Safety Insurance Group Business Model Canvas

Safety Insurance Group: In-Depth Business Model Canvas Revealing Value & Growth

Unlock the full strategic blueprint behind Safety Insurance Group’s business model—our in-depth Business Model Canvas shows how the company creates value, secures customers, and sustains profitable growth in a competitive insurance market.

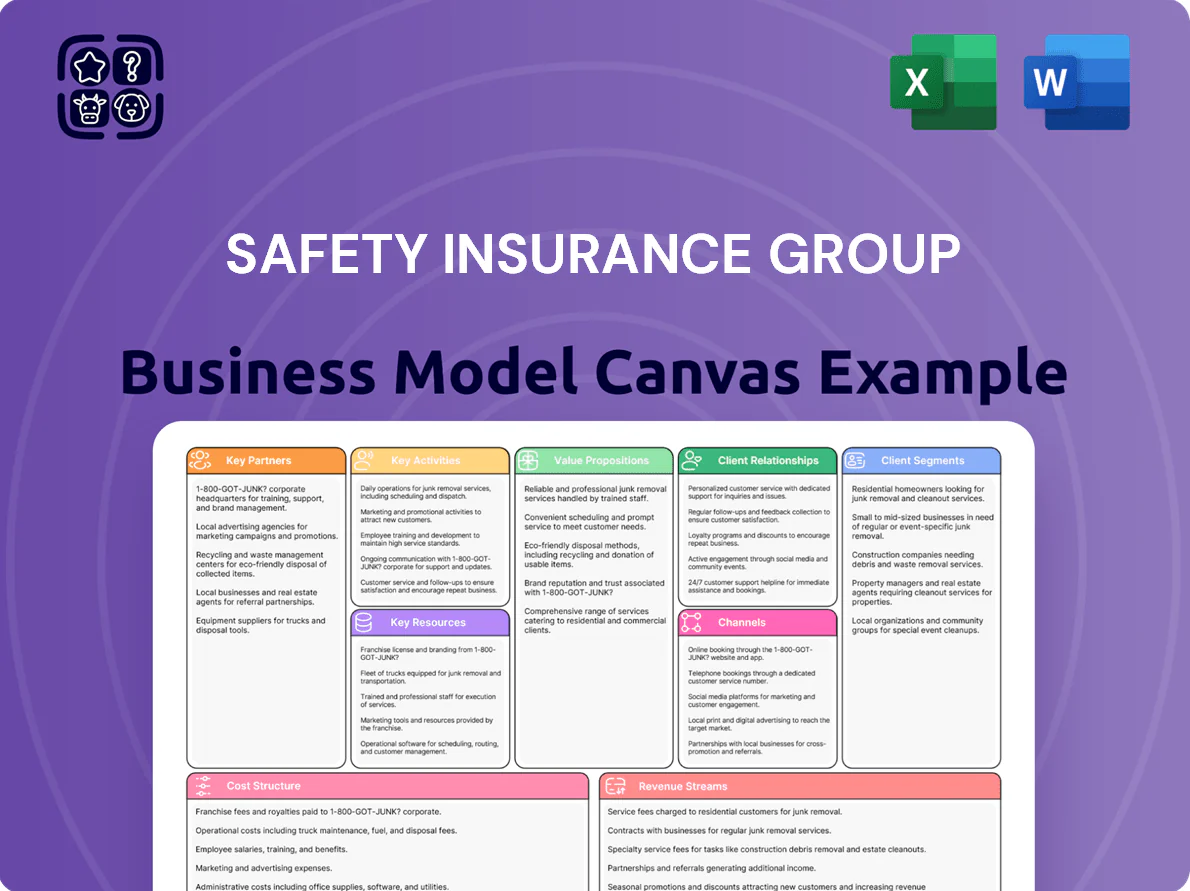

Partnerships

Independent Agency Network

Safety Insurance relies exclusively on a network of ~2,200 independent agents across New England, who serve as the primary sales and customer-acquisition channel and deliver local market expertise.

The company spends roughly $25–30 million annually on agent training, CRM and quoting technology to ensure consistent brand representation and to support its $1.3 billion 2024 written premium base.

Reinsurance Providers

Safety Insurance partners with global reinsurers to cede portions of underwriting risk, limiting balance-sheet exposure to catastrophes; in 2024 it ceded roughly 22% of property catastrophe risk, helping keep combined ratio volatility in check.

Technology and Software Vendors

Safety Insurance partners with specialist IT vendors to run its policy-management and claims systems, enabling real‑time data analysis, digital billing, and agent portals; these integrations supported a 12% IT-driven efficiency gain in 2024 and helped reduce average claim handling time by 18% year-over-year. By adopting advanced software platforms and APIs, the firm enhanced digital policyholder engagement—online self-service interactions rose to 46% of transactions in 2024.

Automotive and Property Repair Networks

Safety Insurance maintains a curated network of preferred repair shops and contractors to speed claims fulfillment, improve repair quality, and contain costs; in 2024 these networks handled roughly 62% of auto claims, reducing average cycle time by 18% versus non-preferred vendors.

- 62% of auto claims routed via preferred shops (2024)

- 18% faster repair cycle time

- Lower average claim cost per repair—company reports ~7% savings

State Regulatory and Industry Bodies

State insurance departments in Massachusetts, New Hampshire, and Maine oversee licensing, rate filings, and solvency; Safety Insurance reported 2024 direct premiums written of $1.05B, so close regulatory coordination reduces filing delays and penalty risk.

Active membership in associations (NAIC, IIABA) keeps the firm current on model laws and regional P&C trends—New England homeowners loss ratios hit 68% in 2023—so these partnerships shape underwriting and compliance strategy.

- Coordinate filings with MA, NH, ME regulators

- Monitor NAIC model laws and IIABA guidance

- Leverage market data: $1.05B DPW (2024), 68% homeowners loss ratio (2023)

Safety Insurance: $1.3B premium, 2,200 agents, digital self-service 46%, 22% ceded

Safety Insurance depends on ~2,200 independent agents as its core sales channel and invests $25–30M annually in training and CRM to support $1.3B written premiums (2024).

It cedes ~22% of property catastrophe risk to global reinsurers, uses specialist IT vendors to cut claim handling time 18% and raise digital self-service to 46%, and routes 62% of auto repairs to preferred shops for ~7% cost savings.

| Metric | 2023–2024 |

|---|---|

| Independent agents | ~2,200 |

| Agent spend | $25–30M |

| Written premium | $1.3B (2024) |

| Cat risk ceded | ~22% |

| Digital self-service | 46% transactions |

| Auto claims via preferred | 62% |

| Claim handling time improve | −18% |

| Repair cost savings | ~7% |

What is included in the product

A concise, pre-written Business Model Canvas for Safety Insurance Group detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned to its real-world property-casualty insurance operations and suitable for presentations, investor discussions, and strategic analysis.

High-level snapshot of Safety Insurance Group’s business model with editable cells to quickly map risk-sharing, distribution channels, and underwriting economics—perfect for boardrooms, collaboration, and fast executive summaries.

Activities

Underwriting and Risk Assessment

The core activity evaluates risk profiles to set coverage and premiums; Safety Insurance used actuarial models and 2019–2024 claim trend data, pricing to target a combined ratio near 95% and ROE ~9% in 2024 to stay competitive and profitable.

Claims Management and Settlement

Efficient claims processing and settlement drive retention—Safety Insurance Group employs 450+ skilled adjusters and automated triage tools, closing 82% of claims within 30 days in 2024, which reduced loss-adjustment expense by 7.4% and boosted customer retention to 89.1%; rapid, fair payouts are a key regional differentiator for reputation-sensitive policyholders.

Product Development and Pricing

Safety Insurance refines personal and commercial products for New England using 2024 loss-cost data showing a 12% rise in severe-weather property claims and MA exposure growth of 3.5%; underwriting teams adjust policy terms to reflect shifting demographics and flood/convective risks. Actuarial models target combined ratio ~92–96% while preserving statutory loss reserves of $1.1B (2024 year-end) and pricing competitively across personal auto and small commercial lines.

Agent Support and Training

Safety Insurance, using an indirect distribution model, invests in agent support through continuous education, marketing kits, quarterly product training, and a digital issuance platform that cut average policy turnaround by 35% in 2024.

Strengthening agents drives higher-quality leads—agents produced ~78% of new personal lines premium in 2024—so ongoing tech and training sustain retention and growth.

- Quarterly trainings and webinars

- Marketing kits and co-op funds

- Digital policy issuance, 35% faster (2024)

- Agents = 78% of new personal lines premium (2024)

Investment Portfolio Management

The company manages a $12.8 billion invested portfolio (2024 year-end), funded mainly by premiums received in advance, and run by professional teams targeting steady returns via diversified fixed-income and low‑risk instruments.

Investment income—about $380 million in 2024—supports net income and cushions underwriting cycles by offsetting loss volatility.

- 2024 invested assets: $12.8B

- 2024 investment income: $380M

- Main assets: fixed income, short-term municipals, cash equivalents

Targeting 92–96% combined ratio, ~9% ROE; $12.8B assets, $380M income, $1.1B reserves

Risk evaluation, pricing to target combined ratio ~92–96% and ROE ~9% (2024); claims ops: 450+ adjusters, 82% closed ≤30 days, LAE down 7.4%, retention 89.1%; product tuning for +12% severe-weather losses, reserves $1.1B; agents drive 78% personal new premium; invested assets $12.8B, investment income $380M (2024).

| Metric | 2024 |

|---|---|

| Combined ratio target | 92–96% |

| ROE | ~9% |

| Claims ≤30 days | 82% |

| Retention | 89.1% |

| Reserves | $1.1B |

| Invested assets | $12.8B |

| Investment income | $380M |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Safety Insurance Group Business Model Canvas—not a mockup—and it mirrors the exact file you’ll receive after purchase.

Upon ordering, you’ll instantly get this same ready-to-edit document in its full form, formatted precisely as shown with all sections and content included.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Safety Insurance Group: In-Depth Business Model Canvas Revealing Value & Growth

Unlock the full strategic blueprint behind Safety Insurance Group’s business model—our in-depth Business Model Canvas shows how the company creates value, secures customers, and sustains profitable growth in a competitive insurance market.

Partnerships

Independent Agency Network

Safety Insurance relies exclusively on a network of ~2,200 independent agents across New England, who serve as the primary sales and customer-acquisition channel and deliver local market expertise.

The company spends roughly $25–30 million annually on agent training, CRM and quoting technology to ensure consistent brand representation and to support its $1.3 billion 2024 written premium base.

Reinsurance Providers

Safety Insurance partners with global reinsurers to cede portions of underwriting risk, limiting balance-sheet exposure to catastrophes; in 2024 it ceded roughly 22% of property catastrophe risk, helping keep combined ratio volatility in check.

Technology and Software Vendors

Safety Insurance partners with specialist IT vendors to run its policy-management and claims systems, enabling real‑time data analysis, digital billing, and agent portals; these integrations supported a 12% IT-driven efficiency gain in 2024 and helped reduce average claim handling time by 18% year-over-year. By adopting advanced software platforms and APIs, the firm enhanced digital policyholder engagement—online self-service interactions rose to 46% of transactions in 2024.

Automotive and Property Repair Networks

Safety Insurance maintains a curated network of preferred repair shops and contractors to speed claims fulfillment, improve repair quality, and contain costs; in 2024 these networks handled roughly 62% of auto claims, reducing average cycle time by 18% versus non-preferred vendors.

- 62% of auto claims routed via preferred shops (2024)

- 18% faster repair cycle time

- Lower average claim cost per repair—company reports ~7% savings

State Regulatory and Industry Bodies

State insurance departments in Massachusetts, New Hampshire, and Maine oversee licensing, rate filings, and solvency; Safety Insurance reported 2024 direct premiums written of $1.05B, so close regulatory coordination reduces filing delays and penalty risk.

Active membership in associations (NAIC, IIABA) keeps the firm current on model laws and regional P&C trends—New England homeowners loss ratios hit 68% in 2023—so these partnerships shape underwriting and compliance strategy.

- Coordinate filings with MA, NH, ME regulators

- Monitor NAIC model laws and IIABA guidance

- Leverage market data: $1.05B DPW (2024), 68% homeowners loss ratio (2023)

Safety Insurance: $1.3B premium, 2,200 agents, digital self-service 46%, 22% ceded

Safety Insurance depends on ~2,200 independent agents as its core sales channel and invests $25–30M annually in training and CRM to support $1.3B written premiums (2024).

It cedes ~22% of property catastrophe risk to global reinsurers, uses specialist IT vendors to cut claim handling time 18% and raise digital self-service to 46%, and routes 62% of auto repairs to preferred shops for ~7% cost savings.

| Metric | 2023–2024 |

|---|---|

| Independent agents | ~2,200 |

| Agent spend | $25–30M |

| Written premium | $1.3B (2024) |

| Cat risk ceded | ~22% |

| Digital self-service | 46% transactions |

| Auto claims via preferred | 62% |

| Claim handling time improve | −18% |

| Repair cost savings | ~7% |

What is included in the product

A concise, pre-written Business Model Canvas for Safety Insurance Group detailing its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—aligned to its real-world property-casualty insurance operations and suitable for presentations, investor discussions, and strategic analysis.

High-level snapshot of Safety Insurance Group’s business model with editable cells to quickly map risk-sharing, distribution channels, and underwriting economics—perfect for boardrooms, collaboration, and fast executive summaries.

Activities

Underwriting and Risk Assessment

The core activity evaluates risk profiles to set coverage and premiums; Safety Insurance used actuarial models and 2019–2024 claim trend data, pricing to target a combined ratio near 95% and ROE ~9% in 2024 to stay competitive and profitable.

Claims Management and Settlement

Efficient claims processing and settlement drive retention—Safety Insurance Group employs 450+ skilled adjusters and automated triage tools, closing 82% of claims within 30 days in 2024, which reduced loss-adjustment expense by 7.4% and boosted customer retention to 89.1%; rapid, fair payouts are a key regional differentiator for reputation-sensitive policyholders.

Product Development and Pricing

Safety Insurance refines personal and commercial products for New England using 2024 loss-cost data showing a 12% rise in severe-weather property claims and MA exposure growth of 3.5%; underwriting teams adjust policy terms to reflect shifting demographics and flood/convective risks. Actuarial models target combined ratio ~92–96% while preserving statutory loss reserves of $1.1B (2024 year-end) and pricing competitively across personal auto and small commercial lines.

Agent Support and Training

Safety Insurance, using an indirect distribution model, invests in agent support through continuous education, marketing kits, quarterly product training, and a digital issuance platform that cut average policy turnaround by 35% in 2024.

Strengthening agents drives higher-quality leads—agents produced ~78% of new personal lines premium in 2024—so ongoing tech and training sustain retention and growth.

- Quarterly trainings and webinars

- Marketing kits and co-op funds

- Digital policy issuance, 35% faster (2024)

- Agents = 78% of new personal lines premium (2024)

Investment Portfolio Management

The company manages a $12.8 billion invested portfolio (2024 year-end), funded mainly by premiums received in advance, and run by professional teams targeting steady returns via diversified fixed-income and low‑risk instruments.

Investment income—about $380 million in 2024—supports net income and cushions underwriting cycles by offsetting loss volatility.

- 2024 invested assets: $12.8B

- 2024 investment income: $380M

- Main assets: fixed income, short-term municipals, cash equivalents

Targeting 92–96% combined ratio, ~9% ROE; $12.8B assets, $380M income, $1.1B reserves

Risk evaluation, pricing to target combined ratio ~92–96% and ROE ~9% (2024); claims ops: 450+ adjusters, 82% closed ≤30 days, LAE down 7.4%, retention 89.1%; product tuning for +12% severe-weather losses, reserves $1.1B; agents drive 78% personal new premium; invested assets $12.8B, investment income $380M (2024).

| Metric | 2024 |

|---|---|

| Combined ratio target | 92–96% |

| ROE | ~9% |

| Claims ≤30 days | 82% |

| Retention | 89.1% |

| Reserves | $1.1B |

| Invested assets | $12.8B |

| Investment income | $380M |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the actual Safety Insurance Group Business Model Canvas—not a mockup—and it mirrors the exact file you’ll receive after purchase.

Upon ordering, you’ll instantly get this same ready-to-edit document in its full form, formatted precisely as shown with all sections and content included.