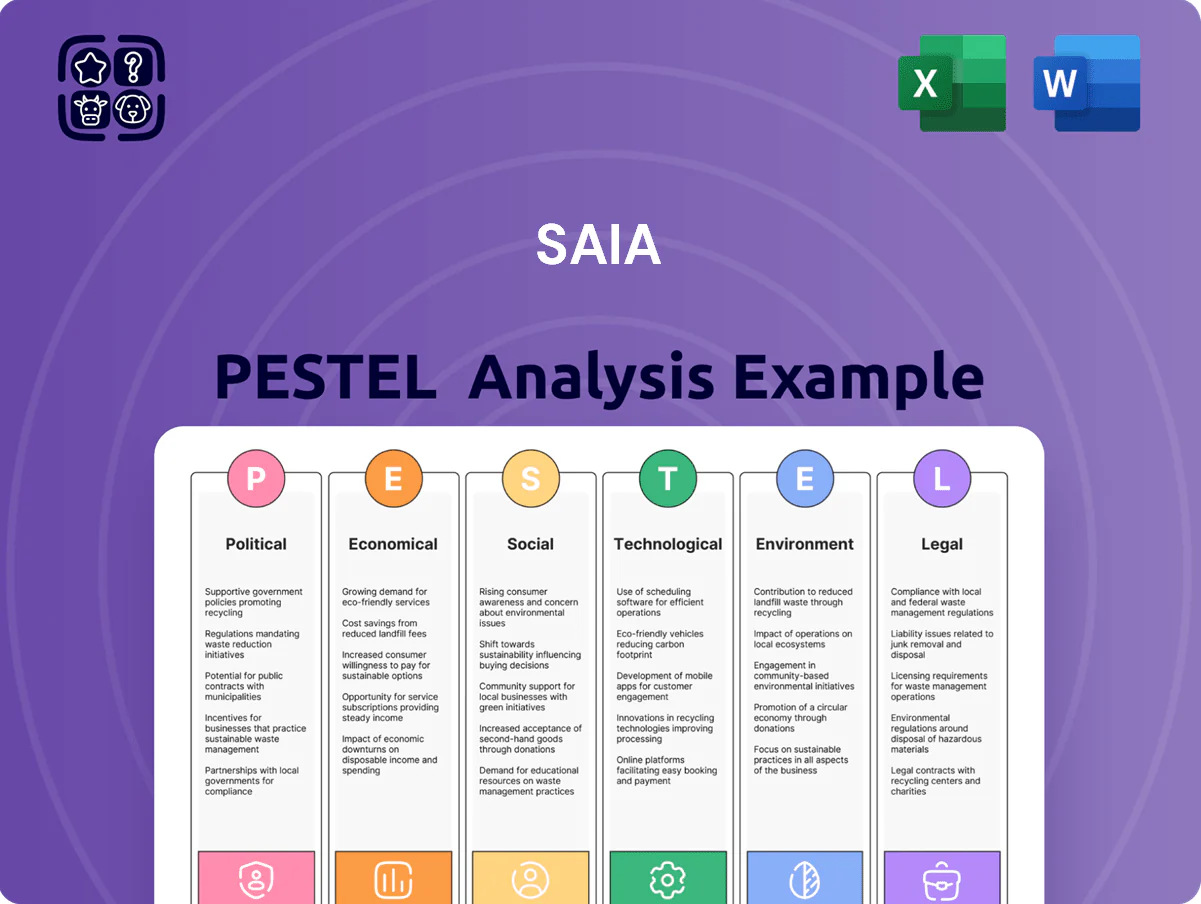

Saia PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological change are reshaping Saia’s growth prospects in our concise PESTLE snapshot—built for investors and strategists who need fast, actionable context. Purchase the full PESTLE to access deep-dive analysis, risk scoring, and practical recommendations you can apply immediately.

Political factors

Federal Infrastructure Investment

The continued rollout of funding from the Infrastructure Investment and Jobs Act, which allocated $1.2 trillion overall and directed roughly $110 billion to roads and bridges, remains a critical driver for Saia’s operational efficiency by lowering maintenance costs and improving route reliability.

Improved highway conditions and bridge repairs reduce vehicle wear and tear and decreased transit times—USDOT estimated a 10–15% congestion reduction on upgraded corridors—supporting lower operating ratios for LTL carriers like Saia.

Federal focus on modernizing freight corridors and $25 billion earmarked for port and intermodal improvements enables more reliable scheduling and underpins Saia’s terminal expansion strategy, enhancing network density and asset utilization.

Trade Policy and Nearshoring

Shifting geopolitical dynamics have accelerated nearshoring, with Mexico manufacturing exports to the US rising ~8.2% in 2024, boosting cross-border freight volumes that favor Saia’s strong southern US footprint.

Saia benefits from policy-driven supply-chain shortening—its 2024 regional volumes grew ~6% year-over-year in southern lanes as shippers rerouted from Asia.

Changes in US trade agreements or tariffs can materially affect LTL demand; a 1% tariff swing on manufactured goods could shift millions in freight flows across Saia’s network, directly impacting revenue mix and yield.

Labor Relations and Unionization

Federal oversight and a pro-union NLRB stance raise compliance costs for trucking; in 2024 union election petitions rose 12% in transportation, pressuring carriers like Saia to monitor labor rule changes that can raise wage floors.

Saia remains primarily non-union, but sector-wide collective bargaining gains could push industry wages above Saia’s 2024 reported median driver pay of about $74,000, increasing labor expense.

Legislative efforts to reclassify independent contractors—affecting roughly 10–15% of trucking capacity nationally—could reduce flexibility and raise payroll liabilities, making ongoing regulatory monitoring essential.

Energy Security and Fuel Regulation

Political choices on domestic oil output and SPR releases drive diesel price swings; U.S. retail diesel averaged 4.08 USD/gal in 2024 and spiked 18% during 2022–23 geopolitical disruptions, increasing Saia's operating fuel costs.

Fuel surcharges offset some volatility, but demand and lane flows shift when prices jump; Saia reported 2024 fuel expense pressure reflected in higher per-RTM costs and margin sensitivity.

Federal incentives—IRA credits and state grants for CNG/electric trucks—reshape Saia's procurement and fleet capex plans, with electrification TCO estimates showing parity windows by late 2030s under current subsidies.

- 2024 U.S. diesel avg 4.08 USD/gal; 18% spike in 2022–23

- Fuel surcharges mitigate but don’t eliminate margin exposure

- IRA and state incentives accelerate alternative-fuel capex planning

Safety and Security Mandates

Heightened government focus on transportation security and national safety standards requires Saia to continuously comply with federal mandates; TSA and DOT updates on hazardous materials and cross-border freight rose 18% in 2024, increasing compliance costs for carriers by an estimated $45–70 million industry-wide.

Adapting to evolving political priorities ensures Saia retains operating licenses and avoids fines—DOT civil penalties exceeded $160 million in 2023—reducing risk of service interruptions and protecting revenue.

- 2024: TSA/DOT policy updates +18%

- Estimated industry compliance cost impact $45–70M

- DOT civil penalties > $160M in 2023

Infrastructure Boosts Network Efficiency but Fuel and Labor Pressures Raise Costs

Federal infrastructure funding (IIJA $110B for roads) and $25B for ports improve network reliability, lowering Saia’s maintenance and transit costs; nearshoring lifted southern volumes ~6% in 2024 while Mexico exports rose ~8.2%; diesel averaged $4.08/gal in 2024 (18% spike 2022–23) raising fuel sensitivity despite surcharges; regulatory and labor shifts (NLRB activity +12% petitions 2024) increase compliance and wage pressure.

| Metric | 2024/Recent |

|---|---|

| IIJA roads funding | $110B |

| Ports/intermodal | $25B |

| Mexico exports growth | +8.2% (2024) |

| Saia southern volumes | +6% YoY (2024) |

| U.S. diesel | $4.08/gal (2024) |

| NLRB petitions in transport | +12% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Saia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to surface actionable risks and opportunities.

Condenses Saia's PESTLE insights into a concise, presentation-ready summary that teams can quickly reference to align on external risks, regulatory shifts, and market positioning.

Economic factors

Interest Rate Environment

As of late 2025, the U.S. Fed funds rate sat near 5.25–5.50%, raising Saia’s marginal cost of debt for terminal buys and fleet financing; higher rates could add several hundred basis points to borrowing costs, constraining expansion.

Industrial Production and ISM Trends

Saia's revenue and tonnage are tightly linked to U.S. industrial production and the ISM Manufacturing PMI; with ISM at 48.5 in Dec 2025 signaling contraction, Saia faced softer volume trends late 2025 versus 2024 when PMI averaged ~52 and industrial production grew ~2.1%, supporting higher yields and improved asset utilization across regional and national lanes.

Inflationary Pressure on Operating Costs

Persistent inflation elevated Saia’s input costs in 2024–25—tire and parts prices rose ~6–9% year-over-year while average driver wage per hour climbed about 8% (per industry TSR data), squeezing margins; disciplined fuel surcharges and pricing helped maintain 2024 adjusted operating ratio near 84–86% but further increases would require tighter route density and cost controls. Saia must carefully pass costs to customers without losing volume in a price-sensitive LTL market.

E-commerce and Retail Resilience

Saia benefits from omnichannel growth: US e-commerce sales hit $1.1 trillion in 2024, driving higher middle-mile LTL volumes as retailers favor frequent, smaller shipments.

Shifts to online spending increase delivery fragmentation, aligning with Saia’s network density and regional hubs that improve asset utilization and margins.

Integration with major retailers—Saia serves top grocers and big-box chains—creates a durable moat versus FTL carriers by capturing recurring LTL flows.

- 2024 US e-commerce: $1.1T

- Higher frequency shipments → more LTL demand

- Saia’s regional network boosts utilization/margins

- Deep retailer integrations = economic moat

Labor Market Dynamics

The shortage and rising cost of qualified CDL drivers remain a key economic challenge for Saia; average U.S. truck driver pay rose about 7% in 2024, pushing Saia’s labor expense upward and contributing to industry-wide tight labor supply.

Wage competition and expanded benefits packages increase Saia’s personnel costs—Saia reported total operating labor expense growth of roughly mid-single digits in 2024, reflecting this pressure.

Macroeconomic shifts affect turnover; with industry turnover around 60% in 2024, Saia must invest heavily in recruitment and retention to sustain service levels, increasing recruiting and training spend.

- CDL driver pay growth ~7% (2024)

- Industry turnover ~60% (2024)

- Saia labor expense growth mid-single digits (2024)

Higher rates, rising costs squeeze Saia margins despite e‑commerce‑driven LTL demand

Higher U.S. rates (Fed funds ~5.25–5.50% in late 2025) raised Saia’s cost of capital; weaker ISM (48.5 Dec 2025) pressured volumes vs 2024; inflation pushed input costs +6–9% and driver pay ~7% (2024), squeezing margins while e-commerce ($1.1T 2024) and retailer contracts bolster LTL demand and network utilization.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| ISM Manufacturing (Dec 2025) | 48.5 |

| US e‑commerce (2024) | $1.1T |

| Driver pay growth (2024) | ~7% |

| Tire/parts inflation (2024–25) | 6–9% YoY |

What You See Is What You Get

Saia PESTLE Analysis

The preview shown here is the exact Saia PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Explore how political shifts, economic cycles, and technological change are reshaping Saia’s growth prospects in our concise PESTLE snapshot—built for investors and strategists who need fast, actionable context. Purchase the full PESTLE to access deep-dive analysis, risk scoring, and practical recommendations you can apply immediately.

Political factors

Federal Infrastructure Investment

The continued rollout of funding from the Infrastructure Investment and Jobs Act, which allocated $1.2 trillion overall and directed roughly $110 billion to roads and bridges, remains a critical driver for Saia’s operational efficiency by lowering maintenance costs and improving route reliability.

Improved highway conditions and bridge repairs reduce vehicle wear and tear and decreased transit times—USDOT estimated a 10–15% congestion reduction on upgraded corridors—supporting lower operating ratios for LTL carriers like Saia.

Federal focus on modernizing freight corridors and $25 billion earmarked for port and intermodal improvements enables more reliable scheduling and underpins Saia’s terminal expansion strategy, enhancing network density and asset utilization.

Trade Policy and Nearshoring

Shifting geopolitical dynamics have accelerated nearshoring, with Mexico manufacturing exports to the US rising ~8.2% in 2024, boosting cross-border freight volumes that favor Saia’s strong southern US footprint.

Saia benefits from policy-driven supply-chain shortening—its 2024 regional volumes grew ~6% year-over-year in southern lanes as shippers rerouted from Asia.

Changes in US trade agreements or tariffs can materially affect LTL demand; a 1% tariff swing on manufactured goods could shift millions in freight flows across Saia’s network, directly impacting revenue mix and yield.

Labor Relations and Unionization

Federal oversight and a pro-union NLRB stance raise compliance costs for trucking; in 2024 union election petitions rose 12% in transportation, pressuring carriers like Saia to monitor labor rule changes that can raise wage floors.

Saia remains primarily non-union, but sector-wide collective bargaining gains could push industry wages above Saia’s 2024 reported median driver pay of about $74,000, increasing labor expense.

Legislative efforts to reclassify independent contractors—affecting roughly 10–15% of trucking capacity nationally—could reduce flexibility and raise payroll liabilities, making ongoing regulatory monitoring essential.

Energy Security and Fuel Regulation

Political choices on domestic oil output and SPR releases drive diesel price swings; U.S. retail diesel averaged 4.08 USD/gal in 2024 and spiked 18% during 2022–23 geopolitical disruptions, increasing Saia's operating fuel costs.

Fuel surcharges offset some volatility, but demand and lane flows shift when prices jump; Saia reported 2024 fuel expense pressure reflected in higher per-RTM costs and margin sensitivity.

Federal incentives—IRA credits and state grants for CNG/electric trucks—reshape Saia's procurement and fleet capex plans, with electrification TCO estimates showing parity windows by late 2030s under current subsidies.

- 2024 U.S. diesel avg 4.08 USD/gal; 18% spike in 2022–23

- Fuel surcharges mitigate but don’t eliminate margin exposure

- IRA and state incentives accelerate alternative-fuel capex planning

Safety and Security Mandates

Heightened government focus on transportation security and national safety standards requires Saia to continuously comply with federal mandates; TSA and DOT updates on hazardous materials and cross-border freight rose 18% in 2024, increasing compliance costs for carriers by an estimated $45–70 million industry-wide.

Adapting to evolving political priorities ensures Saia retains operating licenses and avoids fines—DOT civil penalties exceeded $160 million in 2023—reducing risk of service interruptions and protecting revenue.

- 2024: TSA/DOT policy updates +18%

- Estimated industry compliance cost impact $45–70M

- DOT civil penalties > $160M in 2023

Infrastructure Boosts Network Efficiency but Fuel and Labor Pressures Raise Costs

Federal infrastructure funding (IIJA $110B for roads) and $25B for ports improve network reliability, lowering Saia’s maintenance and transit costs; nearshoring lifted southern volumes ~6% in 2024 while Mexico exports rose ~8.2%; diesel averaged $4.08/gal in 2024 (18% spike 2022–23) raising fuel sensitivity despite surcharges; regulatory and labor shifts (NLRB activity +12% petitions 2024) increase compliance and wage pressure.

| Metric | 2024/Recent |

|---|---|

| IIJA roads funding | $110B |

| Ports/intermodal | $25B |

| Mexico exports growth | +8.2% (2024) |

| Saia southern volumes | +6% YoY (2024) |

| U.S. diesel | $4.08/gal (2024) |

| NLRB petitions in transport | +12% (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Saia across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to surface actionable risks and opportunities.

Condenses Saia's PESTLE insights into a concise, presentation-ready summary that teams can quickly reference to align on external risks, regulatory shifts, and market positioning.

Economic factors

Interest Rate Environment

As of late 2025, the U.S. Fed funds rate sat near 5.25–5.50%, raising Saia’s marginal cost of debt for terminal buys and fleet financing; higher rates could add several hundred basis points to borrowing costs, constraining expansion.

Industrial Production and ISM Trends

Saia's revenue and tonnage are tightly linked to U.S. industrial production and the ISM Manufacturing PMI; with ISM at 48.5 in Dec 2025 signaling contraction, Saia faced softer volume trends late 2025 versus 2024 when PMI averaged ~52 and industrial production grew ~2.1%, supporting higher yields and improved asset utilization across regional and national lanes.

Inflationary Pressure on Operating Costs

Persistent inflation elevated Saia’s input costs in 2024–25—tire and parts prices rose ~6–9% year-over-year while average driver wage per hour climbed about 8% (per industry TSR data), squeezing margins; disciplined fuel surcharges and pricing helped maintain 2024 adjusted operating ratio near 84–86% but further increases would require tighter route density and cost controls. Saia must carefully pass costs to customers without losing volume in a price-sensitive LTL market.

E-commerce and Retail Resilience

Saia benefits from omnichannel growth: US e-commerce sales hit $1.1 trillion in 2024, driving higher middle-mile LTL volumes as retailers favor frequent, smaller shipments.

Shifts to online spending increase delivery fragmentation, aligning with Saia’s network density and regional hubs that improve asset utilization and margins.

Integration with major retailers—Saia serves top grocers and big-box chains—creates a durable moat versus FTL carriers by capturing recurring LTL flows.

- 2024 US e-commerce: $1.1T

- Higher frequency shipments → more LTL demand

- Saia’s regional network boosts utilization/margins

- Deep retailer integrations = economic moat

Labor Market Dynamics

The shortage and rising cost of qualified CDL drivers remain a key economic challenge for Saia; average U.S. truck driver pay rose about 7% in 2024, pushing Saia’s labor expense upward and contributing to industry-wide tight labor supply.

Wage competition and expanded benefits packages increase Saia’s personnel costs—Saia reported total operating labor expense growth of roughly mid-single digits in 2024, reflecting this pressure.

Macroeconomic shifts affect turnover; with industry turnover around 60% in 2024, Saia must invest heavily in recruitment and retention to sustain service levels, increasing recruiting and training spend.

- CDL driver pay growth ~7% (2024)

- Industry turnover ~60% (2024)

- Saia labor expense growth mid-single digits (2024)

Higher rates, rising costs squeeze Saia margins despite e‑commerce‑driven LTL demand

Higher U.S. rates (Fed funds ~5.25–5.50% in late 2025) raised Saia’s cost of capital; weaker ISM (48.5 Dec 2025) pressured volumes vs 2024; inflation pushed input costs +6–9% and driver pay ~7% (2024), squeezing margins while e-commerce ($1.1T 2024) and retailer contracts bolster LTL demand and network utilization.

| Metric | Value |

|---|---|

| Fed funds (late 2025) | 5.25–5.50% |

| ISM Manufacturing (Dec 2025) | 48.5 |

| US e‑commerce (2024) | $1.1T |

| Driver pay growth (2024) | ~7% |

| Tire/parts inflation (2024–25) | 6–9% YoY |

What You See Is What You Get

Saia PESTLE Analysis

The preview shown here is the exact Saia PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.