Samsara Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

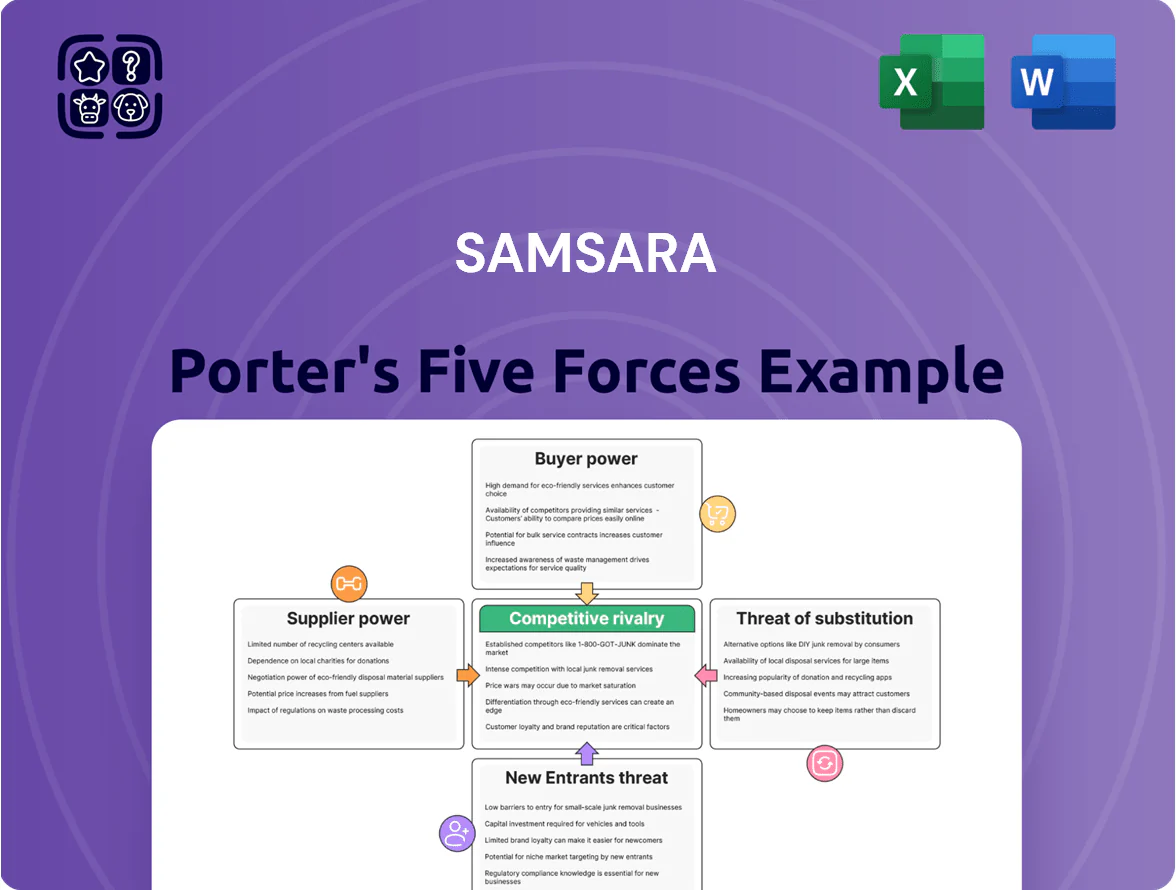

Samsara operates in a rapidly evolving telematics and IoT fleet market where intense rivalry, strong buyer bargaining, and platform-dependent suppliers shape margins and growth prospects; regulatory shifts and tech substitutes add nuanced threats and opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Samsara’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Semiconductor Manufacturers

Samsara depends on specialized chipsets and sensors for its hardware and AI gateways, and a concentrated supplier base gives those vendors moderate bargaining power. By late 2025 global chip supply normalized, yet Samsara still faces price swings—AI processor spot prices rose ~18% YoY in 2025—and 12–24 week lead times for cutting‑edge chips. This supplier leverage matters most for real‑time video analytics processors, where switching costs and qualification time are high.

Cloud Infrastructure and Hosting Costs

Samsara runs largely on AWS and Azure for real-time telematics and video, so suppliers hold strong leverage: in 2024 AWS and Azure together had ~61% global cloud IaaS share, making migration costly and complex for Samsara’s multi-petabyte datasets.

Higher egress and compute tiers can squeeze gross margins; Samsara reported 2024 gross margin ~62%, so a 5–10% cloud price shift could cut margins materially unless offset by efficiency or contract discounts.

Cellular Connectivity Providers

Contract Manufacturing Concentration

Specialized AI Software Talent

- Talent shortage: tight 2025 market

- Median senior ML pay > $300,000 (Bay Area)

- Increases R&D costs, hiring lead times

- Mitigations: retention, outsourcing, partnerships

Samsara faces supplier-driven cost and margin pressure despite mitigation levers

Samsara faces moderate‑to‑strong supplier power: concentrated chip/sensor vendors, AWS/Azure cloud (61% IaaS share 2024), major carriers for 5G/LTE, limited EMS partners, and tight ML talent (median Bay Area senior ML pay > $300,000 in 2025)—these raise costs, margin risk, and lead times; volume contracts, cloud discounts, and retention programs partly mitigate.

| Input | 2024–25 metric |

|---|---|

| Cloud share | AWS+Azure ~61% |

| AI chip price move | +18% YoY (2025) |

| ML pay | Median >$300,000 (Bay Area, 2025) |

What is included in the product

Concise Porter’s Five Forces analysis for Samsara that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Samsara that highlights competitive threats and relief strategies—ideal for quick strategic decisions.

Customers Bargaining Power

Concentration of Large Enterprise Accounts

Low Switching Costs for Small Businesses

Small fleets face low switching costs: they can move between telematics providers with little integration work, so upfront hardware and monthly fees dominate purchase decisions. In 2024 Samsara reported average revenue per customer ~2,900 USD annually; SMB churn pressure means Samsara keeps entry-level pricing and starter bundles competitive—often within a 10–20% range of rivals—to prevent churn in a segment that accounts for roughly 30% of customers.

Availability of Comparative Performance Data

By 2025, Connected Operations maturity produced abundant third-party reviews and benchmarking: Gartner, Forrester, and independent sites list Samsara alongside 8 rivals with feature-parity scores within 6–12 points and uptime claims averaging 99.95% vs Samsara’s reported 99.96% (2024 SOC reports). Buyers now use transparent metrics—NPS, MTTR, SLAs—to pit vendors at renewals, squeezing pricing and demanding tighter SLAs and blended discounts of 8–18%.

Demand for Open API and Data Portability

Customers now expect Open API access and data portability so operational data flows into ERPs and payrolls; Gartner reported 68% of enterprises prioritized API-first integrations in 2024.

This reduces Samsara’s lock-in from proprietary silos and raises churn risk as clients integrate multiple vendors; Samsara disclosed 2024 net dollar retention of ~110%, showing some resilience but vulnerability.

As portability becomes standard, bargaining power shifts to buyers who can mix vendors easily, pressuring pricing and contract terms.

- 68% of enterprises prioritize API-first (Gartner 2024)

- Samsara NDR ≈110% (2024)

- Less vendor lock-in → higher buyer leverage

Internal Development Capabilities

A subset of large, tech-forward fleets (enterprises with 1,000+ vehicles) may build lightweight, proprietary tracking tools for specific workflows, reducing spend on Samsara basic modules.

Building a full AI platform remains hard and costly—enterprise in-house telemetry teams average $2–4M annual run rates—so customers typically only insource simpler functions, capping Samsara’s pricing on basic services.

To preserve premium pricing, Samsara must keep innovating—adding AI-driven safety, predictive maintenance, and integrated telematics—features that exceed what bespoke internal tools can cost-effectively deliver.

- Large fleets (1,000+ units) may insource basics

- In-house AI/platform run rates ~$2–4M/year

- Insourcing caps Samsara pricing on basic tiers

- Continuous innovation required to protect premium pricing

Pricing Pressure: Enterprises Demand Customization, SMBs Threaten Churn — AI Must Outpace Insourcing

| Metric | Value (2024) |

|---|---|

| Enterprise ARR share | ≈40% |

| SMB customers | ≈30% |

| ARPC | $2,900 |

| Gartner API-first | 68% |

| Samsara NDR | ≈110% |

Preview the Actual Deliverable

Samsara Porter's Five Forces Analysis

This preview shows the exact Samsara Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use; no samples, no placeholders. The document displayed is the final deliverable and will be available for instant download upon payment. Use it as-is for strategy, valuation, or competitive assessment without further setup.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Samsara operates in a rapidly evolving telematics and IoT fleet market where intense rivalry, strong buyer bargaining, and platform-dependent suppliers shape margins and growth prospects; regulatory shifts and tech substitutes add nuanced threats and opportunities.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Samsara’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependency on Semiconductor Manufacturers

Samsara depends on specialized chipsets and sensors for its hardware and AI gateways, and a concentrated supplier base gives those vendors moderate bargaining power. By late 2025 global chip supply normalized, yet Samsara still faces price swings—AI processor spot prices rose ~18% YoY in 2025—and 12–24 week lead times for cutting‑edge chips. This supplier leverage matters most for real‑time video analytics processors, where switching costs and qualification time are high.

Cloud Infrastructure and Hosting Costs

Samsara runs largely on AWS and Azure for real-time telematics and video, so suppliers hold strong leverage: in 2024 AWS and Azure together had ~61% global cloud IaaS share, making migration costly and complex for Samsara’s multi-petabyte datasets.

Higher egress and compute tiers can squeeze gross margins; Samsara reported 2024 gross margin ~62%, so a 5–10% cloud price shift could cut margins materially unless offset by efficiency or contract discounts.

Cellular Connectivity Providers

Contract Manufacturing Concentration

Specialized AI Software Talent

- Talent shortage: tight 2025 market

- Median senior ML pay > $300,000 (Bay Area)

- Increases R&D costs, hiring lead times

- Mitigations: retention, outsourcing, partnerships

Samsara faces supplier-driven cost and margin pressure despite mitigation levers

Samsara faces moderate‑to‑strong supplier power: concentrated chip/sensor vendors, AWS/Azure cloud (61% IaaS share 2024), major carriers for 5G/LTE, limited EMS partners, and tight ML talent (median Bay Area senior ML pay > $300,000 in 2025)—these raise costs, margin risk, and lead times; volume contracts, cloud discounts, and retention programs partly mitigate.

| Input | 2024–25 metric |

|---|---|

| Cloud share | AWS+Azure ~61% |

| AI chip price move | +18% YoY (2025) |

| ML pay | Median >$300,000 (Bay Area, 2025) |

What is included in the product

Concise Porter’s Five Forces analysis for Samsara that uncovers competitive drivers, buyer and supplier power, entry barriers, substitute threats, and strategic implications to inform investor materials and internal strategy.

A concise Porter's Five Forces snapshot for Samsara that highlights competitive threats and relief strategies—ideal for quick strategic decisions.

Customers Bargaining Power

Concentration of Large Enterprise Accounts

Low Switching Costs for Small Businesses

Small fleets face low switching costs: they can move between telematics providers with little integration work, so upfront hardware and monthly fees dominate purchase decisions. In 2024 Samsara reported average revenue per customer ~2,900 USD annually; SMB churn pressure means Samsara keeps entry-level pricing and starter bundles competitive—often within a 10–20% range of rivals—to prevent churn in a segment that accounts for roughly 30% of customers.

Availability of Comparative Performance Data

By 2025, Connected Operations maturity produced abundant third-party reviews and benchmarking: Gartner, Forrester, and independent sites list Samsara alongside 8 rivals with feature-parity scores within 6–12 points and uptime claims averaging 99.95% vs Samsara’s reported 99.96% (2024 SOC reports). Buyers now use transparent metrics—NPS, MTTR, SLAs—to pit vendors at renewals, squeezing pricing and demanding tighter SLAs and blended discounts of 8–18%.

Demand for Open API and Data Portability

Customers now expect Open API access and data portability so operational data flows into ERPs and payrolls; Gartner reported 68% of enterprises prioritized API-first integrations in 2024.

This reduces Samsara’s lock-in from proprietary silos and raises churn risk as clients integrate multiple vendors; Samsara disclosed 2024 net dollar retention of ~110%, showing some resilience but vulnerability.

As portability becomes standard, bargaining power shifts to buyers who can mix vendors easily, pressuring pricing and contract terms.

- 68% of enterprises prioritize API-first (Gartner 2024)

- Samsara NDR ≈110% (2024)

- Less vendor lock-in → higher buyer leverage

Internal Development Capabilities

A subset of large, tech-forward fleets (enterprises with 1,000+ vehicles) may build lightweight, proprietary tracking tools for specific workflows, reducing spend on Samsara basic modules.

Building a full AI platform remains hard and costly—enterprise in-house telemetry teams average $2–4M annual run rates—so customers typically only insource simpler functions, capping Samsara’s pricing on basic services.

To preserve premium pricing, Samsara must keep innovating—adding AI-driven safety, predictive maintenance, and integrated telematics—features that exceed what bespoke internal tools can cost-effectively deliver.

- Large fleets (1,000+ units) may insource basics

- In-house AI/platform run rates ~$2–4M/year

- Insourcing caps Samsara pricing on basic tiers

- Continuous innovation required to protect premium pricing

Pricing Pressure: Enterprises Demand Customization, SMBs Threaten Churn — AI Must Outpace Insourcing

| Metric | Value (2024) |

|---|---|

| Enterprise ARR share | ≈40% |

| SMB customers | ≈30% |

| ARPC | $2,900 |

| Gartner API-first | 68% |

| Samsara NDR | ≈110% |

Preview the Actual Deliverable

Samsara Porter's Five Forces Analysis

This preview shows the exact Samsara Porter’s Five Forces analysis you’ll receive immediately after purchase—fully formatted, professionally written, and ready for use; no samples, no placeholders. The document displayed is the final deliverable and will be available for instant download upon payment. Use it as-is for strategy, valuation, or competitive assessment without further setup.