Saga Communications PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Saga Communications—identify regulatory, economic, and technological forces shaping its broadcast and digital operations, and turn those insights into competitive advantage; purchase the full report for a ready-to-use, fully sourced breakdown that accelerates smarter investment and strategy decisions.

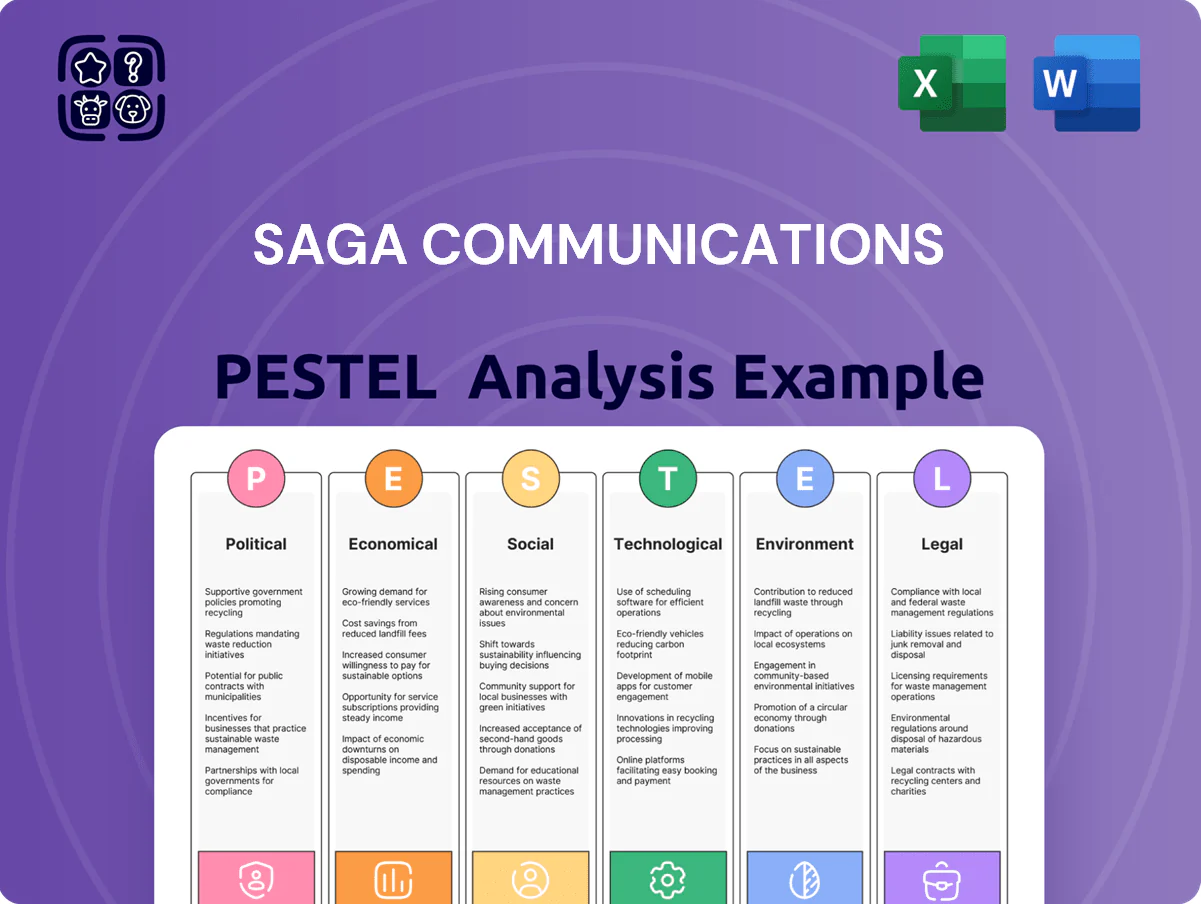

Political factors

FCC ownership deregulation

The FCC's late-2025 proposals signal possible relaxation of local radio ownership caps, which could let Saga Communications expand beyond its current ~70-market footprint; deregulation could enable acquisitions increasing station count and ad revenue share.

With Saga reporting $275.6m revenue in FY2024 and operating margins near 18%, targeted M&A in mid-sized markets could boost economies of scale and improve EBITDA margins.

Political shifts increasing consolidation flexibility would directly affect Saga's ability to grow market share, negotiate better ad rates, and lower per-station costs.

Political advertising revenue cycles

As an off-election year after 2024, Saga faces a typical political ad revenue decline—industry estimates show national political ad spend fell by ~40% in 2025 vs 2024, pressuring high-margin local spots that boosted Saga’s Q4 2024 margins; management is prioritizing stronger local commercial sales and diversifying into events and digital subscriptions to offset an estimated mid-single-digit revenue gap. Polarization keeps news/talk audience engagement robust, supporting CPM resilience.

Federal spectrum management

Ongoing federal debates on repurposing spectrum for 5G and mobile — with FCC incentive auctions reallocating billions in spectrum value (recent auctions raised over $10B in 2021–2023) — present long-term strategic risk to Saga Communications’ AM/FM assets; radio is less targeted than TV but rezoning could reduce coverage or force equipment upgrades costing millions.

Trade policies and hardware costs

Trade tensions and tariffs on electronic components can raise Saga Communications’ capex for transmitter and STL upgrades; US tariffs and 2024 semiconductor supply shocks pushed prices for RF modules up an estimated 8–12%, increasing projected FY2025 capital needs by roughly $1–2M versus prior plans.

Fluctuating international trade policy risks raising costs of specialized broadcast hardware, impacting replacement schedules and spare-parts inventory for Saga’s largely owned-station portfolio.

Stable political relations help preserve Saga’s conservative balance sheet and predictable depreciation, supporting current capex guidance and dividend coverage ratios.

- Tariff-driven RF module price rise ~8–12% (2024)

- Estimated incremental capex impact $1–2M for FY2025

- Stability supports depreciation predictability and conservative leverage

Public broadcasting funding

Political debates over public media funding can boost Saga as cuts to CPB and reduced federal grants—CPB funding fell 9% in FY2024 to about $445 million—shift listeners to commercial stations offering local content.

Saga’s 2024 Q3 local ad revenue resilience (flat Y/Y amid sector declines) suggests markets where it is the primary local news source could capture displaced audiences, enhancing market share and ad yield.

- CPB funding down 9% in FY2024 to ~$445M

- Saga local ad revenue stable in 2024 Q3

- Opportunity: gain listeners seeking community content

Saga Eyes M&A Upside as FCC Shifts, CPB Cuts Boost Local Radio Resilience

Political shifts toward relaxed FCC ownership caps and spectrum repurposing materially affect Saga’s M&A upside and capex; FY2024 revenue $275.6M, operating margin ~18%, tariff-driven RF cost rise ~8–12% adding $1–2M FY2025 capex; CPB funding down 9% to ~$445M may divert listeners to commercial radio, aiding local ad resilience.

| Metric | Value |

|---|---|

| FY2024 Revenue | $275.6M |

| Op Margin | ~18% |

| RF price rise (2024) | 8–12% |

| Est. incremental capex | $1–2M |

| CPB funding FY2024 | $445M (-9%) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Saga Communications across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current trends and localized market/regulatory dynamics to identify threats and opportunities.

A concise, PESTLE-segmented summary of Saga Communications that’s easy to drop into presentations or share across teams, helping quickly align stakeholders on external risks, market positioning, and regulatory impacts.

Economic factors

Local market economic resilience

Saga operates primarily in small to mid-sized U.S. markets that in 2024 showed 1.8% average GDP growth versus 2.1% nationally, often exhibiting steadier consumer spending and lower rent inflation, which can cushion ad demand.

These markets depend on sectors like manufacturing and agriculture; for example, Midwest manufacturing employment fell 0.5% in 2023, directly affecting local ad budgets.

Saga’s 2024 radio advertising revenue mix—over 70% local sales—ties its EBITDA sensitivity to the financial health of community businesses and regional employment trends.

Interest rate environment

By end-2025, elevated U.S. policy rates—Fed funds near 5.25–5.50% in 2024–25—raise Saga Communications’ weighted average cost of capital, increasing borrowing costs for acquisitions despite its strong cash reserves (cash and equivalents were $40–70m in recent years). High rates have cooled M&A activity, constraining deal flow and valuation multiples in radio/broadcasting. A stabilizing rate path would restore predictable debt servicing and support multi-year capital planning for station purchases and capex.

Inflationary pressure on operating costs

Persistent inflation through 2025 lifts wages, transmitter utility costs and admin expenses; US CPI averaged 3.4% in 2024 and consensus 2025 core CPI ~3.0% presses Saga’s OPEX higher, with energy/hardware line items up 8–12% y/y for broadcasters.

Saga faces limited pass-through as local ad budgets contracted ~2–4% in 2024; raising ad rates risks volume loss, so revenue elasticity constraints cap pricing power.

Maintaining margins requires tight cost control—targeting 3–5% efficiency gains, centralizing back-office functions across 25+ station clusters and prioritizing capex with payback under 24 months.

Consumer discretionary spending

Economic health directly drives consumer discretionary spending, which in 2024 rose 2.5% year-over-year but slowed several metros where Saga operates, pressuring retail and automotive ad budgets that account for an estimated 35% of local radio ad revenue.

Declines in consumer confidence—down to 97.2 in Dec 2025 from 109.4 in 2021—prompt immediate pullbacks in local radio ad spend as businesses cut marketing.

Saga’s presence across ~30 small- and mid-sized markets and revenue diversification across formats reduces exposure to any single-local downturn, stabilizing overall ad receipts.

- Consumer discretionary +2.5% (2024)

- Consumer Confidence 97.2 (Dec 2025)

- Retail/auto ≈35% of local ad revenue

- ~30 small/mid markets diversified footprint

Labor market dynamics

Saga’s retention is critical: turnover increases recruitment spend and risks local ratings; maintaining competitive pay and benefits is essential to protect advertising revenue that comprised about 88% of Saga’s 2024 net revenue.

- Wage growth ~3.5%–4% (2024)

- Advertising ~88% of Saga’s 2024 net revenue

- Higher turnover → increased recruitment and margin pressure

Saga faces ad‑revenue pressure as local GDP & consumer confidence lag amid higher rates

Saga’s small/mid‑market exposure ties revenue to local GDP and employment; 2024 local GDP +1.8% vs US +2.1%, consumer discretionary +2.5% and consumer confidence 97.2 (Dec 2025) pressured local ad budgets ~‑2–4%. Higher rates (Fed funds ~5.25–5.50% in 2024–25) raised WACC and cooled M&A; 2024 ad mix: ~70% local, advertising ~88% of net revenue; wage growth ~3.5–4%.

| Metric | Value |

|---|---|

| Local GDP (avg 2024) | +1.8% |

| US GDP (2024) | +2.1% |

| Consumer discretionary (2024) | +2.5% |

| Consumer confidence (Dec 2025) | 97.2 |

| Fed funds (2024–25) | 5.25–5.50% |

| Ad mix local | ~70% |

| Advertising share of revenue (2024) | ~88% |

| Wage growth (2024) | 3.5–4% |

Preview Before You Purchase

Saga Communications PESTLE Analysis

The preview shown here is the exact Saga Communications PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are exactly what you’ll download immediately after payment.

Use it for strategic planning, investor briefings, or coursework with confidence—the file you see is the final product.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our PESTLE Analysis of Saga Communications—identify regulatory, economic, and technological forces shaping its broadcast and digital operations, and turn those insights into competitive advantage; purchase the full report for a ready-to-use, fully sourced breakdown that accelerates smarter investment and strategy decisions.

Political factors

FCC ownership deregulation

The FCC's late-2025 proposals signal possible relaxation of local radio ownership caps, which could let Saga Communications expand beyond its current ~70-market footprint; deregulation could enable acquisitions increasing station count and ad revenue share.

With Saga reporting $275.6m revenue in FY2024 and operating margins near 18%, targeted M&A in mid-sized markets could boost economies of scale and improve EBITDA margins.

Political shifts increasing consolidation flexibility would directly affect Saga's ability to grow market share, negotiate better ad rates, and lower per-station costs.

Political advertising revenue cycles

As an off-election year after 2024, Saga faces a typical political ad revenue decline—industry estimates show national political ad spend fell by ~40% in 2025 vs 2024, pressuring high-margin local spots that boosted Saga’s Q4 2024 margins; management is prioritizing stronger local commercial sales and diversifying into events and digital subscriptions to offset an estimated mid-single-digit revenue gap. Polarization keeps news/talk audience engagement robust, supporting CPM resilience.

Federal spectrum management

Ongoing federal debates on repurposing spectrum for 5G and mobile — with FCC incentive auctions reallocating billions in spectrum value (recent auctions raised over $10B in 2021–2023) — present long-term strategic risk to Saga Communications’ AM/FM assets; radio is less targeted than TV but rezoning could reduce coverage or force equipment upgrades costing millions.

Trade policies and hardware costs

Trade tensions and tariffs on electronic components can raise Saga Communications’ capex for transmitter and STL upgrades; US tariffs and 2024 semiconductor supply shocks pushed prices for RF modules up an estimated 8–12%, increasing projected FY2025 capital needs by roughly $1–2M versus prior plans.

Fluctuating international trade policy risks raising costs of specialized broadcast hardware, impacting replacement schedules and spare-parts inventory for Saga’s largely owned-station portfolio.

Stable political relations help preserve Saga’s conservative balance sheet and predictable depreciation, supporting current capex guidance and dividend coverage ratios.

- Tariff-driven RF module price rise ~8–12% (2024)

- Estimated incremental capex impact $1–2M for FY2025

- Stability supports depreciation predictability and conservative leverage

Public broadcasting funding

Political debates over public media funding can boost Saga as cuts to CPB and reduced federal grants—CPB funding fell 9% in FY2024 to about $445 million—shift listeners to commercial stations offering local content.

Saga’s 2024 Q3 local ad revenue resilience (flat Y/Y amid sector declines) suggests markets where it is the primary local news source could capture displaced audiences, enhancing market share and ad yield.

- CPB funding down 9% in FY2024 to ~$445M

- Saga local ad revenue stable in 2024 Q3

- Opportunity: gain listeners seeking community content

Saga Eyes M&A Upside as FCC Shifts, CPB Cuts Boost Local Radio Resilience

Political shifts toward relaxed FCC ownership caps and spectrum repurposing materially affect Saga’s M&A upside and capex; FY2024 revenue $275.6M, operating margin ~18%, tariff-driven RF cost rise ~8–12% adding $1–2M FY2025 capex; CPB funding down 9% to ~$445M may divert listeners to commercial radio, aiding local ad resilience.

| Metric | Value |

|---|---|

| FY2024 Revenue | $275.6M |

| Op Margin | ~18% |

| RF price rise (2024) | 8–12% |

| Est. incremental capex | $1–2M |

| CPB funding FY2024 | $445M (-9%) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Saga Communications across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section backed by current trends and localized market/regulatory dynamics to identify threats and opportunities.

A concise, PESTLE-segmented summary of Saga Communications that’s easy to drop into presentations or share across teams, helping quickly align stakeholders on external risks, market positioning, and regulatory impacts.

Economic factors

Local market economic resilience

Saga operates primarily in small to mid-sized U.S. markets that in 2024 showed 1.8% average GDP growth versus 2.1% nationally, often exhibiting steadier consumer spending and lower rent inflation, which can cushion ad demand.

These markets depend on sectors like manufacturing and agriculture; for example, Midwest manufacturing employment fell 0.5% in 2023, directly affecting local ad budgets.

Saga’s 2024 radio advertising revenue mix—over 70% local sales—ties its EBITDA sensitivity to the financial health of community businesses and regional employment trends.

Interest rate environment

By end-2025, elevated U.S. policy rates—Fed funds near 5.25–5.50% in 2024–25—raise Saga Communications’ weighted average cost of capital, increasing borrowing costs for acquisitions despite its strong cash reserves (cash and equivalents were $40–70m in recent years). High rates have cooled M&A activity, constraining deal flow and valuation multiples in radio/broadcasting. A stabilizing rate path would restore predictable debt servicing and support multi-year capital planning for station purchases and capex.

Inflationary pressure on operating costs

Persistent inflation through 2025 lifts wages, transmitter utility costs and admin expenses; US CPI averaged 3.4% in 2024 and consensus 2025 core CPI ~3.0% presses Saga’s OPEX higher, with energy/hardware line items up 8–12% y/y for broadcasters.

Saga faces limited pass-through as local ad budgets contracted ~2–4% in 2024; raising ad rates risks volume loss, so revenue elasticity constraints cap pricing power.

Maintaining margins requires tight cost control—targeting 3–5% efficiency gains, centralizing back-office functions across 25+ station clusters and prioritizing capex with payback under 24 months.

Consumer discretionary spending

Economic health directly drives consumer discretionary spending, which in 2024 rose 2.5% year-over-year but slowed several metros where Saga operates, pressuring retail and automotive ad budgets that account for an estimated 35% of local radio ad revenue.

Declines in consumer confidence—down to 97.2 in Dec 2025 from 109.4 in 2021—prompt immediate pullbacks in local radio ad spend as businesses cut marketing.

Saga’s presence across ~30 small- and mid-sized markets and revenue diversification across formats reduces exposure to any single-local downturn, stabilizing overall ad receipts.

- Consumer discretionary +2.5% (2024)

- Consumer Confidence 97.2 (Dec 2025)

- Retail/auto ≈35% of local ad revenue

- ~30 small/mid markets diversified footprint

Labor market dynamics

Saga’s retention is critical: turnover increases recruitment spend and risks local ratings; maintaining competitive pay and benefits is essential to protect advertising revenue that comprised about 88% of Saga’s 2024 net revenue.

- Wage growth ~3.5%–4% (2024)

- Advertising ~88% of Saga’s 2024 net revenue

- Higher turnover → increased recruitment and margin pressure

Saga faces ad‑revenue pressure as local GDP & consumer confidence lag amid higher rates

Saga’s small/mid‑market exposure ties revenue to local GDP and employment; 2024 local GDP +1.8% vs US +2.1%, consumer discretionary +2.5% and consumer confidence 97.2 (Dec 2025) pressured local ad budgets ~‑2–4%. Higher rates (Fed funds ~5.25–5.50% in 2024–25) raised WACC and cooled M&A; 2024 ad mix: ~70% local, advertising ~88% of net revenue; wage growth ~3.5–4%.

| Metric | Value |

|---|---|

| Local GDP (avg 2024) | +1.8% |

| US GDP (2024) | +2.1% |

| Consumer discretionary (2024) | +2.5% |

| Consumer confidence (Dec 2025) | 97.2 |

| Fed funds (2024–25) | 5.25–5.50% |

| Ad mix local | ~70% |

| Advertising share of revenue (2024) | ~88% |

| Wage growth (2024) | 3.5–4% |

Preview Before You Purchase

Saga Communications PESTLE Analysis

The preview shown here is the exact Saga Communications PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the content, layout, and structure visible now are exactly what you’ll download immediately after payment.

Use it for strategic planning, investor briefings, or coursework with confidence—the file you see is the final product.