St Mamet PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping St Mamet’s trajectory—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full analysis for the complete, editable report and actionable insights you can use immediately.

Political factors

Agricultural Sovereignty Policies

The French government has strengthened food sovereignty measures, aiming to cut non-EU fruit imports by 20% by 2027, creating access for St Mamet to regional subsidies and CAP top-ups targeted at domestic processing in Occitanie.

Policy programs earmark roughly EUR 120m (2024–25) for local fruit sector resilience, improving grant and investment credits that can offset operating costs at St Mamet’s French plants.

National initiatives prioritize supply-chain resilience—buffer stock schemes and logistics grants—reducing disruption risk for St Mamet amid rising global volatility and supporting continued domestic production.

EU Common Agricultural Policy Reforms

Ongoing CAP reforms (2023–2027) shift EUR 58 billion in annual EU subsidies toward eco-schemes and conditional payments, altering incentives for St Mamet’s French fruit suppliers and potentially raising raw material costs by 5–12% due to compliance investments. Emphasis on sustainable land use and the Green Deal’s Farm to Fork targets may tighten supply as farmers reallocate acreage, forcing St Mamet to manage procurement complexity and secure compliant contracts to maintain continuity.

Trade Relations and Import Tariffs

Changes to EU trade deals with major fruit exporters like Morocco and Chile shift supply costs for processed fruit; EU imports of canned fruit rose 7.2% in 2023, affecting margins for players such as St Mamet.

Protective tariffs on canned goods, e.g., recent anti-dumping duties averaging 8–12% on some non-EU producers, can make imports pricier and benefit domestic brands like St Mamet.

Trade tensions raise input costs: in 2024 tariffs and logistics disruptions increased machinery and specialized ingredient prices by an estimated 4–6% for Eurozone food processors.

Government Support for Industrial Decarbonization

Political pressure to meet 2030 and 2050 climate targets has unlocked state-funded grants—EU IPCEI and France Relance—covering up to 40% of CAPEX for industrial decarbonization; St Mamet can apply to programs that awarded €3.5bn to food and agri-industrial projects in 2024–25.

Leveraging these grants can reduce transition CAPEX from electrification/biomass retrofits (estimated €15–25m per plant) by ~€6–10m, improving project IRR and signalling alignment with national emissions-reduction goals.

Public funding and compliance improve long-term operational viability, lower regulatory risk, and bolster PR—70% of EU consumers in 2024 favored brands with verified net-zero commitments, enhancing market access.

- Grants cover up to 40% of CAPEX

- €3.5bn allocated to related projects (2024–25)

- Estimated plant CAPEX €15–25m; potential grant €6–10m

- 70% of EU consumers favor net-zero brands (2024)

Geopolitical Stability and Energy Security

European geopolitical tensions keep energy prices volatile; wholesale natural gas averaged about €46/MWh in 2024, up ~18% vs 2023, directly raising pasteurization and canning energy costs at Vauvert and Nîmes.

French policy shifts—accelerated nuclear life‑extension and renewables targets—will alter long‑term tariffs, while infrastructure decisions (e.g., LNG terminals) affect short‑term supply security and logistics costs.

Management must track EU‑Russia relations, Mediterranean pipeline developments, and 2024–25 gas storage levels (France ~70–90% seasonal range) to forecast spikes in processing and transport expenses.

- 2024 avg gas €46/MWh; +18% YoY

- Nuclear/renewables policy affects tariff trajectory

- LNG/infrastructure changes impact short‑term supply

- Monitor Russia/EU relations and gas storage (70–90%)

France boosts food‑sovereignty support amid rising CAP costs, imports and gas‑driven margins

Stronger French food‑sovereignty rules and EUR 120m (2024–25) programmes favor domestic processors; CAP reforms (EUR 58bn/yr) and eco‑schemes may raise supplier costs 5–12%; anti‑dumping duties (8–12%) and 7.2% rise in EU canned‑fruit imports (2023) shift margins; €3.5bn grants (2024–25) cover up to 40% CAPEX; 2024 gas €46/MWh (+18% YoY) pressures processing costs.

| Indicator | Value |

|---|---|

| France programme | €120m (2024–25) |

| CAP budget | €58bn/yr |

| Import change | +7.2% (2023) |

| Gas price | €46/MWh (2024) |

What is included in the product

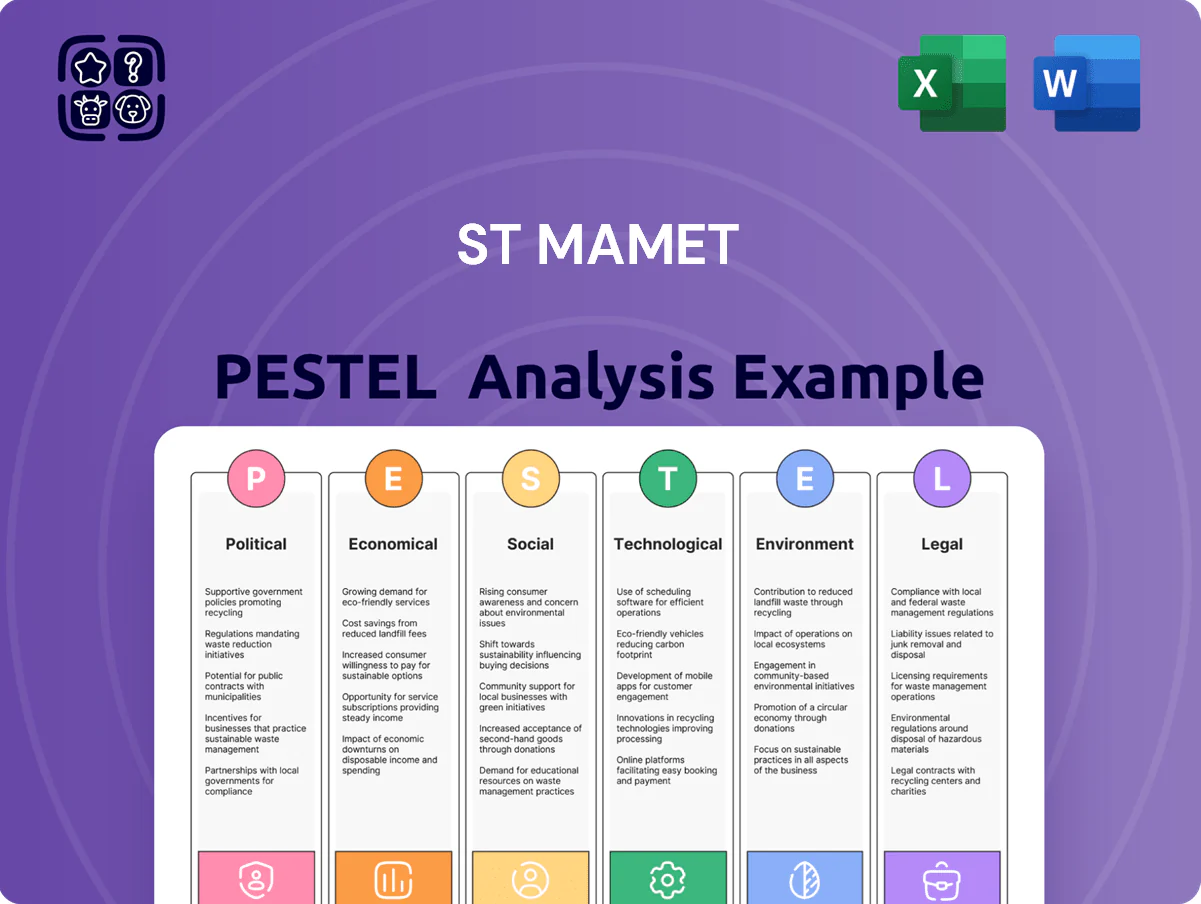

Explores how external macro-environmental factors uniquely affect St Mamet across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend-driven insights to identify threats and opportunities relevant to its region and industry, presented in clean, investor-ready formatting to support strategic planning, funding pitches, and scenario-based decision-making.

Concise, visually segmented PESTLE summary for St Mamet that’s easy to drop into presentations or share across teams, helping streamline risk discussions and strategic alignment during planning sessions.

Economic factors

Inflationary Pressures on Input Costs

Persistent inflation in raw fruit, can-grade steel and refined sugar has pressured margins through late 2025; global sugar prices rose ~18% YoY in 2024 and LME steel coil indices climbed ~22% in 2024–2025, while fruit costs in France increased ~12% since 2023.

Consumer Purchasing Power in France

Labor Market Dynamics and Wage Growth

Rising labor costs in French manufacturing—wages up ~6% 2021–2024 with average hourly manufacturing pay ≈€17.5 in 2024—push St Mamet to invest in automation (CAPEX +12% forecast) to protect margins. Gard’s seasonal fruit processing relies on ~4,000–6,000 temporary workers regionally during peak months, making availability a key constraint. Competitive wages and benefits (seasonal pay premiums ~15–25%) increase unit labor cost and overall cost structure.

Retail Sector Consolidation

The concentration of French retail power—Carrefour and E. Leclerc together account for roughly 35–40% of grocery market share in 2024—exerts strong downward price pressure on suppliers, squeezing St Mamet’s margins and forcing tougher negotiations for shelf space.

Growth of hard discounters (Lidl/ALDI grew ~6–8% in 2024) and private-label expansion demand agile commercial strategies from St Mamet to protect pricing power and secure distribution.

- Carrefour + Leclerc market share ~35–40% (2024)

- Hard discounters growth ~6–8% (2024)

- Margin compression from retailer bargaining power

- Need for agile commercial/pricing strategies to retain shelf space

Interest Rates and Capital Investment

The prevailing interest rate environment affects St Mamet’s cost of borrowing for industrial upgrades and R&D; France’s ECB-driven rate at ~3.75% (2025 average) raises financing costs for capex projects estimated at €20–40m over 2024–2026 to modernize lines and boost yield.

High rates can delay technological adoption or entry into new product categories, potentially reducing planned expansion capex by 15–25% and slowing ROI timelines from 4 to 6 years.

Rising input costs, retailer pressure and rates squeeze margins and capex plans

Inflation in inputs (sugar +18% YoY 2024; steel +22% 2024–25; fruit +12% since 2023) and wage rises (~6% 2021–24; avg €17.5/hr in 2024) compress margins; retailer concentration (Carrefour+Leclerc 35–40%) and discounter growth (Lidl/ALDI +6–8% 2024) force price/placement concessions; ECB rate ~3.75% (2025) raises capex cost for €20–40m modernization, risking 15–25% capex cuts and ROI delays to 4–6 years.

| Metric | Value |

|---|---|

| Sugar price change (2024) | +18% YoY |

| Steel indices (2024–25) | +22% |

| Fruit cost (France) | +12% since 2023 |

| Avg manuf. wage (2024) | €17.5/hr (+6% 2021–24) |

| Retail share: Carrefour+Leclerc (2024) | 35–40% |

| Discounters growth (2024) | +6–8% |

| ECB rate (2025) | ~3.75% |

| Planned capex (2024–26) | €20–40m |

| Potential capex cut / ROI delay | 15–25% / 4–6 yrs |

Preview Before You Purchase

St Mamet PESTLE Analysis

The preview shown here is the exact St Mamet PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and analysis visible are identical to the downloadable file, with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political, economic, social, technological, legal, and environmental forces are shaping St Mamet’s trajectory—our concise PESTLE highlights key risks and opportunities to inform smarter strategy and investment decisions; purchase the full analysis for the complete, editable report and actionable insights you can use immediately.

Political factors

Agricultural Sovereignty Policies

The French government has strengthened food sovereignty measures, aiming to cut non-EU fruit imports by 20% by 2027, creating access for St Mamet to regional subsidies and CAP top-ups targeted at domestic processing in Occitanie.

Policy programs earmark roughly EUR 120m (2024–25) for local fruit sector resilience, improving grant and investment credits that can offset operating costs at St Mamet’s French plants.

National initiatives prioritize supply-chain resilience—buffer stock schemes and logistics grants—reducing disruption risk for St Mamet amid rising global volatility and supporting continued domestic production.

EU Common Agricultural Policy Reforms

Ongoing CAP reforms (2023–2027) shift EUR 58 billion in annual EU subsidies toward eco-schemes and conditional payments, altering incentives for St Mamet’s French fruit suppliers and potentially raising raw material costs by 5–12% due to compliance investments. Emphasis on sustainable land use and the Green Deal’s Farm to Fork targets may tighten supply as farmers reallocate acreage, forcing St Mamet to manage procurement complexity and secure compliant contracts to maintain continuity.

Trade Relations and Import Tariffs

Changes to EU trade deals with major fruit exporters like Morocco and Chile shift supply costs for processed fruit; EU imports of canned fruit rose 7.2% in 2023, affecting margins for players such as St Mamet.

Protective tariffs on canned goods, e.g., recent anti-dumping duties averaging 8–12% on some non-EU producers, can make imports pricier and benefit domestic brands like St Mamet.

Trade tensions raise input costs: in 2024 tariffs and logistics disruptions increased machinery and specialized ingredient prices by an estimated 4–6% for Eurozone food processors.

Government Support for Industrial Decarbonization

Political pressure to meet 2030 and 2050 climate targets has unlocked state-funded grants—EU IPCEI and France Relance—covering up to 40% of CAPEX for industrial decarbonization; St Mamet can apply to programs that awarded €3.5bn to food and agri-industrial projects in 2024–25.

Leveraging these grants can reduce transition CAPEX from electrification/biomass retrofits (estimated €15–25m per plant) by ~€6–10m, improving project IRR and signalling alignment with national emissions-reduction goals.

Public funding and compliance improve long-term operational viability, lower regulatory risk, and bolster PR—70% of EU consumers in 2024 favored brands with verified net-zero commitments, enhancing market access.

- Grants cover up to 40% of CAPEX

- €3.5bn allocated to related projects (2024–25)

- Estimated plant CAPEX €15–25m; potential grant €6–10m

- 70% of EU consumers favor net-zero brands (2024)

Geopolitical Stability and Energy Security

European geopolitical tensions keep energy prices volatile; wholesale natural gas averaged about €46/MWh in 2024, up ~18% vs 2023, directly raising pasteurization and canning energy costs at Vauvert and Nîmes.

French policy shifts—accelerated nuclear life‑extension and renewables targets—will alter long‑term tariffs, while infrastructure decisions (e.g., LNG terminals) affect short‑term supply security and logistics costs.

Management must track EU‑Russia relations, Mediterranean pipeline developments, and 2024–25 gas storage levels (France ~70–90% seasonal range) to forecast spikes in processing and transport expenses.

- 2024 avg gas €46/MWh; +18% YoY

- Nuclear/renewables policy affects tariff trajectory

- LNG/infrastructure changes impact short‑term supply

- Monitor Russia/EU relations and gas storage (70–90%)

France boosts food‑sovereignty support amid rising CAP costs, imports and gas‑driven margins

Stronger French food‑sovereignty rules and EUR 120m (2024–25) programmes favor domestic processors; CAP reforms (EUR 58bn/yr) and eco‑schemes may raise supplier costs 5–12%; anti‑dumping duties (8–12%) and 7.2% rise in EU canned‑fruit imports (2023) shift margins; €3.5bn grants (2024–25) cover up to 40% CAPEX; 2024 gas €46/MWh (+18% YoY) pressures processing costs.

| Indicator | Value |

|---|---|

| France programme | €120m (2024–25) |

| CAP budget | €58bn/yr |

| Import change | +7.2% (2023) |

| Gas price | €46/MWh (2024) |

What is included in the product

Explores how external macro-environmental factors uniquely affect St Mamet across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each backed by current data and trend-driven insights to identify threats and opportunities relevant to its region and industry, presented in clean, investor-ready formatting to support strategic planning, funding pitches, and scenario-based decision-making.

Concise, visually segmented PESTLE summary for St Mamet that’s easy to drop into presentations or share across teams, helping streamline risk discussions and strategic alignment during planning sessions.

Economic factors

Inflationary Pressures on Input Costs

Persistent inflation in raw fruit, can-grade steel and refined sugar has pressured margins through late 2025; global sugar prices rose ~18% YoY in 2024 and LME steel coil indices climbed ~22% in 2024–2025, while fruit costs in France increased ~12% since 2023.

Consumer Purchasing Power in France

Labor Market Dynamics and Wage Growth

Rising labor costs in French manufacturing—wages up ~6% 2021–2024 with average hourly manufacturing pay ≈€17.5 in 2024—push St Mamet to invest in automation (CAPEX +12% forecast) to protect margins. Gard’s seasonal fruit processing relies on ~4,000–6,000 temporary workers regionally during peak months, making availability a key constraint. Competitive wages and benefits (seasonal pay premiums ~15–25%) increase unit labor cost and overall cost structure.

Retail Sector Consolidation

The concentration of French retail power—Carrefour and E. Leclerc together account for roughly 35–40% of grocery market share in 2024—exerts strong downward price pressure on suppliers, squeezing St Mamet’s margins and forcing tougher negotiations for shelf space.

Growth of hard discounters (Lidl/ALDI grew ~6–8% in 2024) and private-label expansion demand agile commercial strategies from St Mamet to protect pricing power and secure distribution.

- Carrefour + Leclerc market share ~35–40% (2024)

- Hard discounters growth ~6–8% (2024)

- Margin compression from retailer bargaining power

- Need for agile commercial/pricing strategies to retain shelf space

Interest Rates and Capital Investment

The prevailing interest rate environment affects St Mamet’s cost of borrowing for industrial upgrades and R&D; France’s ECB-driven rate at ~3.75% (2025 average) raises financing costs for capex projects estimated at €20–40m over 2024–2026 to modernize lines and boost yield.

High rates can delay technological adoption or entry into new product categories, potentially reducing planned expansion capex by 15–25% and slowing ROI timelines from 4 to 6 years.

Rising input costs, retailer pressure and rates squeeze margins and capex plans

Inflation in inputs (sugar +18% YoY 2024; steel +22% 2024–25; fruit +12% since 2023) and wage rises (~6% 2021–24; avg €17.5/hr in 2024) compress margins; retailer concentration (Carrefour+Leclerc 35–40%) and discounter growth (Lidl/ALDI +6–8% 2024) force price/placement concessions; ECB rate ~3.75% (2025) raises capex cost for €20–40m modernization, risking 15–25% capex cuts and ROI delays to 4–6 years.

| Metric | Value |

|---|---|

| Sugar price change (2024) | +18% YoY |

| Steel indices (2024–25) | +22% |

| Fruit cost (France) | +12% since 2023 |

| Avg manuf. wage (2024) | €17.5/hr (+6% 2021–24) |

| Retail share: Carrefour+Leclerc (2024) | 35–40% |

| Discounters growth (2024) | +6–8% |

| ECB rate (2025) | ~3.75% |

| Planned capex (2024–26) | €20–40m |

| Potential capex cut / ROI delay | 15–25% / 4–6 yrs |

Preview Before You Purchase

St Mamet PESTLE Analysis

The preview shown here is the exact St Mamet PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use; the layout, content, and analysis visible are identical to the downloadable file, with no placeholders or surprises.