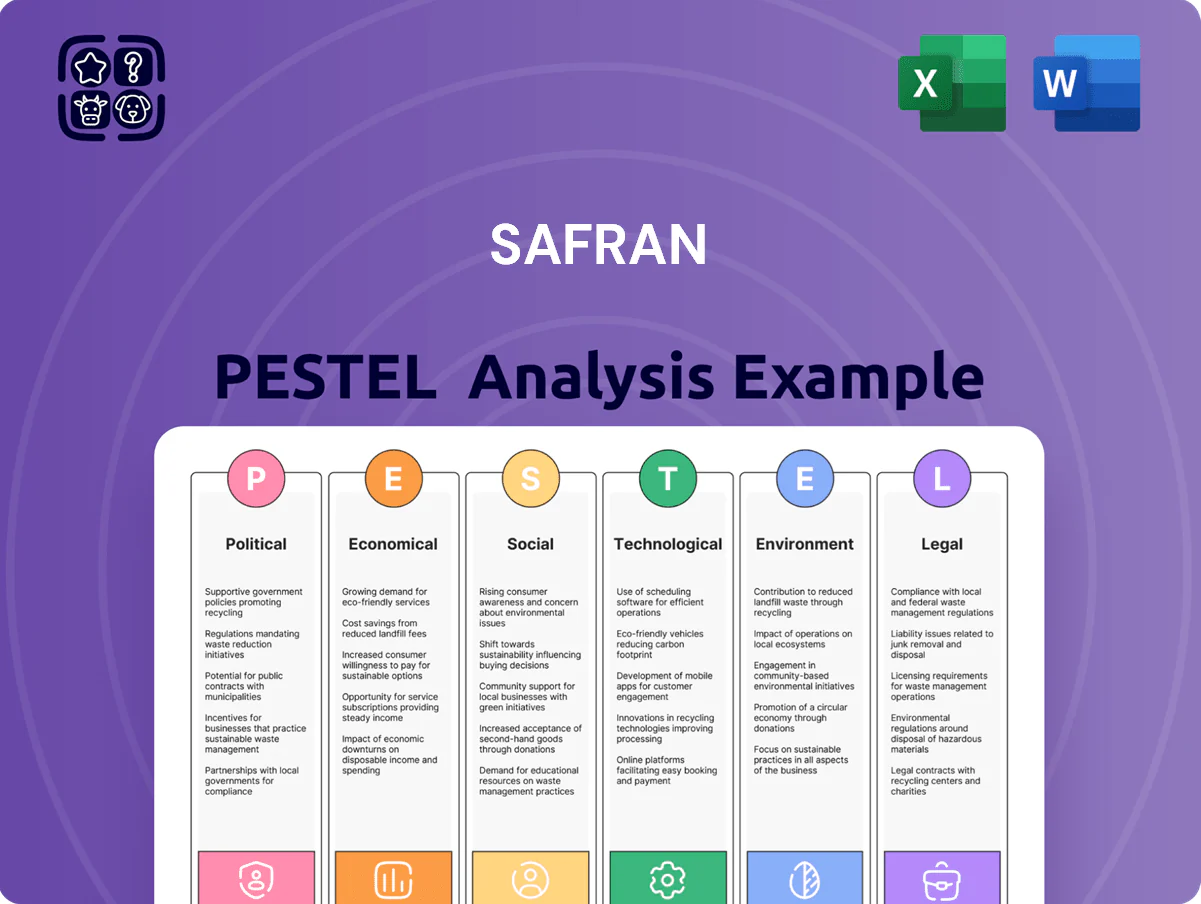

Safran PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Safran—spot political, economic, and technological forces shaping the aerospace leader and turn them into actionable advantages; purchase the full, editable report now for a complete, ready-to-use breakdown.

Political factors

Geopolitical instability and defense spending

The conflicts in Eastern Europe and the Middle East prompted EU defense spending to rise by about 24% from 2021–2024, with EU members pledging €200+ billion extra through 2025; Safran, a leading supplier of propulsion and optronics, captures value via multi-year procurement and MRO contracts.

Sovereignty and European strategic autonomy

Political pressure to reduce reliance on non-European technology has strengthened Safran's role in joint ventures like FCAS, where Safran holds key propulsion and avionics stakes in a program budgeted at roughly €100bn through 2040.

European governments prioritizing domestic supply chains boost Safran's order book—France and Germany increased defense procurement to €55bn and €46bn respectively in 2024—favoring local suppliers for national security and industrial independence.

This trend grants Safran preferential access to state-funded R&D, including multi-year grants and contracts; Safran reported €1.2bn in defense-related R&D revenues in 2024 tied to next-generation platforms.

International trade relations and export controls

Safran's global operations face stringent export controls, notably ITAR in the US and France's dual-use regulations, affecting roughly 40% of its 2025 aerospace revenues (~€12.6bn of group aerospace sales in 2024). Changes in Western trade diplomacy with emerging markets can delay engine deliveries and spare parts, risking order fulfillment in high-growth regions. Effective compliance is critical to protect market share in India and Southeast Asia, which accounted for ~15–20% of commercial aftermarket demand in 2024.

Governmental support for aerospace decarbonization

The French government and EU back green aviation with over EUR 15bn in combined grants and loans (2021-25), including France’s EUR 3.5bn Aviation du Futur envelope supporting low-emission engines and hydrogen projects.

These policies subsidize Safran’s R&D—Safran committed EUR 1.5bn+ to sustainable propulsion—reducing investment risk and accelerating commercialization timelines.

- EUR 15bn+ public funding (2021–25)

- France: EUR 3.5bn Aviation du Futur

- Safran R&D: EUR 1.5bn+ on sustainable propulsion

- De-risks large-capex hydrogen/low-emission engines

Global regulatory harmonization in aviation

Political cooperation between EASA and the FAA is critical for certifying new engine architectures; delays in mutual recognition can add millions in development costs—FAA-EASA bilateral accords reduced duplicate testing by an estimated 20% in 2023.

Safran must navigate divergent political agendas on safety and emissions—EU CO2 standards and US EPA rules differ, impacting R&D prioritization and potentially affecting 2025-2026 product timelines.

Sustained diplomatic engagement helps keep global certification streamlined, supporting faster market entry and protecting projected 2024–2026 commercial engine revenues (Safran Aircraft Engines ~€8.5bn in 2024).

- FAA–EASA cooperation cut duplicate testing ~20% (2023)

- Divergent EU/US environmental rules affect R&D and timelines

- Certification alignment supports Safran Engines revenue ~€8.5bn (2024)

Safran Poised to Gain from €200bn+ EU Defense Boost and Green Aviation Funds

Rising EU defense spend (+24% 2021–24; €200bn+ pledged to 2025) and national procurement (France €55bn, Germany €46bn in 2024) favor Safran’s defense contracts; €15bn+ green aviation funding (2021–25) and France’s €3.5bn Aviation du Futur support Safran’s €1.5bn+ sustainable R&D; export controls/ITAR affect ~40% of aerospace sales (~€12.6bn 2024), FAA–EASA cooperation cut duplicate testing ~20% (2023).

| Metric | Value |

|---|---|

| EU defense spend change 2021–24 | +24% |

| EU pledge to 2025 | €200bn+ |

| Safran defense R&D revenue (2024) | €1.2bn |

| Aerospace sales affected by export controls | ~40% (~€12.6bn) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Safran across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight risks and opportunities for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Safran’s external landscape that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary pressures and supply chain costs

Persistently high raw material costs—titanium up ~18% in 2024 vs 2022 and specialty alloys rising ~12%—compress Safran's manufacturing margins, with 2024 materials spend representing roughly 22% of COGS.

Safran employs long-term hedging and price-escalation clauses; in 2023–24 hedges covered about 60% of exposure, helping stabilize gross margin fluctuations within a 150–200 bp range.

Skilled engineering labor shortages have pushed wage-related operating expenses up ~7%–9% year-over-year, adding further inflationary pressure on Safran's OPEX.

Recovery and growth in air traffic volumes

The full recovery of global narrow-body traffic in 2024-25 propelled record demand for Safran’s CFM56 and LEAP services, with CFM family shop visits up ~18% year-over-year and aftermarket revenue rising to an estimated €7.2bn in 2024. Increased flight cycles boost high-margin spare parts and MRO revenues—LEAP-1A cycles grew ~22% YoY—while airline cashflows and load factors (global LF ~80% in 2024) remain key indicators of Safran’s long-term financial health.

Currency exchange rate volatility

As Safran incurs most costs in euros while about 45% of 2024 commercial revenue was dollar-denominated, the group is highly sensitive to EUR/USD swings; a 10% EUR depreciation could boost reported EBIT by several hundred million euros. Safran uses a multi-year hedge program covering anticipated cash flows—hedges that trimmed 2023 currency impact to roughly -€60m vs an unhedged exposure estimated >€300m. These hedging policies stabilize operating income and cash flow in volatile FX markets.

Interest rates and capital expenditure

The 2025 euro area rate at ~3.75% raises Safran’s average borrowing costs, increasing financing expense for R&D and infrastructure; Safran reported net debt/EBITDA of 1.6x in 2024, signaling disciplined leverage to protect its A2/BBB+ range ratings.

Higher rates pressure aircraft leasing demand, potentially delaying deliveries of engines amid airlines’ capex caution; global airline capex cut forecasts fell ~12% for 2024–25.

Growth in emerging aerospace markets

Economic expansion in India and other emerging aerospace markets has driven record aircraft orders—India's carriers ordered over 1,000 single-aisle jets through 2025—boosting demand for CFM LEAP engines, which powered ~45% of narrowbody deliveries in 2024.

Safran is expanding local manufacturing and MRO capacity in India and Southeast Asia to capture lower production costs and service revenues, with planned investments exceeding €400 million by 2026.

These regions now account for an estimated 20–30% of Safran's medium-term order book and a growing share of service revenue, underpinning long-term aftermarket growth.

- India/EM growth: >1,000 narrowbodies ordered through 2025

- LEAP share: ~45% of 2024 narrowbody deliveries

- Safran regional investment: >€400m planned by 2026

- Future orders/services: ~20–30% of medium-term book

Aftermarket €7.2bn; titanium +18% squeezes margins despite 60% hedges

Rising raw-materials (titanium +18% vs 2022) and wages (+7–9% YoY) squeeze margins; materials = ~22% of COGS. Hedging covered ~60% exposure in 2023–24, limiting gross-margin swing to ~150–200 bp. Aftermarket revenue ~€7.2bn (2024) with CFM shop visits +18% YoY; net debt/EBITDA 1.6x (2024) and euro area rate ~3.75% (2025).

| Metric | Value |

|---|---|

| Titanium change (2022–24) | +18% |

| Materials % of COGS (2024) | ~22% |

| Hedge coverage | ~60% |

| Aftermarket rev (2024) | €7.2bn |

| Net debt/EBITDA (2024) | 1.6x |

| Euro area rate (2025) | ~3.75% |

Full Version Awaits

Safran PESTLE Analysis

The preview shown here is the exact Safran PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Safran—spot political, economic, and technological forces shaping the aerospace leader and turn them into actionable advantages; purchase the full, editable report now for a complete, ready-to-use breakdown.

Political factors

Geopolitical instability and defense spending

The conflicts in Eastern Europe and the Middle East prompted EU defense spending to rise by about 24% from 2021–2024, with EU members pledging €200+ billion extra through 2025; Safran, a leading supplier of propulsion and optronics, captures value via multi-year procurement and MRO contracts.

Sovereignty and European strategic autonomy

Political pressure to reduce reliance on non-European technology has strengthened Safran's role in joint ventures like FCAS, where Safran holds key propulsion and avionics stakes in a program budgeted at roughly €100bn through 2040.

European governments prioritizing domestic supply chains boost Safran's order book—France and Germany increased defense procurement to €55bn and €46bn respectively in 2024—favoring local suppliers for national security and industrial independence.

This trend grants Safran preferential access to state-funded R&D, including multi-year grants and contracts; Safran reported €1.2bn in defense-related R&D revenues in 2024 tied to next-generation platforms.

International trade relations and export controls

Safran's global operations face stringent export controls, notably ITAR in the US and France's dual-use regulations, affecting roughly 40% of its 2025 aerospace revenues (~€12.6bn of group aerospace sales in 2024). Changes in Western trade diplomacy with emerging markets can delay engine deliveries and spare parts, risking order fulfillment in high-growth regions. Effective compliance is critical to protect market share in India and Southeast Asia, which accounted for ~15–20% of commercial aftermarket demand in 2024.

Governmental support for aerospace decarbonization

The French government and EU back green aviation with over EUR 15bn in combined grants and loans (2021-25), including France’s EUR 3.5bn Aviation du Futur envelope supporting low-emission engines and hydrogen projects.

These policies subsidize Safran’s R&D—Safran committed EUR 1.5bn+ to sustainable propulsion—reducing investment risk and accelerating commercialization timelines.

- EUR 15bn+ public funding (2021–25)

- France: EUR 3.5bn Aviation du Futur

- Safran R&D: EUR 1.5bn+ on sustainable propulsion

- De-risks large-capex hydrogen/low-emission engines

Global regulatory harmonization in aviation

Political cooperation between EASA and the FAA is critical for certifying new engine architectures; delays in mutual recognition can add millions in development costs—FAA-EASA bilateral accords reduced duplicate testing by an estimated 20% in 2023.

Safran must navigate divergent political agendas on safety and emissions—EU CO2 standards and US EPA rules differ, impacting R&D prioritization and potentially affecting 2025-2026 product timelines.

Sustained diplomatic engagement helps keep global certification streamlined, supporting faster market entry and protecting projected 2024–2026 commercial engine revenues (Safran Aircraft Engines ~€8.5bn in 2024).

- FAA–EASA cooperation cut duplicate testing ~20% (2023)

- Divergent EU/US environmental rules affect R&D and timelines

- Certification alignment supports Safran Engines revenue ~€8.5bn (2024)

Safran Poised to Gain from €200bn+ EU Defense Boost and Green Aviation Funds

Rising EU defense spend (+24% 2021–24; €200bn+ pledged to 2025) and national procurement (France €55bn, Germany €46bn in 2024) favor Safran’s defense contracts; €15bn+ green aviation funding (2021–25) and France’s €3.5bn Aviation du Futur support Safran’s €1.5bn+ sustainable R&D; export controls/ITAR affect ~40% of aerospace sales (~€12.6bn 2024), FAA–EASA cooperation cut duplicate testing ~20% (2023).

| Metric | Value |

|---|---|

| EU defense spend change 2021–24 | +24% |

| EU pledge to 2025 | €200bn+ |

| Safran defense R&D revenue (2024) | €1.2bn |

| Aerospace sales affected by export controls | ~40% (~€12.6bn) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Safran across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to highlight risks and opportunities for executives, consultants, and investors.

A concise, PESTLE-segmented summary of Safran’s external landscape that’s easily dropped into presentations or shared across teams to streamline risk discussions and strategic planning.

Economic factors

Inflationary pressures and supply chain costs

Persistently high raw material costs—titanium up ~18% in 2024 vs 2022 and specialty alloys rising ~12%—compress Safran's manufacturing margins, with 2024 materials spend representing roughly 22% of COGS.

Safran employs long-term hedging and price-escalation clauses; in 2023–24 hedges covered about 60% of exposure, helping stabilize gross margin fluctuations within a 150–200 bp range.

Skilled engineering labor shortages have pushed wage-related operating expenses up ~7%–9% year-over-year, adding further inflationary pressure on Safran's OPEX.

Recovery and growth in air traffic volumes

The full recovery of global narrow-body traffic in 2024-25 propelled record demand for Safran’s CFM56 and LEAP services, with CFM family shop visits up ~18% year-over-year and aftermarket revenue rising to an estimated €7.2bn in 2024. Increased flight cycles boost high-margin spare parts and MRO revenues—LEAP-1A cycles grew ~22% YoY—while airline cashflows and load factors (global LF ~80% in 2024) remain key indicators of Safran’s long-term financial health.

Currency exchange rate volatility

As Safran incurs most costs in euros while about 45% of 2024 commercial revenue was dollar-denominated, the group is highly sensitive to EUR/USD swings; a 10% EUR depreciation could boost reported EBIT by several hundred million euros. Safran uses a multi-year hedge program covering anticipated cash flows—hedges that trimmed 2023 currency impact to roughly -€60m vs an unhedged exposure estimated >€300m. These hedging policies stabilize operating income and cash flow in volatile FX markets.

Interest rates and capital expenditure

The 2025 euro area rate at ~3.75% raises Safran’s average borrowing costs, increasing financing expense for R&D and infrastructure; Safran reported net debt/EBITDA of 1.6x in 2024, signaling disciplined leverage to protect its A2/BBB+ range ratings.

Higher rates pressure aircraft leasing demand, potentially delaying deliveries of engines amid airlines’ capex caution; global airline capex cut forecasts fell ~12% for 2024–25.

Growth in emerging aerospace markets

Economic expansion in India and other emerging aerospace markets has driven record aircraft orders—India's carriers ordered over 1,000 single-aisle jets through 2025—boosting demand for CFM LEAP engines, which powered ~45% of narrowbody deliveries in 2024.

Safran is expanding local manufacturing and MRO capacity in India and Southeast Asia to capture lower production costs and service revenues, with planned investments exceeding €400 million by 2026.

These regions now account for an estimated 20–30% of Safran's medium-term order book and a growing share of service revenue, underpinning long-term aftermarket growth.

- India/EM growth: >1,000 narrowbodies ordered through 2025

- LEAP share: ~45% of 2024 narrowbody deliveries

- Safran regional investment: >€400m planned by 2026

- Future orders/services: ~20–30% of medium-term book

Aftermarket €7.2bn; titanium +18% squeezes margins despite 60% hedges

Rising raw-materials (titanium +18% vs 2022) and wages (+7–9% YoY) squeeze margins; materials = ~22% of COGS. Hedging covered ~60% exposure in 2023–24, limiting gross-margin swing to ~150–200 bp. Aftermarket revenue ~€7.2bn (2024) with CFM shop visits +18% YoY; net debt/EBITDA 1.6x (2024) and euro area rate ~3.75% (2025).

| Metric | Value |

|---|---|

| Titanium change (2022–24) | +18% |

| Materials % of COGS (2024) | ~22% |

| Hedge coverage | ~60% |

| Aftermarket rev (2024) | €7.2bn |

| Net debt/EBITDA (2024) | 1.6x |

| Euro area rate (2025) | ~3.75% |

Full Version Awaits

Safran PESTLE Analysis

The preview shown here is the exact Safran PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.