Saltchuk Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

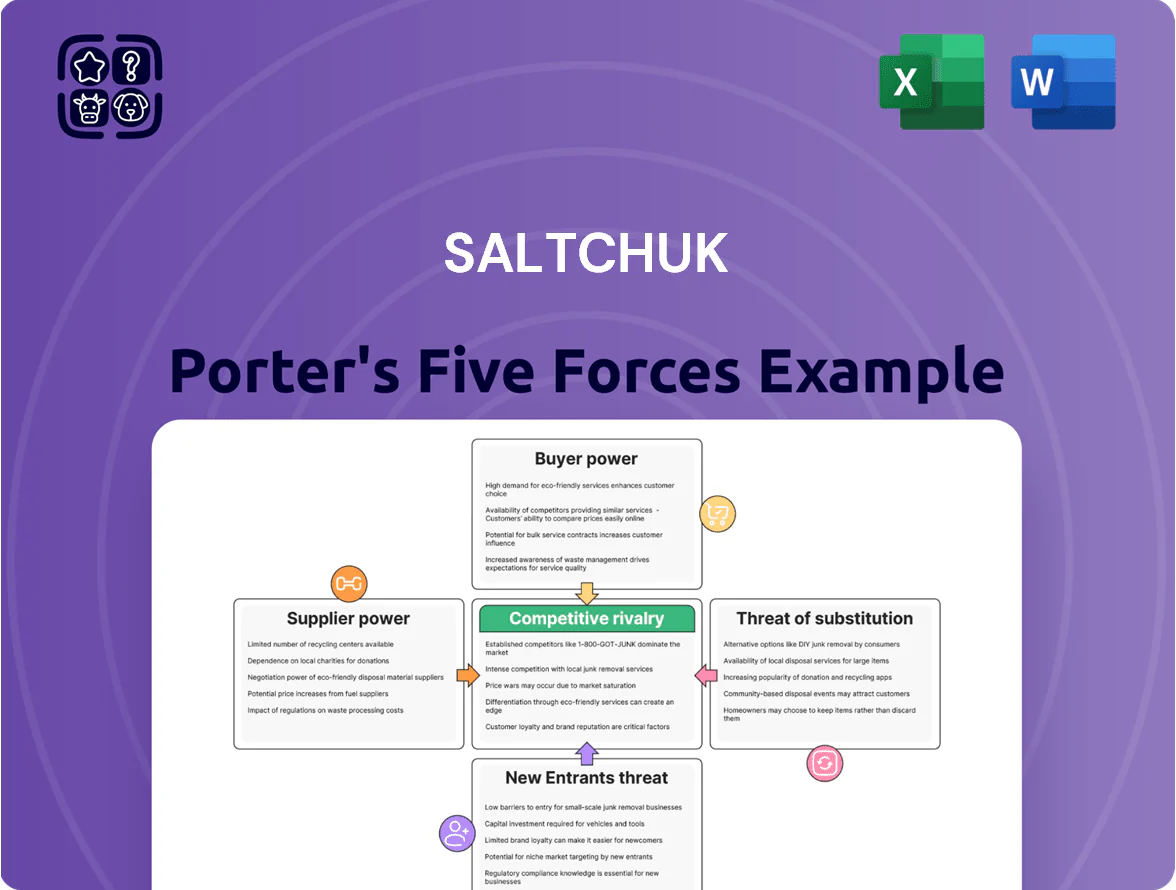

Saltchuk faces moderate competitive rivalry, niche scale advantages, and rising regulatory and labor pressures that shape its margins and growth prospects; suppliers and buyers exert uneven influence across its diversified transport and logistics businesses.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Saltchuk’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized vessel manufacturers

Saltchuk depends on a handful of global shipyards able to build Jones Act vessels, shrinking supplier options and giving builders pricing leverage; only about 5–7 U.S.-compliant yards handle large RoRo/tanker work.

Jones Act legal limits and technical specs raise costs; recent bids for Jones Act tankers showed premiums of 15–25% versus international yards.

Need for 2026 emissions upgrades (IMO-aligned US rules) heightens urgency and bargaining power, with retrofit budgets per vessel often $5–20m, concentrating supplier influence.

Volatility in fuel and energy procurement

Saltchuk, a major shipping and aviation operator, is highly exposed to oil refinery and energy producer pricing; crude price swings (Brent rose ~45% in 2023 and averaged $82/bbl in 2024) force Saltchuk into price-taking positions despite owning NorthStar Energy.

NorthStar mitigates procurement risk via bulk contracts and storage, but global spot volatility still drives fuel cost variance that compressed margins—fuel accounted for ~18–22% of operating costs across logistics units in 2024.

Even a $10/bbl Brent move changes annual fuel spend by roughly $25–40 million for Saltchuk’s fleet and aviation ops, so supplier bargaining power remains high and directly pressures subsidiary EBITDA.

Limited availability of skilled maritime and aviation labor

The pool of certified mariners and FAA-certified aviation mechanics is shrinking—US Merchant Marine officers aged 55+ rose to 38% in 2023 and A&P mechanics retirements pushed vacancy rates above 12% in 2024—tight supply raises hiring and training costs for Saltchuk.

Strong maritime and transport unions (eg, Sailors Union, AMFA) press wages and benefits; 2024 contract settlements averaged 4.5–6% annual wage gains, giving suppliers leverage.

Negotiating long, complex labor contracts forces Saltchuk to absorb higher labor expense and pension liabilities; a 5% wage uptick can add roughly 3–5% to operating margins on services with heavy labor content.

Technological dependence on specialized software providers

Modern logistics rely on specialized fleet-management and visibility software dominated by a few firms (e.g., Oracle, Trimble, FourKites), concentrating supplier power as 60–70% of global shippers use top-tier platforms.

High switching costs—implementation often >$2m plus 6–12 months uptime risk—boost vendor leverage at renewals and pricing talks.

As Saltchuk adds AI analytics by 2026, dependency rises: AI module spend can be 15–25% of total tech OPEX, strengthening suppliers’ bargaining position.

- Dominant vendors: 60–70% market share

- Switch cost: >$2m, 6–12 months

- AI spend: 15–25% of tech OPEX

Infrastructure constraints at port and terminal facilities

Saltchuk’s maritime ops rely on port berths and terminals run by govts or landlords; limited berths and rising fees (US West Coast container fees up ~12% in 2024) cut Saltchuk’s negotiating room.

Owning terminals (e.g., 2023 CAPEX toward terminal assets) reduces exposure, but external infrastructure—peak berth occupancy >85% at key hubs—remains a binding bottleneck.

- Dependency: govt/private terminal control

- Constraint: berth scarcity, fees rising ~12% (2024)

- Mitigation: targeted terminal ownership CAPEX

- Residual risk: peak occupancy >85%

Supplier squeeze: US yards, fuel swings, labor + tech lock-in drive rising vessel costs

Suppliers hold high power: constrained US Jones Act shipyards (5–7 yards), 15–25% build premium, $5–20m retrofit needs; fuel volatility (Brent avg $82/bbl in 2024) shifts $25–40m/yr per $10/bbl; labor shortages (38% mariners 55+ in 2023) and 4.5–6% wage settlements raise costs; software vendor dominance (60–70% market share) with >$2m switch costs locks tech pricing.

| Metric | Value |

|---|---|

| US yards | 5–7 |

| Build premium | 15–25% |

| Retrofit cost | $5–20m/vessel |

| Brent 2024 | $82/bbl |

| Fuel sensitivity | $25–40m per $10 |

| Mariners 55+ | 38% (2023) |

| Vendor share | 60–70% |

What is included in the product

Tailored Porter's Five Forces analysis for Saltchuk that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies emerging disruptions and strategic levers to protect and grow market share.

A concise Porter's Five Forces one-sheet for Saltchuk that highlights competitive pressures and relief points—ideal for fast strategic decisions and boardroom briefings.

Customers Bargaining Power

Concentration of large-scale industrial clients

Low switching costs in standardized freight markets

In regional corridors with 3–6 active carriers, customers easily switch cargo by price or schedule; industry surveys show 42% of shippers switched providers in 2024 for lower rates or faster transit. Saltchuk stresses reliability, but commoditized legs (drayage, short-sea) make buyers sensitive to even 2–4% rate hikes. That dynamic forces Saltchuk to drive down unit costs—example: target operating margin pressure of ~100–200 bps—to stay competitive.

Governmental and military procurement influence

Saltchuk regularly serves US federal, state, and military clients that operate on tight budgets and formal bidding rules; federal contracting for maritime services totaled about $7.4bn in 2024, concentrating negotiating power with institutional buyers. These clients can set strict contract terms and demand transparency, compliance with FAR (Federal Acquisition Regulation), and audited reporting. Competitive bids—over 60% of government maritime contracts in 2024 were competitively awarded—limit Saltchuk’s ability to pass cost increases to these buyers. Contract size and renewal rates hinge on demonstrated cost control, safety, and regulatory compliance.

Availability of real-time price transparency

The rise of digital freight marketplaces lets customers compare rates and service levels instantly, eroding Saltchuk’s pricing power as buyers shop multiple carriers in seconds.

Real-time market data enables aggressive negotiation: customers use live spot rates and tender acceptance metrics to push Saltchuk on price and capacity terms.

By 2025, predictive pricing tools used by shippers—adopted by ~60% of large shippers per 2024 industry surveys—have shifted the information advantage to buyers.

- Instant rate comparison lowers transaction costs

- Live spot/tender data fuels tougher negotiations

- ~60% large shippers using predictive pricing (2024)

- Price transparency compresses Saltchuk margins

Vertical integration of large retailers

- Walmart 2024 transport spend: $14.4B

- Amazon logistics capex 2023–24: ~$40B

- Defensive play: niche services + long-term contracts

Concentrated Buyers, Predictive Pricing Squeeze Saltchuk Margins 100–200 bps

| Metric | 2024 |

|---|---|

| Share of operating income from large contracts | ~55% |

| Aloha cargo revenue from top accounts | ~40% |

| Large shippers using predictive pricing | ~60% |

| Federal maritime contracting (US) | $7.4bn |

| Margin pressure | ~100–200 bps |

Preview the Actual Deliverable

Saltchuk Porter's Five Forces Analysis

This preview shows the exact Saltchuk Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for download.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Saltchuk faces moderate competitive rivalry, niche scale advantages, and rising regulatory and labor pressures that shape its margins and growth prospects; suppliers and buyers exert uneven influence across its diversified transport and logistics businesses.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Saltchuk’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of specialized vessel manufacturers

Saltchuk depends on a handful of global shipyards able to build Jones Act vessels, shrinking supplier options and giving builders pricing leverage; only about 5–7 U.S.-compliant yards handle large RoRo/tanker work.

Jones Act legal limits and technical specs raise costs; recent bids for Jones Act tankers showed premiums of 15–25% versus international yards.

Need for 2026 emissions upgrades (IMO-aligned US rules) heightens urgency and bargaining power, with retrofit budgets per vessel often $5–20m, concentrating supplier influence.

Volatility in fuel and energy procurement

Saltchuk, a major shipping and aviation operator, is highly exposed to oil refinery and energy producer pricing; crude price swings (Brent rose ~45% in 2023 and averaged $82/bbl in 2024) force Saltchuk into price-taking positions despite owning NorthStar Energy.

NorthStar mitigates procurement risk via bulk contracts and storage, but global spot volatility still drives fuel cost variance that compressed margins—fuel accounted for ~18–22% of operating costs across logistics units in 2024.

Even a $10/bbl Brent move changes annual fuel spend by roughly $25–40 million for Saltchuk’s fleet and aviation ops, so supplier bargaining power remains high and directly pressures subsidiary EBITDA.

Limited availability of skilled maritime and aviation labor

The pool of certified mariners and FAA-certified aviation mechanics is shrinking—US Merchant Marine officers aged 55+ rose to 38% in 2023 and A&P mechanics retirements pushed vacancy rates above 12% in 2024—tight supply raises hiring and training costs for Saltchuk.

Strong maritime and transport unions (eg, Sailors Union, AMFA) press wages and benefits; 2024 contract settlements averaged 4.5–6% annual wage gains, giving suppliers leverage.

Negotiating long, complex labor contracts forces Saltchuk to absorb higher labor expense and pension liabilities; a 5% wage uptick can add roughly 3–5% to operating margins on services with heavy labor content.

Technological dependence on specialized software providers

Modern logistics rely on specialized fleet-management and visibility software dominated by a few firms (e.g., Oracle, Trimble, FourKites), concentrating supplier power as 60–70% of global shippers use top-tier platforms.

High switching costs—implementation often >$2m plus 6–12 months uptime risk—boost vendor leverage at renewals and pricing talks.

As Saltchuk adds AI analytics by 2026, dependency rises: AI module spend can be 15–25% of total tech OPEX, strengthening suppliers’ bargaining position.

- Dominant vendors: 60–70% market share

- Switch cost: >$2m, 6–12 months

- AI spend: 15–25% of tech OPEX

Infrastructure constraints at port and terminal facilities

Saltchuk’s maritime ops rely on port berths and terminals run by govts or landlords; limited berths and rising fees (US West Coast container fees up ~12% in 2024) cut Saltchuk’s negotiating room.

Owning terminals (e.g., 2023 CAPEX toward terminal assets) reduces exposure, but external infrastructure—peak berth occupancy >85% at key hubs—remains a binding bottleneck.

- Dependency: govt/private terminal control

- Constraint: berth scarcity, fees rising ~12% (2024)

- Mitigation: targeted terminal ownership CAPEX

- Residual risk: peak occupancy >85%

Supplier squeeze: US yards, fuel swings, labor + tech lock-in drive rising vessel costs

Suppliers hold high power: constrained US Jones Act shipyards (5–7 yards), 15–25% build premium, $5–20m retrofit needs; fuel volatility (Brent avg $82/bbl in 2024) shifts $25–40m/yr per $10/bbl; labor shortages (38% mariners 55+ in 2023) and 4.5–6% wage settlements raise costs; software vendor dominance (60–70% market share) with >$2m switch costs locks tech pricing.

| Metric | Value |

|---|---|

| US yards | 5–7 |

| Build premium | 15–25% |

| Retrofit cost | $5–20m/vessel |

| Brent 2024 | $82/bbl |

| Fuel sensitivity | $25–40m per $10 |

| Mariners 55+ | 38% (2023) |

| Vendor share | 60–70% |

What is included in the product

Tailored Porter's Five Forces analysis for Saltchuk that uncovers competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and identifies emerging disruptions and strategic levers to protect and grow market share.

A concise Porter's Five Forces one-sheet for Saltchuk that highlights competitive pressures and relief points—ideal for fast strategic decisions and boardroom briefings.

Customers Bargaining Power

Concentration of large-scale industrial clients

Low switching costs in standardized freight markets

In regional corridors with 3–6 active carriers, customers easily switch cargo by price or schedule; industry surveys show 42% of shippers switched providers in 2024 for lower rates or faster transit. Saltchuk stresses reliability, but commoditized legs (drayage, short-sea) make buyers sensitive to even 2–4% rate hikes. That dynamic forces Saltchuk to drive down unit costs—example: target operating margin pressure of ~100–200 bps—to stay competitive.

Governmental and military procurement influence

Saltchuk regularly serves US federal, state, and military clients that operate on tight budgets and formal bidding rules; federal contracting for maritime services totaled about $7.4bn in 2024, concentrating negotiating power with institutional buyers. These clients can set strict contract terms and demand transparency, compliance with FAR (Federal Acquisition Regulation), and audited reporting. Competitive bids—over 60% of government maritime contracts in 2024 were competitively awarded—limit Saltchuk’s ability to pass cost increases to these buyers. Contract size and renewal rates hinge on demonstrated cost control, safety, and regulatory compliance.

Availability of real-time price transparency

The rise of digital freight marketplaces lets customers compare rates and service levels instantly, eroding Saltchuk’s pricing power as buyers shop multiple carriers in seconds.

Real-time market data enables aggressive negotiation: customers use live spot rates and tender acceptance metrics to push Saltchuk on price and capacity terms.

By 2025, predictive pricing tools used by shippers—adopted by ~60% of large shippers per 2024 industry surveys—have shifted the information advantage to buyers.

- Instant rate comparison lowers transaction costs

- Live spot/tender data fuels tougher negotiations

- ~60% large shippers using predictive pricing (2024)

- Price transparency compresses Saltchuk margins

Vertical integration of large retailers

- Walmart 2024 transport spend: $14.4B

- Amazon logistics capex 2023–24: ~$40B

- Defensive play: niche services + long-term contracts

Concentrated Buyers, Predictive Pricing Squeeze Saltchuk Margins 100–200 bps

| Metric | 2024 |

|---|---|

| Share of operating income from large contracts | ~55% |

| Aloha cargo revenue from top accounts | ~40% |

| Large shippers using predictive pricing | ~60% |

| Federal maritime contracting (US) | $7.4bn |

| Margin pressure | ~100–200 bps |

Preview the Actual Deliverable

Saltchuk Porter's Five Forces Analysis

This preview shows the exact Saltchuk Porter’s Five Forces analysis you’ll receive immediately after purchase—no mockups, no placeholders, fully formatted and ready for download.