth in digital banking users in 2024, raising Akbank customer leverage to demand seamless apps and higher rates.

Customers expect instant onboarding and competitive yields, so price and UX sensitivity rise; 48% of Turkish retail customers say they would switch for better digital service (2024 BKM survey).

Akbank counters with a broad ecosystem—cards, payments, wealth and insurance—driving higher wallet share and making exit costs tangible; its digital active user base reached 14.2 million in 2024, lowering churn risk.

Industrial B2B contract negotiations

Energy market liberalization

Energy market liberalization in Turkey lets large industrial buyers pick suppliers by price and sustainability, raising their bargaining power and pressuring Enerjisa to cut costs and certify green power; in 2024 over 60% of industrial consumption could switch suppliers under new tariffs.

Sabanci counters by diversifying generation (solar, wind, natural gas) and selling energy-management services and guarantees of origin, with Enerjisa reporting a 2024 B2B contract growth of ~18% and 12% of generation tied to renewables.

- Industrial buyer choice boosts price/sustainability leverage

- 2024: ~60% industrial switching potential; 18% B2B contract growth

- Sabanci: diversified mix, energy-management services, green certificates

- Result: focus on cost efficiency and renewables to retain clients

Digital transparency and information access

Digital transparency in 2025 gives Turkish retail and institutional buyers realtime access to pricing, provenance, and ESG scores; 68% of global investors used ESG data in 2024 decisions and Turkish searches for supplier sustainability rose 42% year-over-year, raising customer bargaining power across Sabanci’s units.

Sabanci’s public ESG targets—net-zero by 2050 for energy affiliates and 25% reduction in Scope 1–2 emissions by 2027—help retain price-sensitive customers who now prefer verified low-impact products, reducing churn and softening raw-price bargaining.

Clear governance disclosures lower perceived supplier risk for corporate clients, enabling Sabanci to negotiate longer contracts and premium pricing in segments where verified sustainability gives competitive advantage.

- 68% of investors used ESG data in 2024

- Turkish sustainability searches +42% YoY

- Net-zero by 2050; 25% emissions cut target by 2027

Customers Gain Power: Price Sensitivity, Digital Growth & Big B2B Shifts Reshape Sabanci

Customers hold high bargaining power across Sabanci: retail price transparency raised sensitivity ~18% vs 2022 (2025 analytics); Akbank faces 25% digital‑user growth (2024) and 14.2m digital actives; industrial buyers place >$50m orders, trimming margins 200–400bps; Enerjisa sees ~60% industrial switching potential (2024) while B2B contracts grew ~18% in 2024.

| Area | Metric | 2024–25 |

|---|---|---|

| Retail | Price sensitivity ↑ | +18% |

| Banking | Digital users | +25% / 14.2m |

| Industry | Order size / margin hit | >$50m / 200–400bps |

| Energy | Switching potential | ~60% / B2B +18% |

Preview the Actual Deliverable

Sabanci Holding Porter's Five Forces Analysis

This preview shows the exact Sabanci Holding Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders.

The document displayed here is part of the full version you’ll get—fully formatted, ready for download and immediate use the moment you buy.

No mockups or samples: this is the final, professionally written deliverable you’ll be able to download instantly after payment.