Samsung SDI Co Business Model Canvas

Samsung SDI Business Model Canvas: EV Battery Leadership, Partnerships & Growth

Unlock the full strategic blueprint behind Samsung SDI Co’s business model—this concise Business Model Canvas highlights its EV battery leadership, key partnerships, technology-driven value propositions, and diversified revenue streams to help you assess competitive positioning and growth levers.

Partnerships

Strategic Automotive Joint Ventures

Samsung SDI formed large joint ventures with automakers including Stellantis and General Motors—notably StarPlus Energy—committing to build North American battery plants that secure long-term offtake and split upfront capex (estimated $4–6 billion per major plant).

By end-2025 these JV plants produce >40 GWh combined capacity locally, meeting regional content rules and supporting projected EV demand growth of ~25% CAGR in North America through 2030.

Upstream Material Suppliers

Samsung SDI secures high-nickel cathode and anode supply through deep-tier partners like EcoPro BM, using multi-year volume contracts that hedged roughly 60–70% of lithium and nickel exposure in 2024 to limit price volatility; these deals underpin PRiMX battery performance and helped Samsung SDI meet a 2024 EV battery shipment target of ~6 GWh while improving supply resilience.

Samsung Group Ecosystem

As part of Samsung Group, Samsung SDI works closely with Samsung Electronics and Samsung Electro-Mechanics to co-develop cells tuned for next-gen smartphones and wearables, enabling a 20% faster prototype-to-production cycle reported in 2024 and contributing to SDI’s 2024 battery sales of KRW 5.1 trillion; group-wide buying power and logistics reduce component costs and cut lead times versus independent rivals.

Battery Recycling Alliances

Samsung SDI partners with specialized recyclers to recover cobalt, nickel and lithium from end-of-life batteries, closing the loop and cutting reliance on virgin mining; by 2025 recycled material targets help meet EU and US recycled-content rules and lower Scope 3 emissions.

- Recovered metals reduce raw-material spend and supply risk

- 2024 pilot yields ~10–15% of battery-grade nickel from feedstock

- Alliances support compliance with 2025 recycled-content regulations

Academic and Research Institutions

Samsung SDI partners with top universities and global labs on long-term solid-state battery R&D, targeting solid electrolyte stability and lithium metal anode safety to keep a competitive lead; joint projects accounted for an estimated 18% of external R&D spend in 2024 (≈KRW 120bn of KRW 670bn total R&D).

Outsourcing fundamental research to academia speeds innovation and reduces internal R&D risk, enabling Samsung SDI to shorten lab-to-pilot timelines by about 20% in recent projects.

- Long-term collaborations with top-tier universities and global labs

- Focus: solid electrolytes and lithium metal anodes

- ~18% of external R&D spend in 2024 (≈KRW 120bn)

- Reduces internal R&D risk, cuts lab-to-pilot time ~20%

Samsung SDI scales NA capacity >40GWh, 60–70% hedged inputs, +20% P→P speed

Samsung SDI relies on JV automaker partners (Stellantis, GM/StarPlus) for >40 GWh North America capacity by 2025, multi-year buys with EcoPro BM hedging ~60–70% of 2024 lithium/nickel exposure, group co-development with Samsung Electronics boosting prototype-to-production speed ~20%, recycling pilots yielding 10–15% battery-grade nickel (2024), and ~KRW120bn external R&D (18% of R&D) for solid-state work.

| Partnership | Key metric | 2024–25 figure |

|---|---|---|

| JV automakers | NA capacity by 2025 | >40 GWh |

| Raw-material partners | Hedged exposure | 60–70% |

| Samsung Group | Faster P→P cycle | +20% |

| Recycling pilots | Nickel yield | 10–15% |

| Academic R&D | External R&D spend | KRW 120bn (18%) |

What is included in the product

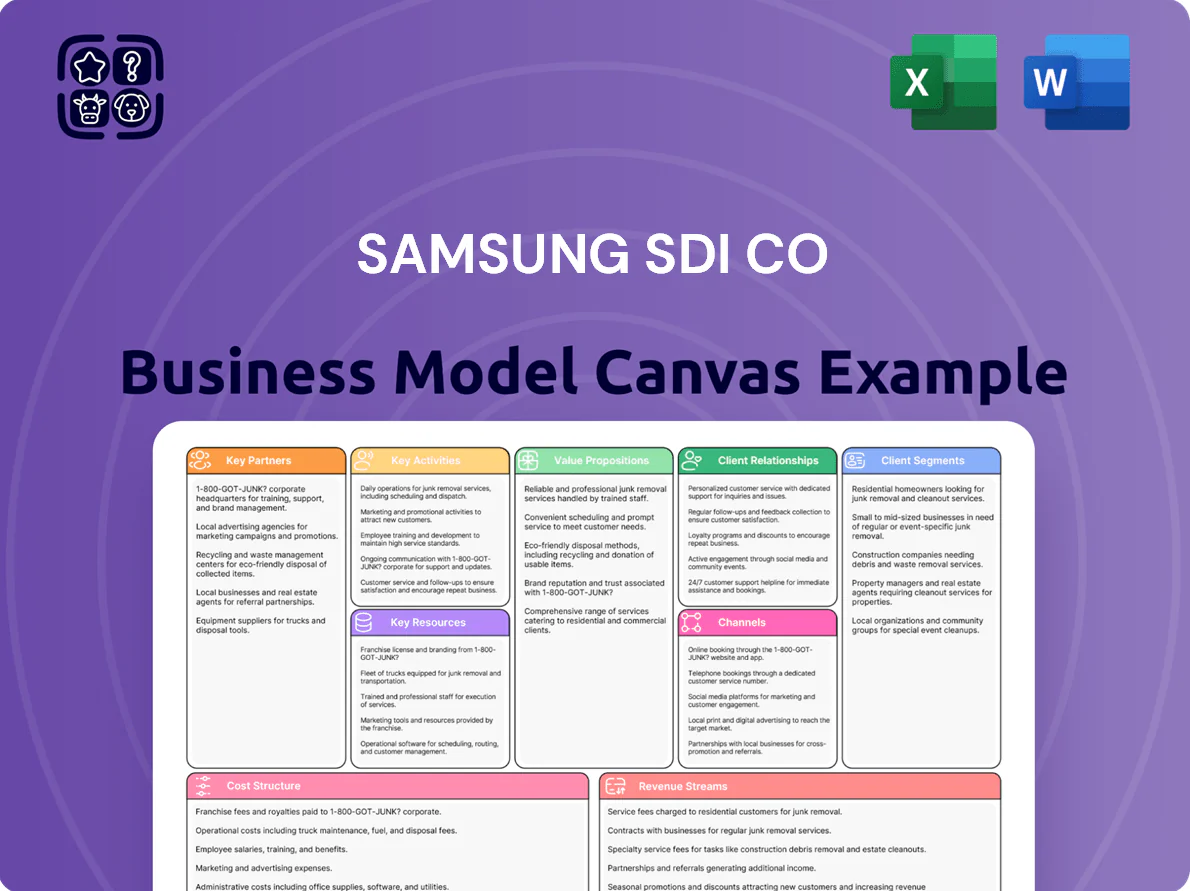

A comprehensive, pre-written Business Model Canvas for Samsung SDI detailing customer segments, channels, and value propositions across energy storage systems and advanced materials, reflecting real-world operations and strategic plans; organized into 9 BMC blocks with competitive advantage analysis, SWOT linkage, and investor-ready narrative to inform decisions and support presentations.

High-level view of Samsung SDI Co’s business model with editable cells to quickly pinpoint battery segment strengths, supply-chain risks, and growth levers for strategy meetings or investor briefs.

Activities

Advanced R and D for Next-Gen Cells

Large Scale Automated Manufacturing

Samsung SDI runs highly automated lines in South Korea, China, Hungary and the US producing prismatic and cylindrical cells; in 2025 its battery division reported 24% YoY production volume growth to support 22 GWh of announced annual capacity. The firm uses AI-driven visual inspection and process control to lift yield rates above 98% and cut defect-related costs, enabling the scale-based unit-cost reductions needed to compete globally.

Supply Chain and Mineral Sourcing

Samsung SDI actively manages a global supply chain to secure ethically sourced lithium, cobalt, and nickel, auditing suppliers for environmental and social governance (ESG) and human rights compliance across more than 20 sourcing countries; in 2024 the company reported supplier audits covering 85% of critical-material spend. Strategic sourcing reduced raw-material cost volatility, helping protect gross margin—nickel and lithium price swings in 2023–24 cut industry margins by ~6–9%, which Samsung SDI mitigated via multi-sourcing and long-term contracts.

Quality Assurance and Safety Testing

Samsung SDI embeds extensive safety protocols in production to prevent thermal runaway and extend cycle life; in 2024 its safety-related R&D spend was reported around KRW 300 billion, reflecting heavy investment in prevention and longevity.

Cells undergo extreme stress tests—nail penetration, overcharge, and 150°C exposure—to validate durability for automotive and ESS clients; these QA steps support a safety-first reputation that helps secure contracts with OEMs and utilities.

- R&D safety spend ~KRW 300 billion (2024)

- Tests: nail penetration, overcharge, 150°C exposure

- Targets: automotive, energy storage systems (ESS)

- Outcome: fewer field failures, stronger OEM contracts

Market Analysis and Strategic Planning

Samsung SDI monitors global rules like the 2022 US Inflation Reduction Act and EU battery passport, and shifted planned capacity to U.S. and EU sites to chase up to 30% tax credits and avoid market access barriers.

This planning aligns 2025 capacity expansions with OEM demand—targeting a 20–25 GWh mix for EV clients and preserving R&D spend at ~KRW 900 billion to meet regional specs.

- Captures up to 30% IRA credits in US

- Aligns 20–25 GWh EV-focused capacity by 2025

- Maintains KRW 900 billion R&D (2024–25)

Samsung SDI scales to 22GWh, targets 5GWh solid‑state, 98%+ yield, KRW 1.5T R&D/safety

Samsung SDI runs global automated cell lines (KR, CN, HU, US) scaling EV/ESS capacity to ~22 GWh (2025) with R&D ~KRW 1.2T (2024) and safety R&D ~KRW 300B; targets 5 GWh solid-state pilot-to-mass and CAPEX ~KRW 700B (2026), 98%+ yield via AI inspection, supplier audits covering 85% critical spend, and IRA-driven site shifts to capture up to 30% credits.

| Metric | Value |

|---|---|

| 2025 capacity | 22 GWh |

| Solid-state target | 5 GWh (2026 ramp) |

| R&D (2024) | KRW 1.2T |

| Safety R&D (2024) | KRW 300B |

| Yield | 98%+ |

| Supplier audit coverage | 85% |

| Planned CAPEX (2026) | KRW 700B |

| IRA credit capture | Up to 30% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Samsung SDI Co. Business Model Canvas you will receive—no mockups or samples—formatted and ready to use for strategic analysis and presentation.

Upon purchase, you’ll instantly download the full file in the same structure and layout shown here, editable for Word and Excel to tailor to your needs.

We value transparency: what you see is the final deliverable, complete and ready for immediate application.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Samsung SDI Business Model Canvas: EV Battery Leadership, Partnerships & Growth

Unlock the full strategic blueprint behind Samsung SDI Co’s business model—this concise Business Model Canvas highlights its EV battery leadership, key partnerships, technology-driven value propositions, and diversified revenue streams to help you assess competitive positioning and growth levers.

Partnerships

Strategic Automotive Joint Ventures

Samsung SDI formed large joint ventures with automakers including Stellantis and General Motors—notably StarPlus Energy—committing to build North American battery plants that secure long-term offtake and split upfront capex (estimated $4–6 billion per major plant).

By end-2025 these JV plants produce >40 GWh combined capacity locally, meeting regional content rules and supporting projected EV demand growth of ~25% CAGR in North America through 2030.

Upstream Material Suppliers

Samsung SDI secures high-nickel cathode and anode supply through deep-tier partners like EcoPro BM, using multi-year volume contracts that hedged roughly 60–70% of lithium and nickel exposure in 2024 to limit price volatility; these deals underpin PRiMX battery performance and helped Samsung SDI meet a 2024 EV battery shipment target of ~6 GWh while improving supply resilience.

Samsung Group Ecosystem

As part of Samsung Group, Samsung SDI works closely with Samsung Electronics and Samsung Electro-Mechanics to co-develop cells tuned for next-gen smartphones and wearables, enabling a 20% faster prototype-to-production cycle reported in 2024 and contributing to SDI’s 2024 battery sales of KRW 5.1 trillion; group-wide buying power and logistics reduce component costs and cut lead times versus independent rivals.

Battery Recycling Alliances

Samsung SDI partners with specialized recyclers to recover cobalt, nickel and lithium from end-of-life batteries, closing the loop and cutting reliance on virgin mining; by 2025 recycled material targets help meet EU and US recycled-content rules and lower Scope 3 emissions.

- Recovered metals reduce raw-material spend and supply risk

- 2024 pilot yields ~10–15% of battery-grade nickel from feedstock

- Alliances support compliance with 2025 recycled-content regulations

Academic and Research Institutions

Samsung SDI partners with top universities and global labs on long-term solid-state battery R&D, targeting solid electrolyte stability and lithium metal anode safety to keep a competitive lead; joint projects accounted for an estimated 18% of external R&D spend in 2024 (≈KRW 120bn of KRW 670bn total R&D).

Outsourcing fundamental research to academia speeds innovation and reduces internal R&D risk, enabling Samsung SDI to shorten lab-to-pilot timelines by about 20% in recent projects.

- Long-term collaborations with top-tier universities and global labs

- Focus: solid electrolytes and lithium metal anodes

- ~18% of external R&D spend in 2024 (≈KRW 120bn)

- Reduces internal R&D risk, cuts lab-to-pilot time ~20%

Samsung SDI scales NA capacity >40GWh, 60–70% hedged inputs, +20% P→P speed

Samsung SDI relies on JV automaker partners (Stellantis, GM/StarPlus) for >40 GWh North America capacity by 2025, multi-year buys with EcoPro BM hedging ~60–70% of 2024 lithium/nickel exposure, group co-development with Samsung Electronics boosting prototype-to-production speed ~20%, recycling pilots yielding 10–15% battery-grade nickel (2024), and ~KRW120bn external R&D (18% of R&D) for solid-state work.

| Partnership | Key metric | 2024–25 figure |

|---|---|---|

| JV automakers | NA capacity by 2025 | >40 GWh |

| Raw-material partners | Hedged exposure | 60–70% |

| Samsung Group | Faster P→P cycle | +20% |

| Recycling pilots | Nickel yield | 10–15% |

| Academic R&D | External R&D spend | KRW 120bn (18%) |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Samsung SDI detailing customer segments, channels, and value propositions across energy storage systems and advanced materials, reflecting real-world operations and strategic plans; organized into 9 BMC blocks with competitive advantage analysis, SWOT linkage, and investor-ready narrative to inform decisions and support presentations.

High-level view of Samsung SDI Co’s business model with editable cells to quickly pinpoint battery segment strengths, supply-chain risks, and growth levers for strategy meetings or investor briefs.

Activities

Advanced R and D for Next-Gen Cells

Large Scale Automated Manufacturing

Samsung SDI runs highly automated lines in South Korea, China, Hungary and the US producing prismatic and cylindrical cells; in 2025 its battery division reported 24% YoY production volume growth to support 22 GWh of announced annual capacity. The firm uses AI-driven visual inspection and process control to lift yield rates above 98% and cut defect-related costs, enabling the scale-based unit-cost reductions needed to compete globally.

Supply Chain and Mineral Sourcing

Samsung SDI actively manages a global supply chain to secure ethically sourced lithium, cobalt, and nickel, auditing suppliers for environmental and social governance (ESG) and human rights compliance across more than 20 sourcing countries; in 2024 the company reported supplier audits covering 85% of critical-material spend. Strategic sourcing reduced raw-material cost volatility, helping protect gross margin—nickel and lithium price swings in 2023–24 cut industry margins by ~6–9%, which Samsung SDI mitigated via multi-sourcing and long-term contracts.

Quality Assurance and Safety Testing

Samsung SDI embeds extensive safety protocols in production to prevent thermal runaway and extend cycle life; in 2024 its safety-related R&D spend was reported around KRW 300 billion, reflecting heavy investment in prevention and longevity.

Cells undergo extreme stress tests—nail penetration, overcharge, and 150°C exposure—to validate durability for automotive and ESS clients; these QA steps support a safety-first reputation that helps secure contracts with OEMs and utilities.

- R&D safety spend ~KRW 300 billion (2024)

- Tests: nail penetration, overcharge, 150°C exposure

- Targets: automotive, energy storage systems (ESS)

- Outcome: fewer field failures, stronger OEM contracts

Market Analysis and Strategic Planning

Samsung SDI monitors global rules like the 2022 US Inflation Reduction Act and EU battery passport, and shifted planned capacity to U.S. and EU sites to chase up to 30% tax credits and avoid market access barriers.

This planning aligns 2025 capacity expansions with OEM demand—targeting a 20–25 GWh mix for EV clients and preserving R&D spend at ~KRW 900 billion to meet regional specs.

- Captures up to 30% IRA credits in US

- Aligns 20–25 GWh EV-focused capacity by 2025

- Maintains KRW 900 billion R&D (2024–25)

Samsung SDI scales to 22GWh, targets 5GWh solid‑state, 98%+ yield, KRW 1.5T R&D/safety

Samsung SDI runs global automated cell lines (KR, CN, HU, US) scaling EV/ESS capacity to ~22 GWh (2025) with R&D ~KRW 1.2T (2024) and safety R&D ~KRW 300B; targets 5 GWh solid-state pilot-to-mass and CAPEX ~KRW 700B (2026), 98%+ yield via AI inspection, supplier audits covering 85% critical spend, and IRA-driven site shifts to capture up to 30% credits.

| Metric | Value |

|---|---|

| 2025 capacity | 22 GWh |

| Solid-state target | 5 GWh (2026 ramp) |

| R&D (2024) | KRW 1.2T |

| Safety R&D (2024) | KRW 300B |

| Yield | 98%+ |

| Supplier audit coverage | 85% |

| Planned CAPEX (2026) | KRW 700B |

| IRA credit capture | Up to 30% |

Full Document Unlocks After Purchase

Business Model Canvas

The document you're previewing is the exact Samsung SDI Co. Business Model Canvas you will receive—no mockups or samples—formatted and ready to use for strategic analysis and presentation.

Upon purchase, you’ll instantly download the full file in the same structure and layout shown here, editable for Word and Excel to tailor to your needs.

We value transparency: what you see is the final deliverable, complete and ready for immediate application.