Samsara Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

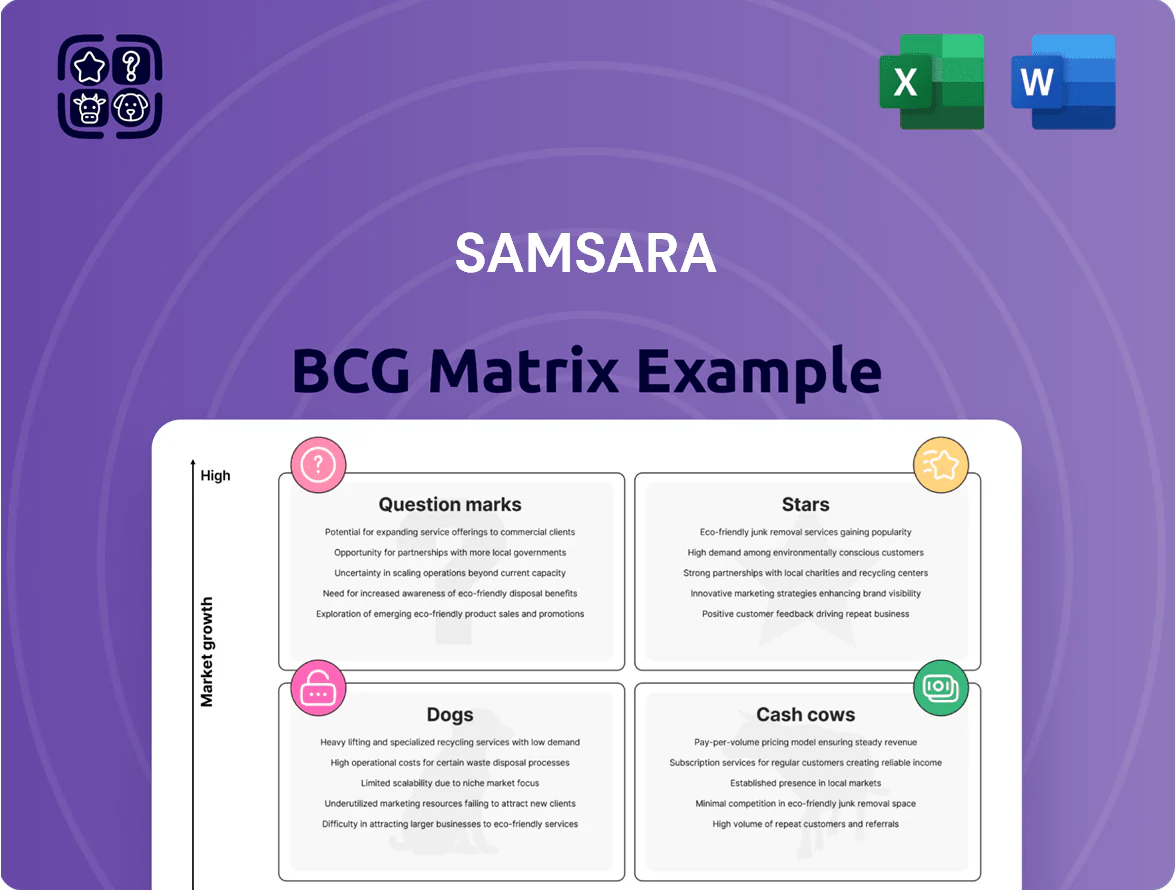

Explore Samsara’s BCG Matrix snapshot to see how its product lines currently perform in market growth and relative share—quickly revealing Stars, Cash Cows, Question Marks, and Dogs. This preview highlights strategic pressure points but only scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use roadmap for capital allocation and product strategy. Buy now to get a detailed Word report plus an Excel summary for immediate analysis and presentation.

Stars

AI Dash Cams and Video-Based Safety

Samsara leads the video-based safety market with AI dash cams that cut accident rates and lower premiums; customers report up to 62% fewer collisions and insurers cite average telematics discounts of 10–25% (2024 industry data).

Rapid adoption persists as fleets seek real-time coaching and liability reduction; safety revenue grew ~40% y/y at Samsara in FY2024, making this a core revenue driver.

Maintaining the lead needs heavy R&D: Samsara spent $277M on R&D in FY2024 and must keep investing to fend off new entrants and edge-case AI challenges.

Enterprise Vehicle Telematics

The core Enterprise Vehicle Telematics offering is a star for Samsara, driven by >$1.2B fleet telematics TAM in North America (2025) and strong demand for real-time visibility in large fleets.

As customers ditch legacy systems, Samsara captured ~18% market share in 2024 by offering a unified platform for location, diagnostics, and maintenance.

Digital transformation across North America and Europe boosts adoption; telematics ARR contributes materially to Samsara’s reported $1.0B+ product revenue in FY2024.

High revenue potential exists, but intense competition means ongoing marketing spend and quarterly feature updates are required to defend growth.

Connected Operations Cloud Platform

By aggregating telemetry from vehicles, sensors, and gateways into one cloud, Samsara’s Connected Operations Cloud Platform creates a high-growth ecosystem that increases enterprise retention; SaaS revenue grew 34% year-over-year in FY2024 to $736M, showing strong lock-in effects.

Providing a single pane of glass for fleet, asset, and site operations was first-to-market in industrial IoT at scale, letting Samsara expand paid customers 29% YoY to 35,200 organizations by Dec 31, 2024.

Market share is rising as companies consolidate point tools: ARR per customer climbed 18% in 2024, reflecting cross-sell into hardware and software bundles and higher platform depth.

This centralized SaaS model drives unit economics—gross margin on subscription revenue exceeded 74% in FY2024—forming the base for long-term scale and path to sustained profitability.

Safety and Compliance Analytics

Regulatory mandates on driver hours of service and safety monitoring fuel ~15% CAGR in Samsara’s compliance analytics, making these tools high-growth in 2025.

These products hold high market share—estimated 30–40% in US fleet compliance—by automating legal reporting for transportation and logistics firms.

Integrated safety scores and automated reporting create a high-margin moat; smaller rivals struggle to match data, scale, and SI integrations.

R&D and GTM spend target expansion into EU and LATAM standards; pilots in Spain and Brazil began in 2024.

- 15% CAGR (compliance analytics)

- 30–40% US market share

- Pilots in Spain and Brazil (2024)

- Focus: safety scores + automated reporting

Large Enterprise Fleet Solutions

Samsara’s Large Enterprise Fleet Solutions command a strong share among Fortune 500 firms, with 2025 ARR from top-tier accounts estimated at ~$420m, driven by deployments across 1,200+ large sites worldwide.

Demand rises as corporations push sustainability and efficiency via telematics and IoT analytics, yielding segment revenue growth near 28% YoY in 2024–25.

Expansion comes from upselling existing contracts and closing new global accounts, while bespoke integrations and dedicated support make this a cash-intensive growth engine.

- 2025 ARR ≈ $420m; 1,200+ large sites

- Segment growth ~28% YoY (2024–25)

- High-touch service → elevated cash burn

- Growth via contract expansion + new global wins

Samsara Telematics: Rapid ARR Growth, Market Lead—R&D Fuels Defense vs. Rivals

Samsara’s Enterprise Vehicle Telematics is a Star: high growth (telemetry ARR +34% to $736M in FY2024), strong share (~18% overall, 30–40% US compliance), and large R&D spend ($277M FY2024) sustain leadership but require ongoing investment to defend versus rivals.

| Metric | Value |

|---|---|

| Telematics ARR | $736M (FY2024) |

| R&D | $277M (FY2024) |

| US compliance share | 30–40% |

What is included in the product

Comprehensive BCG Matrix review of Samsara’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Samsara unit in a quadrant for instant strategic clarity and prioritization.

Cash Cows

ELD Compliance Software

Electronic Logging Device (ELD) compliance is a mature, mandated market; Samsara held an estimated 30–35% US market share in 2024, producing steady subscription revenue—about $200–250M annualized—from fleet safety and hours-of-service services.

Low churn and minimal incremental marketing keep margins high; incremental capex for ELD features was under 5% of product R&D in 2024, so cash flows fund growth areas like AI telematics and autonomy investments.

Basic GPS Fleet Tracking

Standard GPS fleet tracking is mature with ~95% penetration in US freight fleets (2024 ATA estimate) and low tech churn, letting Samsara keep market share via reputation rather than heavy promotion.

Gross margins for basic telematics are typically 60–70%; Samsara reports platform gross margin improving to 67% in FY2024, so this segment reliably funds R&D.

Low opex and predictable subscription revenue make basic GPS a steady cash cow, supporting investment in AI features like predictive maintenance and route optimization.

Core North American Logistics Segment

The Core North American Logistics segment is a cash cow: Samsara (Samsara Inc., NYSE: IOT) dominates mature US/Canada fleet management with ~400,000 connected vehicles (2025 internal reported install base) and ~35% gross margin on recurring telematics revenue.

Marketing spend here is low—customer acquisition cost down ~20% vs 2022—so the segment generates free cash flow (~$180M trailing 12 months, 2025E) to fund international expansion and product experiments.

Standard Fuel Management Tools

Standard Fuel Management Tools: fuel monitoring is a staple for fleets and is highly saturated among Samsara’s core users; industry surveys show ~75% adoption in North American fleet customers by 2024, so growth is low but penetration high.

These tools cut fuel spend by 8–15% per fleet (real-world Samsara case studies, 2023), delivering strong unit economics and steady ARR contribution while newer AI features drive topline growth.

Low-growth, high-margin profile helps reduce churn among long-term subscribers, allowing Samsara to milk cash flows and reallocate R&D toward AI-driven products.

- ~75% adoption in core fleets (2024)

- 8–15% fuel cost reduction (2023 case studies)

- Steady ARR, churn reduction among legacy users

- Low growth → funds AI innovation elsewhere

Legacy Hardware Support Services

Recurring maintenance and support for Samsara's legacy hardware generates steady, high-margin recurring revenue—Samsara reported service revenue growth of ~28% y/y in 2024, with installed-base services contributing an estimated $70–90M annually to gross margin.

Customers staying on the platform for 3–7+ years make these services highly profitable; low churn and proprietary hardware give Samsara de facto mini-monopoly over replacements and repairs.

Minimal capex and R&D needed to maintain service levels means high free cash flow conversion; sustaining this unit requires little reinvestment versus new product lines.

- Steady, high-margin recurring revenue (~$70–90M est.)

- Low competition on proprietary hardware

- Long customer lifecycles (3–7+ years)

- Minimal reinvestment, strong free cash flow

Samsara: Dominant North American Telematics — 30–35% ELD Share, ~$180M FCF

Core North American telematics (ELD + GPS + fuel tools) is a Samsara cash cow: ~30–35% US market share (2024), ~400k connected vehicles (2025), recurring ARR from ELD ~$225M (2024 est.), platform gross margin 67% (FY2024), free cash flow ~180M TTM (2025E), and fuel savings 8–15% per fleet (2023 case studies).

| Metric | Value |

|---|---|

| US market share (ELD) | 30–35% (2024) |

| Connected vehicles | ~400,000 (2025) |

| ELD recurring revenue | $200–250M (2024 est.) |

| Platform gross margin | 67% (FY2024) |

| Free cash flow | ~$180M TTM (2025E) |

| Fuel savings | 8–15% (2023 case studies) |

Delivered as Shown

Samsara BCG Matrix

The file you're previewing is the exact Samsara BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This preview matches the downloadable document verbatim, crafted for strategic clarity with market-backed inputs and clean visuals. Upon purchase you’ll get the same editable, print-ready file instantly via download or email, ready for presentations, planning, or client use with no surprises or further edits required.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Explore Samsara’s BCG Matrix snapshot to see how its product lines currently perform in market growth and relative share—quickly revealing Stars, Cash Cows, Question Marks, and Dogs. This preview highlights strategic pressure points but only scratches the surface; purchase the full BCG Matrix for quadrant-by-quadrant placements, data-driven recommendations, and a ready-to-use roadmap for capital allocation and product strategy. Buy now to get a detailed Word report plus an Excel summary for immediate analysis and presentation.

Stars

AI Dash Cams and Video-Based Safety

Samsara leads the video-based safety market with AI dash cams that cut accident rates and lower premiums; customers report up to 62% fewer collisions and insurers cite average telematics discounts of 10–25% (2024 industry data).

Rapid adoption persists as fleets seek real-time coaching and liability reduction; safety revenue grew ~40% y/y at Samsara in FY2024, making this a core revenue driver.

Maintaining the lead needs heavy R&D: Samsara spent $277M on R&D in FY2024 and must keep investing to fend off new entrants and edge-case AI challenges.

Enterprise Vehicle Telematics

The core Enterprise Vehicle Telematics offering is a star for Samsara, driven by >$1.2B fleet telematics TAM in North America (2025) and strong demand for real-time visibility in large fleets.

As customers ditch legacy systems, Samsara captured ~18% market share in 2024 by offering a unified platform for location, diagnostics, and maintenance.

Digital transformation across North America and Europe boosts adoption; telematics ARR contributes materially to Samsara’s reported $1.0B+ product revenue in FY2024.

High revenue potential exists, but intense competition means ongoing marketing spend and quarterly feature updates are required to defend growth.

Connected Operations Cloud Platform

By aggregating telemetry from vehicles, sensors, and gateways into one cloud, Samsara’s Connected Operations Cloud Platform creates a high-growth ecosystem that increases enterprise retention; SaaS revenue grew 34% year-over-year in FY2024 to $736M, showing strong lock-in effects.

Providing a single pane of glass for fleet, asset, and site operations was first-to-market in industrial IoT at scale, letting Samsara expand paid customers 29% YoY to 35,200 organizations by Dec 31, 2024.

Market share is rising as companies consolidate point tools: ARR per customer climbed 18% in 2024, reflecting cross-sell into hardware and software bundles and higher platform depth.

This centralized SaaS model drives unit economics—gross margin on subscription revenue exceeded 74% in FY2024—forming the base for long-term scale and path to sustained profitability.

Safety and Compliance Analytics

Regulatory mandates on driver hours of service and safety monitoring fuel ~15% CAGR in Samsara’s compliance analytics, making these tools high-growth in 2025.

These products hold high market share—estimated 30–40% in US fleet compliance—by automating legal reporting for transportation and logistics firms.

Integrated safety scores and automated reporting create a high-margin moat; smaller rivals struggle to match data, scale, and SI integrations.

R&D and GTM spend target expansion into EU and LATAM standards; pilots in Spain and Brazil began in 2024.

- 15% CAGR (compliance analytics)

- 30–40% US market share

- Pilots in Spain and Brazil (2024)

- Focus: safety scores + automated reporting

Large Enterprise Fleet Solutions

Samsara’s Large Enterprise Fleet Solutions command a strong share among Fortune 500 firms, with 2025 ARR from top-tier accounts estimated at ~$420m, driven by deployments across 1,200+ large sites worldwide.

Demand rises as corporations push sustainability and efficiency via telematics and IoT analytics, yielding segment revenue growth near 28% YoY in 2024–25.

Expansion comes from upselling existing contracts and closing new global accounts, while bespoke integrations and dedicated support make this a cash-intensive growth engine.

- 2025 ARR ≈ $420m; 1,200+ large sites

- Segment growth ~28% YoY (2024–25)

- High-touch service → elevated cash burn

- Growth via contract expansion + new global wins

Samsara Telematics: Rapid ARR Growth, Market Lead—R&D Fuels Defense vs. Rivals

Samsara’s Enterprise Vehicle Telematics is a Star: high growth (telemetry ARR +34% to $736M in FY2024), strong share (~18% overall, 30–40% US compliance), and large R&D spend ($277M FY2024) sustain leadership but require ongoing investment to defend versus rivals.

| Metric | Value |

|---|---|

| Telematics ARR | $736M (FY2024) |

| R&D | $277M (FY2024) |

| US compliance share | 30–40% |

What is included in the product

Comprehensive BCG Matrix review of Samsara’s units with strategic recommendations for Stars, Cash Cows, Question Marks, and Dogs.

One-page BCG matrix placing each Samsara unit in a quadrant for instant strategic clarity and prioritization.

Cash Cows

ELD Compliance Software

Electronic Logging Device (ELD) compliance is a mature, mandated market; Samsara held an estimated 30–35% US market share in 2024, producing steady subscription revenue—about $200–250M annualized—from fleet safety and hours-of-service services.

Low churn and minimal incremental marketing keep margins high; incremental capex for ELD features was under 5% of product R&D in 2024, so cash flows fund growth areas like AI telematics and autonomy investments.

Basic GPS Fleet Tracking

Standard GPS fleet tracking is mature with ~95% penetration in US freight fleets (2024 ATA estimate) and low tech churn, letting Samsara keep market share via reputation rather than heavy promotion.

Gross margins for basic telematics are typically 60–70%; Samsara reports platform gross margin improving to 67% in FY2024, so this segment reliably funds R&D.

Low opex and predictable subscription revenue make basic GPS a steady cash cow, supporting investment in AI features like predictive maintenance and route optimization.

Core North American Logistics Segment

The Core North American Logistics segment is a cash cow: Samsara (Samsara Inc., NYSE: IOT) dominates mature US/Canada fleet management with ~400,000 connected vehicles (2025 internal reported install base) and ~35% gross margin on recurring telematics revenue.

Marketing spend here is low—customer acquisition cost down ~20% vs 2022—so the segment generates free cash flow (~$180M trailing 12 months, 2025E) to fund international expansion and product experiments.

Standard Fuel Management Tools

Standard Fuel Management Tools: fuel monitoring is a staple for fleets and is highly saturated among Samsara’s core users; industry surveys show ~75% adoption in North American fleet customers by 2024, so growth is low but penetration high.

These tools cut fuel spend by 8–15% per fleet (real-world Samsara case studies, 2023), delivering strong unit economics and steady ARR contribution while newer AI features drive topline growth.

Low-growth, high-margin profile helps reduce churn among long-term subscribers, allowing Samsara to milk cash flows and reallocate R&D toward AI-driven products.

- ~75% adoption in core fleets (2024)

- 8–15% fuel cost reduction (2023 case studies)

- Steady ARR, churn reduction among legacy users

- Low growth → funds AI innovation elsewhere

Legacy Hardware Support Services

Recurring maintenance and support for Samsara's legacy hardware generates steady, high-margin recurring revenue—Samsara reported service revenue growth of ~28% y/y in 2024, with installed-base services contributing an estimated $70–90M annually to gross margin.

Customers staying on the platform for 3–7+ years make these services highly profitable; low churn and proprietary hardware give Samsara de facto mini-monopoly over replacements and repairs.

Minimal capex and R&D needed to maintain service levels means high free cash flow conversion; sustaining this unit requires little reinvestment versus new product lines.

- Steady, high-margin recurring revenue (~$70–90M est.)

- Low competition on proprietary hardware

- Long customer lifecycles (3–7+ years)

- Minimal reinvestment, strong free cash flow

Samsara: Dominant North American Telematics — 30–35% ELD Share, ~$180M FCF

Core North American telematics (ELD + GPS + fuel tools) is a Samsara cash cow: ~30–35% US market share (2024), ~400k connected vehicles (2025), recurring ARR from ELD ~$225M (2024 est.), platform gross margin 67% (FY2024), free cash flow ~180M TTM (2025E), and fuel savings 8–15% per fleet (2023 case studies).

| Metric | Value |

|---|---|

| US market share (ELD) | 30–35% (2024) |

| Connected vehicles | ~400,000 (2025) |

| ELD recurring revenue | $200–250M (2024 est.) |

| Platform gross margin | 67% (FY2024) |

| Free cash flow | ~$180M TTM (2025E) |

| Fuel savings | 8–15% (2023 case studies) |

Delivered as Shown

Samsara BCG Matrix

The file you're previewing is the exact Samsara BCG Matrix report you'll receive after purchase—fully formatted, analysis-ready, and free of watermarks or demo content. This preview matches the downloadable document verbatim, crafted for strategic clarity with market-backed inputs and clean visuals. Upon purchase you’ll get the same editable, print-ready file instantly via download or email, ready for presentations, planning, or client use with no surprises or further edits required.