Saga Porter's Five Forces Analysis

Don't Miss the Bigger Picture

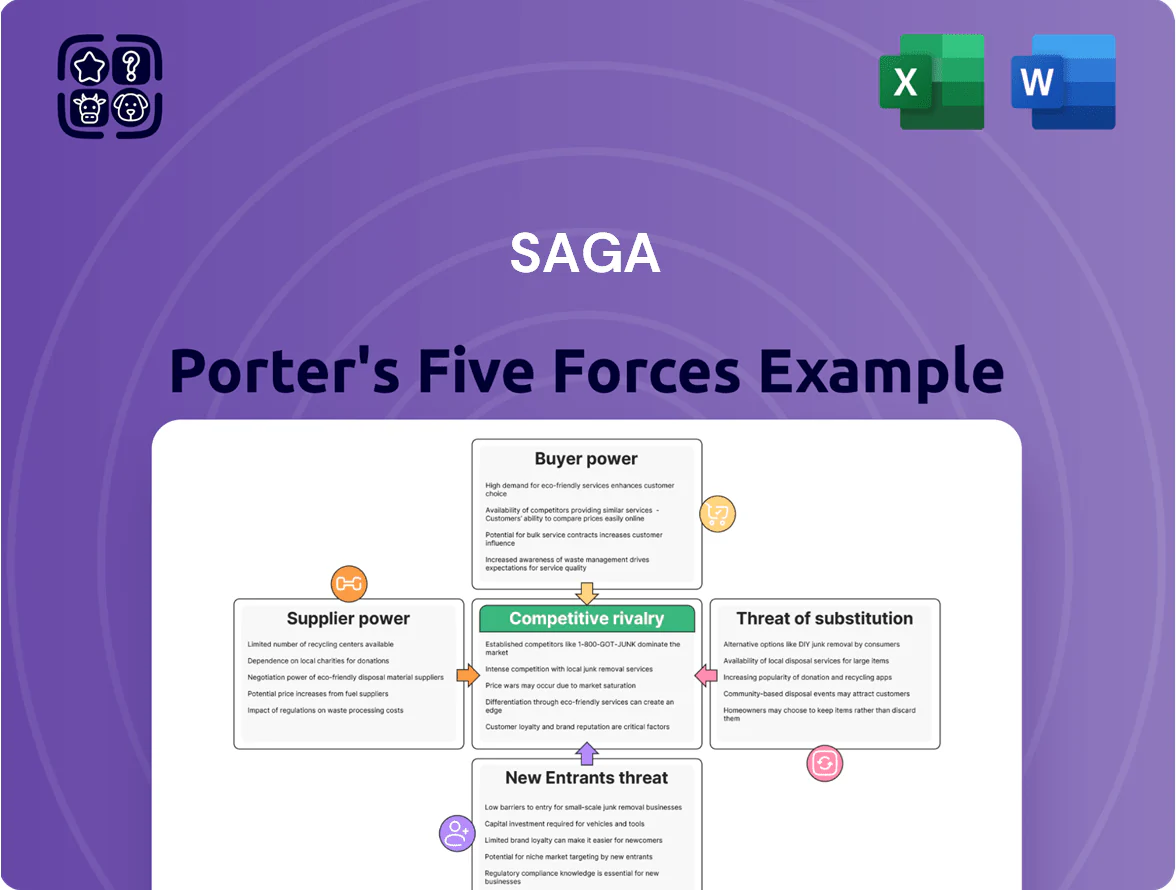

Saga faces moderate competitive pressure driven by niche customer loyalty and aging demographics, while supplier leverage and regulatory constraints shape margins; substitutes and new entrants pose variable threats depending on digital adoption and service diversification. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Saga’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Reinsurance and Underwriting Capacity

Saga’s shift to a capital-light model increases reliance on third-party underwriters and reinsurers; by late 2025 six global reinsurers control ~60% of capacity for specialised over-50s portfolios, limiting partner options.

This concentration gives suppliers leverage to raise ceded-premium rates and tighten risk-sharing, squeezing Saga’s combined ratios; a 1ppt premium cost rise could cut underwriting margin by ~10%.

Saga must keep strategic partnerships and multi-year capacity deals for motor and home lines to secure pricing and continuity; loss of a major partner could force short-term rate hikes or capacity shortfalls.

Specialized Maritime and Cruise Ship Maintenance

As a boutique cruise operator, Saga relies on a handful of high-end shipyards and specialist maritime engineers for Spirit-class maintenance, so supplier leverage is high.

Switching costs for major overhauls are large due to technical complexity, and alternative providers are scarce, raising dependency risk.

In 2025 European shipyard labor costs rose ~6–8% and dry-dock slot scarcity pushed average wait times to 6–9 months, boosting supplier pricing power.

Result: upward pressure on CapEx and longer operational downtime to manage scheduling and costs.

Technological and Digital Infrastructure Providers

The shift to data-driven pricing and personalized travel makes Saga highly dependent on major cloud and AI vendors, which in 2025 control ~70% of enterprise cloud spend and use multiyear contracts; deep integration with Saga’s proprietary customer databases raises switching costs—migration projects typically cost 15–30% of annual IT budgets and take 12–24 months—letting vendors keep firm pricing for core cybersecurity and CRM tools.

Fuel and Energy Suppliers for Travel Operations

The travel division is highly sensitive to global marine fuel pricing, with compliant low-carbon fuels still scarce; bunker fuel prices rose ~35% in 2023–2024 and low-sulfur/alternative fuel premiums averaged $60–$120/ton in 2024.

By 2025 the shift to low-carbon fuels keeps supply concentrated among a few energy conglomerates, limiting Saga’s price influence while regulatory costs rise.

Saga uses hedging to cut short-term volatility, but long-term exposure to commodity swings and supply tightness remains a persistent profit risk for cruises and tours.

- 2023–24 bunker price +35%

- Low-carbon fuel premium $60–$120/ton (2024)

- Few suppliers control market share

- Hedging reduces short-term, not structural, risk

Niche Destination and Ground Handling Partners

Saga’s curated packages depend on niche local tour operators and boutique hotels that meet older travelers’ accessibility and service standards, shrinking supplier choice despite many global chains; in 2024 boutique partners supplied ~35% of Saga’s key-destination bookings, concentrating leverage.

Specialized suppliers extract premiums in peak season—local partner rates rose ~12–18% in 2023–24—so Saga keeps a diverse portfolio to avoid any single operator gaining pricing power and to protect margins.

- 35% of key-destination bookings from boutiques (2024)

- Peak-season partner rate increase 12–18% (2023–24)

- Diversity of partners cuts supplier concentration risk

- Accessibility standards limit scalable alternatives

Saga squeezed by concentrated suppliers: reinsurers, shipyards, cloud & boutique partners

Saga faces high supplier power across insurance reinsurers (~60% capacity held by six global reinsurers by late 2025), shipyards (6–9 month dry-dock waits, 6–8% labor cost rise in 2025), cloud/AI vendors (70% enterprise cloud spend), and niche tour partners (35% of key bookings in 2024), driving higher premiums, longer downtime, and elevated CapEx and IT migration costs.

| Supplier | 2024–25 Metric | Impact |

|---|---|---|

| Reinsurers | ~60% capacity, 6 firms (late 2025) | Higher ceded rates, -10% underwriting margin per 1ppt cost |

| Shipyards | 6–9 mo wait; labor +6–8% (2025) | Longer downtime, higher CapEx |

| Cloud/AI | 70% cloud spend; migration 15–30% IT budget | High switching cost, firm pricing |

| Boutique partners | 35% bookings (2024); rates +12–18% | Peak-season premium pressure |

What is included in the product

Tailored Five Forces analysis for Saga that uncovers competitive drivers, evaluates supplier and buyer power, assesses entry barriers and substitutes, and highlights emerging threats to inform strategic decisions and investor materials.

One-sheet Five Forces summary that highlights competitive pressures and strategic levers—ideal for swift decision-making and slide-ready presentations.

Customers Bargaining Power

High Price Sensitivity in the Insurance Market

Despite Saga’s specialised insurance, price comparison sites in 2025 let buyers find cheapest premiums quickly; 74% of UK adults used comparison tools for insurance in 2024, boosting customer leverage. Older customers have become more digital—45% of over-65s compared quotes online in 2024—so Saga faces direct rate competition from generalist insurers offering lower prices. This transparency forces Saga to justify premiums via service and benefits, while easy switching at renewal (47% of UK motor renewals switched in 2023) keeps customer bargaining power high.

Demand for Specialized and High-Quality Service

The over-50s expect high-touch, often phone-based, personalized service, pressuring Saga to fund costlier staffing and call-centre capacity; UK Age UK reports 60% of 55–74s prefer phone contact (2023).

If service slips, this vocal cohort quickly defects—Saga saw NPS drop correlate with churn spikes in 2022, so maintaining a high Net Promoter Score is critical to revenue stability.

Low Switching Costs in the Travel Segment

In cruises and escorted tours, switching costs are minimal, so customers freely move between providers; 2024–25 saw 28+ luxury and niche brands targeting the silver economy, raising choice and price sensitivity.

By 2025 Saga must deepen loyalty via membership perks and exclusive offers—membership retention rates fell 3% industry-wide in 2024, so retention is critical.

Consumers now reward novel itineraries and all‑inclusive value over heritage, forcing Saga to compete on experience and bundled pricing to maintain margins.

Influence of Online Reviews and Social Proof

The collective power of customer feedback on platforms like Trustpilot (Saga Cruises rated 3.1/5 on Trustpilot as of Nov 2025) and specialist travel forums strongly affects Saga’s lead generation; negative posts on insurance claims or cruise disruptions spread quickly within the over-50s cohort and cut conversion rates.

Consumers now use reviews to hold Saga to its marketing promises, shifting bargaining power toward buyers who can dent brand equity and reduce future bookings with a single viral review.

- Trustpilot 3.1/5 (Nov 2025) — signal to prospects

- Over-50s online engagement rising; social sharing boosts negative reach

- Single viral complaint can drop short-term bookings by double digits

Increased Financial Literacy and Product Knowledge

The over-50 cohort is now markedly more financially literate: UK FCA data (2023) shows 61% of adults 55–64 actively compare financial products, and Saga’s 2024 member survey found 48% shop annually rather than auto-renew, eroding inertia.

They unbundle services—40% of 55+ buyers seek standalone travel cover or savings separate from packages—so Saga must deliver transparent, high-value products that withstand comparison shopping.

- 61% of adults 55–64 compare products (FCA 2023)

- 48% of Saga members shop annually (Saga survey 2024)

- 40% seek standalone product components (market studies 2022–24)

High customer bargaining power: comparison sites & annual shopping drive price competition

Customers hold strong bargaining power: 74% used comparison sites for insurance in 2024, 48% of Saga members shop annually (Saga survey 2024), and 47% of UK motor renewals switched in 2023, forcing Saga to compete on price, service, and bundles to retain margins.

| Metric | Value |

|---|---|

| Comparison site use (UK, 2024) | 74% |

| Saga members shopping annually (2024) | 48% |

| Motor renewal switching (2023) | 47% |

Preview the Actual Deliverable

Saga Porter's Five Forces Analysis

This preview shows the exact Saga Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy.

You’re viewing the final deliverable; once payment is complete, you’ll get instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Saga faces moderate competitive pressure driven by niche customer loyalty and aging demographics, while supplier leverage and regulatory constraints shape margins; substitutes and new entrants pose variable threats depending on digital adoption and service diversification. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Saga’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Reinsurance and Underwriting Capacity

Saga’s shift to a capital-light model increases reliance on third-party underwriters and reinsurers; by late 2025 six global reinsurers control ~60% of capacity for specialised over-50s portfolios, limiting partner options.

This concentration gives suppliers leverage to raise ceded-premium rates and tighten risk-sharing, squeezing Saga’s combined ratios; a 1ppt premium cost rise could cut underwriting margin by ~10%.

Saga must keep strategic partnerships and multi-year capacity deals for motor and home lines to secure pricing and continuity; loss of a major partner could force short-term rate hikes or capacity shortfalls.

Specialized Maritime and Cruise Ship Maintenance

As a boutique cruise operator, Saga relies on a handful of high-end shipyards and specialist maritime engineers for Spirit-class maintenance, so supplier leverage is high.

Switching costs for major overhauls are large due to technical complexity, and alternative providers are scarce, raising dependency risk.

In 2025 European shipyard labor costs rose ~6–8% and dry-dock slot scarcity pushed average wait times to 6–9 months, boosting supplier pricing power.

Result: upward pressure on CapEx and longer operational downtime to manage scheduling and costs.

Technological and Digital Infrastructure Providers

The shift to data-driven pricing and personalized travel makes Saga highly dependent on major cloud and AI vendors, which in 2025 control ~70% of enterprise cloud spend and use multiyear contracts; deep integration with Saga’s proprietary customer databases raises switching costs—migration projects typically cost 15–30% of annual IT budgets and take 12–24 months—letting vendors keep firm pricing for core cybersecurity and CRM tools.

Fuel and Energy Suppliers for Travel Operations

The travel division is highly sensitive to global marine fuel pricing, with compliant low-carbon fuels still scarce; bunker fuel prices rose ~35% in 2023–2024 and low-sulfur/alternative fuel premiums averaged $60–$120/ton in 2024.

By 2025 the shift to low-carbon fuels keeps supply concentrated among a few energy conglomerates, limiting Saga’s price influence while regulatory costs rise.

Saga uses hedging to cut short-term volatility, but long-term exposure to commodity swings and supply tightness remains a persistent profit risk for cruises and tours.

- 2023–24 bunker price +35%

- Low-carbon fuel premium $60–$120/ton (2024)

- Few suppliers control market share

- Hedging reduces short-term, not structural, risk

Niche Destination and Ground Handling Partners

Saga’s curated packages depend on niche local tour operators and boutique hotels that meet older travelers’ accessibility and service standards, shrinking supplier choice despite many global chains; in 2024 boutique partners supplied ~35% of Saga’s key-destination bookings, concentrating leverage.

Specialized suppliers extract premiums in peak season—local partner rates rose ~12–18% in 2023–24—so Saga keeps a diverse portfolio to avoid any single operator gaining pricing power and to protect margins.

- 35% of key-destination bookings from boutiques (2024)

- Peak-season partner rate increase 12–18% (2023–24)

- Diversity of partners cuts supplier concentration risk

- Accessibility standards limit scalable alternatives

Saga squeezed by concentrated suppliers: reinsurers, shipyards, cloud & boutique partners

Saga faces high supplier power across insurance reinsurers (~60% capacity held by six global reinsurers by late 2025), shipyards (6–9 month dry-dock waits, 6–8% labor cost rise in 2025), cloud/AI vendors (70% enterprise cloud spend), and niche tour partners (35% of key bookings in 2024), driving higher premiums, longer downtime, and elevated CapEx and IT migration costs.

| Supplier | 2024–25 Metric | Impact |

|---|---|---|

| Reinsurers | ~60% capacity, 6 firms (late 2025) | Higher ceded rates, -10% underwriting margin per 1ppt cost |

| Shipyards | 6–9 mo wait; labor +6–8% (2025) | Longer downtime, higher CapEx |

| Cloud/AI | 70% cloud spend; migration 15–30% IT budget | High switching cost, firm pricing |

| Boutique partners | 35% bookings (2024); rates +12–18% | Peak-season premium pressure |

What is included in the product

Tailored Five Forces analysis for Saga that uncovers competitive drivers, evaluates supplier and buyer power, assesses entry barriers and substitutes, and highlights emerging threats to inform strategic decisions and investor materials.

One-sheet Five Forces summary that highlights competitive pressures and strategic levers—ideal for swift decision-making and slide-ready presentations.

Customers Bargaining Power

High Price Sensitivity in the Insurance Market

Despite Saga’s specialised insurance, price comparison sites in 2025 let buyers find cheapest premiums quickly; 74% of UK adults used comparison tools for insurance in 2024, boosting customer leverage. Older customers have become more digital—45% of over-65s compared quotes online in 2024—so Saga faces direct rate competition from generalist insurers offering lower prices. This transparency forces Saga to justify premiums via service and benefits, while easy switching at renewal (47% of UK motor renewals switched in 2023) keeps customer bargaining power high.

Demand for Specialized and High-Quality Service

The over-50s expect high-touch, often phone-based, personalized service, pressuring Saga to fund costlier staffing and call-centre capacity; UK Age UK reports 60% of 55–74s prefer phone contact (2023).

If service slips, this vocal cohort quickly defects—Saga saw NPS drop correlate with churn spikes in 2022, so maintaining a high Net Promoter Score is critical to revenue stability.

Low Switching Costs in the Travel Segment

In cruises and escorted tours, switching costs are minimal, so customers freely move between providers; 2024–25 saw 28+ luxury and niche brands targeting the silver economy, raising choice and price sensitivity.

By 2025 Saga must deepen loyalty via membership perks and exclusive offers—membership retention rates fell 3% industry-wide in 2024, so retention is critical.

Consumers now reward novel itineraries and all‑inclusive value over heritage, forcing Saga to compete on experience and bundled pricing to maintain margins.

Influence of Online Reviews and Social Proof

The collective power of customer feedback on platforms like Trustpilot (Saga Cruises rated 3.1/5 on Trustpilot as of Nov 2025) and specialist travel forums strongly affects Saga’s lead generation; negative posts on insurance claims or cruise disruptions spread quickly within the over-50s cohort and cut conversion rates.

Consumers now use reviews to hold Saga to its marketing promises, shifting bargaining power toward buyers who can dent brand equity and reduce future bookings with a single viral review.

- Trustpilot 3.1/5 (Nov 2025) — signal to prospects

- Over-50s online engagement rising; social sharing boosts negative reach

- Single viral complaint can drop short-term bookings by double digits

Increased Financial Literacy and Product Knowledge

The over-50 cohort is now markedly more financially literate: UK FCA data (2023) shows 61% of adults 55–64 actively compare financial products, and Saga’s 2024 member survey found 48% shop annually rather than auto-renew, eroding inertia.

They unbundle services—40% of 55+ buyers seek standalone travel cover or savings separate from packages—so Saga must deliver transparent, high-value products that withstand comparison shopping.

- 61% of adults 55–64 compare products (FCA 2023)

- 48% of Saga members shop annually (Saga survey 2024)

- 40% seek standalone product components (market studies 2022–24)

High customer bargaining power: comparison sites & annual shopping drive price competition

Customers hold strong bargaining power: 74% used comparison sites for insurance in 2024, 48% of Saga members shop annually (Saga survey 2024), and 47% of UK motor renewals switched in 2023, forcing Saga to compete on price, service, and bundles to retain margins.

| Metric | Value |

|---|---|

| Comparison site use (UK, 2024) | 74% |

| Saga members shopping annually (2024) | 48% |

| Motor renewal switching (2023) | 47% |

Preview the Actual Deliverable

Saga Porter's Five Forces Analysis

This preview shows the exact Saga Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed is the full, professionally formatted analysis, ready for download and use the moment you buy.

You’re viewing the final deliverable; once payment is complete, you’ll get instant access to this identical file.