Saga PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

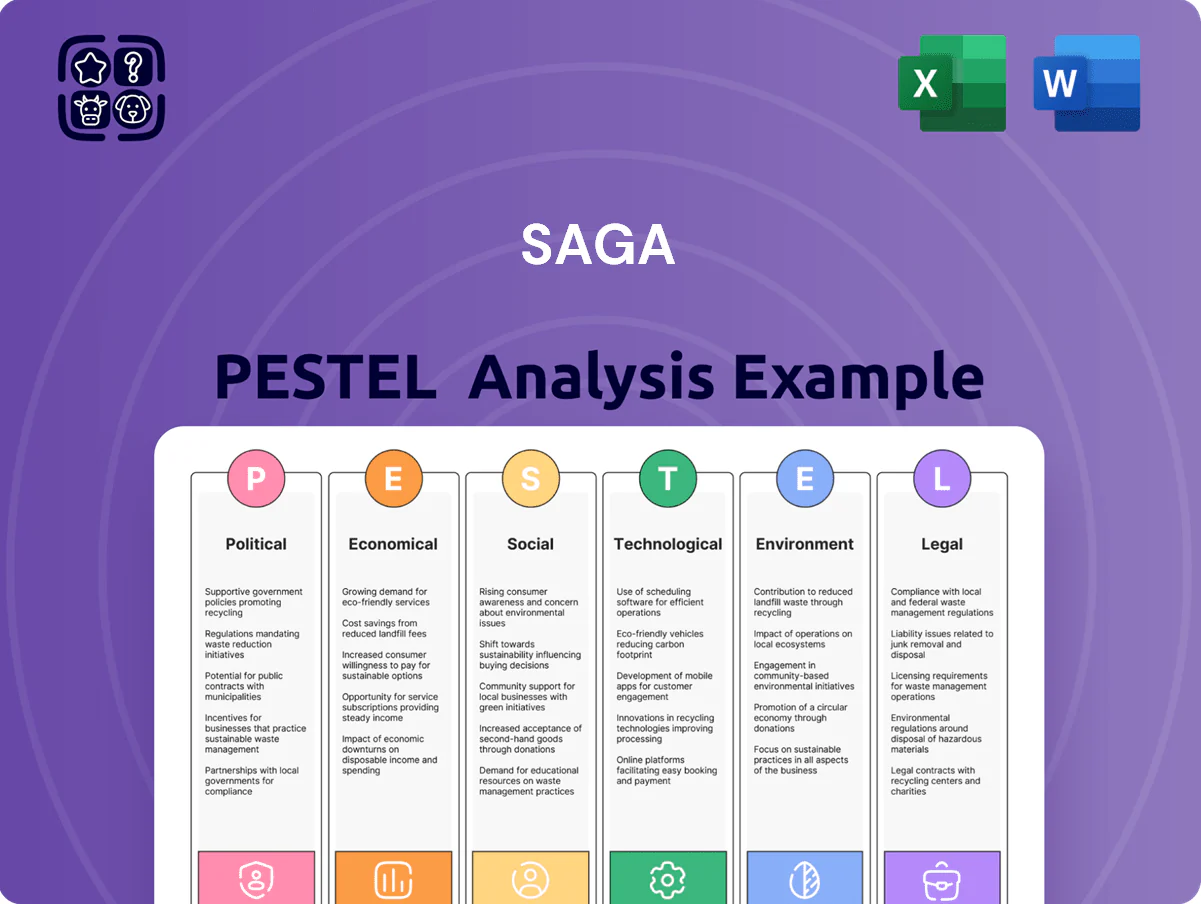

Gain a competitive edge with our PESTLE Analysis of Saga—meticulously researched to reveal political, economic, social, technological, legal, and environmental forces shaping its future; purchase the full report to access actionable insights, forecasts, and strategic recommendations tailored for investors, consultants, and executives.

Political factors

UK Political Stability and Policy

The UK political landscape after the 2024 general election—where the governing party secured a 58-seat majority—remains pivotal for Saga as shifts in social care and state pension policy affect its 50+ customer base; proposals in 2025 to increase state pension by CPI+2.5% and a projected £10bn uplift in social care funding could raise disposable incomes for retirees, supporting demand for Saga’s holidays and insurance, while sustained political stability underpins consumer confidence critical to the company’s revenue forecasts.

Post-Brexit Travel Regulations

Ongoing post-Brexit adjustments to UK-EU travel agreements continue to affect Saga’s cruise and tour operations; in 2024 UK-EU visa and transit rule changes increased pre-clearance paperwork by an estimated 12%, raising administrative costs. Political talks on visa waivers, border controls and health insurance reciprocity influence booking confidence—EU arrivals to UK tourism fell 8% in 2023-24, which could reduce Saga’s European holiday demand. Any diplomatic friction or new bureaucratic hurdles may add to operating costs and deter bookings, pressuring Saga’s FY24 European revenue mix.

International Maritime Governance

Saga’s cruise operations are shaped by evolving international maritime agreements like SOLAS and UNCLOS, with IMO 2024 safety amendments affecting vessel compliance costs; Saga reported £18m in fleet safety CAPEX in 2024.

Political tensions in the Mediterranean and Middle East forced route adjustments in 2024–25, increasing fuel and itinerary-change costs by an estimated 6–9% for regional sailings.

Multinational security efforts to protect key shipping lanes (e.g., Gulf of Aden convoys) are critical to maintaining passenger confidence and limiting insurance premiums that directly affect Saga’s luxury cruise margins.

Government Health and Social Care Reform

Government reforms to UK health and social care—such as the 2023 Health and Care Act funding changes and ongoing social care green paper proposals—disproportionately impact Saga’s 50+ customer base, where 40% of spending is health-related for households aged 55–74 (ONS 2024); increased out‑of‑pocket care costs could cut discretionary spending and pressure uptake of Saga travel and financial products.

Supportive policy moves—e.g., expanded preventative care or targeted senior wellbeing funding—could drive demand for Saga’s health services and insurance; NHS waiting‑list reductions (down 3% in 2024) and rising private care spend (£18.9bn 2023) signal both risk and opportunity for product expansion.

- Policies shifting care costs to individuals reduce discretionary income for travel/financial services.

- 40% of 55–74 household spend health‑related (ONS 2024) increases sensitivity to reforms.

- Private care spend £18.9bn (2023) and NHS waitlist down 3% (2024) create market openings for Saga health products.

Geopolitical Influence on Energy Costs

Global political instability drives oil price volatility; Brent crude averaged about 94 USD/bbl in 2024, raising bunker costs and materially increasing Saga Cruises’ fuel bill given fleet consumption patterns.

Decisions by OPEC+ and sanctions on producers can cause abrupt spikes, compressing travel division margins as fuel accounts for a significant portion of operating costs.

Saga needs active hedging—forward contracts and fuel swaps—to stabilize cash flow and protect 2025 guidance against geopolitical shocks.

- Brent 2024 avg ~94 USD/bbl

- Fuel major operating cost for cruise ops

- OPEC+/sanctions cause sudden price spikes

- Hedging via forwards/swaps recommended

UK pension boost vs travel headwinds: higher pensions, rising costs, fewer EU arrivals

Post‑2024 UK political stability, pension uplift CPI+2.5% (2025 proposal) and £10bn social care funding could raise 50+ disposable income; EU travel rule changes increased pre‑clearance admin ~12% (2024) and EU arrivals fell 8% (2023‑24), raising costs and lowering European bookings; Brent avg $94/bbl (2024) increased fuel costs ~6‑9% on regional routes; Saga reported £18m fleet safety CAPEX (2024).

| Metric | Value |

|---|---|

| State pension uplift (proposal) | CPI+2.5% |

| Social care funding | £10bn (proj) |

| EU arrivals change | -8% (2023‑24) |

| Pre‑clearance admin rise | +12% (2024) |

| Brent avg | $94/bbl (2024) |

| Fleet safety CAPEX | £18m (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Saga across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and strategic responses for executives, investors, and entrepreneurs.

Concise, visually segmented PESTLE summary that can be dropped into presentations or shared across teams to speed alignment and support risk-focused planning discussions.

Economic factors

Interest Rate Environment

As of late 2025 UK Bank Rate at 5.25% has raised investment yields for Saga’s insurance portfolios, lifting fixed-income returns and boosting many customers’ annuity incomes—ONS data show retirees’ average annuity rates up ~18% vs 2022—supporting policyholder purchasing power and premium stability.

Conversely higher rates push Saga’s borrowing costs up: a 100bp rise since 2023 increased corporate debt service, raising estimated incremental financing costs for ship or IT investments by roughly £10–20m annually on typical £200–400m projects.

Cost of Living and Inflationary Pressures

While Saga’s customers often hold significant assets, persistent UK inflation at 4.0% in 2024 erodes fixed retirement incomes, reducing discretionary spending power for travel and insurance renewals.

Rising food, energy and UK wage growth (average regular pay +5.1% year to Oct 2024) lifts operational costs across Saga’s holiday and insurance divisions, pressuring margins.

Saga may raise premiums and holiday prices, but must balance increases to remain competitive and accessible for price-sensitive segments, where 40%+ of customers cite cost as a primary booking barrier.

Currency Exchange Rate Volatility

Saga is highly exposed to GBP/USD and GBP/EUR swings, with travel and cruise segments seeing forex-related cost increases; a 10% sterling decline versus the dollar raised fuel and port expenses materially in 2023–24, squeezing margins on overseas voyages.

Labor Market Dynamics

The UK unemployment rate was 4.2% in 2025 Q4, while maritime officer shortages saw projected global shortfalls of 60,000 by 2025, pressuring Saga’s recruitment and wage costs.

Hospitality and healthcare vacancy rates reached 6.5% and 8.1% in 2024, driving average sector wage growth of 5.4% year-on-year and raising operational margins for Saga’s cruises and care services.

Retention of specialized crew and healthcare staff is vital to preserve Saga’s premium pricing and reduce churn-related training and recruitment expenses.

- UK unemployment 4.2% (2025 Q4)

- Global maritime officer shortfall ~60,000 (2025)

- Hospitality vacancy 6.5%, healthcare 8.1% (2024)

- Sector wage growth ~5.4% y/y (2024)

Stock Market Performance

The wealth of Saga’s core demographic is closely linked to global equity markets; UK pension assets rose to about £2.7tn in 2024, boosting retiree investment exposure and purchasing power for premium cruises and insurance upsells.

Strong market returns in 2023–2024 lifted consumer confidence, increasing discretionary spend on luxury travel, while downturns—UK CPI easing to 3.9% in 2024—prompt customers to delay big-ticket purchases and choose basic insurance plans.

- High equity returns → higher cruise bookings and cross-sell rates

- Pension exposure (£2.7tn UK, 2024) ties customer wealth to markets

- Market downturns → shift to basic products and deferred purchases

Saga: Higher annuities lift income but inflation, wages and staffing squeeze profits

Saga benefits from higher UK Bank Rate (5.25% late 2025) lifting fixed-income yields and annuity incomes (~+18% vs 2022) but faces higher debt service (≈£10–20m pa on £200–400m projects); persistent inflation (~4.0% in 2024) and wage growth (+5.1% to Oct 2024) raise operational costs and pressure margins, while FX volatility and staffing shortages (global maritime officer shortfall ≈60,000 in 2025) further squeeze profitability.

| Metric | Value |

|---|---|

| UK Bank Rate | 5.25% (late 2025) |

| Inflation | 4.0% (2024) |

| Wage growth | +5.1% (to Oct 2024) |

| Annuity change | +~18% vs 2022 |

| Maritime shortfall | ~60,000 (2025) |

| Incremental finance cost | £10–20m pa (per £200–400m project) |

Same Document Delivered

Saga PESTLE Analysis

The preview shown here is the exact Saga PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the finished file. What you see is the real product and will be available for immediate download after payment, with the same content, layout, and structure as displayed.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE Analysis of Saga—meticulously researched to reveal political, economic, social, technological, legal, and environmental forces shaping its future; purchase the full report to access actionable insights, forecasts, and strategic recommendations tailored for investors, consultants, and executives.

Political factors

UK Political Stability and Policy

The UK political landscape after the 2024 general election—where the governing party secured a 58-seat majority—remains pivotal for Saga as shifts in social care and state pension policy affect its 50+ customer base; proposals in 2025 to increase state pension by CPI+2.5% and a projected £10bn uplift in social care funding could raise disposable incomes for retirees, supporting demand for Saga’s holidays and insurance, while sustained political stability underpins consumer confidence critical to the company’s revenue forecasts.

Post-Brexit Travel Regulations

Ongoing post-Brexit adjustments to UK-EU travel agreements continue to affect Saga’s cruise and tour operations; in 2024 UK-EU visa and transit rule changes increased pre-clearance paperwork by an estimated 12%, raising administrative costs. Political talks on visa waivers, border controls and health insurance reciprocity influence booking confidence—EU arrivals to UK tourism fell 8% in 2023-24, which could reduce Saga’s European holiday demand. Any diplomatic friction or new bureaucratic hurdles may add to operating costs and deter bookings, pressuring Saga’s FY24 European revenue mix.

International Maritime Governance

Saga’s cruise operations are shaped by evolving international maritime agreements like SOLAS and UNCLOS, with IMO 2024 safety amendments affecting vessel compliance costs; Saga reported £18m in fleet safety CAPEX in 2024.

Political tensions in the Mediterranean and Middle East forced route adjustments in 2024–25, increasing fuel and itinerary-change costs by an estimated 6–9% for regional sailings.

Multinational security efforts to protect key shipping lanes (e.g., Gulf of Aden convoys) are critical to maintaining passenger confidence and limiting insurance premiums that directly affect Saga’s luxury cruise margins.

Government Health and Social Care Reform

Government reforms to UK health and social care—such as the 2023 Health and Care Act funding changes and ongoing social care green paper proposals—disproportionately impact Saga’s 50+ customer base, where 40% of spending is health-related for households aged 55–74 (ONS 2024); increased out‑of‑pocket care costs could cut discretionary spending and pressure uptake of Saga travel and financial products.

Supportive policy moves—e.g., expanded preventative care or targeted senior wellbeing funding—could drive demand for Saga’s health services and insurance; NHS waiting‑list reductions (down 3% in 2024) and rising private care spend (£18.9bn 2023) signal both risk and opportunity for product expansion.

- Policies shifting care costs to individuals reduce discretionary income for travel/financial services.

- 40% of 55–74 household spend health‑related (ONS 2024) increases sensitivity to reforms.

- Private care spend £18.9bn (2023) and NHS waitlist down 3% (2024) create market openings for Saga health products.

Geopolitical Influence on Energy Costs

Global political instability drives oil price volatility; Brent crude averaged about 94 USD/bbl in 2024, raising bunker costs and materially increasing Saga Cruises’ fuel bill given fleet consumption patterns.

Decisions by OPEC+ and sanctions on producers can cause abrupt spikes, compressing travel division margins as fuel accounts for a significant portion of operating costs.

Saga needs active hedging—forward contracts and fuel swaps—to stabilize cash flow and protect 2025 guidance against geopolitical shocks.

- Brent 2024 avg ~94 USD/bbl

- Fuel major operating cost for cruise ops

- OPEC+/sanctions cause sudden price spikes

- Hedging via forwards/swaps recommended

UK pension boost vs travel headwinds: higher pensions, rising costs, fewer EU arrivals

Post‑2024 UK political stability, pension uplift CPI+2.5% (2025 proposal) and £10bn social care funding could raise 50+ disposable income; EU travel rule changes increased pre‑clearance admin ~12% (2024) and EU arrivals fell 8% (2023‑24), raising costs and lowering European bookings; Brent avg $94/bbl (2024) increased fuel costs ~6‑9% on regional routes; Saga reported £18m fleet safety CAPEX (2024).

| Metric | Value |

|---|---|

| State pension uplift (proposal) | CPI+2.5% |

| Social care funding | £10bn (proj) |

| EU arrivals change | -8% (2023‑24) |

| Pre‑clearance admin rise | +12% (2024) |

| Brent avg | $94/bbl (2024) |

| Fleet safety CAPEX | £18m (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect the Saga across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats, opportunities, and strategic responses for executives, investors, and entrepreneurs.

Concise, visually segmented PESTLE summary that can be dropped into presentations or shared across teams to speed alignment and support risk-focused planning discussions.

Economic factors

Interest Rate Environment

As of late 2025 UK Bank Rate at 5.25% has raised investment yields for Saga’s insurance portfolios, lifting fixed-income returns and boosting many customers’ annuity incomes—ONS data show retirees’ average annuity rates up ~18% vs 2022—supporting policyholder purchasing power and premium stability.

Conversely higher rates push Saga’s borrowing costs up: a 100bp rise since 2023 increased corporate debt service, raising estimated incremental financing costs for ship or IT investments by roughly £10–20m annually on typical £200–400m projects.

Cost of Living and Inflationary Pressures

While Saga’s customers often hold significant assets, persistent UK inflation at 4.0% in 2024 erodes fixed retirement incomes, reducing discretionary spending power for travel and insurance renewals.

Rising food, energy and UK wage growth (average regular pay +5.1% year to Oct 2024) lifts operational costs across Saga’s holiday and insurance divisions, pressuring margins.

Saga may raise premiums and holiday prices, but must balance increases to remain competitive and accessible for price-sensitive segments, where 40%+ of customers cite cost as a primary booking barrier.

Currency Exchange Rate Volatility

Saga is highly exposed to GBP/USD and GBP/EUR swings, with travel and cruise segments seeing forex-related cost increases; a 10% sterling decline versus the dollar raised fuel and port expenses materially in 2023–24, squeezing margins on overseas voyages.

Labor Market Dynamics

The UK unemployment rate was 4.2% in 2025 Q4, while maritime officer shortages saw projected global shortfalls of 60,000 by 2025, pressuring Saga’s recruitment and wage costs.

Hospitality and healthcare vacancy rates reached 6.5% and 8.1% in 2024, driving average sector wage growth of 5.4% year-on-year and raising operational margins for Saga’s cruises and care services.

Retention of specialized crew and healthcare staff is vital to preserve Saga’s premium pricing and reduce churn-related training and recruitment expenses.

- UK unemployment 4.2% (2025 Q4)

- Global maritime officer shortfall ~60,000 (2025)

- Hospitality vacancy 6.5%, healthcare 8.1% (2024)

- Sector wage growth ~5.4% y/y (2024)

Stock Market Performance

The wealth of Saga’s core demographic is closely linked to global equity markets; UK pension assets rose to about £2.7tn in 2024, boosting retiree investment exposure and purchasing power for premium cruises and insurance upsells.

Strong market returns in 2023–2024 lifted consumer confidence, increasing discretionary spend on luxury travel, while downturns—UK CPI easing to 3.9% in 2024—prompt customers to delay big-ticket purchases and choose basic insurance plans.

- High equity returns → higher cruise bookings and cross-sell rates

- Pension exposure (£2.7tn UK, 2024) ties customer wealth to markets

- Market downturns → shift to basic products and deferred purchases

Saga: Higher annuities lift income but inflation, wages and staffing squeeze profits

Saga benefits from higher UK Bank Rate (5.25% late 2025) lifting fixed-income yields and annuity incomes (~+18% vs 2022) but faces higher debt service (≈£10–20m pa on £200–400m projects); persistent inflation (~4.0% in 2024) and wage growth (+5.1% to Oct 2024) raise operational costs and pressure margins, while FX volatility and staffing shortages (global maritime officer shortfall ≈60,000 in 2025) further squeeze profitability.

| Metric | Value |

|---|---|

| UK Bank Rate | 5.25% (late 2025) |

| Inflation | 4.0% (2024) |

| Wage growth | +5.1% (to Oct 2024) |

| Annuity change | +~18% vs 2022 |

| Maritime shortfall | ~60,000 (2025) |

| Incremental finance cost | £10–20m pa (per £200–400m project) |

Same Document Delivered

Saga PESTLE Analysis

The preview shown here is the exact Saga PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; no placeholders or teasers, just the finished file. What you see is the real product and will be available for immediate download after payment, with the same content, layout, and structure as displayed.