Samyang Boston Consulting Group Matrix

Actionable Strategy Starts Here

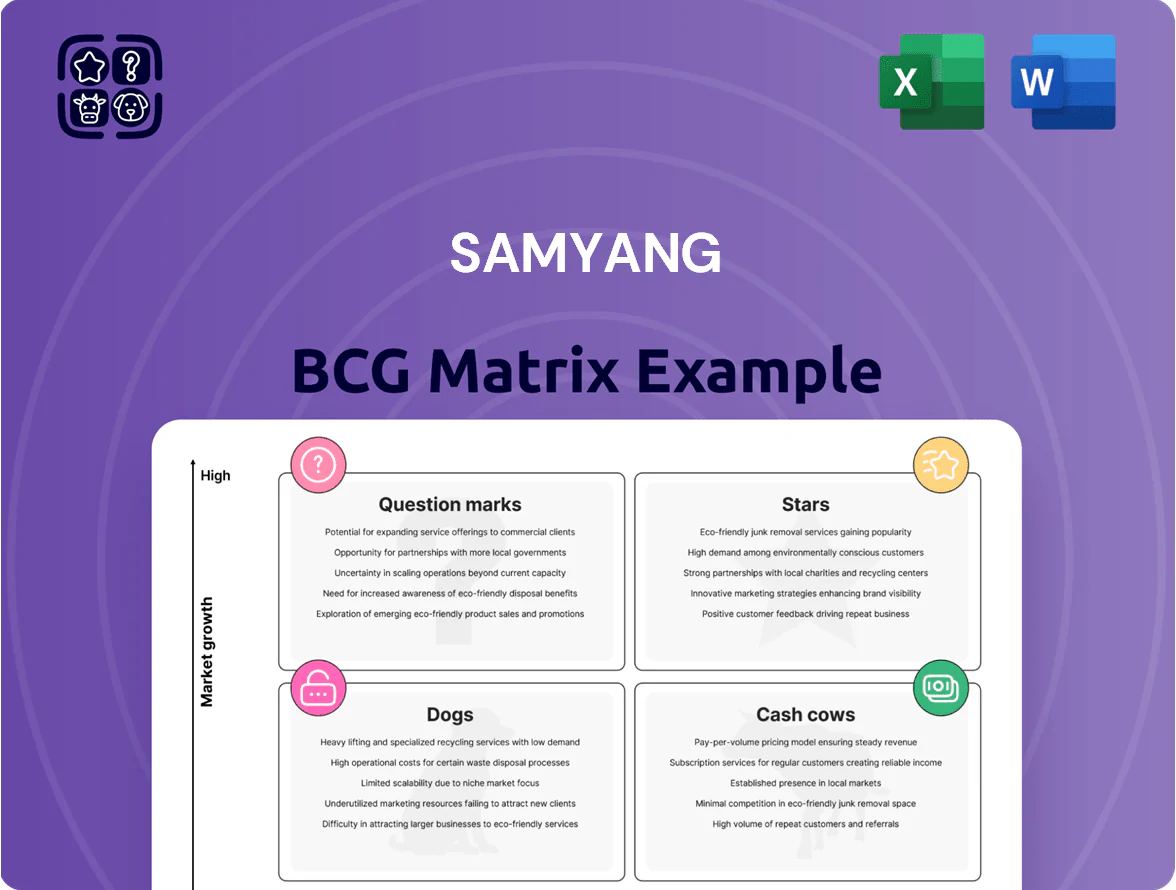

Samyang’s BCG Matrix preview highlights how its flagship products perform across market share and growth—revealing emerging Stars, steady Cash Cows, and potential Question Marks that warrant attention. This snapshot teases where resources are best deployed but stops short of granular guidance. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed strategic moves, and ready-to-use Word and Excel files that let you act with confidence.

Stars

Bio-based Isosorbide Materials

Samyang leads global isosorbide production, supplying ~40% of commercial capacity and growing volumes to 85 kt/year after 2024 expansions; isosorbide is used in biodegradable PLA blends and high‑Tg polycarbonates.

Tighter single‑use plastic rules through late 2025 (EU SUP Directive extensions, 2024–25 national bans) push segment CAGR to ~18% (2023–2026); Samyang reports 2025 isosorbide sales up 32% YoY.

Samyang is reinvesting ~KRW 200 billion (2023–2026 capex) to add 40 ktpa capacity, keeping margins above 16% on premium bio‑polymer grades and defending market share.

Allulose and Next-Generation Sweeteners

Samyang’s Allulose is a Star: global sugar-reduction demand grew 9.8% CAGR 2019–2024, pushing Allulose to ~18% share of the specialty sweetener market in 2024 and revenue of KRW 72bn (2024).

The unit uses proprietary enzyme tech that cut production costs ~28% vs peers, enabling scalable output of 6,500 tonnes/year capacity as of Q3 2025.

Samyang is investing KRW 45bn in 2025 CAPEX for global distribution and marketing to defend leadership and chase 25% market share by 2027.

EV Battery Thermal Management Materials

Samyang’s engineering plastics for EV battery housings and thermal management—used in >1.5M EVs globally in 2024—are Stars in the BCG matrix due to high heat resistance (service temps >200°C) and low density (≈1.3 g/cm3), supporting 8–12% lighter packs and improving range by ~3–5% in partner vehicles.

Advanced Drug Delivery Systems

Samyang's biopharma SENS-N polymeric micelle platform is a Star: oncology revenues rose 38% in 2025 to KRW 120 billion, driven by three Phase II programs and partnerships in the US and EU.

Micelle tech boosts drug solubility and lowers toxicity, improving response rates by ~15–25% in early trials; ongoing spend: KRW 45 billion in 2025 on trials and regulatory work.

To stay a Star, Samyang must keep investing in late‑stage trials and global approvals; failure to scale trials or win approvals would slow market capture and ROI.

- 2025 oncology revenue KRW 120B

- Revenue growth 38% YoY

- Trial/regulatory spend KRW 45B in 2025

- Early trial response lift ~15–25%

High-Performance Polycarbonate Compounds

High-performance polycarbonate compounds are a Stars category: demand in electronics and automotive rose ~7% CAGR 2020–2024, driven by miniaturization and durability; Samyang holds ~22% niche market share in 2024, above its 12% share in general-purpose plastics.

Samyang is investing $35M in 2025 to scale recycled/sustainable grades to meet Tier 1 electronics ESG specs, aiming for 30% recycled content by 2027.

- 2024 niche growth ~7% CAGR

- Samyang niche share ~22% (2024)

- $35M capex planned in 2025

- Target 30% recycled content by 2027

Samyang surge: isosorbide scale, allulose growth, EV plastics & SENS‑N lift margins

Samyang Stars: isosorbide (40% supply, 85 ktpa post‑2024; 32% sales rise in 2025), allulose (6.5 ktpa capacity Q3‑2025; KRW 72bn revenue 2024), EV plastics (>1.5M EVs 2024; saves 8–12% mass), SENS‑N (oncology KRW 120bn 2025; +38% YoY). Continued KRW 290bn capex (2023–2026) targets share gains and margin >16%.

| Product | Key metric | 2024–25 |

|---|---|---|

| Isosorbide | Capacity | 85 ktpa |

| Allulose | Revenue | KRW 72bn |

| SENS‑N | Revenue | KRW 120bn |

What is included in the product

Comprehensive BCG assessment of Samyang’s portfolio with quadrant-specific strategies, investment priorities, and trend-driven risks and opportunities.

One-page Samyang BCG Matrix mapping each product by market share and growth for fast strategic decisions.

Cash Cows

Qone Refined Sugar Market Leadership

Qone holds a 52% share of South Korea's refined sugar market as of 2025, remaining the clear market leader in a segment growing <1% annually; stable volume and pricing produced KRW 85 billion in operating cash flow in FY2024 with marketing spend under 3% of revenue.

PET Preform and Packaging Solutions

Samyang's PET preform and packaging unit is a cash cow, supplying roughly 30% of South Korea's beverage container market and generating stable annual revenue near KRW 220 billion in 2024.

The domestic PET bottle market is mature, with flat 1–2% annual volume growth and gross margins around 18–22%, delivering predictable free cash flow for Samyang.

Ongoing capex-light efficiency gains—20% lower energy use per ton since 2019 and logistics optimizations cutting distribution cost 12%—have raised operating cash conversion and maximized cash yield from this established business.

Flour and Grain Milling Operations

The flour and grain milling division delivers steady revenue—about KRW 350 billion in 2024, roughly 18% of Samyang Group’s consolidated sales—supplying industrial bakers and retail channels with staples like wheat flour and cornmeal.

Market growth is under 3% annually and high capital, scale, and grain sourcing barriers protect Samyang’s share, keeping price competition muted.

It behaves as a cash cow: low capex (≈2–3% of division sales) and stable margins fund corporate debt service—Samyang’s net debt/EBITDA fell to 1.8x in 2024—providing reliable liquidity.

Standard Polycarbonate Resins

Standard polycarbonate resins at Samyang are a mature cash cow, generating steady EBITDA margins around 18–22% in 2024 on volume sales of ~240 ktpa, supported by long-term supply contracts with automotive and electronics firms.

With plant utilization at ~88% and scale advantages, management prioritizes cost cuts (energy down 6% YoY) and capital efficiency to sustain margins in a low-growth commodity market.

- ~240 ktpa output

- EBITDA 18–22% (2024)

- Utilization ~88%

- Energy costs down 6% YoY

- Focus: cost optimization & asset utilization

Industrial Starch and Sweeteners

Samyang’s Industrial Starch and Sweeteners unit is a cash cow: corn-based starch and sucrose products lead the food and paper markets with ~25% domestic share and stable EBITDA margins near 18% in 2025, despite market growth under 2% annually.

Long-term supply-chain scale and 12% lower per-ton production costs versus peers sustain high cash flow, which funds R&D into high-value functional ingredients; ~KRW 40 billion redirected in 2024.

- Market share ~25% (2025)

- EBITDA margin ~18% (2025)

- Market growth <2% CAGR

- 2024 R&D funding ~KRW 40 billion

- Per-ton cost ~12% below peers

Diversified cash cows: PET, Qone sugar, flour, PC resin & starch driving strong margins

Cash cows: PET preforms (KRW 220b rev 2024, 30% market), refined sugar Qone (52% share, KRW 85b OCF 2024), flour milling (KRW 350b rev 2024, 18% group sales), polycarbonate (240 ktpa, EBITDA 18–22%), starch & sweeteners (25% share, EBITDA ~18%, KRW 40b R&D 2024).

| Unit | Key metric (2024/25) |

|---|---|

| PET | KRW 220b, 30% market |

| Qone sugar | 52% share, KRW 85b OCF |

| Flour | KRW 350b, 18% sales |

| PC resin | 240 ktpa, EBITDA 18–22% |

| Starch | 25% share, EBITDA ~18% |

What You’re Viewing Is Included

Samyang BCG Matrix

The file you're previewing on this page is the final Samyang BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a professionally formatted, strategy-ready report for immediate use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Actionable Strategy Starts Here

Samyang’s BCG Matrix preview highlights how its flagship products perform across market share and growth—revealing emerging Stars, steady Cash Cows, and potential Question Marks that warrant attention. This snapshot teases where resources are best deployed but stops short of granular guidance. Purchase the full BCG Matrix to get quadrant-by-quadrant placements, data-backed strategic moves, and ready-to-use Word and Excel files that let you act with confidence.

Stars

Bio-based Isosorbide Materials

Samyang leads global isosorbide production, supplying ~40% of commercial capacity and growing volumes to 85 kt/year after 2024 expansions; isosorbide is used in biodegradable PLA blends and high‑Tg polycarbonates.

Tighter single‑use plastic rules through late 2025 (EU SUP Directive extensions, 2024–25 national bans) push segment CAGR to ~18% (2023–2026); Samyang reports 2025 isosorbide sales up 32% YoY.

Samyang is reinvesting ~KRW 200 billion (2023–2026 capex) to add 40 ktpa capacity, keeping margins above 16% on premium bio‑polymer grades and defending market share.

Allulose and Next-Generation Sweeteners

Samyang’s Allulose is a Star: global sugar-reduction demand grew 9.8% CAGR 2019–2024, pushing Allulose to ~18% share of the specialty sweetener market in 2024 and revenue of KRW 72bn (2024).

The unit uses proprietary enzyme tech that cut production costs ~28% vs peers, enabling scalable output of 6,500 tonnes/year capacity as of Q3 2025.

Samyang is investing KRW 45bn in 2025 CAPEX for global distribution and marketing to defend leadership and chase 25% market share by 2027.

EV Battery Thermal Management Materials

Samyang’s engineering plastics for EV battery housings and thermal management—used in >1.5M EVs globally in 2024—are Stars in the BCG matrix due to high heat resistance (service temps >200°C) and low density (≈1.3 g/cm3), supporting 8–12% lighter packs and improving range by ~3–5% in partner vehicles.

Advanced Drug Delivery Systems

Samyang's biopharma SENS-N polymeric micelle platform is a Star: oncology revenues rose 38% in 2025 to KRW 120 billion, driven by three Phase II programs and partnerships in the US and EU.

Micelle tech boosts drug solubility and lowers toxicity, improving response rates by ~15–25% in early trials; ongoing spend: KRW 45 billion in 2025 on trials and regulatory work.

To stay a Star, Samyang must keep investing in late‑stage trials and global approvals; failure to scale trials or win approvals would slow market capture and ROI.

- 2025 oncology revenue KRW 120B

- Revenue growth 38% YoY

- Trial/regulatory spend KRW 45B in 2025

- Early trial response lift ~15–25%

High-Performance Polycarbonate Compounds

High-performance polycarbonate compounds are a Stars category: demand in electronics and automotive rose ~7% CAGR 2020–2024, driven by miniaturization and durability; Samyang holds ~22% niche market share in 2024, above its 12% share in general-purpose plastics.

Samyang is investing $35M in 2025 to scale recycled/sustainable grades to meet Tier 1 electronics ESG specs, aiming for 30% recycled content by 2027.

- 2024 niche growth ~7% CAGR

- Samyang niche share ~22% (2024)

- $35M capex planned in 2025

- Target 30% recycled content by 2027

Samyang surge: isosorbide scale, allulose growth, EV plastics & SENS‑N lift margins

Samyang Stars: isosorbide (40% supply, 85 ktpa post‑2024; 32% sales rise in 2025), allulose (6.5 ktpa capacity Q3‑2025; KRW 72bn revenue 2024), EV plastics (>1.5M EVs 2024; saves 8–12% mass), SENS‑N (oncology KRW 120bn 2025; +38% YoY). Continued KRW 290bn capex (2023–2026) targets share gains and margin >16%.

| Product | Key metric | 2024–25 |

|---|---|---|

| Isosorbide | Capacity | 85 ktpa |

| Allulose | Revenue | KRW 72bn |

| SENS‑N | Revenue | KRW 120bn |

What is included in the product

Comprehensive BCG assessment of Samyang’s portfolio with quadrant-specific strategies, investment priorities, and trend-driven risks and opportunities.

One-page Samyang BCG Matrix mapping each product by market share and growth for fast strategic decisions.

Cash Cows

Qone Refined Sugar Market Leadership

Qone holds a 52% share of South Korea's refined sugar market as of 2025, remaining the clear market leader in a segment growing <1% annually; stable volume and pricing produced KRW 85 billion in operating cash flow in FY2024 with marketing spend under 3% of revenue.

PET Preform and Packaging Solutions

Samyang's PET preform and packaging unit is a cash cow, supplying roughly 30% of South Korea's beverage container market and generating stable annual revenue near KRW 220 billion in 2024.

The domestic PET bottle market is mature, with flat 1–2% annual volume growth and gross margins around 18–22%, delivering predictable free cash flow for Samyang.

Ongoing capex-light efficiency gains—20% lower energy use per ton since 2019 and logistics optimizations cutting distribution cost 12%—have raised operating cash conversion and maximized cash yield from this established business.

Flour and Grain Milling Operations

The flour and grain milling division delivers steady revenue—about KRW 350 billion in 2024, roughly 18% of Samyang Group’s consolidated sales—supplying industrial bakers and retail channels with staples like wheat flour and cornmeal.

Market growth is under 3% annually and high capital, scale, and grain sourcing barriers protect Samyang’s share, keeping price competition muted.

It behaves as a cash cow: low capex (≈2–3% of division sales) and stable margins fund corporate debt service—Samyang’s net debt/EBITDA fell to 1.8x in 2024—providing reliable liquidity.

Standard Polycarbonate Resins

Standard polycarbonate resins at Samyang are a mature cash cow, generating steady EBITDA margins around 18–22% in 2024 on volume sales of ~240 ktpa, supported by long-term supply contracts with automotive and electronics firms.

With plant utilization at ~88% and scale advantages, management prioritizes cost cuts (energy down 6% YoY) and capital efficiency to sustain margins in a low-growth commodity market.

- ~240 ktpa output

- EBITDA 18–22% (2024)

- Utilization ~88%

- Energy costs down 6% YoY

- Focus: cost optimization & asset utilization

Industrial Starch and Sweeteners

Samyang’s Industrial Starch and Sweeteners unit is a cash cow: corn-based starch and sucrose products lead the food and paper markets with ~25% domestic share and stable EBITDA margins near 18% in 2025, despite market growth under 2% annually.

Long-term supply-chain scale and 12% lower per-ton production costs versus peers sustain high cash flow, which funds R&D into high-value functional ingredients; ~KRW 40 billion redirected in 2024.

- Market share ~25% (2025)

- EBITDA margin ~18% (2025)

- Market growth <2% CAGR

- 2024 R&D funding ~KRW 40 billion

- Per-ton cost ~12% below peers

Diversified cash cows: PET, Qone sugar, flour, PC resin & starch driving strong margins

Cash cows: PET preforms (KRW 220b rev 2024, 30% market), refined sugar Qone (52% share, KRW 85b OCF 2024), flour milling (KRW 350b rev 2024, 18% group sales), polycarbonate (240 ktpa, EBITDA 18–22%), starch & sweeteners (25% share, EBITDA ~18%, KRW 40b R&D 2024).

| Unit | Key metric (2024/25) |

|---|---|

| PET | KRW 220b, 30% market |

| Qone sugar | 52% share, KRW 85b OCF |

| Flour | KRW 350b, 18% sales |

| PC resin | 240 ktpa, EBITDA 18–22% |

| Starch | 25% share, EBITDA ~18% |

What You’re Viewing Is Included

Samyang BCG Matrix

The file you're previewing on this page is the final Samyang BCG Matrix you'll receive after purchase—no watermarks, no demo content, just a professionally formatted, strategy-ready report for immediate use.